Global Chlorinated Polyethylene Market Size, Share Analysis Report By Product (CPE 135A, CPE 135B, Others), By Application (Impact Modifier, Wire And Cable Jacketing, Hose And Tubing, Adhesives, Magnetics, IR ABS, Others) , By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: April 2026

- Report ID: 184061

- Number of Pages: 248

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

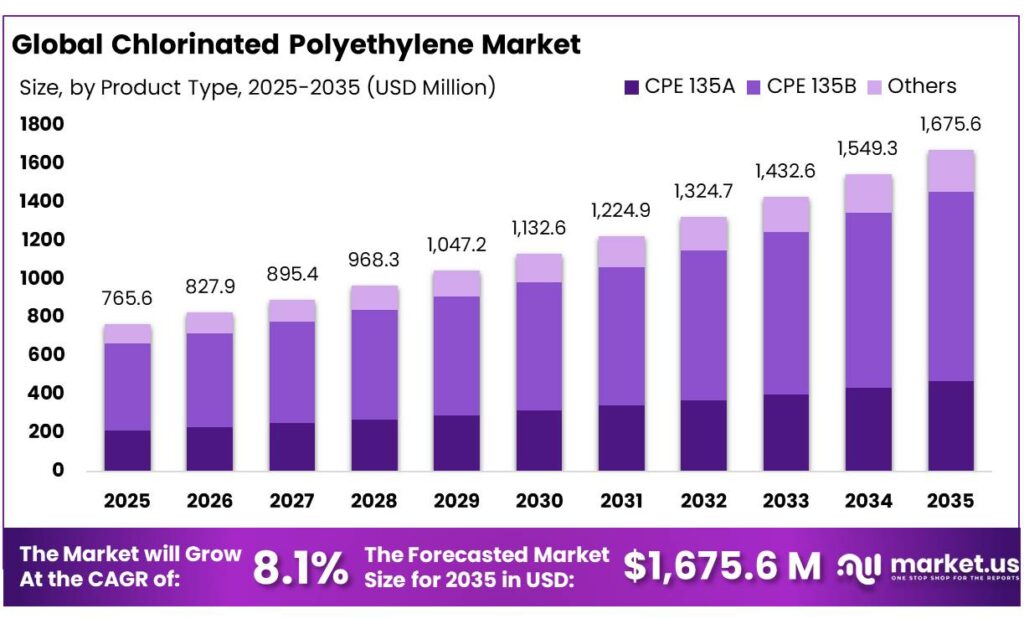

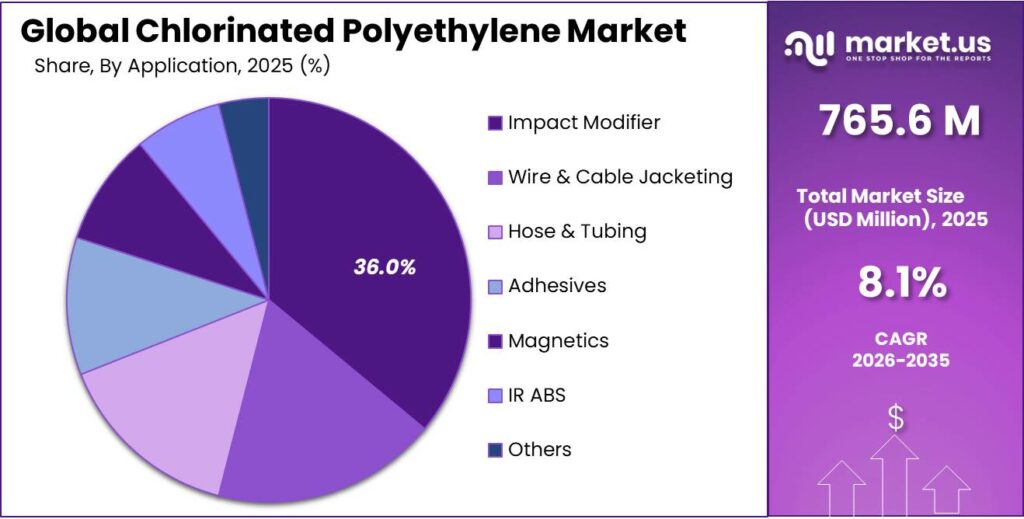

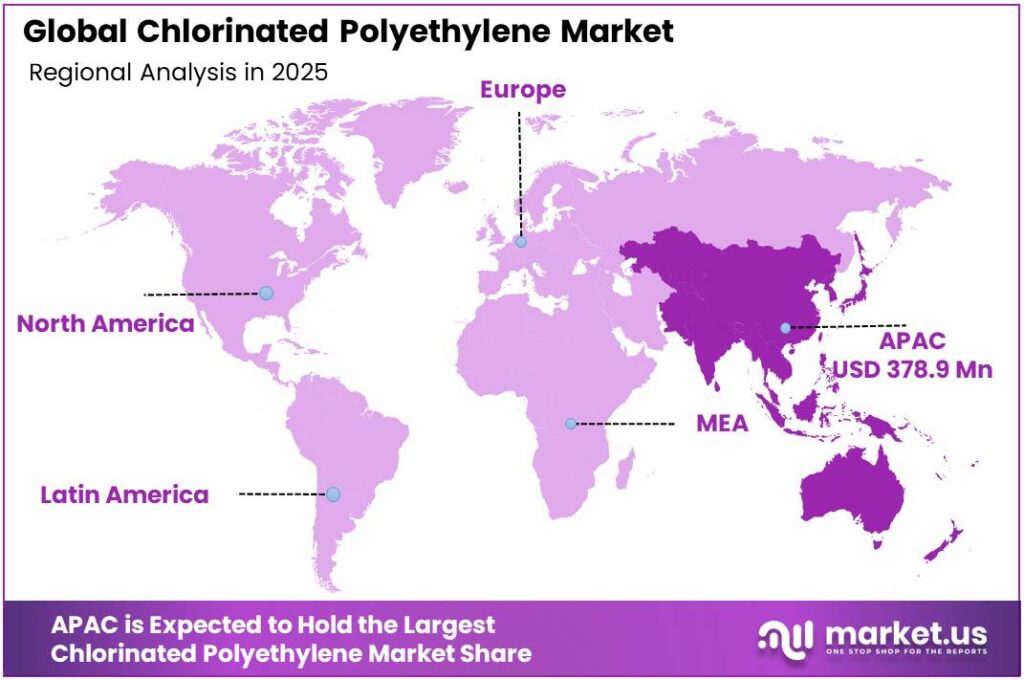

The Global Chlorinated Polyethylene Market size is expected to be worth around USD 1,675.6 Million by 2035, from USD 765.6 Million in 2025, growing at a CAGR of 8.1% during the forecast period from 2026 to 2035. In 2025, Asia Pacific held a dominant market position, capturing more than a 49.5% share, holding USD 378.9 Million revenue.

Chlorinated polyethylene (CPE) is generally positioned as a specialty chlorinated polyolefin used both as an impact modifier for rigid PVC and as an elastomeric material for wire, cable, hose, roofing and industrial sheeting. Commercial CPE grades typically contain about 25–50 wt% chlorine, while U.S. food-contact rules allow chlorinated polyethylene with up to 60 wt% total chlorine and permit its use in food-contact articles under specified conditions; for fatty-food applications, its use in PVC articles is limited to 15 wt% as a modifier.

The current industrial scenario remains closely tied to construction, electrification and automotive production. In the United States, total construction spending reached a seasonally adjusted annual rate of $2,190.4 billion in January 2026, including $933.0 billion in residential construction, $728.2 billion in nonresidential construction and $148.5 billion in highway construction. In Europe, the policy backdrop also remains supportive: the European Commission’s Renovation Wave targets 35 million buildings to be renovated by 2030, with at least a doubling of the annual energy-renovation rate.

