Global Diesel Particulate Filter Market Size, Share, And Enhanced Productivit By Product Type (Regenerating Type Filters, Disposable Type Filters), By Material Type (Silicon Carbide Wall Flow Filters, Cordierite Wall Flow Filters, Ceramic Fiber Filters, Others), By Application (Heavy Vehicles, Light Vehicles), By Sales Channel (Original Equipment Manufacturer (OEM), Aftersales Market), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2026-2035

- Published date: March 2026

- Report ID: 179971

- Number of Pages: 256

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

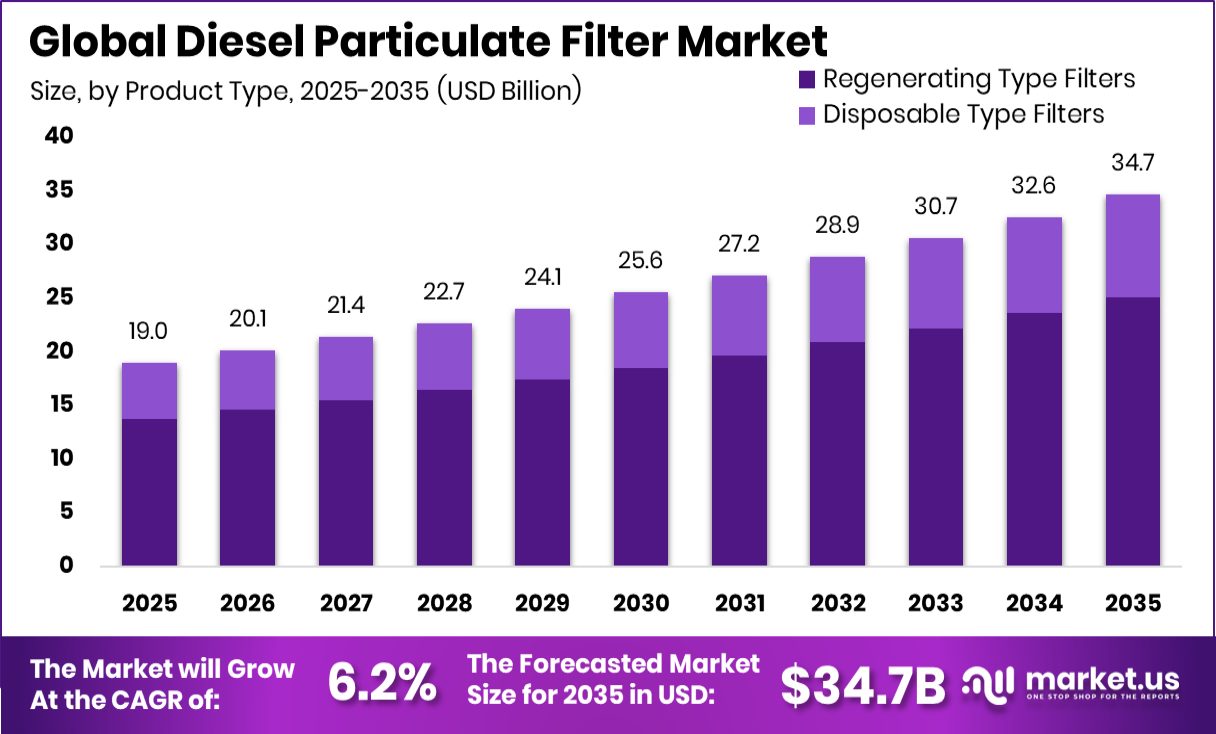

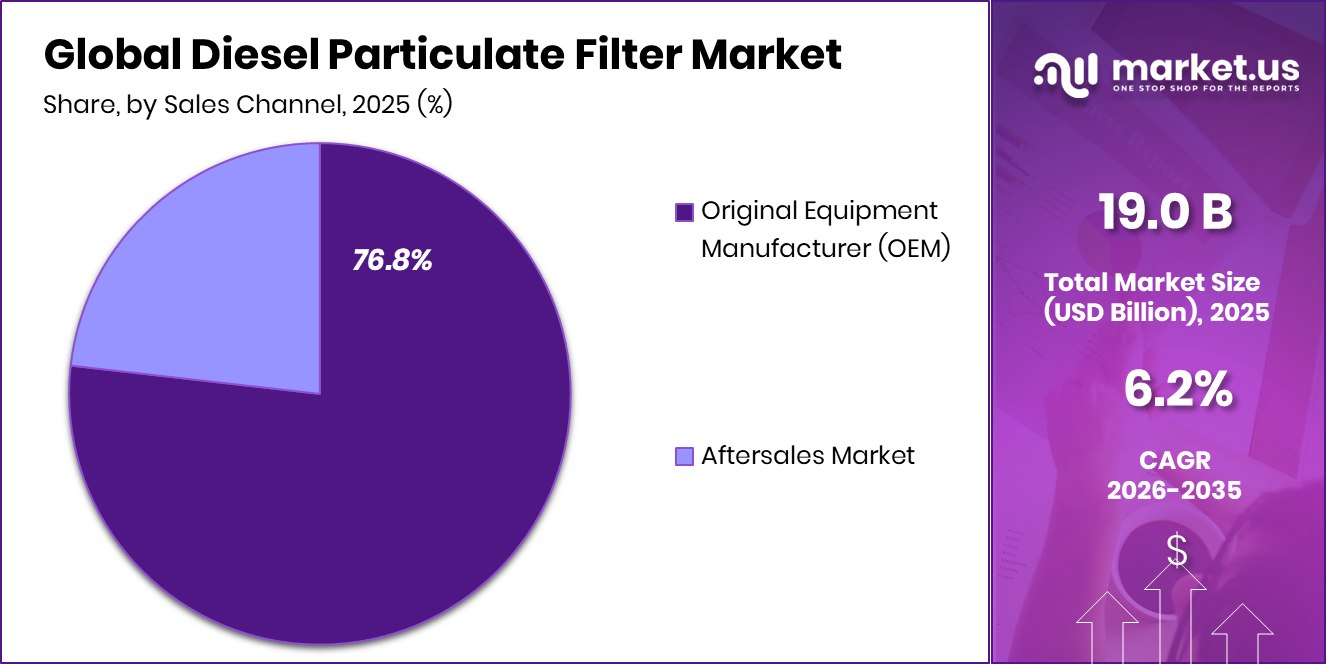

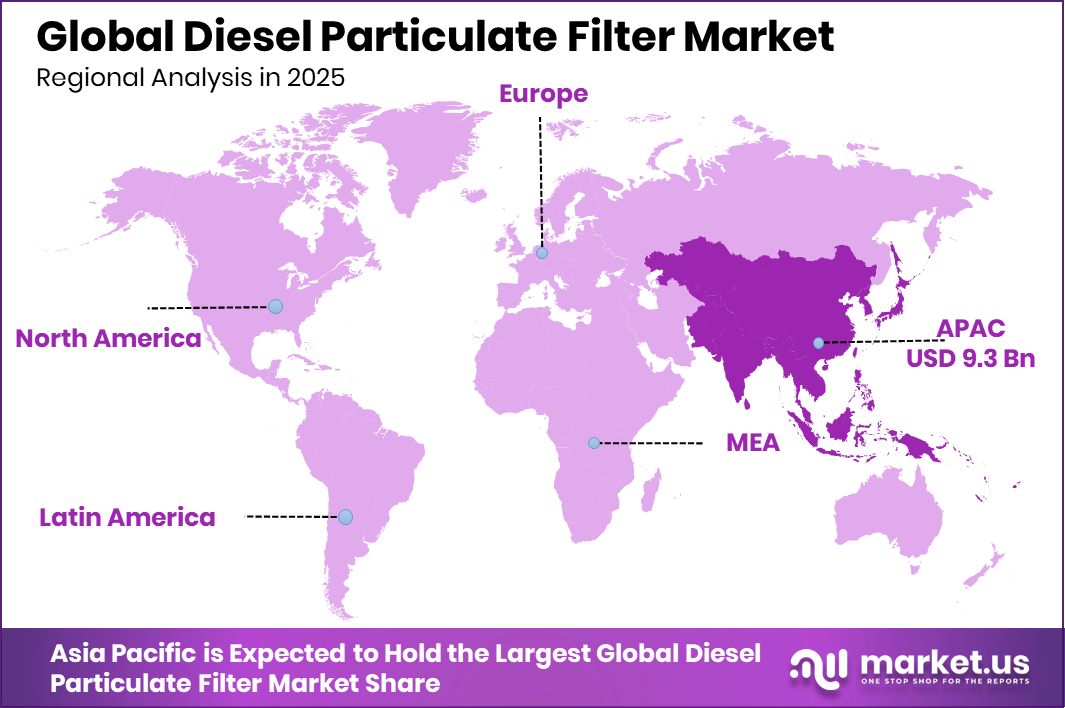

The Global Diesel Particulate Filter Market is expected to be worth around USD 34.7 billion by 2035, up from USD 19.0 billion in 2025, and is projected to grow at a CAGR of 6.2% from 2026 to 2035. Asia Pacific maintained leadership at 49.3% and USD 9.3 Bn, supported by expanding diesel fleets.

