Global BYOD and Enterprise Mobility Market Size, Share and Analysis Report By Solution (Software, Services), By Security (Data Security, Email Security, Network Security, Identity Access Management, Application Security), By Deployment Type (Cloud, On-Premises), By End-User (BFSI, IT and Telecommunications, Automobile, Retail, Healthcare, Transportation and Logistics, Others), By Regional Analysis, Global Trends and Opportunity, Future Outlook By 2025-2035

- Published date: Feb. 2026

- Report ID: 179620

- Number of Pages: 256

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Key Takeaway

- Key BYOD & Enterprise Mobility Statistics

- By Solution: Software at 74.5%

- By Security: Data Security at 44.2%

- By Deployment Type: On Premises at 65.7%

- By End User: BFSI at 39.5%

- North America at 35.6%

- U.S. Market Size

- Emerging Trends Analysis

- Growth Factors Analysis

- Key Market Segments

- Drivers

- Restraint

- Opportunities

- Challenges

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

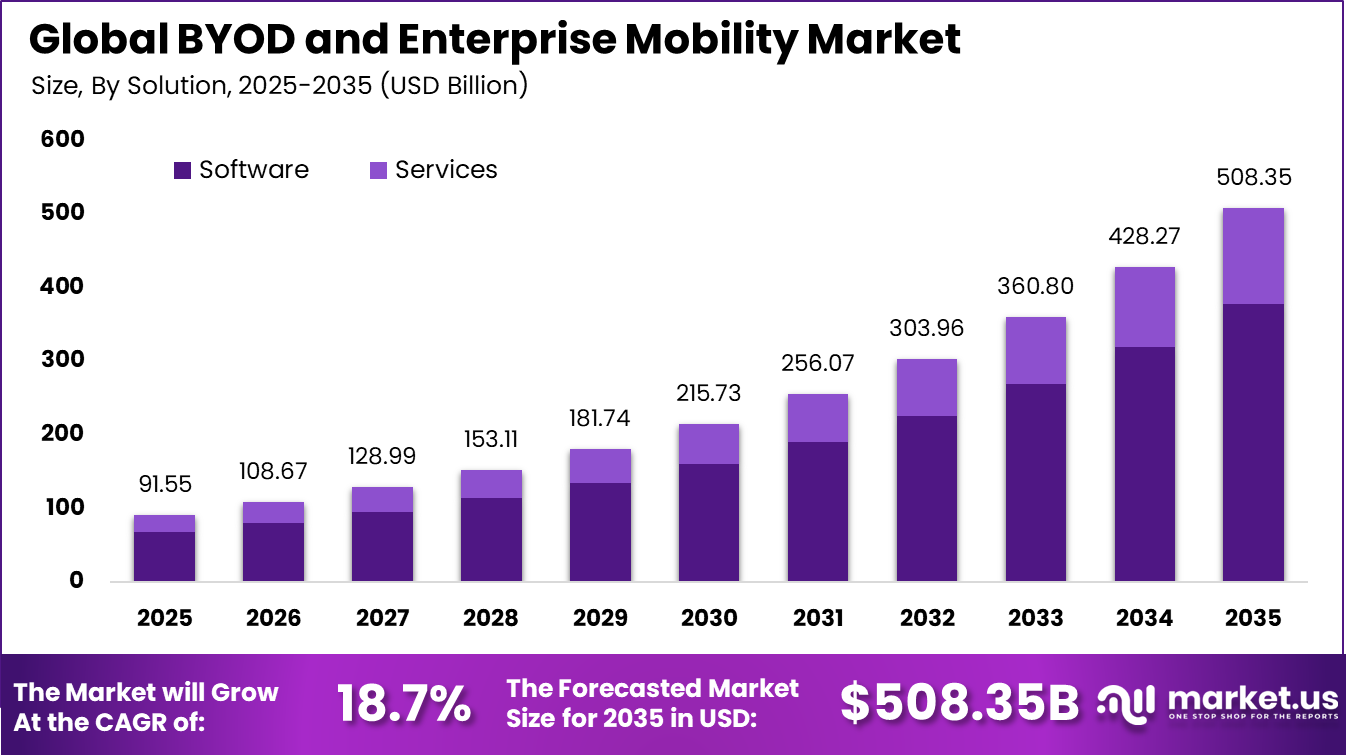

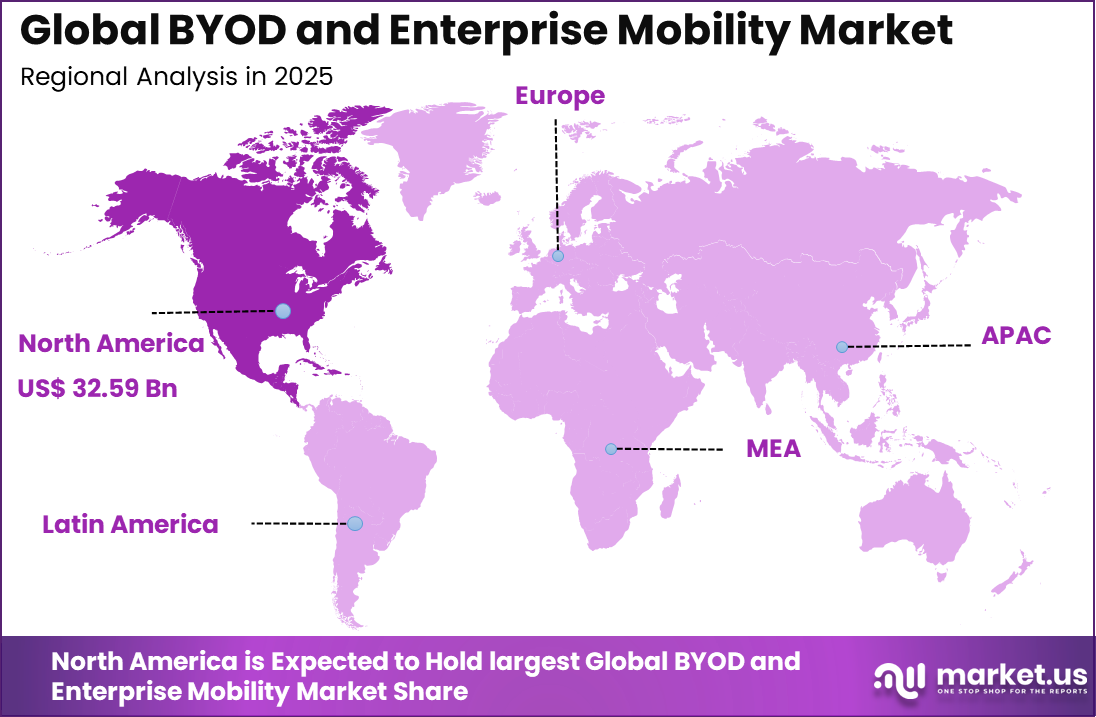

The Global BYOD And Enterprise Mobility Market size is expected to be worth around USD 508.35 billion by 2035, from USD 91.55 billion in 2025, growing at a CAGR of 18.7% during the forecast period from 2025 to 2035. North America held a dominant market position, capturing more than a 35.6% share, holding USD 32.59 billion in revenue.

The BYOD and Enterprise Mobility Market covers the policies, platforms, and services that allow employees to use personal devices for work while keeping business data protected. Adoption has been supported by hybrid work patterns, wider use of cloud applications, and the need to access business systems from anywhere. The market activity has increasingly been shaped by security requirements because personal devices often sit outside full corporate control.

Industry guidance has continued to stress that personally owned devices must be managed with clear controls across the full device lifecycle. BYOD and enterprise mobility let employees use their own smartphones, tablets, or laptops to access work systems. Today, more than 80% of organizations support personal device use for work, and around 70% have formal BYOD policies. This reflects how flexible work and remote access have become standard, with workers expecting secure access from anywhere at any time.

Flexible work options and a remote work culture are key drivers for BYOD and mobility. Nearly 50% of firms report rising demand due to remote work patterns and employees wanting to use familiar personal devices. Growing mobile internet and faster networks help people connect to business apps even outside the office.

Cost and operational flexibility have remained major drivers because BYOD can reduce the need to purchase and refresh full device fleets. In sector specific surveys, cost has been cited as a primary reason for BYOD adoption, and use of personal smartphones has been common where workforce mobility is high. These conditions have supported continued demand for enterprise mobility controls, especially in distributed workforces.

