Global Dental Floss Market Size, Share, Growth Analysis By Product Type (Floss Picks, Multifilament Floss, Monofilament Floss, Dental Tape, Super Floss, Others), By Form (Waxed Floss, Unwaxed Floss, Dental Tape, Others), By Usage (Disposable, Re-Usable), By Distribution Channel (Supermarket/Hypermarket, Hospital Pharmacies, Drug Stores, Retail Pharmacies, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 180008

- Number of Pages: 202

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

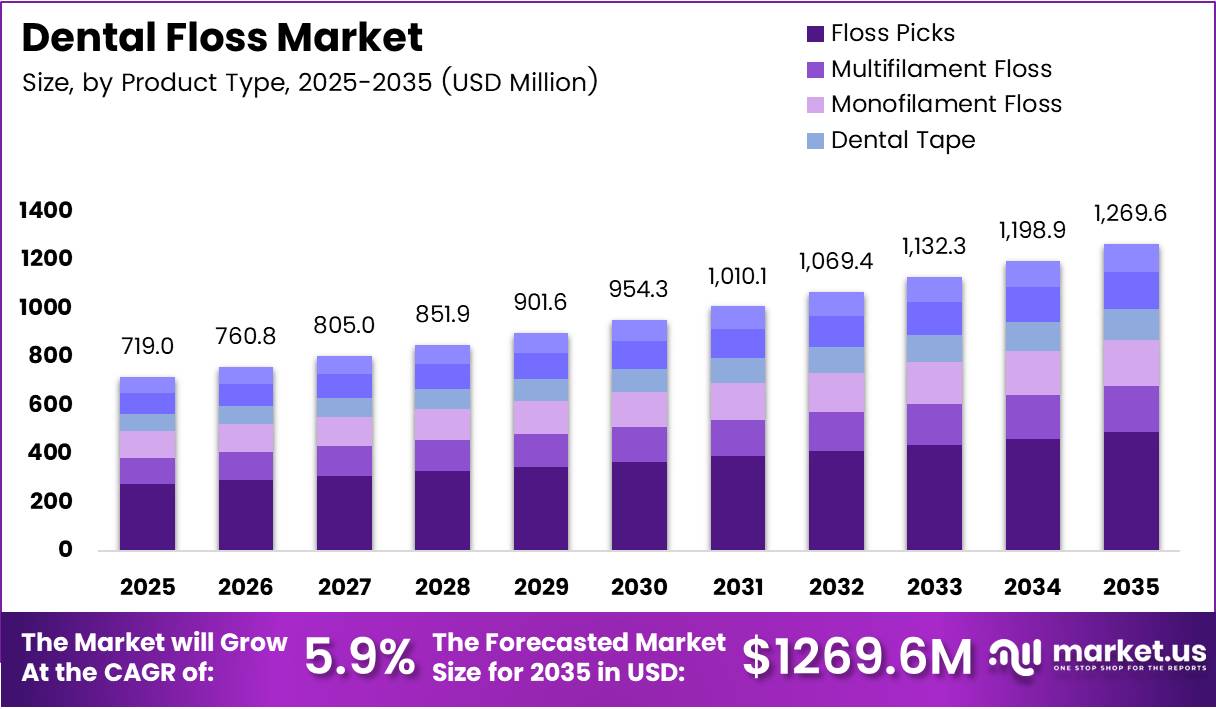

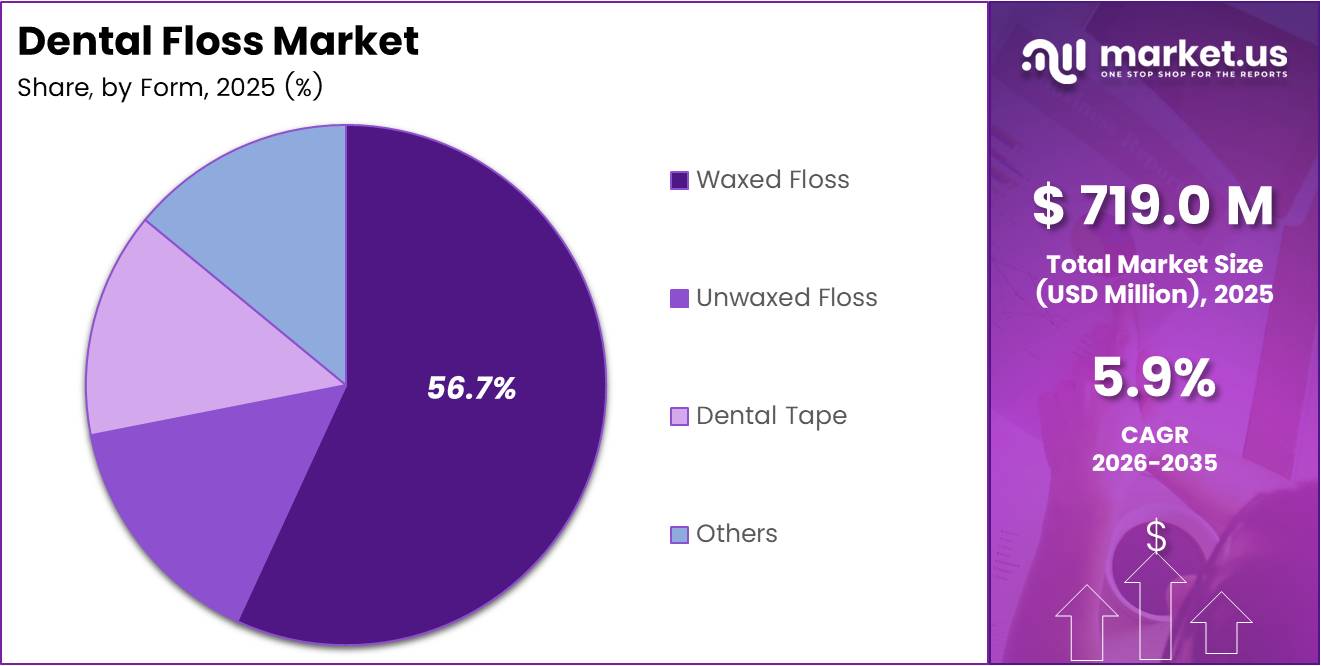

Global Dental Floss Market size is expected to be worth around USD 1,269.6 Million by 2035 from USD 719.0 Million in 2025, growing at a CAGR of 5.9% during the forecast period 2026 to 2035.

The dental floss market covers a range of interdental cleaning products designed to remove plaque and food particles from between teeth. Products include waxed and unwaxed floss, dental tape, floss picks, monofilament varieties, and super floss. These products reach consumers through pharmacies, supermarkets, hospital channels, and direct-to-consumer platforms.

Preventive oral care forms the commercial backbone of this market. Dentists globally recommend daily flossing as an essential complement to brushing, and that clinical endorsement directly translates into shelf demand. The expansion of pharmacy chains and e-commerce platforms has made dental floss more accessible to consumers across income levels and geographies.

