Quick Navigation

Report Overview

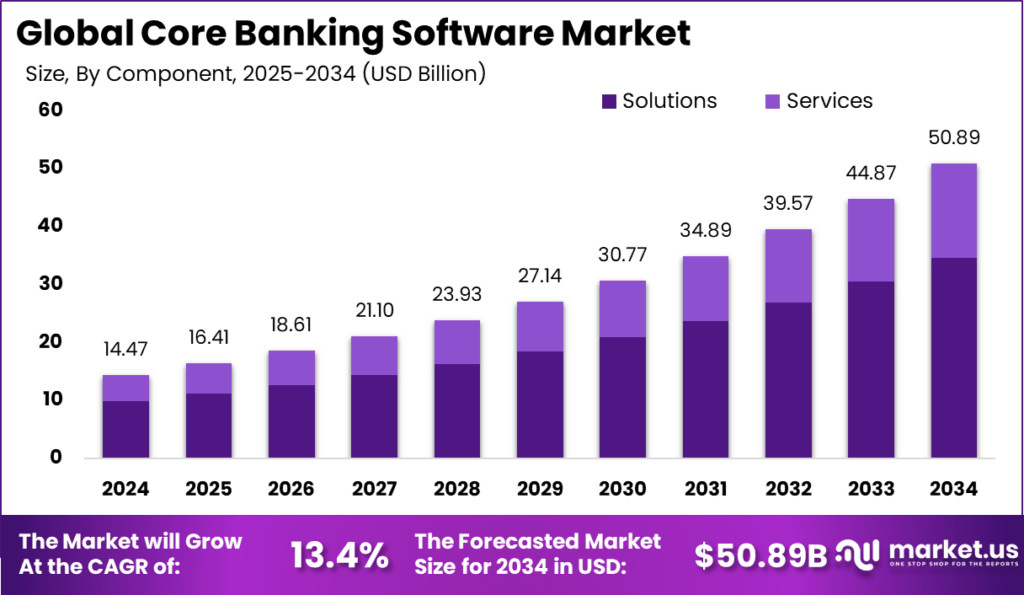

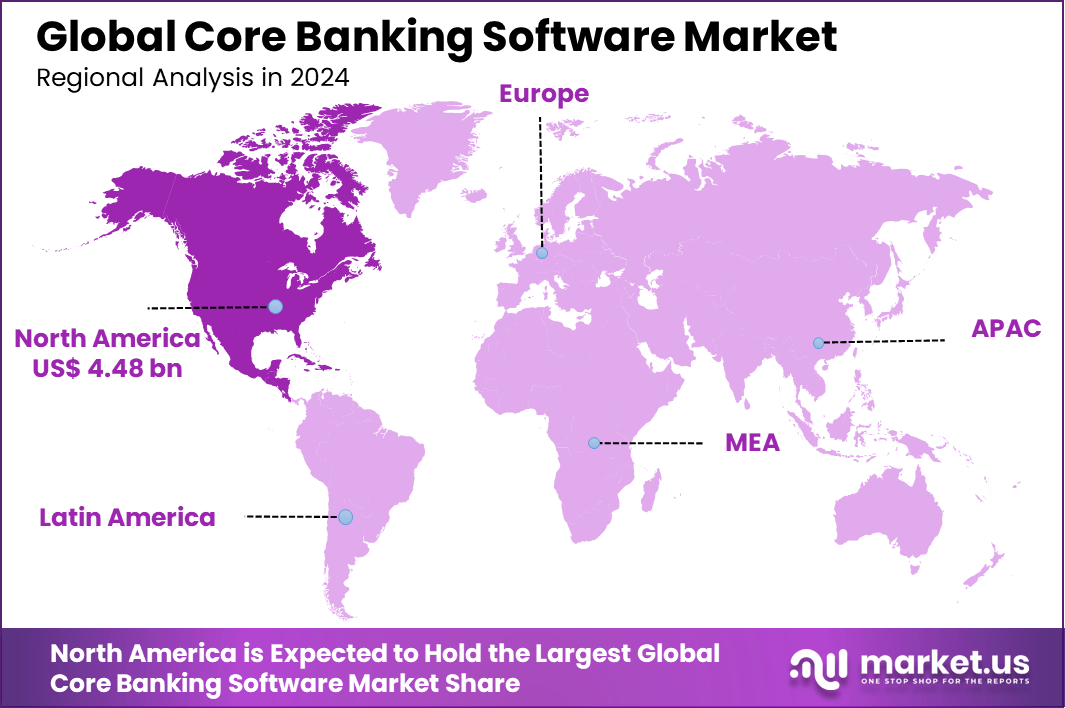

The Global Core Banking Software Market size is expected to be worth around USD 50.89 billion by 2034, from USD 14.47 billion in 2024, growing at a CAGR of 13.4% during the forecast period from 2025 to 2034. In 2024, North America held a dominant market position, capturing more than a 31% share, holding USD 4.48 billion in revenue.

The global core banking software market is experiencing significant growth, driven by the increasing demand for digital transformation in the banking sector. Several key factors are propelling the adoption of core banking software. The increasing demand for real-time banking services, the need for improved operational efficiency, and the rising expectations of customers for seamless digital experiences are primary drivers.

The demand for core banking software is further amplified by the proliferation of digital banking channels. As more consumers prefer online and mobile banking, financial institutions are compelled to adopt core banking systems that support these platforms. This shift is particularly evident in emerging markets, where mobile banking adoption is accelerating rapidly.

Technological advancements are playing a pivotal role in shaping the core banking software landscape. The integration of artificial intelligence (AI) and machine learning (ML) enables banks to offer personalized services, detect fraud more effectively, and streamline operations. Cloud computing is also gaining traction, offering scalability, cost-effectiveness, and enhanced data security.

According to Market.us, The global Generative AI in Banking market is poised for a transformative expansion, projected to grow from approximately USD 818 million in 2023 to reach nearly USD 13,957 million by 2033, registering a striking CAGR of 32.8% over the forecast period. This growth reflects the banking sector’s accelerated shift toward intelligent automation, customer-centric innovation, and risk-sensitive digital transformation.

The core banking software market presents substantial investment opportunities. As banks and financial institutions prioritize digital transformation, there is a growing demand for innovative solutions that can enhance customer engagement and operational efficiency. Investors can explore opportunities in companies developing advanced core banking platforms, especially those leveraging AI, ML, and cloud technologies.

Key Takeaways

- The global core banking software market is expected to grow from USD 14.47 billion in 2024 to around USD 50.89 billion by 2034, expanding at a robust CAGR of 13.4% from 2025 to 2034.

- North America led the global market in 2024, capturing over 31% share with total revenue of approximately USD 4.48 billion, supported by the high concentration of digitally advanced banks and early adoption of banking tech platforms.