Demand is also being reinforced by electrification and cable-network investment. The IEA states that energy-sector capital flows are set to rise to USD 3.3 trillion in 2025, with around USD 2.2 trillion directed to renewables, nuclear, grids, storage, low-emissions fuels, efficiency and electrification. Separately, the U.S. DOE’s GRIP framework is designed to invest approximately $10.5 billion over FY22–FY26, while DOE also announced up to $3.46 billion in GRIP selections in October 2023.

The U.S. Department of Energy states that its GRIP program will invest about $10.5 billion across FY2022-FY2026, while the European Commission said in June 2025 that Europe will need an estimated €730 billion in distribution grid investment and €477 billion in transmission grid development by 2040. For CPE, this points to medium-term opportunity in power cable accessories, protective sheathing, and infrastructure components that must tolerate heat, weathering, and mechanical stress.

Dow, meanwhile, announced on 7 July 2025 the shutdown of three upstream European assets, targeting more than $6 billion in near-term cash support and an approximate $200 million EBITDA uplift over time; later, at K 2025, it highlighted solutions for wire and cable, piping and building materials, including recycled-plastic cable-jacket resins. The medium-term growth opportunity for CPE is not likely to come from speculative volume expansion alone, but from higher-value formulations aligned with grid modernization, building renovation, circularity and durable infrastructure performance.