The Diesel Particulate Filter (DPF) is a specialized exhaust after-treatment device designed to capture and store soot particles produced during diesel combustion. It prevents these fine particulates from being released into the air, helping vehicles meet stricter emission standards. Within the Diesel Particulate Filter Market, technologies are structured across product types such as regenerating and disposable filters, alongside material categories like silicon carbide, cordierite, ceramic fiber, and others. The market further aligns with applications in heavy and light vehicles and sales channels spanning OEM installations and the growing after-sales segment.

Growth in this market is driven by global moves toward cleaner mobility, supported by funding programs that accelerate low-emission transport. Initiatives such as indiGO Tech raising $54 million for light EVs, €422 million EU funding for zero-emission mobility, and the UK’s £77 million support for new zero-emission vehicle projects reflect how governments are pushing industries to modernize fleets. These actions indirectly increase the need for advanced emission-control systems in existing diesel vehicles during the long transition toward electrification.

Demand is further strengthened by infrastructure-focused programs. The CEC’s approval of $1.4 billion for zero-emission transportation expansion, MTA’s $213 million grant to upgrade light rail, and clean-energy investment surpassing $2 billion under TRC create pressure for fleets to comply with evolving standards. As newer technologies roll out, diesel vehicles still in operation require efficient filtration, opening opportunities for OEM and aftermarket DPF providers as regulatory compliance and replacement cycles continue to rise.

Key Takeaways

- The Global Diesel Particulate Filter Market is expected to be worth around USD 34.7 billion by 2035, up from USD 19.0 billion in 2025, and is projected to grow at a CAGR of 6.2% from 2026 to 2035.

- Diesel Particulate Filter Market sees regenerating type filters leading with a strong 72.4% share.

- Diesel Particulate Filter market growth is supported by silicon carbide wall-flow filters, which hold 67.2% penetration.

- Diesel Particulate Filter Market demand rises as heavy vehicles contribute a notable 51.6% share of applications.

- Diesel Particulate Filter Market expands steadily, with OEM sales channels capturing a dominant 76.8% share.

- The Asia Pacific Diesel Particulate Filter Market reached USD 9.3 Bn, reflecting strong regulatory adoption.

By Product Type Analysis

Diesel Particulate Filter Market regenerating type filters dominated with a 72.4% share.

In 2025, the Diesel Particulate Filter Market is led strongly by regenerating type filters, which dominated with a 72.4% share. These filters continue to gain preference because they clean themselves during operation, reducing maintenance downtime for fleet owners.

As emission standards grow tighter across major economies, OEMs and engine makers are shifting rapidly toward filters that offer durability and longer service intervals. This segment also benefits from wider adoption in commercial trucks and city buses, where high-temperature regeneration cycles work efficiently.

Manufacturers are investing more in thermal-resistant coatings and improved regeneration technologies, which keep this category ahead of passive filter systems. Ongoing regulations worldwide are expected to further strengthen this leadership position.

By Material Type Analysis

Diesel Particulate Filter Market silicon carbide wall flow filters dominated with 67.2% share.

In 2025, silicon carbide wall-flow filters dominated the Diesel Particulate Filter Market with a 67.2% share, driven by their strong thermal conductivity and ability to withstand severe engine temperatures. Heavy-duty engines in transportation, construction, and mining rely heavily on this material due to its stable filtration efficiency even under high-soot conditions. The rising adoption of advanced combustion engines has pushed demand for filter materials that maintain structural integrity during continuous regeneration cycles.

Silicon carbide fits this requirement better than cordierite, making it the preferred choice among OEMs. As governments enforce stricter limits on particulate emissions, industries are prioritizing durable materials that deliver consistent, long-term performance, reinforcing silicon carbide’s dominant position in the market.

By Application Analysis

Diesel Particulate Filter Market heavy vehicles application dominated the segment with 51.6% share.

In 2025, heavy vehicles dominated the Diesel Particulate Filter Market with a 51.6% share, reflecting their high fuel consumption and greater particulate output compared to light-duty vehicles. Trucks, buses, agricultural machinery, and construction equipment increasingly require high-capacity DPF systems to meet global emission rules. The expansion of logistics networks, rising road freight movement, and growth in construction activities are all contributing to higher installation rates.

