Global Drip Irrigation Market Size, Share, And Enhanced Productivity By Component (Emitters and Drippers, Drip Tubes and Lines, Filters, Pressure Pumps, Valves and Fittings, Controllers and Sensors, Accessories), By Crop Type (Field Crops, Vegetable Crops, Orchard Crops, Vineyards, Others), By Application (Surface Drip Irrigation, Subsurface Drip Irrigation), By End-User (Commercial Farms, Greenhouses and Nurseries, Residential Gardens and Landscapes, Sports Fields and Golf Courses), By Sales Channel (Direct Sales, Dealer and Distributor, Online Retail), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2025-2034

- Published date: February 2026

- Report ID: 178737

- Number of Pages: 248

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

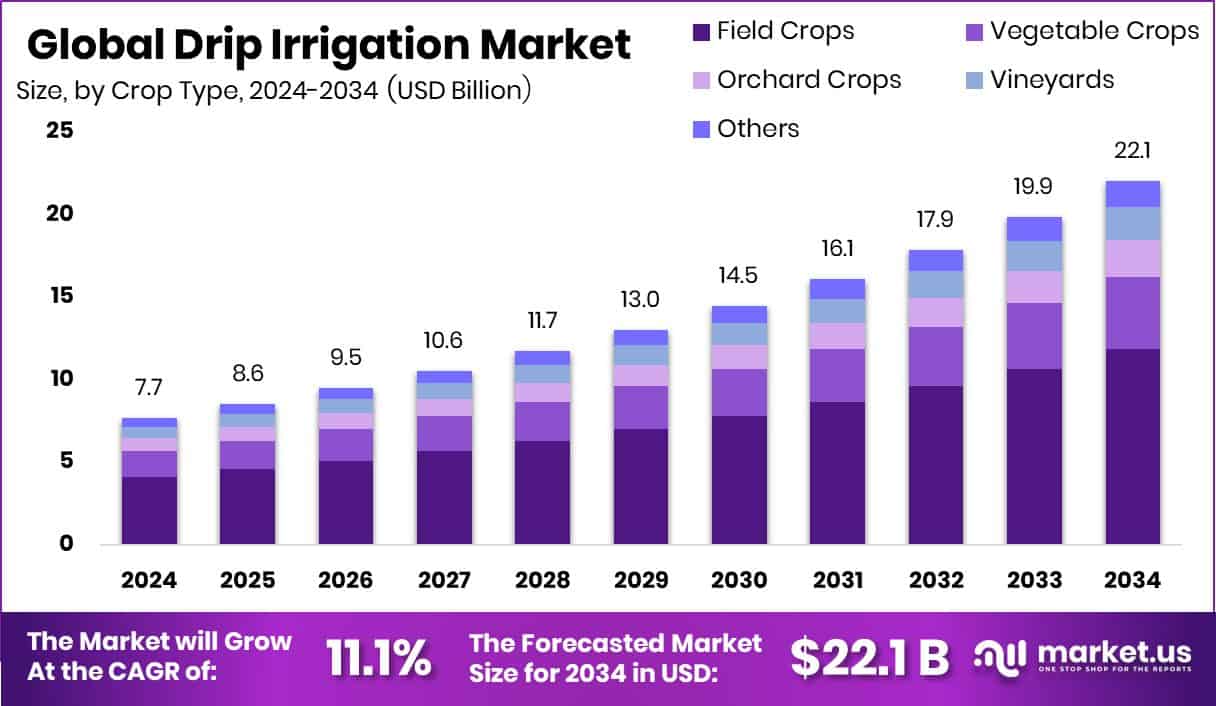

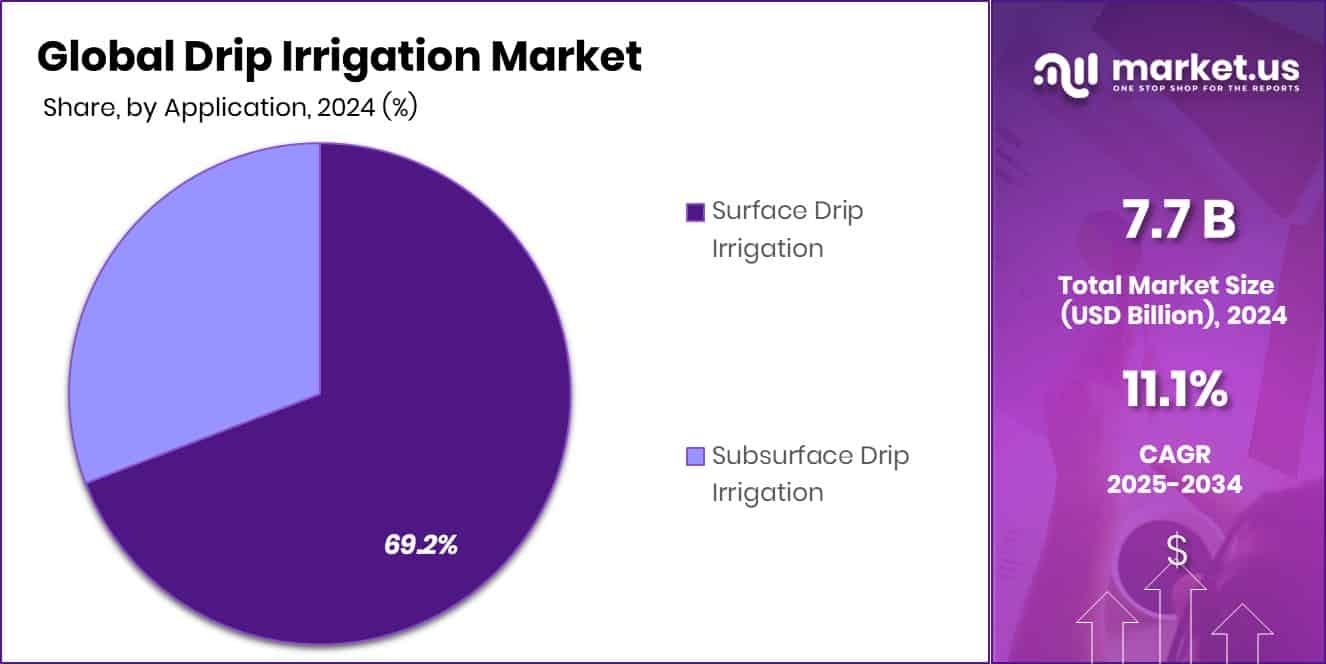

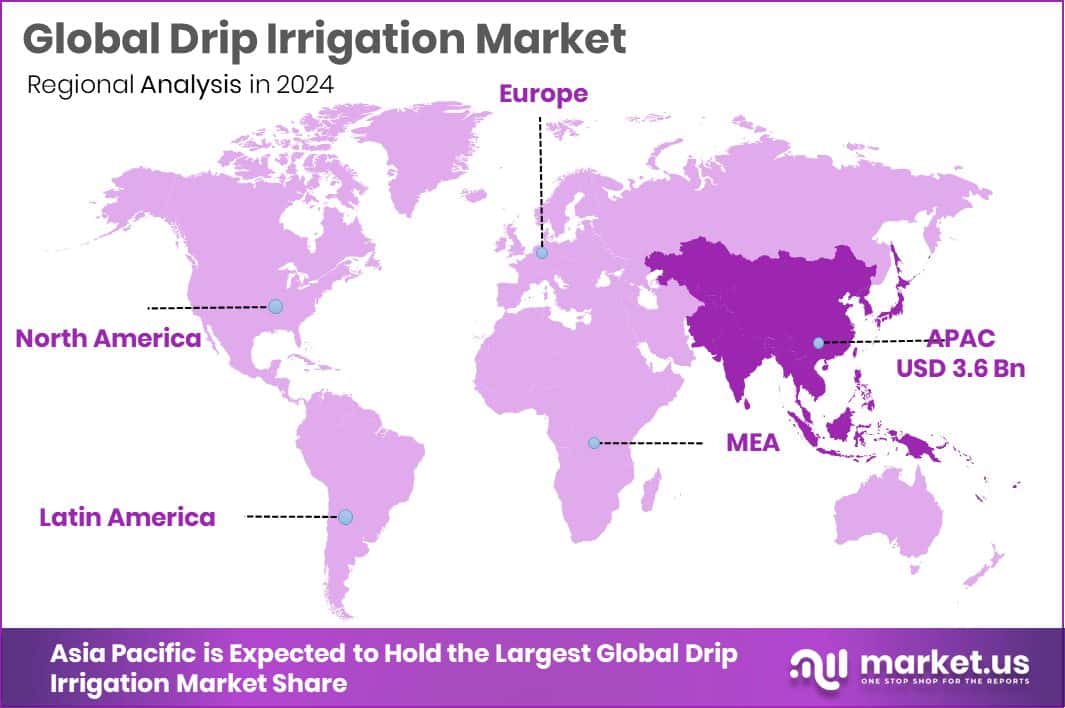

The Global Drip Irrigation Market is expected to be worth around USD 22.1 billion by 2034, up from USD 7.7 billion in 2024, and is projected to grow at a CAGR of 11.1% from 2025 to 2034. Regional demand in the Asia Pacific drove USD 3.6 Bn revenue, capturing 46.9% share overall.

The global drip irrigation market continues to grow as farmers, greenhouse operators, and residential users move toward water-efficient irrigation systems. The industry spans a wide taxonomy, including emitters and drippers, drip tubes and lines, filters, pressure pumps, valves and fittings, controllers, sensors, and