Key Takeaways

- Chlorinated Polyethylene Market size is expected to be worth around USD 1,675.6 Million by 2035, from USD 765.6 Million in 2025, growing at a CAGR of 8.1%.

- CPE 135A held a dominant market position, capturing more than a 59.6% share.

- Impact Modifier held a dominant market position, capturing more than a 36.1% share.

- Asia Pacific held the dominant position in the chlorinated polyethylene market, accounting for 49.5% of the global share and reaching USD 378.9 million.

By Product Analysis

CPE 135A dominates with 59.6% share due to its strong fit across wire, cable, hose, and impact-modified plastic applications.

In 2025, CPE 135A held a dominant market position, capturing more than a 59.6% share. This leading position was mainly supported by its wide use in applications that require a strong balance of flexibility, weather resistance, flame retardancy, and durability. The grade remained highly preferred across wire and cable insulation, rubber blending, hoses, magnetic materials, and impact modification for plastic products, where consistent processing performance is important. Its reliable compatibility with PVC and other polymer systems also made it a practical choice for manufacturers looking for stable quality in large-scale production.

By Application Analysis

Impact Modifier leads with 36.1% share, supported by strong demand for tougher and more durable plastic products.

In 2025, Impact Modifier held a dominant market position, capturing more than a 36.1% share. This segment’s strong performance was largely driven by the growing use of chlorinated polyethylene in improving the toughness, crack resistance, and low-temperature durability of plastic materials, especially PVC-based products. It remained widely used in pipes, window profiles, siding, sheets, and molded construction materials where higher impact strength is essential for long-term performance. Manufacturers continued to favor chlorinated polyethylene as an impact modifier because it helps finished products withstand physical stress, rough handling, and changing weather conditions without losing structural stability.

Key Market Segments

By Product

- CPE 135A

- CPE 135B

- Others

By Application

- Impact Modifier

- Wire & Cable Jacketing

- Hose & Tubing

- Adhesives

- Magnetics

- IR ABS

- Others

Emerging Trends

Shift Toward Green Cable Compounds and Renewable Power Infrastructure is the Latest Key Trend

One major latest trend in the chlorinated polyethylene market is the growing shift toward green power infrastructure and high-performance cable compounds. As renewable energy capacity additions continue to rise globally, demand for durable wire and cable jacketing materials is also moving up, where CPE remains a preferred choice due to its flame resistance, weather durability, and long outdoor life. The International Energy Agency reported that the world added 510 GW of renewable capacity in 2023, up 50% from 2022, marking the fastest growth on record.

This rapid rise in solar and wind installations is increasing the need for UV-resistant and flexible cable insulation across solar farms, wind parks, and grid extension projects. CPE is increasingly being selected in these applications because it performs reliably under heat, moisture, and harsh environmental exposure. The trend is especially visible in utility-scale solar parks and underground transmission cables linked with government-backed clean energy expansion plans. As renewable networks continue expanding through 2025 and 2026, the use of advanced CPE compounds in cable protection is becoming one of the clearest market trends.

Membrane Cell Upgrades and Low-Emission Chlor-Alkali Processing are Reshaping Supply Trends

Another major trend is the move toward membrane-cell based chlor-alkali modernization, which is improving the quality consistency and sustainability profile of downstream CPE production. Since chlorine is the core feedstock for chlorinated polyethylene, upgrades in chlor-alkali technology directly influence product purity and operating economics. Recent industry-backed alkali bulletins show that single electrolyser production capacity has increased by 22%–46%, reflecting the fast adoption of efficient membrane systems in 2025.

This trend is important because cleaner chlorine production with lower power consumption helps CPE manufacturers improve both cost control and environmental compliance. Governments and industrial regulators are also encouraging energy-efficient chemical processing routes, pushing more producers to replace older mercury and diaphragm systems with membrane technology. As this transition spreads across Asia and Europe, the market is seeing a clear trend toward cleaner-value-chain CPE grades designed for electrical, automotive, and construction applications.

Drivers

Expanding PVC Pipe and Profile Demand from Infrastructure Projects

A major driving factor for the chlorinated polyethylene market is the steady rise in infrastructure and construction activity, especially in PVC pipes, window profiles, siding, and cable conduits where CPE is widely used as an impact modifier. Governments across major economies are increasing spending on housing, water supply, sanitation, and urban infrastructure, which directly supports PVC consumption. For example, India’s Department of Chemicals and Petrochemicals reported that the country’s PVC production reached 1.78 million metric tons in 2023–24, reflecting strong downstream demand from pipes and construction materials.