Operators in these segments focus strongly on reliability, pushing demand for robust, regenerating filter technologies. With more countries enforcing mandatory particulate control for commercial fleets, heavy vehicles remain the largest contributors to DPF adoption. The segment’s consistent operational intensity further supports its dominant market share.

By Sales Channel Analysis

Diesel Particulate Filter Market OEM sales channel dominated overall demand with a 76.8% share.

In 2025, the OEM segment dominated the Diesel Particulate Filter Market with a 76.8% share, supported by the mandatory installation of DPF systems in all newly manufactured diesel vehicles. Automakers are integrating advanced filter technologies during production to comply with tightening emission standards across Europe, Asia, and North America. This early-stage installation also helps maintain vehicle warranty standards and ensures optimized engine-filter compatibility.

As regulatory agencies continue pushing for lower soot emissions, OEMs are upgrading designs to include highly efficient regenerating systems and durable materials like silicon carbide. While aftermarket sales continue to grow for replacement needs, OEM installations hold the strongest position due to regulatory enforcement and industry-wide manufacturing alignment.

Key Market Segments

By Product Type

- Regenerating Type Filters

- Disposable Type Filters

By Material Type

- Silicon Carbide Wall Flow Filters

- Cordierite Wall Flow Filters

- Ceramic Fiber Filters

- Others

By Application

- Heavy Vehicles

- Light Vehicles

By Sales Channel

- Original Equipment Manufacturer (OEM)

- Aftersales Market

Driving Factors

Stricter emission norms drive filtration adoption

Stricter emission norms continue to push steady adoption of diesel particulate filtration across commercial and passenger fleets, especially as regulators tighten soot and NOx limits for urban mobility. These rules create a direct need for dependable DPF systems, reinforcing installation rates in both OEM and replacement segments. Alongside regulations, industry activity is being influenced by parallel clean-transport funding.

The announcement that an Ethanol-Diesel Tech Company gets $30M highlights the broader momentum toward cleaner fuel technologies, indirectly raising expectations for particulate control in mixed-fuel engines. Similarly, Titan Freight Systems’ landing a $1.2M grant for electric trucks signals a transition path where diesel fleets still operating must meet higher filtration standards during the shift to electrified logistics.

Restraining Factors

High system costs limit penetration

High system costs continue to limit wider penetration of diesel particulate filters, particularly in regions where fleet operators face tight operating budgets and slower enforcement of emission rules. Maintenance expenses, regeneration requirements, and periodic replacement cycles add to ownership cost concerns, dampening uptake in cost-sensitive segments. Market constraints are also shaped by the direction of public funding toward alternative clean-transport initiatives.

The California Air Resources Board’s awarding $31 million to the LA MER project demonstrates how grant focus is shifting toward future mobility systems. Likewise, the South Korean government’s plan to invest $153M to support green shipbuilding and reduce GHG emissions shows increased backing for non-diesel pathways, indirectly restraining long-term diesel filtration commitments.

Growth Opportunity

Expanding aftermarket replacements increases sales

Expanding aftermarket replacement cycles are creating significant opportunities in the Diesel Particulate Filter Market, particularly as aging diesel fleets require new filters to stay compliant with evolving regulations. Growing enforcement around inspection and maintenance standards ensures steady demand for well-performing DPF systems throughout the vehicle’s life span. Broader investment in clean transit also influences opportunity areas for DPF providers supporting existing diesel vehicle populations.

The emergence of Propane as the key to $1.5 billion in federal transit grants shows that funding is flowing toward cleaner operations overall, which encourages diesel fleet operators to maintain compliant equipment. This regulatory environment strengthens replacement needs for active fleets that must continue meeting particulate-reduction requirements.

Latest Trends

Shift toward advanced regenerating filter systems

A major trend shaping the Diesel Particulate Filter Market is the rapid shift toward more advanced regenerating systems designed to improve durability and reduce manual maintenance. These upgraded technologies help fleets cut downtime and maintain consistent particulate-capture performance under diverse operating conditions. Another part of the trend landscape is the direction of clean-transport funding that signals long-term decarbonization pathways.

For example, the Golden State trio winning a $31M grant to test zero-emission vessel technology reflects accelerating innovation in non-diesel mobility sectors. As such technologies expand, diesel vehicles that remain in service are increasingly expected to adopt higher-efficiency DPF solutions, keeping filtration advancements relevant during the transition to lower-carbon transport.

Regional Analysis

Asia Pacific dominated the Diesel Particulate Filter Market with 49.3% share, driving regional demand.

In the Diesel Particulate Filter Market, regional performance shows clear differences across major geographies. Asia Pacific remains the dominant region with a 49.3% share and a value of USD 9.3 Bn, supported by expanding commercial fleets and widespread adoption of emission-control systems across industrial economies.

North America continues to record stable demand as heavy-duty trucks and long-haul logistics rely heavily on diesel engines, creating consistent installation requirements for DPF systems. Europe maintains strong adoption driven by long-standing emission legislation and steady replacement demand in mature vehicle fleets.

The Middle East & Africa region shows a gradual uptake, mainly led by growing construction activities and increased diesel-powered equipment usage. Latin America reflects moderate growth as developing economies expand freight transportation and agricultural machinery usage. Across all regions, the higher dominance of Asia Pacific highlights its large diesel vehicle base and rapid regulatory alignment with global emission norms.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2025, BASF continues to strengthen its position in the global Diesel Particulate Filter Market through its long-standing expertise in emission control materials. The company’s catalytic coating technologies remain central to improving filtration efficiency and supporting compliance with evolving diesel emission standards. BASF’s focus on durable catalyst formulations helps automakers meet stringent particulate-reduction targets, especially in heavy-duty engine platforms. Its sustained involvement in advanced substrate and coating development reinforces its influence across OEM partnerships worldwide, making it a steady contributor to high-performance DPF solutions.

Corning Incorporated plays a crucial role in the market through its well-established diesel filter substrates. The company’s ceramic-based wall-flow designs remain widely adopted, especially in applications requiring strong thermal resilience and reliable particulate trapping. Corning’s continuous refinement of silicon carbide and cordierite structures enhances soot-loading capacity and mechanical strength, supporting long-term field performance in commercial and passenger diesel vehicles. By maintaining strong relationships with global automotive manufacturers, the company sustains a major share of the DPF substrate supply landscape in 2025.

Johnson Matthey maintains a solid competitive position due to its deep specialization in emission control catalysts integrated into diesel particulate filters. Its engineered catalyst layers support efficient regeneration and lower soot accumulation, which are essential for heavy-duty diesel operations. The company’s focus on clean-air technologies strengthens its relevance as diesel platforms evolve under stricter environmental compliance. Across global markets, Johnson Matthey’s technical capabilities and continued innovation ensure it remains an important contributor to high-performance DPF systems in 2025.

Top Key Players in the Market

- BASF

- Corning Incorporated

- Johnson Matthey

- MANN+HUMMEL

- Faurecia SE

- BorgWarner

- DENSO CORPORATION

- Cummins Inc.

- Donaldson Company Inc.

- Eberspächer

- Bosal

- NGK INSULATORS, LTD.

- Haldor Topsoe

- Eminox

- Afton Chemical

Recent Developments

- In December 2024, BASF opened a new Catalyst Development and Solids Processing Center aimed at accelerating catalyst innovations. This center supports advanced catalyst and emissions solutions, strengthening BASF’s technical foundation for future emissions-related products (including diesel aftertreatment catalysts).

- In April 2024, Corning reported that its Environmental Technologies segment, which includes particulate filters, grew sales to $455 million, up 6% year-over-year. The increase was driven partly by strong demand for particulate filters in China, showing ongoing market momentum for its emissions products.

Report Scope

Report Features Description Market Value (2025) USD 19.0 Billion Forecast Revenue (2035) USD 34.7 Billion CAGR (2026-2035) 6.2% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Regenerating Type Filters, Disposable Type Filters), By Material Type (Silicon Carbide Wall Flow Filters, Cordierite Wall Flow Filters, Ceramic Fiber Filters, Others), By Application (Heavy Vehicles, Light Vehicles), By Sales Channel (Original Equipment Manufacturer (OEM), Aftersales Market) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape BASF, Corning Incorporated, Johnson Matthey, MANN+HUMMEL, Faurecia SE, BorgWarner, DENSO CORPORATION, Cummins Inc., Donaldson Company Inc., Eberspächer, Bosal, NGK INSULATORS, LTD., Haldor Topsoe, Eminox, Afton Chemical Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Diesel Particulate Filter MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Diesel Particulate Filter MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- BASF

- Corning Incorporated

- Johnson Matthey

- MANN+HUMMEL

- Faurecia SE

- BorgWarner

- DENSO CORPORATION

- Cummins Inc.

- Donaldson Company Inc.

- Eberspächer

- Bosal

- NGK INSULATORS, LTD.

- Haldor Topsoe

- Eminox

- Afton Chemical

Our Clients

- 179971

- March 2026