accessories. Adoption is rising across field crops, vegetable farms, orchards, vineyards, and landscaping, supported by both surface and subsurface systems. Demand stems from commercial farms, nurseries, residential gardens, and sports facilities, while distribution moves through direct sales, dealer networks, and online retail.

Drip irrigation is a method of delivering water directly to plant roots through small emitters or tubes, reducing evaporation and runoff. It ensures consistent moisture levels, improves nutrient uptake, and helps farmers maintain crop health even under limited water availability.

The drip irrigation market refers to the ecosystem of products, technologies, installations, and services that support low-pressure, water-saving irrigation solutions for agriculture and landscapes. It also includes digital controllers, filtration systems, tubing networks, and soil-based monitoring that enhance precision watering.

Growth in this market is strongly influenced by increasing pressure on global water resources and the need for efficient crop production. Governments and development agencies are actively supporting the switch to modern irrigation. For instance, Moldovan farmers now receive grants of up to $7,500 to modernize irrigation systems, helping them transition from flood irrigation to controlled drip lines. Similar initiatives continue to push farmers toward water-smart solutions.

Demand is also rising in regions facing severe water stress. Recent funding—such as US $350,000 granted for water-saving drip irrigation projects in Nigeria—shows how emerging markets are turning to drip systems to secure food production. The ability to save water while improving yields is becoming a core requirement for modern agriculture.

Opportunity in this market expands further as private investors support next-generation drip technologies. N-Drip recently completed a $20 million Series B round, while large-scale financing continues to flow into infrastructure, such as $500 million allocated for drip irrigation expansion in India and China. Strengthening safety and storage systems also plays a role, supported by initiatives like the World Bank’s additional $137 million funding to enhance dam safety in India, ensuring the long-term reliability of irrigation networks. These shifts collectively create a solid foundation for market growth in the years ahead.

Key Takeaways

- The Global Drip Irrigation Market is expected to be worth around USD 22.1 billion by 2034, up from USD 7.7 billion in 2024, and is projected to grow at a CAGR of 11.1% from 2025 to 2034.

- Drip Irrigation Market sees emitters and drippers contributing significantly, accounting for a strong 39.6%.

- Drip Irrigation Market demand rises as field crops dominate usage, holding a notable 53.7% share.

- Drip Irrigation Market expands rapidly with surface drip irrigation leading applications at a substantial 69.2%.