As chlorinated polyethylene improves toughness, weather resistance, and crack durability in PVC products, this rise in polymer usage naturally lifts its demand. The effect is especially visible in water management and irrigation networks, where PVC pipes continue to replace traditional metal systems due to lower cost and longer life. This makes construction-led PVC demand one of the strongest long-term growth engines for chlorinated polyethylene, particularly in fast-urbanizing economies moving into 2025 and 2026.

Government Housing and Utility Expansion Supporting Material Consumption

Another strong growth driver is public investment in housing, smart cities, and utility expansion, where durable plastic materials are essential. Many government-backed programs now focus on affordable housing, drainage, renewable power cabling, and underground electrical networks, all of which use PVC compounds modified with chlorinated polyethylene for better impact strength and longer outdoor performance. Global construction output is projected to grow by 3.0% in 2024 and 4.5% in 2025, according to Oxford Economics data highlighted in construction industry trend reporting.

This matters because a large share of modern construction materials now depends on polymer-modified plastics that can withstand harsh environments. CPE benefits directly from this trend through its use in roofing membranes, wire jacketing, door profiles, and structural fittings. As governments continue to prioritize resilient infrastructure and safer electrical systems, the need for stronger PVC formulations keeps rising, creating stable and practical growth momentum for the chlorinated polyethylene market over the next few years.

Restraints

Volatility in Chlor-alkali Raw Material Economics Limits CPE Production Stability

A major restraining factor for the chlorinated polyethylene market is the unstable cost structure of chlorine and chlor-alkali feedstocks used in production. Since CPE manufacturing depends heavily on chlorine availability and energy-intensive chlor-alkali operations, any imbalance in upstream economics directly affects production costs and pricing consistency. In India, the chlor-alkali segment represented 92.3 lakh tonnes in FY2024, accounting for over 71% of total chemical production, showing how strongly downstream products like CPE depend on this supply chain.

At the same time, industry estimates indicate caustic soda capacities may rise by 9.1% over the next five years, while demand growth remains uneven. Such mismatches often create volatility in chlorine realization, because chlorine output is linked to caustic soda production. When chlorine pricing weakens or supply becomes inconsistent, CPE manufacturers face difficulty in maintaining stable margins, especially in cost-sensitive applications such as PVC impact modifiers and wire compounds.

Tightening Environmental Compliance and Energy Costs Slow Capacity Expansion

Another important restraint is the increasing compliance burden linked to energy use, emissions, and chemical handling standards in chlorine-based manufacturing. Chlorinated polyethylene production requires strict environmental controls because chlorine chemistry, waste streams, and power usage are closely monitored under industrial safety norms. According to recent industry-backed chemical sector analysis, India’s chlor-alkali production is projected to reach 11.5 million tonnes by FY2030, around 23% growth from FY2024, but this expansion also means higher investment in cleaner power sourcing and pollution control systems.

For many mid-sized producers, the cost of upgrading membrane cell systems, waste treatment, and emission monitoring infrastructure can slow new capacity additions. This is especially true in regions where governments are tightening industrial discharge and electricity efficiency requirements. While these initiatives are positive for long-term sustainability, they increase operating expenses in the near term and can reduce competitiveness for smaller CPE manufacturers.

Opportunity

Rising Wire, Cable, and Grid Modernization Projects Create Strong Growth Space

One major growth opportunity for the chlorinated polyethylene market is the fast expansion of power transmission, distribution cables, and industrial wiring infrastructure. CPE is widely used in wire and cable jacketing because it offers excellent flame resistance, flexibility, abrasion protection, and weather durability. As countries continue to upgrade aging electricity systems and add renewable energy connections, the need for stronger cable insulation materials is increasing steadily.

According to the International Energy Agency, global electricity demand from clean technologies such as electric vehicles, air conditioning, and industrial electrification is putting rising pressure on grid networks, making large-scale grid upgrades essential. The IEA also highlights that electricity grids are becoming the backbone of modern energy systems and require significant investment in new power lines and cable networks.

Electric Vehicle Charging Infrastructure Expansion Opens New Demand Channels

Another major opportunity comes from the rapid buildout of electric vehicle charging networks and EV-related wiring systems. Chlorinated polyethylene is increasingly used in EV cables, battery protection wiring, charging connectors, and under-hood insulation parts because it performs well under heat, oil exposure, and mechanical stress. The International Energy Agency reported that global electric car sales exceeded 17 million units in 2024, showing how quickly EV ecosystems are expanding into 2025.