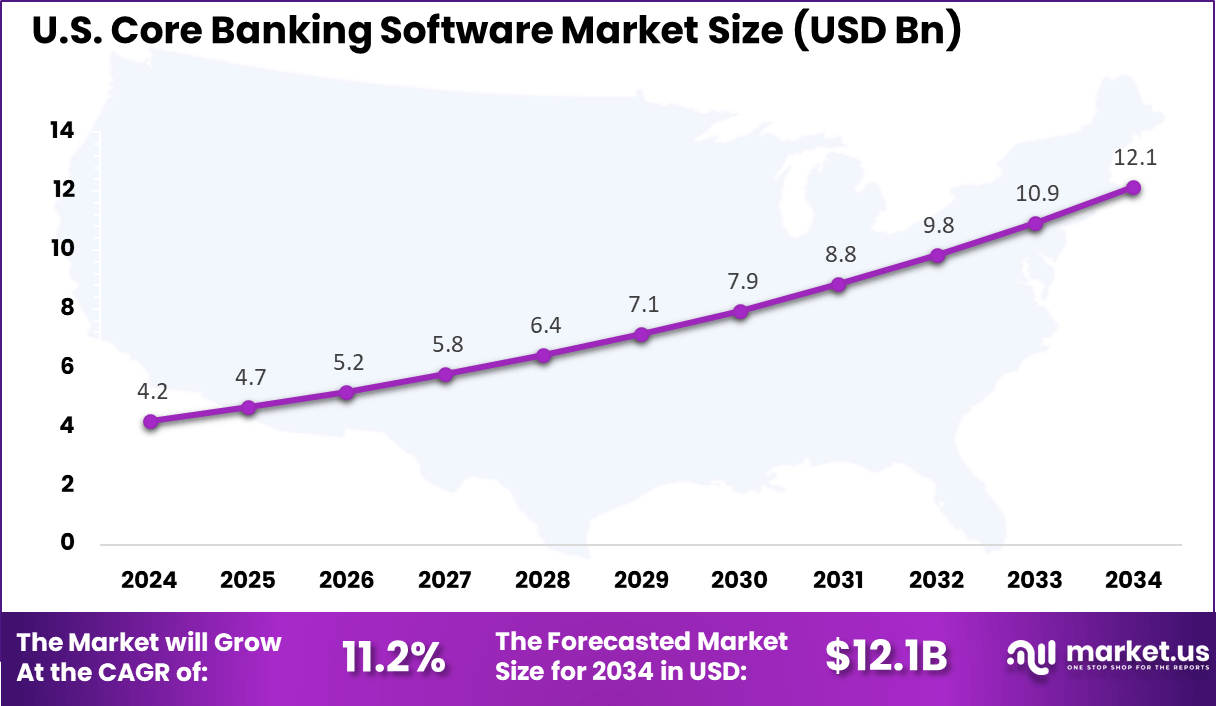

- The U.S. market is currently valued at USD 4.2 billion and is forecasted to grow steadily at a CAGR of 11.2%, driven by demand for modernization of legacy banking systems and improved digital customer experiences.

- Solutions dominated the market by component, accounting for 68% of the revenue share in 2024, due to increasing preference for integrated core banking platforms over separate modules.

- On-premise deployment models held a larger share at 57%, reflecting the banking sector’s continued focus on data control, compliance, and internal security protocols.