- Drip Irrigation Market growth strengthens as commercial farms remain primary end-users, representing an impressive 59.5% share.

- Drip Irrigation Market relies heavily on dealer and distributor networks, which control 49.1% overall sales.

- Asia Pacific dominated with a 46.9% share, generating USD 3.6 Bn in market value overall regionally.

By Component Analysis

Drip Irrigation Market is dominated by emitters and drippers, holding 39.6%.

In 2024, the Drip Irrigation Market saw Emitters and Drippers dominate with a 39.6% share, reflecting strong adoption of precision water-delivery components. This dominance came from farmers needing consistent water flow, lower wastage, and improved crop uniformity, especially in water-stressed regions.

Emitters and drippers remained the backbone of modern drip systems because they help maintain exact moisture levels at the plant root zone. Their performance efficiency also encouraged commercial growers to shift from traditional flood irrigation to micro-irrigation setups. Manufacturers focused on durable, clog-resistant emitters, which further strengthened market traction. As farm sizes expand and irrigation modernization accelerates, this component category has reinforced its leadership position throughout 2024.

By Crop Type Analysis

Drip Irrigation Market field crops dominate strongly with a leading 53.7%.

In 2024, the Drip Irrigation Market was dominated by Field Crops, accounting for 53.7%, showing how large-scale farming increasingly relies on water-efficient irrigation. Crops such as maize, sugarcane, cotton, soybean, and cereals drove this demand as growers looked to improve yields while conserving water. Rising awareness of water scarcity and government incentives for micro-irrigation systems supported higher adoption in field crop plantations.

Drip lines helped farmers achieve better nutrient delivery and reduce overall input costs. The strong shift toward sustainable agriculture made field crops the largest contributor to market revenues. This segment’s scale, combined with the continuous expansion of commercial agriculture, ensured its leading share throughout the year.

By Application Analysis

Drip Irrigation Market Surface drip irrigation dominates overall applications with 69.2%.

In 2024, Surface Drip Irrigation dominated the market with a 69.2% share, making it the most widely used application method. Farmers preferred surface systems because they are easier to install, maintain, and integrate into existing crop layouts. This approach works especially well for row crops, vegetables, orchards, and plantations that demand regulated moisture without extensive labor. The lower cost of setup compared to subsurface systems helped surface drip irrigation gain traction among small and large farms alike.

Its flexibility in seasonal cropping cycles and compatibility with fertigation technologies further increased usage. As growers aimed to improve water use efficiency, surface drip irrigation remained the preferred method throughout 2024.

By End-User Analysis

Drip Irrigation Market: Commercial farms dominate adoption, capturing a substantial 59.5%.

In 2024, Commercial Farms led the Drip Irrigation Market with a 59.5% share, demonstrating their broad-scale shift toward precision irrigation. Large growers adopted drip systems to reduce water costs, enhance crop productivity, and meet sustainability standards required by buyers and exporters. The need for consistent, high-quality output motivated farms to switch from traditional irrigation practices.

Drip irrigation also helped commercial farmers optimize fertilizer use and minimize labor expenses. With commercial agriculture expanding across developing regions, investments in advanced irrigation infrastructure increased significantly. This segment’s strong focus on maximizing returns and improving farm efficiency ensured its dominant position throughout the year.

By Sales Channel Analysis

Drip Irrigation Market dealer distributor channels dominate overall sales, reaching 49.1%.

In 2024, the Dealer and Distributor channel dominated sales with a 49.1% share, remaining the primary way farmers sourced drip irrigation systems. Most growers relied on established dealer networks for product availability, installation assistance, and after-sales service. Distributors played a vital role in supplying rural markets where direct company presence is limited. Their ability to provide on-ground support, spare parts, and guided system selection contributed to this large share.

Partnerships between manufacturers and local dealers strengthened supply chains, ensuring farmers had timely access to emitters, drippers, pipes, pumps, and controllers. This strong distribution ecosystem kept the dealer-distributor segment at the forefront in 2024.