This growth is not limited to vehicles alone, as every EV sold adds demand for charging stations, power cables, flexible protective jackets, and durable electrical connectors. Government-backed EV infrastructure programs in India, Europe, China, and North America are further strengthening this opportunity by increasing public charging coverage and grid-linked fast charging systems. Since CPE helps improve cable safety and long-term performance in outdoor charging environments, the expansion of EV infrastructure is opening a very practical and scalable growth avenue for manufacturers.

Regional Insights

Asia Pacific dominates with 49.5% share, reaching USD 378.9 Mn on the back of strong PVC, wire & cable, and construction demand

Asia Pacific held the dominant position in the chlorinated polyethylene market, accounting for 49.5% of the global share and reaching USD 378.9 million, making it the leading regional market in 2025. The region’s strength is mainly supported by its large-scale PVC processing industry, rapid infrastructure development, and expanding electrical and construction sectors across China, India, Japan, South Korea, and Southeast Asia.

Chlorinated polyethylene sees strong consumption here as an impact modifier in PVC pipes, fittings, profiles, roofing sheets, and siding products, all of which continue to witness healthy demand from urban development and public utility projects. The region also benefits from a highly integrated chlor-alkali and chlorine value chain, ensuring stable raw material availability for downstream CPE manufacturing. Asia Pacific’s chlor-alkali industry alone was valued at USD 36.80 billion in 2025, highlighting the strong upstream ecosystem that supports chlorine-based specialty polymers.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Dow remains one of the most established names in the chlorinated polyethylene space, supported by its broad polymer science capabilities and deep integration across performance plastics. In 2025, Dow reported net sales of around USD 42.9 billion, giving it strong financial flexibility to support specialty elastomer and modifier businesses.

Resonac Holdings Corporation continues to be a technically strong participant in the chlorinated polyethylene market, particularly in Asia. In 2025, the company’s consolidated revenue remained above JPY 1.3 trillion, highlighting its large advanced materials and chemicals base. Its strength comes from integrating chlorinated polymers with electronics, industrial materials, and specialty elastomer technologies.

Sundow Polymers has built a solid market presence as a specialized chlorinated polyethylene manufacturer with strong focus on PVC modifiers and elastomer blends. The company is estimated to operate with 50,000+ metric tons of annual CPE capacity, enabling reliable supply to both domestic and export markets. Its portfolio is widely used in PVC pipes, window profiles, waterproof membranes, and cable jacketing.

Top Key Players Outlook

- Dow

- Arkema

- Resonac Holdings Corporation.

- Weifang Yaxing Chemical Co., Ltd.

- Sundow Polymers Co., Ltd.

- NIPPON SHOKUBAI CO., LTD.

- INEOS Group Limited

- Shandong Novista Chemicals Co., Ltd.

- Hangzhou Keli Chemical Co., Ltd.

- Shandong Xuye New Materials Co., Ltd.

- Focus Technology Co., Ltd.

Recent Industry Developments

In 2025, Dow’s Packaging & Specialty Plastics segment reported net sales of USD 5.3 billion, while full-year 2025 segment sales were about USD 21.8 billion, showing the scale of its polymer business that indirectly supports CPE-related product development and downstream demand.

In 2025 results, Arkema reported sales of €9,068 million and EBITDA of €1,251 million, showing the financial scale behind its specialty materials platform.

Report Scope

Report Features Description Market Value (2025) USD 765.6 Mn Forecast Revenue (2035) USD 1,675.6 Mn CAGR (2026-2035) 8.1% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product (CPE 135A, CPE 135B, Others), By Application (Impact Modifier, Wire And Cable Jacketing, Hose And Tubing, Adhesives, Magnetics, IR ABS, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape Dow, Arkema, Resonac Holdings Corporation., Weifang Yaxing Chemical Co., Ltd., Sundow Polymers Co., Ltd., NIPPON SHOKUBAI CO., LTD., INEOS Group Limited, Shandong Novista Chemicals Co., Ltd., Hangzhou Keli Chemical Co., Ltd., Shandong Xuye New Materials Co., Ltd., Focus Technology Co., Ltd. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Chlorinated Polyethylene MarketPublished date: April 2026add_shopping_cartBuy Now get_appDownload Sample

Chlorinated Polyethylene MarketPublished date: April 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Dow

- Arkema

- Resonac Holdings Corporation.

- Weifang Yaxing Chemical Co., Ltd.

- Sundow Polymers Co., Ltd.

- NIPPON SHOKUBAI CO., LTD.

- INEOS Group Limited

- Shandong Novista Chemicals Co., Ltd.

- Hangzhou Keli Chemical Co., Ltd.

- Shandong Xuye New Materials Co., Ltd.

- Focus Technology Co., Ltd.

Our Clients

- 184061

- April 2026