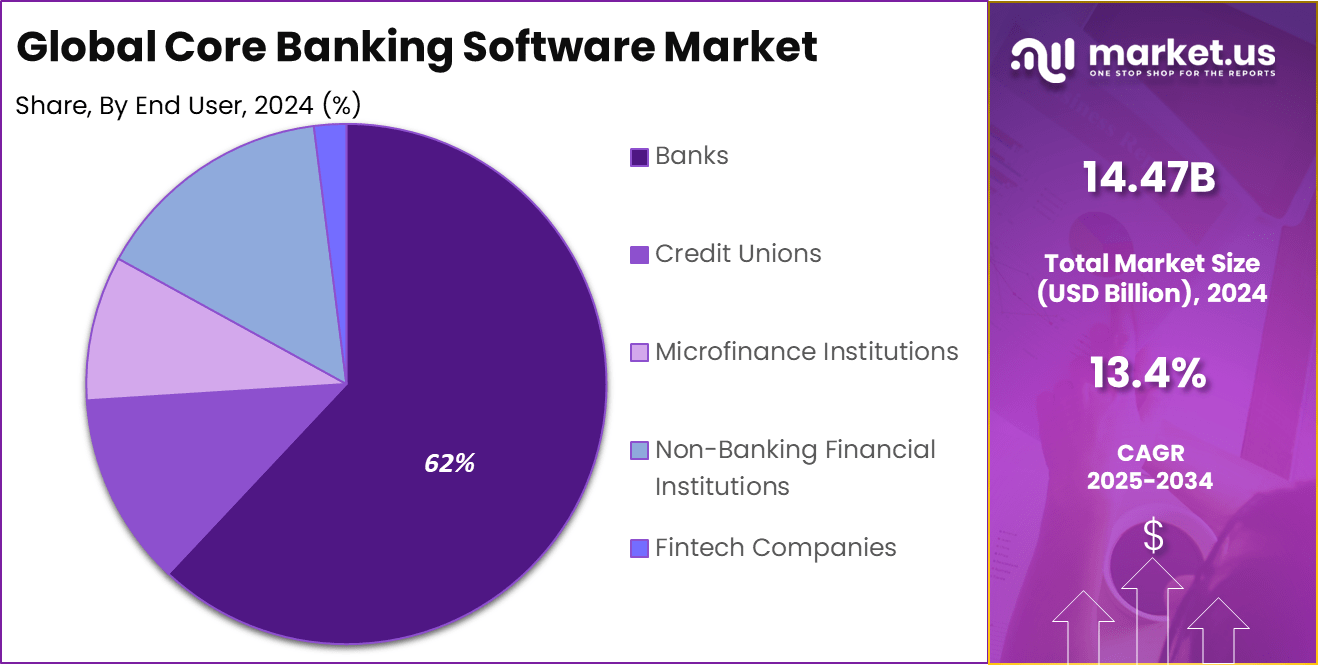

- Banks were the dominant end-user segment, making up 62% of the global market, as financial institutions drive major investments in digital transformation, omnichannel services, and API-enabled banking.

Role of AI

The integration of artificial intelligence (AI) into core banking software is significantly transforming the financial services industry. This transformation is evident in enhanced operational efficiency, improved customer experiences, and robust risk management.

AI technologies are streamlining banking operations by automating routine tasks, reducing manual errors, and accelerating transaction processing. For instance, AI-driven systems can automate loan and credit decisions, track market trends, and manage regulatory compliance and risk . These capabilities enable banks to operate more efficiently and allocate resources to more strategic initiatives.

AI is also revolutionizing customer interactions in banking. Through the use of natural language processing and conversational AI, banks can offer personalized services and recommendations, improving customer satisfaction and loyalty. AI-powered chatbots provide 24/7 customer support, addressing queries promptly and accurately. Additionally, AI analyzes customer data to predict preferences, allowing banks to tailor their offerings effectively.

In the realm of risk management, AI enhances the ability of banks to detect and prevent fraudulent activities. By analyzing patterns and anomalies in transaction data, AI systems can identify potential fraud and money laundering activities more effectively. Furthermore, AI aids in regulatory compliance by automating the monitoring and reporting processes, ensuring adherence to evolving regulations.

US Market Expansion

The market for Core Banking Software within the U.S. is growing tremendously and is currently valued at USD 4.2 billion, the market has a projected CAGR of 11.2%. The market for Core Banking Software within the U.S. is growing tremendously due to increasing demand for digital banking solutions, real-time payment capabilities, and enhanced regulatory compliance.

U.S. financial institutions are rapidly modernizing legacy systems to improve customer experience and operational agility. Additionally, the rise of fintech partnerships and open banking initiatives is driving banks to adopt flexible, cloud-based core banking platforms that support innovation and seamless integration. Regulatory mandates such as the FedNow Service further accelerate the need for real-time transaction processing, fueling market growth.

For instance, In May 2025, UK-based Starling Bank revealed its entry into the U.S. market by offering its cloud-native core banking software to American financial institutions. This strategic move underscores the rising demand in the U.S. for modern, scalable, and API-first core banking platforms that support rapid digital transformation and strengthen competitiveness against fintech disruptors.

North America Growth

In 2024, North America held a dominant 31% share of the Global Core Banking Software Market, generating over USD 4.48 billion in revenue. This leadership is rooted in the region’s robust digital infrastructure, widespread cloud adoption, and the active role of top financial institutions in modernizing core systems.