Demand for enterprise mobility is high because organizations see direct benefits. Allowing BYOD reduces the need to buy and manage many corporate devices. Younger workers especially expect mobile access as a basic feature of work. Surveys show that employers often save money and improve efficiency by permitting personal devices instead of issuing separate hardware for every employee.

For instance, in January 2026, HCL Technologies expanded its BYOD security offerings with new endpoint management tools for Asia-Pacific clients. Amid rapid digitalization, this positions HCL strongly in the fastest-growing region for enterprise mobility adoption.

Key Takeaway

- In 2025, the Software segment led the Global BYOD and Enterprise Mobility Market, accounting for 74.5% of total share.

- In 2025, Data Security emerged as the leading solution area, capturing 44.2% of the market.

- In 2025, On-Premises deployment remained dominant with a 65.7% share.

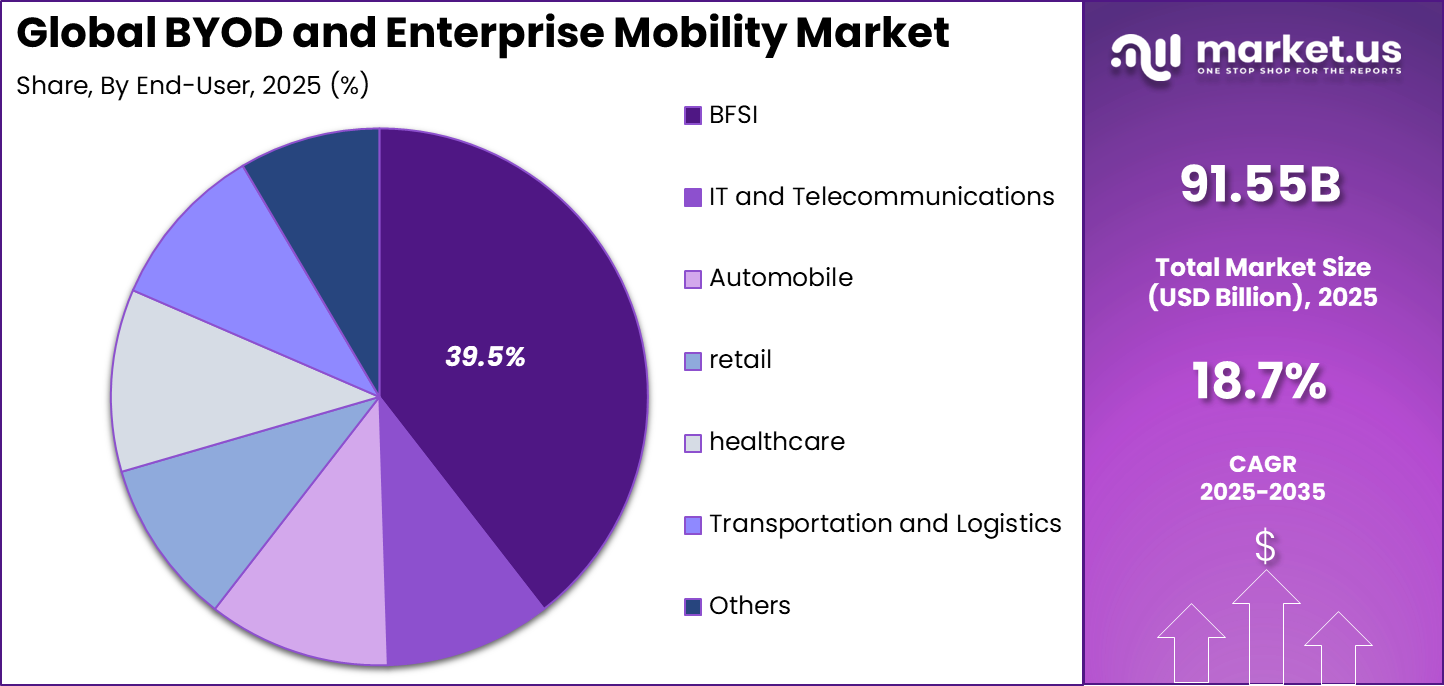

- In 2025, the BFSI sector represented the largest industry segment, contributing 39.5% of overall demand.

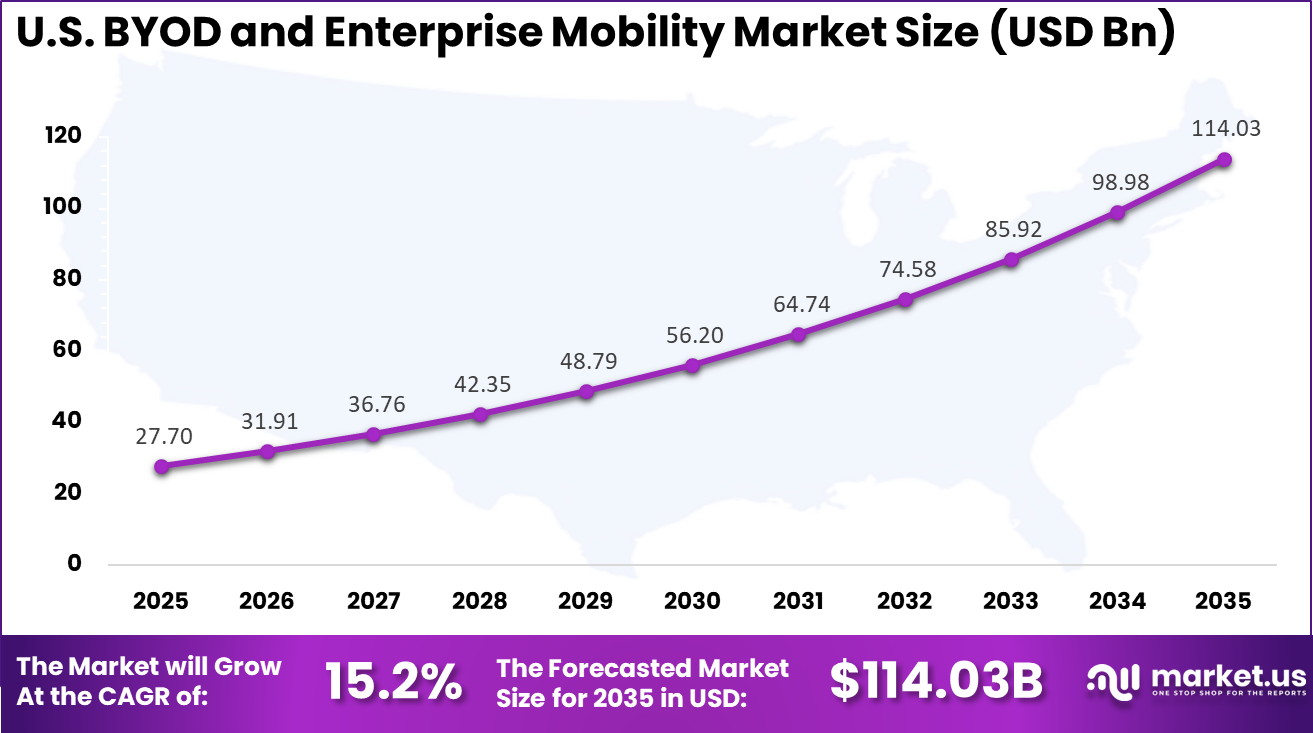

- In 2025, the U.S. BYOD and Enterprise Mobility Market reached USD 27.70 billion and recorded a strong growth rate of 15.2%.

- In 2025, North America maintained regional leadership, securing more than 35.6% of the Global BYOD and Enterprise Mobility Market.

Key BYOD & Enterprise Mobility Statistics

- More than 80% of organizations currently support or implement Bring Your Own Device policies.

- As of late 2024, about 67% of companies operate formal BYOD policies to manage security and compliance.

- Around 68% of organizations report measurable improvements in employee productivity through enterprise mobility programs.

- Employees using personal devices for work save nearly 58 minutes per day, reflecting a 34% increase in productivity.

- In the United States, 38% of workers used personal devices for work in 2023, up from 31% in 2022, indicating rising adoption of flexible work models.

By Solution: Software at 74.5%

Software dominance at 74.5% indicates that the main spending focus has been placed on control layers, not on devices themselves. Mobile device management, mobile application management, and identity linked access controls have typically been purchased as scalable software capabilities that can be applied across mixed device fleets. This structure has suited BYOD because device diversity is normal and control must be consistent across operating systems.

The value of software has also been reinforced by platform level separation features that lower privacy concerns while keeping work data controlled. Android work profiles have been designed to isolate work apps and data from personal apps, supporting safer adoption on employee owned devices. Apple’s account driven User Enrolment has been framed around managing only organisational accounts and settings, not personal data, which supports broader employee acceptance.

For Instance, in February 2026, Microsoft rolled out deeper Intune updates for software management in BYOD setups. These tools now handle app deployment across personal devices with less friction, helping IT teams keep software consistent. Firms love how it boosts productivity without constant oversight.

By Security: Data Security at 44.2%

Data security leadership at 44.2% reflects how enterprise mobility risk has moved beyond device loss and into data leakage, credential misuse, and human error. Breach reporting has continued to highlight that non malicious human actions play a large role in incidents and that extortion methods remain significant. This has increased demand for controls that keep work data inside managed apps and prevent unsafe sharing paths.

Controls are increasingly being implemented at the app layer because this is where business data is created, edited, and shared. App protection policies have been positioned to enforce encryption for organisational data, restrict copy and paste, and block saving to personal locations. Selective wipe capabilities have also been used to remove only business data when risk is detected, reducing disruption while protecting sensitive information.

For instance, in January 2026, Cisco sharpened its data encryption tools for BYOD setups, focusing on real-time threat blocks. These updates help lock down files on mixed-use phones and laptops, easing compliance worries. Teams now spot risks faster, making security feel less like a chore.

By Deployment Type: On Premises at 65.7%

On premises dominance at 65.7% indicates that a large share of buyers still prefer direct control over mobility infrastructure, policy enforcement, and sensitive data handling. This is often linked to regulated environments where data residency, auditability, and internal governance requirements are strict. It can also reflect integration needs with legacy identity systems and internal applications that remain within private environments.

Even in on premises settings, modern access patterns have shifted toward application specific access, rather than broad network exposure. Zero Trust Network Access has been presented as identity and context based access to specific applications, reducing unnecessary network reach. This approach can support on premises resources while still improving control for BYOD endpoints connecting from external networks.

For Instance, in January 2026, Oracle unveiled on-premises upgrades for mobility management early this year. It gives full control over local servers, perfect for firms dodging cloud uncertainties. Sticking with familiar setups helps scale BYOD safely, fueling this segment’s strength in regulated spaces where data stays house-bound.

By End User: BFSI at 39.5%

BFSI leadership at 39.5% is consistent with the sector’s high exposure to fraud, credential theft, and strict compliance requirements. Mobile access is often necessary for customer support, approvals, and internal workflows, but the data involved is highly sensitive. This combination has driven sustained investment in controlled mobility, strong authentication, and tight data handling rules across employee devices.

The economic impact of incidents has further strengthened mobility investment decisions in BFSI. IBM reporting has shown that breach costs in financial services can exceed the global average, which increases the value placed on prevention and rapid containment. As a result, BYOD programs in BFSI are often designed with tighter app controls, stronger identity checks, and fast selective wipe and response processes.

For Instance, in February 2026, Infosys announced BFSI-specific mobility tweaks this month, speeding up secure banking apps. It helps advisors handle deals from anywhere while meeting strict rules. This sector thrives on such innovations, as digital transactions boom and demand foolproof access on personal gear.

North America at 35.6%

North America leadership at 35.6% has been supported by early adoption of enterprise mobility governance and wider maturity in managed endpoint practices. Large scale hybrid workforces and cloud application usage have increased the need for consistent mobile access control across locations. This has typically resulted in multi layer programs that combine identity, device posture, and app level protection.

Security conditions have also reinforced demand because the region faces similar breach patterns tied to human action, credential misuse, and vulnerability exploitation. Verizon’s reporting has highlighted persistent human involvement in breaches and significant activity linked to exploitation and extortion. These patterns have supported ongoing funding for enterprise mobility controls that reduce data exposure from mobile endpoints.

For instance, in February 2026, Microsoft strengthened north america dominance in BYOD and Enterprise Mobility by enhancing Intune with advanced AI security features at MWC 2026, enabling seamless device management across hybrid workforces. This innovation reinforces North America’s leadership in secure enterprise mobility solutions.

U.S. Market Size

The market for BYOD and Enterprise Mobility within the U.S. is growing tremendously and is currently valued at USD 27.70 billion; the market has a projected CAGR of 15.2%. The market is growing strongly because companies are adapting to flexible work, and employees want to use personal devices for faster, easier access to systems.

Better mobile networks and cloud platforms make secure remote access simpler for IT teams. Organizations see lower hardware costs, improved collaboration, and higher worker satisfaction, which together drive more widespread adoption of BYOD and mobility solutions across industries.

For instance, in January 2026, Cisco expanded its enterprise mobility leadership with new Meraki updates featuring zero-trust networking for BYOD environments. The California-based giant continues powering secure North American corporate networks, reinforcing U.S. market dominance in mobile security infrastructure.

Emerging Trends Analysis

A key trend has been the move toward platform level privacy preserving BYOD enrolment, where separation between work and personal data is built into the operating system. Android work profiles and Apple account driven User Enrolment both support this direction by limiting what IT administrators can see and control while still protecting organisational data. This has reduced employee resistance and has made BYOD programs easier to scale.

Another trend has been stronger application specific access models that reduce broad network access from unmanaged endpoints. Zero Trust Network Access has been described as granting access to specific applications based on identity and context, which aligns with BYOD risk controls. This model is increasingly used alongside app protection policies to keep data inside approved apps while access decisions adapt to user and device conditions.

Growth Factors Analysis

Hybrid work and mobile first operations have been major growth factors because employees need secure access to enterprise services across changing locations. The more business processes move into collaboration tools and cloud platforms, the more value is created by consistent mobile access governance. This has driven continued investment in identity linked access and mobile app controls.

Rising breach costs have also supported market growth because the return on prevention has become easier to justify. IBM reporting has measured high breach costs at a global level and higher costs for financial services, which reinforces the need to reduce exposure across mobile endpoints. Investments that reduce leakage risk and shorten containment time have been prioritised as direct cost avoidance.

Key Market Segments

By Solution

- Software

- Data Management

- Email Management

- Application Management

- Device Management

- Others

- Services

- Managed Services

- Professional Services

By Security

- Data Security

- Email Security

- Network Security

- Identity Access Management

- Application Security

By Deployment Type

- Cloud

- On-Premises

By End-User

- BFSI

- IT and Telecommunications

- Automobile

- retail

- healthcare

- Transportation and Logistics

- Others

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Drivers

The main driver has been the need to protect organisational data accessed from devices that are not fully owned or fully controlled by the employer. Industry guidance has highlighted that personally owned deployment scenarios must be managed with suitable countermeasures across the device lifecycle. This has made enterprise mobility management an operational requirement rather than an optional upgrade.

This driver has strengthened as breach patterns continue to show high levels of human involvement and credential based compromise. Verizon reporting has repeatedly shown that human factors remain common in breaches and that extortion remains a major issue. As a result, mobility programs are often funded as part of broader risk reduction plans that focus on identity, access control, and data handling discipline.

For instance, in February 2026, Microsoft rolled out deeper Windows 11 ties with 5G tools to make laptops always connected for remote teams. This lets workers log in from anywhere using personal devices with smooth policy controls, easing IT work and fitting hybrid schedules. Staff gains reliable access without extra hardware, boosting daily flow in spread-out offices.

Restraint

A key restraint has been the complexity of managing diverse endpoints while maintaining employee trust and privacy. BYOD programs can fail to scale when employees do not understand policies or when governance is inconsistent across business units. Surveys in specific sectors have shown that BYOD usage can be widespread even where formal policies are missing or not well understood.

Security teams also face visibility limits when devices are not enrolled or are only partially managed, which can increase exposure to credential compromise and unsafe app use. Where unmanaged access persists, policy enforcement can be incomplete and incident response can become slower. This restraint has pushed organisations toward app level protections and platform supported separation rather than heavy device control.

For instance, in January 2026, BlackBerry updated its device software to tackle risks from mixed personal and work data on one phone. The fix adds stronger walls around files to stop leaks from weak setups or lost units. Companies now feel safer rolling out BYOD as it cuts worry over private info slipping out.

Opportunities

A clear opportunity exists in expanding app level data protection for organisations that cannot fully enrol personal devices. App protection policies have been positioned to protect organisational data on both enrolled and unenrolled devices, which matches real BYOD adoption behaviour. This creates a large upgrade path from informal BYOD usage to controlled BYOD usage without forcing full device control.

Another opportunity is the shift from network based remote access toward application specific access controls. Zero Trust Network Access has been presented as limiting access to specific applications based on identity and context, which reduces unnecessary exposure. This approach supports a cleaner security posture for mixed fleets and can reduce operational load compared with older remote access patterns.

For instance, in December 2025, SAP enhanced its cloud suite with role checks that let workers use their own devices via simple ID scans. This opens doors for quick team shares without heavy installs. Businesses grab this to scale access fast, drawing folks who want easy logins anywhere.

Challenges

A major challenge is keeping security controls effective while avoiding user pushback that leads to policy avoidance. When controls are too intrusive, employees may work around them using personal email, personal storage, or unapproved apps, which increases risk. This challenge has made privacy preserving platform separation models and app targeted controls more important for long term compliance.

Another challenge is the ongoing pace of attacker methods, including phishing, credential theft, and exploitation driven entry points. Verizon reporting has shown continuing human involvement in breaches and strong levels of exploitation and extortion activity. Enterprise mobility programs must therefore keep improving user training, access checks, and rapid response processes, not only device configuration.

For instance, in October 2025, Accenture highlighted management headaches from tablet and phone variety in a workshop series. IT groups chase patches for old versions that break features. Firms face rising calls for help, shifting focus from core tasks to endless tweaks.

Key Players Analysis

Competition is shaped by vendors that can provide end to end mobility coverage across identity, device management, application controls, and secure access. Microsoft has been closely associated with app protection policies and conditional access aligned controls that support BYOD without full device enrolment, which can appeal to mixed device fleets. Cisco has positioned Zero Trust Network Access as application specific access based on identity and context, supporting stronger control for remote and mobile endpoints.

IBM, SAP, Oracle, and Infosys have been more visible in mobility programs that connect endpoint governance with enterprise applications, identity systems, and security operations practices. This positioning is often valued in large organisations where mobility must align with broader risk management and audit needs. Honeywell’s relevance is often stronger where mobility connects with operational environments and frontline workflows, where device reliability and controlled access are critical.

BlackBerry, Accenture, Capgemini, and HCL Technologies have tended to compete through security focused mobility offerings, deployment support, and managed services, especially for complex multi year enterprise programs. In many deals, differentiation is created through integration capability, policy governance design, and ongoing operations rather than a single technical feature.

Top Key Players in the Market

- Microsoft

- Cisco Systems, Inc.

- BlackBerry Limited

- Infosys Limited

- IBM Corporation

- SAP SE

- Honeywell International Inc.

- Capgemini

- Accenture

- HCL Technologies Limited

- Oracle Corporation.

- Others

Recent Developments

- In January 2026, IBM enhanced its enterprise mobility stack with new zero-trust features for BYOD environments. Drawing from its MobilityFirst push, the updates focus on AI-driven device management, helping firms secure personal devices without stifling employee flexibility.

- In December 2025, Honeywell launched updated IoT mobility solutions tailored for industrial BYOD, featuring edge computing for secure field operations. This bolsters worker safety and efficiency in manufacturing, extending Honeywell’s edge in rugged enterprise environments.

Report Scope

Report Features Description Market Value (2025) USD 91.5 Bn Forecast Revenue (2035) USD 508.3 Bn CAGR (2026-2035) 18.7% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends Segments Covered By Solution (Software, Services), By Security (Data Security, Email Security, Network Security, Identity Access Management, Application Security), By Deployment Type (Cloud, On-Premises), By End-User (BFSI, IT and Telecommunications, Automobile, Retail, Healthcare, Transportation and Logistics, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Microsoft, Cisco Systems, Inc., BlackBerry Limited, Infosys Limited, IBM Corporation, SAP SE, Honeywell International Inc., Capgemini, Accenture, HCL Technologies Limited, Oracle Corporation, Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  BYOD and Enterprise Mobility MarketPublished date: Feb. 2026add_shopping_cartBuy Now get_appDownload Sample

BYOD and Enterprise Mobility MarketPublished date: Feb. 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Microsoft

- Cisco Systems, Inc.

- BlackBerry Limited

- Infosys Limited

- IBM Corporation

- SAP SE

- Honeywell International Inc.

- Capgemini

- Accenture

- HCL Technologies Limited

- Oracle Corporation.

- Others

Our Clients

- 179620

- Feb. 2026