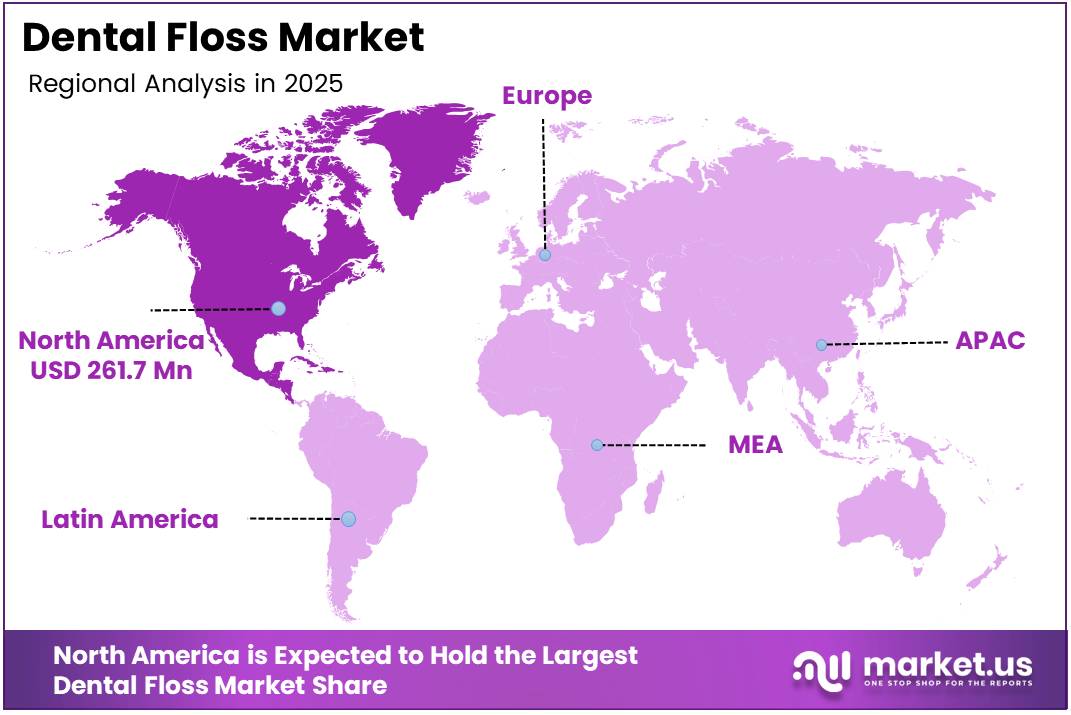

North America holds the dominant regional position, accounting for 36.40% of global revenue — equivalent to USD 261.7 Million. This leadership reflects mature oral care infrastructure, strong dentist-to-patient ratios, and established consumer habits around preventive dental hygiene. These structural conditions set a high baseline that other regions are only beginning to replicate.

Disposable floss formats command 87.3% of the usage segment, which signals that convenience and single-use hygiene remain non-negotiable for most consumers. This pattern limits the near-term viability of reusable floss solutions but opens a clear product differentiation lane for premium materials and eco-conscious disposable variants.

According to PubMed, only 31.6% of U.S. adults floss daily. This figure reveals a structural gap between clinical recommendation and actual consumer behavior — and that gap represents the addressable growth opportunity for brands that invest in habit-formation strategies, convenience formats, and behavioral marketing.

According to ADHA Journal, more than 90% of survey respondents believe flossing improves gum health, yet only about 16% actually floss daily. This disconnect between awareness and action confirms that the market’s primary barrier is not education but behavioral compliance — a challenge that product design, subscription models, and digital engagement are positioned to solve.

Key Takeaways

- The global dental floss market is valued at USD 719.0 Million in 2025 and is forecast to reach USD 1,269.6 Million by 2035.

- The market grows at a CAGR of 5.9% during the forecast period 2026 to 2035.

- North America leads all regions with a 36.40% market share, valued at USD 261.7 Million.

- Floss Picks is the dominant product type segment, holding a 38.8% share.

- Waxed Floss leads the By Form segment with a 56.7% share.

- Disposable floss dominates the By Usage segment at 87.3%.

- Supermarket/Hypermarket leads distribution channels with a 33.6% share.

Product Type Analysis

Floss Picks dominate with 38.8% due to convenience and single-handed ease of use.

In 2025, Floss Picks held a dominant market position in the By Product Type segment of the Dental Floss Market, with a 38.8% share. Their ergonomic design removes the coordination barrier that traditional string floss presents, making them particularly appealing to older adults and first-time flossers. This format drives adoption beyond core oral care consumers into casual and convenience-motivated buyer segments.

Multifilament Floss serves as the foundational product in the dental floss category, favored by consumers who prioritize clinical effectiveness. Its nylon-based construction enables tight contact between teeth, making it effective in standard interdental spaces. However, its reliance on technique-dependent use positions it as a product for habitual flossers rather than new adopters.

Monofilament Floss carries a premium positioning within the product portfolio. Constructed from a single PTFE or similar polymer strand, it slides more easily between tight contacts and resists shredding, reducing user frustration. This functional advantage supports a higher price point and appeals to consumers who have experienced limitations with multifilament options.

Dental Tape differentiates through its broader, flat ribbon form, designed for consumers with wider interdental gaps or bridgework. It is particularly common among patients with orthodontic appliances or dental restorations. This niche positioning limits its volume share but creates a defensible segment with low price sensitivity.

Super Floss addresses a specific clinical use case — cleaning around braces, bridges, and implants. Its three-component structure (stiffened end, spongy floss, and regular floss) is designed for complex mouth geometries. This format commands a loyal segment among orthodontic patients and is frequently recommended by dental professionals.

Others in the product type segment include novelty formats and emerging innovations such as floss-pick hybrids and charcoal-infused options. While their combined share remains modest, product launches in this category are increasing, signaling that manufacturers see room for premiumization and differentiation beyond legacy formats.

Form Analysis

Waxed Floss dominates with 56.7% due to lower friction and broad consumer accessibility.

In 2025, Waxed Floss held a dominant market position in the By Form segment of the Dental Floss Market, with a 56.7% share. The wax coating reduces friction during use, making the flossing experience more comfortable, particularly for consumers with tightly spaced teeth. This usability advantage is a direct factor in higher compliance and repeat purchase rates compared to unwaxed alternatives.

Unwaxed Floss appeals to a specific consumer segment — typically more experienced flossers who prefer a thinner profile and direct tactile feedback. However, its tendency to shred or snap in tight contacts limits mass appeal. It retains its position as the choice for consumers prioritizing simplicity and avoiding synthetic coatings.

Dental Tape within the form segment targets consumers with dental restorations or wider gaps, functioning differently from standard string configurations. Its flat ribbon format provides wider surface contact, making cleaning around fixed prosthetics more effective. Retail placement typically alongside specialist dental products supports its professional recommendation pathway.

Others in the form segment capture emerging variants such as charcoal-infused, flavored, or biodegradable material options. Although currently a small share, product launches in this area reflect where innovation investment is concentrated. Brands entering through sustainable materials or functional additives are building early positioning in a segment that consumer preferences are beginning to shift toward.

Usage Analysis

Disposable floss dominates with 87.3% due to hygiene convenience and mass accessibility.

In 2025, Disposable floss held a dominant market position in the By Usage segment of the Dental Floss Market, with an 87.3% share. The single-use format aligns with consumer hygiene expectations and eliminates the storage and maintenance friction associated with reusable designs. This dominance confirms that the vast majority of purchasing decisions in this category are driven by convenience rather than sustainability.

Re-Usable floss formats represent a structurally small but directionally important segment. Consumer interest in reducing plastic waste is creating an opening for reusable floss devices — including refillable dispensers and durable flossing tools. However, adoption remains limited by habit inertia and price premiums, meaning this segment requires behavioral change investment before it scales.

Distribution Channel Analysis

Supermarket/Hypermarket dominates with 33.6% due to high footfall and impulse purchase behavior.

In 2025, Supermarket/Hypermarket held a dominant market position in the By Distribution Channel segment of the Dental Floss Market, with a 33.6% share. Their high weekly consumer footfall and oral care aisle placement generate consistent volume through habitual and impulse purchases. This channel also enables promotional bundling with toothbrushes and toothpaste, increasing basket size and brand visibility.

Hospital Pharmacies serve a distinct consumer segment — patients with specific dental or medical conditions who require clinically recommended floss varieties. This channel benefits from direct dentist or hygienist referrals, which increases conversion rates and brand loyalty. However, its volume remains limited to patients actively in contact with healthcare providers.

Drug Stores function as the second-largest accessible retail format for dental floss consumers. Their location convenience and pharmacist advisory role support both routine purchases and recommendation-driven switching. Drug stores are particularly relevant for consumers seeking specific varieties such as waxed, PTFE, or orthodontic floss.

Retail Pharmacies overlap with drug stores in function but operate in a broader retail context, often serving suburban and lower-density markets where dedicated pharmacy chains are less present. Their strength lies in proximity to residential consumers and integration with loyalty programs that drive repeat purchases.

Others in distribution include e-commerce platforms, direct-to-consumer subscription services, and specialty health stores. This channel is growing as brands launch subscription-based oral care kits that bundle floss with complementary products. The data-driven targeting capabilities of online channels allow brands to reach specific buyer profiles — particularly younger, health-conscious consumers — that traditional retail underserves.

Key Market Segments

By Product Type

- Floss Picks

- Multifilament Floss

- Monofilament Floss

- Dental Tape

- Super Floss

- Others

By Form

- Waxed Floss

- Unwaxed Floss

- Dental Tape

- Others

By Usage

- Disposable

- Re-Usable

By Distribution Channel

- Supermarket/Hypermarket

- Hospital Pharmacies

- Drug Stores

- Retail Pharmacies

- Others

Drivers

Preventive Oral Care Awareness and Dentist-Led Recommendations Accelerate Floss Adoption

Dental professionals consistently recommend daily flossing as the clinically effective method for removing interdental plaque. This professional endorsement creates a direct purchase trigger — particularly after dental visits — which generates consistent demand across demographics. When dentist recommendations are paired with educational campaigns, compliance rates among patients with active dental relationships improve measurably.

According to Harvard Health, flossing removes up to 80% of plaque between teeth that brushing alone misses. This clinical evidence gives dental floss a defensible functional position that competing interdental products have not fully displaced. For manufacturers, this data point supports premium pricing and evidence-based marketing claims that resonate with health-conscious consumers.

In January 2025, Floss Ring launched its innovative product to integrate floss with toothbrushes, making daily flossing more convenient. This type of product-design innovation directly addresses the compliance gap between awareness and behavior. Consequently, product formats that reduce friction in the flossing routine are likely to unlock adoption among the large segment of consumers who acknowledge the benefit but lack the daily habit.

Restraints

Competition from Alternative Interdental Devices and Low Adult Compliance Limit Market Penetration

Water flossers and interdental brushes have gained significant shelf space and consumer mindshare as substitutes for traditional dental floss. These devices offer perceived ease of use and are marketed as more effective for specific oral conditions. Their availability at competitive price points means consumers who lapse from string floss rarely return to it — they switch to an alternative format instead.

According to PubMed, around 32% of adults report never flossing at all. This figure exposes the hard ceiling on market expansion through existing product formats. No amount of distribution improvement resolves a behavioral adoption problem — meaning the market’s growth ceiling is structurally constrained until product innovation or health campaigns change consumer compliance at scale.

Low flossing compliance is not uniformly distributed across populations — it concentrates among lower-income households, younger adults, and regions with limited dental care infrastructure. This demographic clustering means that volume growth in underserved segments requires more than product availability. Therefore, market participants must invest in behavioral change programs alongside distribution expansion to generate meaningful penetration gains.

Growth Factors

Eco-Friendly Innovation and Premium Product Formats Open New Consumer and Geographic Segments

Consumer demand for biodegradable and sustainable oral care products is creating a viable premium segment within dental floss. Manufacturers that introduce plant-based, recycled, or plastic-free floss variants are differentiating on values rather than price — a positioning that commands higher margins and attracts repeat-purchase loyalty. In 2025, TePe updated its sustainability goals to include 100% renewable, recycled, or certified packaging, signaling that eco-alignment is becoming a commercial strategy, not just a branding exercise.

According to PubMed, adults with higher income were about 62.6% more likely to use dental floss than those with lower income. This income correlation reveals a premium market concentration — and confirms that product innovation targeting higher-income consumers carries a disproportionate revenue return. Flavored, charcoal-infused, and therapeutic floss variants are well-positioned to capture this segment at above-average margins.

Subscription-based oral care kits and direct-to-consumer models represent a structural expansion opportunity. Bundling dental floss with complementary products — toothbrushes, whitening strips, or mouthwash — increases average order value and builds consumption habit through regular delivery. Emerging economies with rising income levels and expanding e-commerce infrastructure represent the next wave of addressable consumers for these models.

Emerging Trends

Sustainable Packaging, Social Media Influence, and Smart Oral Care Ecosystems Reshape Product Positioning

The rise of dental influencers and social media-driven oral health content is shifting consumer behavior at scale. Platforms where dental professionals share preventive care routines have measurably increased interest in flossing among younger demographics who historically underuse the product. This channel is now a cost-effective way for brands to reach consumers who distrust traditional advertising.

According to MDPI, among over 11,000 Korean adults, only 17.5% used dental floss regularly. This data point illustrates how large the untapped adoption gap remains in major Asian markets — and how much room exists for brands that tailor their messaging and product formats to cultural habits and preferences in these geographies. Social media engagement is an especially efficient entry tool in markets where dentist-recommendation networks are thinner.

Multifunctional oral care products that combine flossing, picking, and toothpick functions are gaining traction among consumers seeking simplified hygiene routines. Additionally, dental floss is increasingly positioned as a component within smart oral care ecosystems that include connected toothbrushes and app-based habit tracking. Brands that integrate floss into broader digital health routines benefit from stickier consumer relationships and higher switching costs.

Regional Analysis

North America Dominates the Dental Floss Market with a Market Share of 36.40%, Valued at USD 261.7 Million

North America holds 36.40% of global dental floss revenue, valued at USD 261.7 Million. This leadership position reflects a combination of mature dental care infrastructure, high dentist-to-population ratios, and established consumer routines around preventive oral hygiene. The region also benefits from well-developed pharmacy and retail distribution networks that maintain consistent product availability.

Europe Dental Floss Market Trends

Europe represents a structurally strong secondary market, supported by national health systems that promote preventive dental care and a well-educated consumer base. Western European markets in particular show higher compliance rates than global averages, driven by school-based dental health programs. The region’s strong sustainability regulations also accelerate adoption of eco-friendly floss variants, creating favorable conditions for premium product positioning.

Asia Pacific Dental Floss Market Trends

Asia Pacific presents the largest volume expansion opportunity among all regions. Rising middle-class income levels, an expanding base of urban dental clinics, and growing e-commerce penetration are collectively increasing product accessibility. However, flossing adoption rates remain low across several major markets, meaning demand growth depends on behavioral change initiatives alongside distribution improvements.

Middle East and Africa Dental Floss Market Trends

The Middle East and Africa region shows a wide range of adoption levels, from relatively higher usage in Gulf urban centers to very low awareness in Sub-Saharan markets. Infrastructure gaps in dental care access constrain the professional recommendation channel that drives floss adoption elsewhere. Nevertheless, urbanization and rising health awareness in major cities create a gradual but real demand trajectory.

Latin America Dental Floss Market Trends

Latin America’s dental floss market is shaped by the contrast between urban centers with modern retail infrastructure and rural areas with limited oral care access. Brazil and Mexico are the most commercially active markets, supported by strong pharmacy retail networks and growing dental tourism industries. Income inequality remains the primary structural constraint on per-capita floss consumption across the region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Procter & Gamble holds a structural advantage in this market through its Oral-B brand portfolio, which allows floss products to be bundled with toothbrush and toothpaste lines under a single consumer relationship. This cross-sell architecture gives the company disproportionate shelf presence and consumer recall. Their investment in product innovation and retailer partnerships reinforces their ability to defend share against both private-label and specialty entrants.

Colgate-Palmolive Company competes through global distribution scale and a trusted brand identity that dental professionals actively recommend. Their position in emerging markets is particularly strategic — as rising income levels in Asia and Latin America create first-time floss buyers, Colgate’s existing toothpaste relationships give it an early conversion advantage. The company’s pharmacy and supermarket channel depth provides wide accessibility that challenger brands cannot easily replicate.

Prestige Consumer Healthcare, Inc. positions itself in the over-the-counter personal care space with a portfolio strategy that includes dental hygiene. Their approach focuses on accessible price points and broad retail distribution rather than premium differentiation. This strategy targets the high-volume, value-conscious consumer segment — a position that generates stable revenue but limits margin expansion as premium and eco-friendly segments grow faster than value tiers.

Johnson & Johnson Services, Inc. brings clinical credibility to its dental floss positioning through its broader healthcare brand equity. Their floss products benefit from co-placement with medical and personal care items in pharmacy environments, reinforcing the health-professional endorsement narrative. This channel alignment is a strategic asset — particularly for reaching consumers who make purchase decisions at the pharmacy counter on clinical advice rather than price or packaging.

Key players

- Procter & Gamble

- Colgate-Palmolive Company

- Prestige Consumer Healthcare, Inc.

- Johnson & Johnson Services, Inc.

- 3M

- Lion Corporation

- Wild

- Sunstar Suisse SA

- The Humble Co.

Recent Developments

- July 2025 — TePe introduced its dental floss made from 100% recycled polyester sourced from plastic bottles, directly reducing plastic waste in the oral care supply chain. This launch positions TePe as a sustainability leader in the floss segment and targets the growing base of eco-conscious consumers willing to pay a premium for environmentally responsible oral care products.

- June 2025 — Flaus launched an electric flosser using recycled plastic components, offering a lower-plastic alternative to standard floss picks. This product targets environmentally motivated consumers who previously viewed electric flossing devices as incompatible with a sustainable lifestyle, expanding the addressable market for premium power-flossing devices.

Report Scope

Report Features Description Market Value (2025) USD 719.0 Million Forecast Revenue (2035) USD 1,269.6 Million CAGR (2026-2035) 5.9% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Floss Picks, Multifilament Floss, Monofilament Floss, Dental Tape, Super Floss, Others), By Form (Waxed Floss, Unwaxed Floss, Dental Tape, Others), By Usage (Disposable, Re-Usable), By Distribution Channel (Supermarket/Hypermarket, Hospital Pharmacies, Drug Stores, Retail Pharmacies, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Procter & Gamble, Colgate-Palmolive Company, Prestige Consumer Healthcare Inc., Johnson & Johnson Services Inc., 3M, Lion Corporation, Wild, Sunstar Suisse SA, The Humble Co. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Procter & Gamble

- Colgate-Palmolive Company

- Prestige Consumer Healthcare, Inc.

- Johnson & Johnson Services, Inc.

- 3M

- Lion Corporation

- Wild

- Sunstar Suisse SA

- The Humble Co.

Our Clients

- 180008

- Feb 2026