For instance, March 2025 partnership between Finastra and i2c, aiming to equip North American banks with advanced digital wallet and real-time payment solutions. This alliance highlights the region’s strategic push toward digital transformation, AI integration, and cybersecurity enhancements within banking infrastructure, reinforcing its global market dominance.

By Component Analysis

In 2024, the Solutions segment held a dominant market position in the global core banking software market, capturing more than a 68% share. This leadership is primarily attributed to the increasing demand for advanced digital banking capabilities, which encompass modules such as deposits, loans, and enterprise customer solutions.

Financial institutions are prioritizing the modernization of their core systems to enhance operational efficiency, ensure regulatory compliance, and meet evolving customer expectations. The adoption of comprehensive solutions facilitates seamless integration across various banking functions, enabling real-time processing and improved customer service.

For instance, In May 2025, Tata Consultancy Services (TCS) partnered with Khan Bank in Mongolia to modernize its core banking systems using AI and machine learning. TCS delivered end-to-end consulting and managed services to boost operational efficiency and customer experience. This move highlights the rising role of tech services in driving digital transformation in banking.

The prominence of the Solutions segment is further reinforced by the growing trend of digital transformation within the banking sector. Banks are investing in scalable and flexible core banking solutions to support the rapid deployment of new financial products and services.

Additionally, the shift towards cloud-based deployments and the integration of emerging technologies such as artificial intelligence and machine learning are driving the adoption of sophisticated core banking solutions. These advancements allow financial institutions to offer personalized banking experiences, streamline operations, and maintain a competitive edge in a dynamic market environment.

By Deployment Mode Analysis

In 2024, the on-premise deployment segment held a dominant position in the global core banking software market, capturing more than a 57% share. This dominance is primarily attributed to the stringent data security and compliance requirements prevalent in the banking sector.

Financial institutions often prefer on-premise solutions to maintain direct control over their data and IT infrastructure, ensuring adherence to regulatory standards and minimizing potential security breaches. The ability to customize and integrate these solutions with existing legacy systems further reinforces their appeal among traditional banks.

Moreover, the established infrastructure and significant investments in on-premise systems make financial institutions hesitant to transition to alternative deployment models. The familiarity and proven reliability of on-premise solutions provide a sense of stability and continuity, which is crucial for maintaining uninterrupted banking operations.

For instance, In November 2024, Temenos partnered with NVIDIA to launch an on-premises AI banking platform that delivers advanced AI capabilities while keeping data within banks’ secure environments. By merging Temenos’ core banking strengths with NVIDIA’s high-performance AI processing, the solution addresses growing demand for secure, compliant, and powerful on-premise deployments, balancing innovation with strict regulatory needs.

By End-User Analysis

In 2024, the Banks segment held a dominant position in the global core banking software market, capturing more than a 62% share. This leadership is primarily attributed to the substantial investments made by banks in modernizing their IT infrastructure to enhance operational efficiency and customer experience.

The adoption of advanced core banking solutions enables banks to streamline processes such as account management, transaction processing, and customer relationship management, thereby improving service delivery and competitiveness. Furthermore, the increasing demand for digital banking services has compelled banks to upgrade their core systems to support real-time processing and integration with digital channels.

The implementation of core banking software facilitates centralized data management, regulatory compliance, and scalability, which are critical for banks to adapt to evolving market dynamics and customer expectations. Additionally, collaborations between banks and technology providers have accelerated the development and deployment of innovative banking solutions, reinforcing the dominance of the Banks segment in the core banking software market.

For instance, In April 2025, Access Bank Plc, a prominent pan-African financial institution, began a major core banking system upgrade to improve scalability, operational efficiency, and customer experience across its African operations. The initiative involves deploying advanced digital banking solutions to enable real-time transactions and multi-channel engagement, reinforcing the bank’s commitment to digital transformation and strategic market differentiation in the region.

