Global Automotive Wrap Films Market By Type (Calendered and Cast), By Finish (Gloss, Matte, Chrome, Metallic, Carbon Fiber, and Others), By Application (Full Body Wrap, Partial Body Wrap, and Others), By Propulsion Type (Internal Combustion Engines, Electric Vehicles, and Hybrid), By Vehicle Type (Passenger Cars and Commercial Vehicles), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2035

- Published date: Feb 2026

- Report ID: 179780

- Number of Pages: 369

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

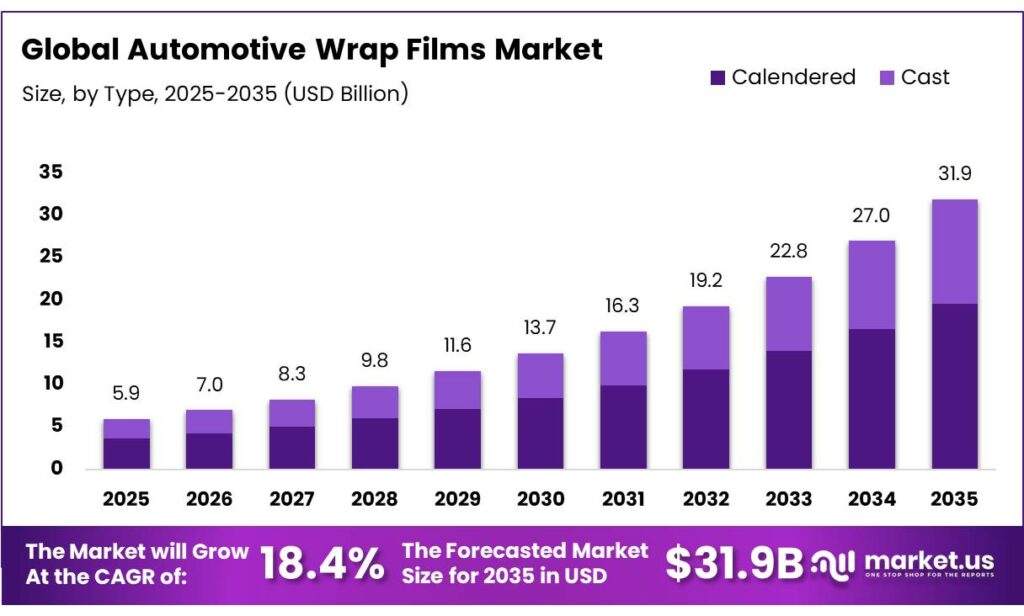

The Global Automotive Wrap Films Market is expected to be worth around USD 31.9 Billion by 2035, up from USD 5.9 Billion in 2025, at a CAGR of 18.4% from 2026 to 2035. The Asia Pacific segment maintained 48.9%, supporting a Magnesium value of USD 2.8 Bn.

Automotive wrap films are thin, adhesive-backed layers made primarily of polyvinyl chloride (PVC) polymer that are applied directly over a vehicle’s original paint to change its appearance and provide surface protection. These films act as a second skin, allowing for complete color transformations or custom graphic designs without the permanence or high cost of a professional repaint. The market is driven by growing demand for vehicle customization, advertising, and protection.

Passenger cars are the largest segment, with consumers seeking aesthetic enhancement through full-body wraps, particularly glossy finishes that offer versatility, ease of maintenance, and vibrant appeal. Additionally, commercial fleets use wraps for branding, benefiting from their cost-effectiveness in advertising. Calendered automotive wrap films are more widely used than cast films due to their lower cost and ease of application, especially for larger fleets.

However, challenges such as installation complexity and labor shortages impact the market, as skilled installers are essential for achieving high-quality results. Similarly, the market is influenced by sustainability trends, with manufacturers exploring non-PVC, eco-friendly alternatives. Despite these challenges, the North American market remains dominant due to its robust automotive aftermarket sector and demand for customization.

Key Takeaways

- The global automotive wrap films market was valued at USD 5.9 billion in 2024.

- The global automotive wrap films market is projected to grow at a CAGR of 18.4% and is estimated to reach USD 31.9 billion by 2034.

- On the basis of types, calendered automotive wrap films dominated the market, constituting 61.3% of the total market share.

- Based on the finish, glossy automotive wrap films dominated the market, with a substantial market share of around 34.3%.

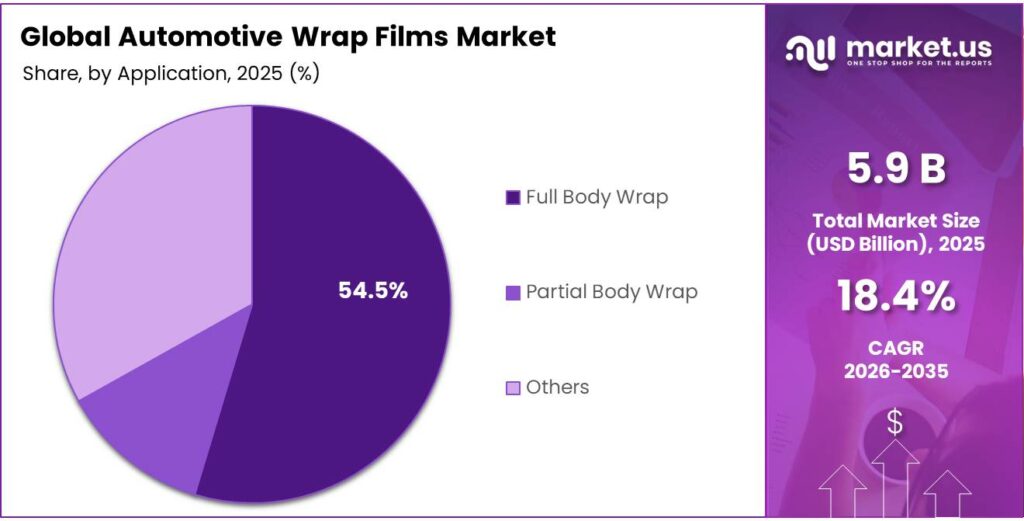

- Based on the applications, full body wraps led the market, comprising 54.5% of the total market.

- Among the propulsion types, internal combustion engine vehicles held a major share in the automotive wrap films market, 86.3% of the market share.

- Among the vehicle types, passenger cars are the most considerable within the market, accounting for around 64.1% of the revenue.

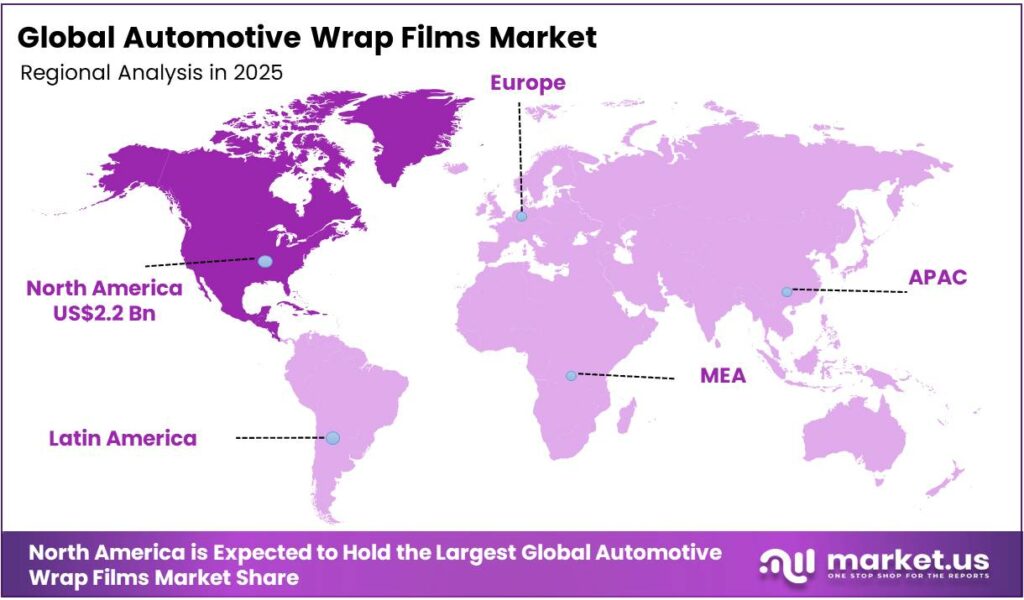

- In 2024, North America was the most dominant region in the automotive wrap films market, accounting for 37.6% of the total global consumption.

Type Analysis

Calendered Automotive Wrap Films are a Prominent Segment in the Market.

The market is segmented based on types of automotive wrap films into calendered and cast. The calendared automotive wrap films led the market, comprising 61.3% of the market share, primarily due to their cost-effectiveness and easier production process. Calendered films are made by passing vinyl material through rollers, which stretches the material and makes it more affordable to produce at scale.

This makes calendered wraps an attractive option for large vehicle fleets and budget-conscious customers. While cast films offer superior durability and flexibility, calendered films meet the needs of many users who prioritize affordability over long-term performance. They are well-suited for flat or moderately curved surfaces, making them ideal for widespread use in applications such as commercial fleet branding. Additionally, calendered wraps are easier to handle and apply for installers, contributing to their greater adoption.

Finish Analysis

Glossy Automotive Wrap Films Dominated the Automotive Wrap Films Market.

On the basis of finish, the automotive wrap films market is segmented into gloss, matte, chrome, metallic, carbon fiber, and others. The glossy automotive wrap films dominated the market, comprising 34.3% of the market share, due to their versatility, visual appeal, and ease of maintenance. Glossy finishes provide a clean, sleek look that enhances the natural shine of the vehicle, making them popular for a broad range of automotive customization needs.

Additionally, this finish tends to highlight the vehicle’s contours and body lines more effectively, offering a vibrant, attention-grabbing effect. Similarly, glossy films are easier to clean, which makes them a preferred option for users looking for low-maintenance yet visually striking outcomes.

In contrast, other finishes, such as matte or chrome, require more careful maintenance, as they can be prone to fingerprints, scratches, and surface wear. Additionally, glossy films are often more cost-effective to produce and install compared to specialized finishes such as carbon fiber or metallic wraps, contributing to their widespread use.

Application Analysis

Full Body Wrap Films Are the Most Widely Utilized Automotive Wrap Films.

The full body wrap films services dominated the automotive wrap films market, with a notable market share of 54.5%, due to their comprehensive coverage and enhanced aesthetic impact. A full body wrap provides complete customization, transforming the entire vehicle’s appearance with a seamless finish, which is particularly appealing for personal vehicle owners and commercial fleets seeking a bold, cohesive look.

Additionally, it offers more branding space for companies and ensures a uniform appearance, making it highly attractive for advertising purposes. Similarly, full-body wraps provide better protection against environmental damage, such as UV rays, dirt, and scratches, as they cover all surfaces. Similarly, they offer long-term durability and a smoother, more consistent application compared to partial wraps, which may risk mismatched sections or visible lines.

Propulsion Type Analysis

Internal Combustion Engine Vehicles Held a Major Share of the Automotive Wrap Films Market.

Based on propulsion types, the automotive wrap films market is segmented into internal combustion engines, electric vehicles, and hybrid vehicles. Among the propulsion types, 86.3% of the automotive wrap films consumed globally are by internal combustion engine vehicles. ICE vehicles make up the majority of the global vehicle fleet, resulting in higher demand for customization. These vehicles are more prevalent in the aftermarket sector, where wraps are often used for aesthetic changes, branding, or fleet marketing.

In contrast, electric and hybrid vehicles, while growing in popularity, represent a smaller portion of the market. Additionally, EV and hybrid owners often focus on long-term sustainability, which may include eco-friendly modifications and paint protection rather than aesthetic customization. Furthermore, as electric vehicles (EVs) generally feature modern, sleek designs, some owners may feel less need for wraps compared to traditional vehicles.

Vehicle Type Analysis

Automotive Wrap Films Services Are Mostly Utilized by Passenger Cars.

Among the vehicle types, 64.1% of the total global consumption of automotive wrap films is utilized by passenger cars, primarily due to differences in customization needs and usage patterns. Passenger car owners often prioritize aesthetics and personalization, seeking unique designs, colors, and finishes, which wraps can easily provide. This trend aligns with the growing desire among consumers to distinguish their vehicles.

In contrast, commercial vehicles typically focus more on practicality and functionality, with wraps primarily used for branding and advertising rather than customization. The designs on commercial vehicles are often simple, logo-based, and focused on visibility, not aesthetic variation. Additionally, passenger cars generally have more complex, curved surfaces that benefit from the diverse wrap options available, whereas the large, utilitarian surfaces of commercial vehicles may not require the same level of decorative wrap usage.

Key Market Segments:

By Type

- Calendered

- Cast

By Finish

- Gloss

- Matte

- Chrome

- Metallic

- Carbon Fiber

- Others

By Application

- Full Body Wrap

- Partial Body Wrap

- Others

By Propulsion Type

- Internal Combustion Engines

- Electric Vehicles

- Hybrid

By Vehicle Type

- Passenger Cars

- Hatchback

- Sedan

- SUV

- Others

- Commercial Vehicles

- Light Duty

- Heavy Duty

Drivers

Vehicle Customization and Paint Protection Films (PPF) Drive the Automotive Wrap Films Market.

Vehicle customization and paint protection films (PPF) are pivotal factors driving growth in the automotive wrap films market. The increasing demand for vehicle personalization has spurred the popularity of wraps, especially among consumers seeking unique aesthetics and protection. Wraps offer cost-effective alternatives to traditional painting, providing high-quality, customizable finishes with minimal downtime.

Additionally, PPF is gaining traction due to its ability to protect vehicle surfaces from environmental damage, scratches, and fading. The PPF products are especially popular in regions with harsh climates, including areas with high UV exposure, where vehicles are more prone to damage. Furthermore, regulatory bodies such as the National Highway Traffic Safety Administration have noted that wraps and films do not hinder vehicle safety standards, promoting their adoption in consumer vehicles.

Similarly, the traditional boundary between color-change vinyl and protective film is dissolving. Leveraging the trend, several market leaders have introduced color PPF, which integrates aesthetic variety with functional protection. For instance, XPEL launched a collection in 2025 featuring 16 colors using multi-layer polyurethane designed to resist oxidation and road debris.

Restraints

Installation Complexity and Labor Shortages Pose Challenges to the Automotive Wrap Films Market.

Installation complexity and labor shortages represent significant structural barriers to the automotive wrap films market, characterized by a widening gap between material innovation and technical proficiency. Modern films require advanced handling of complex curves, film repositioning, and precision trimming.

The process demands specialized skills, as improper application can result in wrinkles, bubbles, and peeling, reducing the longevity of the film. For instance, the International Carwash Association notes that wraps require professional installation, which increases both time and cost for consumers.

Labor shortages exacerbate this issue, particularly in regions with high demand for customization. According to the U.S. Bureau of Labor Statistics, the automotive service industry experienced a 20% decline in skilled workers over five years till 2022. This shortage delays wrap installations and increases operational costs, further limiting the scalability of wrap services.

These challenges have prompted industry leaders, such as 3M, to invest in technician training programs to address skill gaps in the workforce. 3M emphasizes that their professional-grade certifications, such as 3M Preferred Installer, require rigorous multi-day training and are not intended for entry-level workers.

Opportunity

Commercial Fleet Branding and Advertising Creates Opportunities in the Automotive Wrap Films Market.

Commercial fleet branding and advertising represent a primary growth opportunity for the automotive wrap films market, driven by high impression rates and lower comparative costs. The use of vehicle wraps in commercial fleets has increased due to their effectiveness in enhancing brand visibility. Unlike stationary advertisements, wrapped vehicles serve as mobile billboards.

A study by the Outdoor Advertising Association of America (OAAA) indicates that a single vehicle wrap can generate between 30,000 and 70,000 daily impressions, depending on the traffic areas. In intra-city environments, a single truck can generate up to 16 million annual visual impressions. In addition, mobile advertising achieves a 97% message recall rate, significantly higher than the 19% recall for stationary advertisements.

Furthermore, automotive wraps offer the lowest cost-per-thousand impressions (CPM) among out-of-home (OOH) options compared to billboards and newspaper ads. The automotive wrap industry’s growth is directly tied to this trend, with many companies adopting wraps for brand recognition and direct marketing in urban environments.

Trends

Shift Towards Sustainable and Non-PVC Materials.

The shift toward sustainable and non-PVC (polyvinyl chloride) materials is a primary technical trend in the automotive wrap market, driven by regulatory pressure on substances of concern and corporate ESG (Environmental, Social, and Governance) targets. The U.S. Environmental Protection Agency (EPA) highlighted concerns over the environmental impact of PVC-based products, particularly in terms of toxicity and landfill waste.

Consequently, manufacturers are increasingly adopting eco-friendly alternatives. For instance, 3M’s Envision series utilizes a non-PVC, phthalate-free polymer that is GREENGUARD Gold certified, and is engineered with 47% bio-based materials and offers higher tensile strength to prevent tearing during removal. Similarly, Avery Dennison expanded its sustainable portfolio in 2024 with the SP 1504 Easy Apply RS, a PVC-free digital print film designed for large-scale fleet branding.

Furthermore, the European Union’s REACH regulations have prompted the automotive sector to adopt safer, more sustainable materials, including biodegradable and recyclable films. The shift is further fueled by growing consumer demand for eco-conscious products. Many automotive wrap suppliers are now exploring or implementing sustainable options in their offerings, indicating a clear trend towards reduced reliance on traditional PVC materials in the market.

Geopolitical Impact Analysis

Geopolitical Tensions Have Led to Increased Prices of Automotive Wrap Films.

The geopolitical tensions are influencing the automotive wrap films market, primarily through disruptions in global supply chains and material shortages. The trade restrictions and tariffs have impacted the availability of key raw materials, such as PVC and petrochemical-based products, which are essential for producing automotive wrap films.

For instance, in January 2025, the European Commission imposed definitive anti-dumping duties of 58-100% on PVC from the U.S. and Egypt. Similarly, under Section 301, the U.S. implemented a 25% tariff on strategic Chinese goods, including chemicals and plastics, effective late 2024 with further increases through 2026.

Furthermore, the ongoing conflict in Eastern Europe has further exacerbated the issue, with disruptions in the supply of energy and raw materials from the region. Consequently, there is a 15% reduction in the availability of certain petrochemical derivatives, affecting film production capabilities.

Additionally, geopolitical instability has led to inflationary pressures on material costs. These cost increases, along with uncertainty in international logistics, have prompted manufacturers to reconsider sourcing strategies, as evidenced by shifting procurement patterns in response to trade restrictions and rising fuel prices.

Such disruptions affect the timeline for product delivery and installation, which can delay projects and increase operating costs for companies relying on automotive wraps for advertising and fleet branding.

Regional Analysis

North America Held the Largest Share of the Global Automotive Wrap Films Market.

In 2024, North America dominated the global automotive wrap films market, holding about 37.6% of the total global consumption, driven by consumer demand for vehicle customization and commercial fleet branding. Over 30% of vehicles in the U.S. are customized in some form, contributing to the growing preference for wraps as an alternative to traditional paint. Furthermore, the demand for vehicle wraps is particularly strong among commercial fleets, with approximately 14.89 million single-unit (2-axle, 6-tire or more) and combination trucks registered in 2023 in the US.

In addition, regulatory support, such as the Federal Motor Vehicle Safety Standards, allows for the widespread use of wraps without compromising vehicle safety, further driving adoption. North America’s extensive automotive aftermarket sector further facilitates wrap installations. The region’s robust infrastructure for skilled labor and material supply contributes to its position as a leader in the automotive wrap films market.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis:

Manufacturers of automotive wrap films focus on continuous innovation in material technology, such as developing non-PVC, eco-friendly wraps that align with increasing environmental concerns. For instance, some manufacturers are incorporating self-healing and scratch-resistant properties into their films to improve durability and reduce maintenance costs. Additionally, companies invest in expanding their distribution networks and establishing partnerships with automotive service providers to ensure easier access for consumers.

Training and certification programs for installers are another critical area, ensuring high-quality applications and customer satisfaction. Manufacturers further prioritize product customization options, allowing customers to select from a wide range of colors, textures, and finishes to suit personal or branding needs. Moreover, many companies focus on geographic expansion, targeting emerging markets with growing automotive customization trends.

The major players in the industry

- Avery Dennison Corporation

- 3M Company

- Arlon Graphics, LLC

- HEXIS S.A.S.

- KPMF

- Fedrigoni S.P.A.

- WrapMaster

- ORAFOL Europe GmbH

- Eastman Chemical Company

- Teckwrap International

- CARBINS Film

- Metamark

- INOZETEK

- Rvinyl

- Other Key Players

Key Development:

- In October 2025, Avery Dennison Graphics Solutions announced the launch of its neo matte black paint protection film, a highly anticipated addition to its premium line of wet-apply color PPFs. The product complemented its successful neo noir gloss black PPF, offering installers and automotive enthusiasts two of the most sought-after black finishes.

- In September 2024, KPMF partnered with Spandex to expand the availability of its VWS IV (Vehicle Wrapping System) range, offering over 100 color options with next-day delivery for wrap professionals in the UK.

Report Scope:

Report Features Description Market Value (2024) US$5.9 Bn Forecast Revenue (2034) US$31.9 Bn CAGR (2025-2034) 18.4% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Calendered and Cast), By Finish (Gloss, Matte, Chrome, Metallic, Carbon Fiber, and Others), By Application (Full Body Wrap, Partial Body Wrap, and Others), By Propulsion Type (Internal Combustion Engines, Electric Vehicles, and Hybrid), By Vehicle Type (Passenger Cars and Commercial Vehicles) Regional Analysis North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA Competitive Landscape Avery Dennison Corporation, 3M Company, Arlon Graphics, LLC, HEXIS S.A.S., KPMF, Fedrigoni S.P.A., WrapMaster, ORAFOL Europe GmbH, Eastman Chemical Company, Teckwrap International, CARBINS Film, Metamark, INOZETEK, Rvinyl, and Other Players. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Automotive Wrap Films MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample

Automotive Wrap Films MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Avery Dennison Corporation

- 3M Company

- Arlon Graphics, LLC

- HEXIS S.A.S.

- KPMF

- Fedrigoni S.P.A.

- WrapMaster

- ORAFOL Europe GmbH

- Eastman Chemical Company

- Teckwrap International

- CARBINS Film

- Metamark

- INOZETEK

- Rvinyl

- Other Key Players

Our Clients

- 179780

- Feb 2026