Key Market Segments

By Component

- Emitters and Drippers

- Drip Tubes and Lines

- Filters

- Pressure Pumps

- Valves and Fittings

- Controllers and Sensors

- Accessories

By Crop Type

- Field Crops

- Vegetable Crops

- Orchard Crops

- Vineyards

- Others

By Application

- Surface Drip Irrigation

- Subsurface Drip Irrigation

By End-User

- Commercial Farms

- Greenhouses and Nurseries

- Residential Gardens and Landscapes

- Sports Fields and Golf Courses

By Sales Channel

- Direct Sales

- Dealer and Distributor

- Online Retail

Driving Factors

Rising need for efficient water management

The drip irrigation market is gaining strong momentum as the need for efficient water management becomes unavoidable across both large and small farming landscapes. Farmers are increasingly shifting toward controlled irrigation systems to reduce water loss, stabilize yields, and manage rising input costs. This movement is further supported by public funding aimed at improving agricultural efficiency, such as the $1 million grant dedicated to new research into nursery industry automation, which indirectly strengthens demand for precision irrigation.

As nurseries and growers automate more processes, the requirement for accurate, low-waste watering systems naturally increases. Alongside growing water scarcity and pressure on freshwater sources, these developments together create a powerful push for wider adoption of drip irrigation systems.

Restraining Factors

High installation costs hinder small farmers

Despite its clear benefits, high installation costs continue to discourage adoption among small and marginal farmers in many regions. The initial expense of pumps, filtration units, tubing networks, and maintenance often exceeds what smallholders can afford without financial support. Adding to this, competing priorities in rural development programs sometimes limit the flow of funds directly toward irrigation upgrades.

An example is the $20 million grant awarded to Millersville for a migrant education program, highlighting how public spending often gets distributed across multiple non-agricultural rural needs. While such investments are important, they also demonstrate how limited budgets can slow the rollout of modern irrigation technologies for farmers who need them most.

Growth Opportunity

Expanding adoption across emerging agricultural regions

Significant growth opportunities lie in emerging agricultural regions that are upgrading from traditional flood irrigation to precision water delivery. Countries with developing farming systems are increasingly adopting drip irrigation to improve yields, reduce labor, and cope with unpredictable rainfall. The expansion is also supported by targeted funding that strengthens nursery and seedling production—critical entry points for modern farming practices.

A notable example is Cove Nursery receiving $276,000 from the Oregon Department of Forestry to expand seedling capacity, which directly boosts the need for controlled watering systems. As more nurseries scale up, demand for efficient water technologies rises, opening new pathways for drip irrigation suppliers and solution providers across both domestic and export markets.

Latest Trends

Shift toward low-pressure precision drip systems

A key trend shaping the drip irrigation landscape is the move toward low-pressure precision systems that require less energy while delivering highly targeted water application. Farmers and growers are also adopting more automated and digitally controlled setups to maintain consistency across large plots.

Recent federal support programs reinforce this transition, such as the USDA’s $2 billion aid package for floriculture growers, encouraging investment in modern greenhouse infrastructure and efficient watering solutions. As greenhouse operators modernize with upgraded irrigation and environmental control systems, the preference for refined, low-waste drip technologies grows. This shift toward energy-efficient and sensor-supported irrigation continues to define the technological direction of the industry.

Regional Analysis

In 2024, the Asia Pacific held 46.9% Drip Irrigation Market share worth USD 3.6 billion.

In 2024, the Drip Irrigation Market showed varied regional performance across North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America, each shaped by crop patterns and water-efficiency needs. Asia Pacific remained the dominating region, holding 46.9% of the market and reaching USD 3.6 billion, driven by large-scale cultivation of field crops and rapid adoption of modern irrigation systems across emerging economies.

North America continued to expand due to the rising shift toward precision irrigation practices among commercial growers, while Europe maintained steady growth supported by sustainable agriculture initiatives and efficient water-use policies. The Middle East & Africa showed increasing uptake of drip systems due to arid climate conditions and the need to improve crop yields under limited water availability.

Latin America also progressed as farmers adopted drip solutions to enhance productivity in fruit, vegetable, and plantation crops. Across these regions, demand for emitters, drippers, and surface drip solutions remained strong, but Asia Pacific clearly led the global landscape, supported by widespread agricultural modernization and strong market penetration.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, ARKA continued to strengthen its position in the global Drip Irrigation Market by focusing on practical, field-ready irrigation technologies that support efficient water delivery. The company’s emphasis on durable emitters, tubing, and pressure-balanced systems aligned well with rising demand from growers seeking consistent performance in varied climatic conditions. ARKA’s portfolio resonated strongly with farms adopting modern irrigation layouts, reinforcing its relevance across both smallholder and commercial segments. Its approach to reliability and ease of installation helped maintain steady market recognition.

Antelco built its 2024 momentum through its specialization in micro-irrigation components designed for precision water application. The company’s drippers, fittings, and micro-spray products remained well-accepted among users needing flexible yet dependable options for orchards, horticulture, and landscaped environments. Antelco’s reputation for consistent product performance supported its strong presence in regions prioritizing water savings and uniform crop output. Its focus on user-friendly designs and adaptable components positioned the company favorably amid the expanding demand for customized drip systems.

Meanwhile, Amiad Water Systems Ltd. played a crucial supporting role in the drip irrigation ecosystem through its filtration expertise. In 2024, the company’s solutions helped protect emitters and pipelines from clogging, enabling long-term system efficiency for growers worldwide. Amiad’s contribution became increasingly important as farms expanded drip networks and required reliable water quality management. Its filtration technologies effectively complement leading drip components, making the company an indispensable partner within the broader irrigation value chain.

Top Key Players in the Market

- ARKA

- Antelco

- Amiad Water Systems Ltd.

- AZUD

- Chinadrip Irrigation Equipment (Xiamen) Co., Ltd

- HUNTER INDUSTRIES INC.

- Irritec S.p.A

- Jain Irrigation Systems Ltd.

- Lindsay Corporation

- NETAFIM

Recent Developments

- In November 2025, Amiad Water Systems showcased its innovative water filtration solutions at the Pollutec 2025 exhibition in France. At the event, the company displayed its products used in irrigation and water treatment, helping visitors learn about its latest filtration technologies used to protect irrigation systems and improve water quality. This participation highlights Amiad’s effort to connect with international customers and promote its solutions for agricultural and industrial filtration.

- In October 2024, Antelco updated its official website to support over 20 languages, making product information more accessible to global customers. This change helps growers and distributors worldwide understand irrigation products better, such as drippers, sprays, and fittings. The update reflects Antelco’s effort to grow its presence internationally.

Report Scope

Report Features Description Market Value (2024) USD 7.7 Billion Forecast Revenue (2034) USD 22.1 Billion CAGR (2025-2034) 11.1% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Component (Emitters and Drippers, Drip Tubes and Lines, Filters, Pressure Pumps, Valves and Fittings, Controllers and Sensors, Accessories), By Crop Type (Field Crops, Vegetable Crops, Orchard Crops, Vineyards, Others), By Application (Surface Drip Irrigation, Subsurface Drip Irrigation), By End-User (Commercial Farms, Greenhouses and Nurseries, Residential Gardens and Landscapes, Sports Fields and Golf Courses), By Sales Channel (Direct Sales, Dealer and Distributor, Online Retail) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape ARKA, Antelco, Amiad Water Systems Ltd., AZUD, Chinadrip Irrigation Equipment (Xiamen) Co., Ltd, HUNTER INDUSTRIES INC., Irritec S.p.A, Jain Irrigation Systems Ltd., Lindsay Corporation, NETAFIM Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Drip Irrigation MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample

Drip Irrigation MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- ARKA

- Antelco

- Amiad Water Systems Ltd.

- AZUD

- Chinadrip Irrigation Equipment (Xiamen) Co., Ltd

- HUNTER INDUSTRIES INC.

- Irritec S.p.A

- Jain Irrigation Systems Ltd.

- Lindsay Corporation

- NETAFIM

Our Clients

- 178737

- February 2026