Key Market Segments

By Component

- Solution

- Deposits

- Loans

- Enterprise Customer Solutions

- Others

- Services

- Professional Services

- Managed Services

By Deployment Mode

- On-Premise

- Cloud-Based

By End-User

- Banks

- Credit Unions

- Microfinance Institutions

- Non-Banking Financial Institutions (NBFIs)

- Fintech Companies

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver

Digital Transformation in Banking

Financial institutions worldwide are intensifying digital transformation initiatives to deliver superior customer experiences, improve operational efficiency, and ensure compliance with evolving regulations. Core banking software serves as the backbone of these transformations by facilitating real-time transaction processing, seamless multi-channel integration, and agile product development.

This foundational role positions CBS as a critical enabler for banks seeking competitive differentiation and scalability in a digitally driven marketplace. For instance, In May 2025, a report by Bottomline Technologies revealed that U.S. banks and financial institutions are rapidly adopting real-time payments (RTP) to meet rising demand for instant fund transfers from both consumers and businesses.

The report underscores the importance of modernizing core banking infrastructure, strengthening fraud detection, and ensuring regulatory compliance. Bottomline also noted that RTP adoption enhances customer satisfaction while opening up new revenue opportunities through innovative payment solutions.

Restraint

Legacy Systems Impeding Core Banking Software Implementation

Despite the advantages of modern CBS, many banks face challenges due to entrenched legacy systems. These outdated platforms, often built on monolithic architectures and obsolete programming languages, hinder the integration of new technologies and limit operational agility. The rigidity of legacy systems makes it difficult to introduce innovative services or adapt to regulatory changes promptly.

For instance, in July 2024, a Reserve Bank of India (RBI) report, highlighted by CNBC-TV18, revealed a rise in cyberattacks and data breaches across India’s banking sector due to rapid digitalization. As banks adopt new technologies, the lack of robust cybersecurity measures has increased the risk of exposing sensitive customer data. This has positioned data security as a major restraint in the modernization of core banking software.

Moreover, maintaining these systems incurs high costs, both in terms of financial resources and human capital. The scarcity of professionals skilled in legacy technologies exacerbates the issue, leading to increased operational risks and potential service disruptions. These factors collectively restrain the widespread adoption of advanced CBS, as banks must navigate the complexities of transitioning from legacy infrastructures to modern platforms.

Opportunity

Cloud Adoption Unlocking New Potential in Core Banking

The migration to cloud-based CBS presents a significant opportunity for banks to enhance their service offerings and operational efficiency. Cloud computing enables financial institutions to scale resources dynamically, reduce infrastructure costs, and accelerate the deployment of new services.

Cloud-based CBS solutions support real-time data processing and analytics, facilitating personalized customer experiences and informed decision-making. Additionally, the flexibility of cloud platforms allows banks to integrate emerging technologies seamlessly, fostering innovation and competitiveness. As regulatory frameworks evolve to accommodate cloud adoption, banks are increasingly positioned to leverage these platforms for strategic growth.

Challenge

Cybersecurity Threats in the Digital Banking Landscape

The digitalization of banking services has heightened the importance of robust cybersecurity measures. As banks adopt advanced CBS and expand their digital footprints, they become more susceptible to cyber threats, including data breaches and system intrusions. The complexity of modern banking ecosystems, characterized by interconnected platforms and third-party integrations, amplifies these risks.

Ensuring the security of customer data and maintaining trust are paramount. Banks must invest in comprehensive cybersecurity frameworks that encompass real-time threat detection, incident response strategies, and compliance with regulatory standards. The challenge lies in balancing the pursuit of innovation with the imperative to safeguard digital assets, necessitating a proactive and holistic approach to cybersecurity in the core banking environment.

Emerging Trends

The core banking software (CBS) landscape is undergoing significant transformation, driven by technological advancements and evolving customer expectations. One prominent trend is the adoption of composable banking architectures, which utilize microservices and APIs to enable banks to assemble tailored solutions from various components.

This modular approach enhances flexibility and accelerates innovation, allowing financial institutions to respond swiftly to market changes and customer needs. Additionally, the integration of artificial intelligence (AI) and machine learning (ML) into CBS is revolutionizing operations by enabling predictive analytics, personalized customer experiences, and intelligent automation of routine tasks.

Another emerging trend is the shift towards cloud-native core banking solutions. Cloud-based CBS offers scalability, cost-effectiveness, and improved disaster recovery capabilities, making it an attractive option for banks seeking to modernize their infrastructure. Furthermore, the emphasis on open banking is reshaping the industry by promoting interoperability and data sharing through standardized APIs.

Business Benefits

Implementing modern core banking software yields substantial business benefits for financial institutions. One key advantage is enhanced operational efficiency. By automating routine processes and consolidating disparate systems, CBS reduces manual workloads, minimizes errors, and accelerates transaction processing.

This streamlining of operations not only lowers operational costs but also frees up resources to focus on strategic initiatives and customer engagement. Moreover, real-time data processing capabilities enable banks to gain immediate insights into their operations, facilitating informed decision-making and agile responses to market dynamics.

Another significant benefit is improved customer experience. Modern CBS platforms support omnichannel banking, allowing customers to access services seamlessly across various channels, including mobile apps, online portals, and physical branches. This consistency enhances customer satisfaction and loyalty. Additionally, the integration of advanced analytics enables banks to offer personalized products and services tailored to individual customer needs and preferences.

Key Player Analysis

Leading players in the core banking software market – including Capgemini, Finastra, Infosys Limited, Temenos, and Fiserv, Inc. are actively strengthening their positions through a mix of strategic partnerships, product innovations, and technology-driven initiatives.

These efforts are aimed at meeting the growing demand for agile, secure, and scalable banking systems while staying ahead in an increasingly competitive environment. By focusing on digital transformation and customer-centric solutions, these companies are helping financial institutions modernize core operations and enhance service delivery.

Top Key Players Covered

- Temenos AG

- Infosys Ltd.

- FIS (Fidelity National Information Services)

- Finastra

- Oracle Corporation

- SAP SE

- Tata Consultancy Services (TCS)

- Jack Henry & Associates, Inc.

- nCino

- Mambu

- Backbase

- Thought Machine

- Others

Recent Developments

- In March 2025, Fiserv, Inc. strengthened its position in embedded finance by acquiring Payfare Inc., a provider of program management technology solutions. The acquisition is expected to enhance Fiserv’s capabilities in delivering integrated financial services and expand its portfolio of embedded finance offerings.

- In February 2025, Al Rayan Bank of Qatar selected Finastra to implement a customized core banking solution. As part of its ongoing technology transformation, the bank aims to adopt advanced digital tools to improve service performance and deliver a more seamless customer experience.

- In January 2025, Infosys Finacle, a subsidiary of Infosys under EdgeVerve Systems, launched the Finacle Asset Liability Management Solution. This risk management platform provides banks with a comprehensive view of their balance sheet exposures, supporting better financial decision-making and regulatory compliance.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 14.47 Bn |

| Forecast Revenue (2034) | USD 50.89 Bn |

| CAGR (2025-2034) | 13.4% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Component (Solution (Deposits, Loans, Enterprise Customer Solutions, Others), Services), By Deployment Mode (On-Premise, Cloud-Based), By End-User (Banks, Credit Unions, Microfinance Institutions, Non-Banking Financial Institutions (NBFIs), Fintech Companies) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Temenos AG, Infosys Ltd., FIS (Fidelity National Information Services), Finastra, Oracle Corporation, SAP SE, Tata Consultancy Services (TCS), Jack Henry & Associates, Inc., nCino, Mambu, Backbase, Thought Machine, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |