Quick Navigation

Report Overview

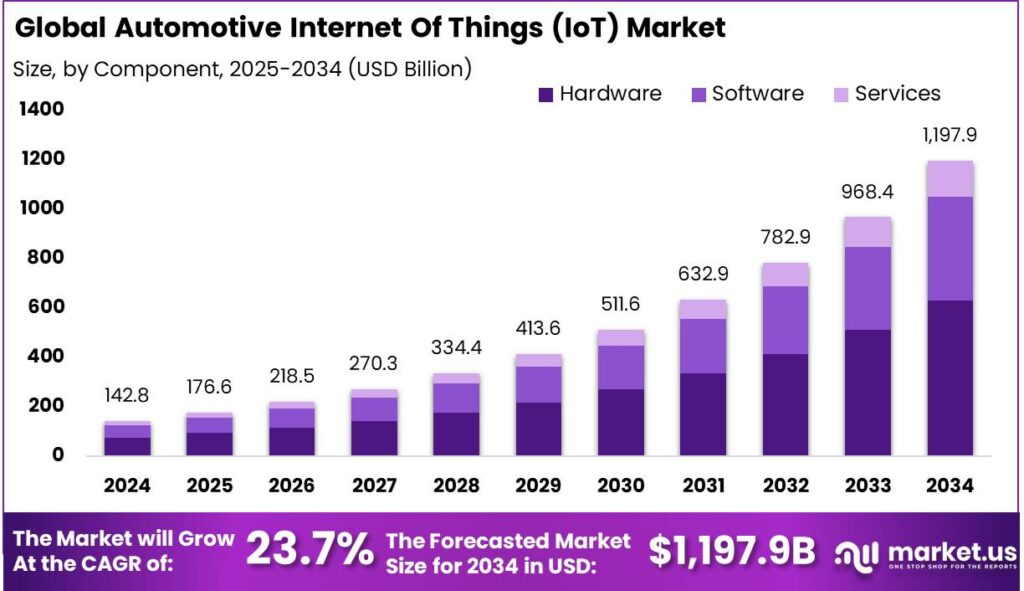

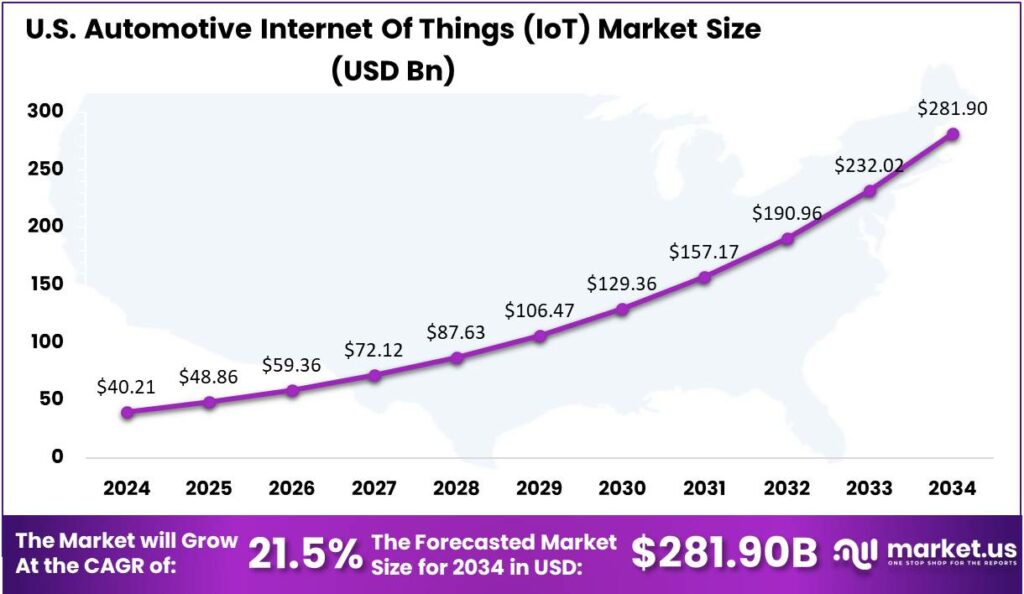

The Automotive IoT Market size is expected to be worth around USD 1,197.9 Bn By 2034, from USD 142.8 Bn in 2024, growing at a CAGR of 23.70% during the forecast period from 2025 to 2034. In 2024, North America dominated the Automotive IoT market with over 35.2% market share, generating USD 50.2 bn in revenue. The U.S. market reached USD 40.21 bn and is expected to grow at a CAGR of 21.5%.

Automotive Internet of Things (IoT) refers to the integration of connected devices, sensors, and software within vehicles to enhance performance, safety, and the overall driving experience. This technology allows vehicles to communicate with each other and with infrastructure, enabling advanced functionalities like real-time traffic alerts, vehicle diagnostics, and predictive maintenance.

The Automotive IoT market is experiencing significant growth, driven by the increasing demand for connected vehicles and smart transportation solutions. This market encompasses a range of applications, including autonomous driving, V2X communication, and in-vehicle infotainment systems. The proliferation of high-speed internet technologies and the expansion of automotive manufacturing capabilities are key factors propelling this market forward.

The primary drivers of the Automotive IoT market include the growing consumer demand for enhanced vehicle safety, improved fuel efficiency, and superior driving experiences. The proliferation of telematics, smart gadget integration, and in-car infotainment systems also significantly contribute to market expansion.

Technological advancements in connectivity, such as 5G and edge computing, further propel this market growth. Current demand in the Automotive IoT sector is robust, driven by consumer expectations for connected and autonomous vehicles. The integration of IoT devices in automotive manufacturing is increasing, fueled by the need for data-driven decision-making and operational efficiency.

As technology costs decrease and software capabilities expand, demand is expected to grow, particularly in emerging markets. The market is set to expand further as advancements in 5G technology and machine learning algorithms enhance the capabilities of IoT devices in vehicles. This expansion is expected to bring new features and services, reshaping the relationship between automakers and drivers, and setting new standards in the industry’s shift towards fully autonomous driving.

Key Takeaways

- The Global Automotive Internet Of Things (IoT) Market size is expected to reach USD 1,197.9 Billion by 2034, up from USD 142.8 Billion in 2024, growing at a CAGR of 23.70% during the forecast period from 2025 to 2034.

- In 2024, the Hardware segment held a dominant position in the Automotive IoT market, capturing more than 52.7% of the market share.

- In 2024, the Embedded segment held a dominant market position within the Automotive IoT market, capturing more than 38.6% of the market share.

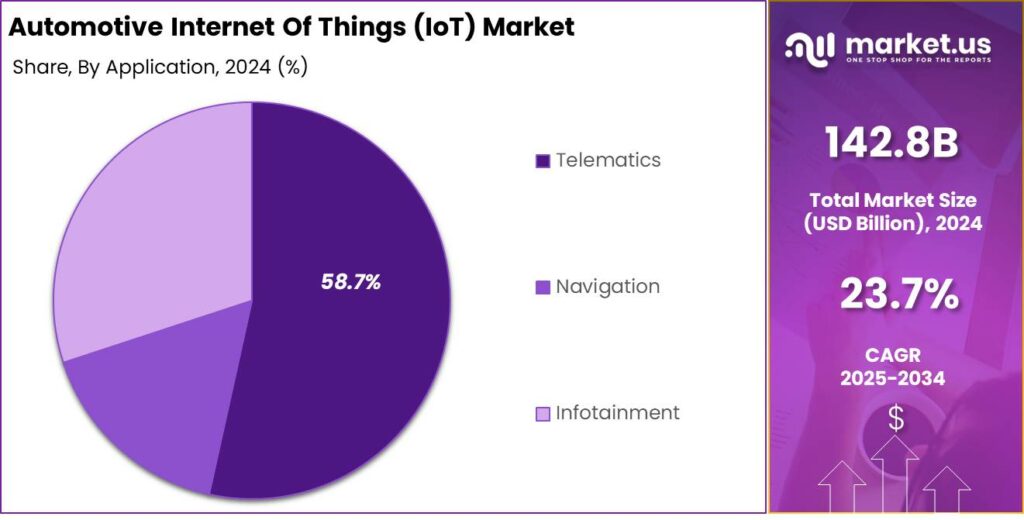

- In 2024, the Telematics segment held a dominant market position within the Automotive IoT industry, capturing more than 58.7% of the market share.

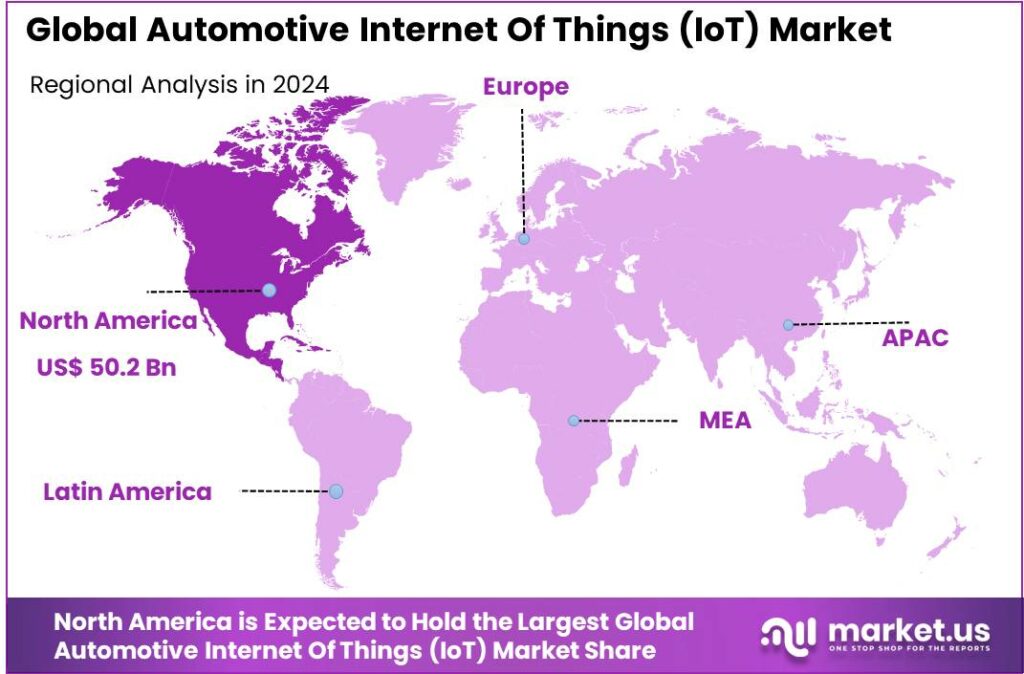

- In 2024, North America held a dominant market position in the Automotive IoT sector, capturing more than 35.2% of the market share, with revenues up to USD 50.2 billion.

- In 2024, the U.S. Automotive IoT market reached a valuation of USD 40.21 billion, and it is projected to expand at a CAGR of 21.5%.

Analysts’ Viewpoint

Key factors impacting the Automotive IoT market include technological advancements, cybersecurity concerns, and the global semiconductor shortage. Additionally, consumer privacy issues and the need for standardized protocols across different regions and manufacturers play significant roles in shaping market dynamics.

The adoption of IoT in the automotive industry offers numerous business benefits, including enhanced operational efficiency, reduced maintenance costs, and improved customer satisfaction. Automakers are leveraging IoT to gain real-time insights into vehicle performance and user behavior, enabling proactive service offerings and optimized product development.

The regulatory environment for Automotive IoT is evolving, with increased emphasis on safety, data protection, and environmental impact. Governments worldwide are implementing standards and policies to ensure secure and reliable vehicle communication systems. These regulations also aim to foster innovation while addressing the challenges posed by such disruptive technologies.

U.S. Market Growth

In 2024, the U.S. Automotive Internet of Things (IoT) market reached a valuation of USD 40.21 billion. This market is projected to expand at a compound annual growth rate (CAGR) of 21.5%.

The U.S. Automotive IoT market is experiencing robust growth due to several key factors. A major driver is the growing demand for improved vehicle connectivity and telematics, enhancing safety, maintenance, and user experience. As automotive manufacturers adopt advanced technologies like autonomous driving and predictive maintenance, IoT solutions are becoming integral to the industry.

The growth of the Automotive IoT sector is also driven by the rise of electric vehicles (EVs). IoT devices help monitor battery performance, ensuring efficient energy use and longer battery life. Government incentives promoting EV adoption further support IoT expansion. As the market evolves, new opportunities will emerge for applications and services that improve vehicle performance and passenger experience.

In 2024, North America held a dominant market position in the Automotive Internet of Things (IoT) sector, capturing more than a 35.2% share with revenues amounting to USD 50.2 billion. This leading position can be attributed to several key factors that drive the integration of IoT technologies in the automotive industry across the region.

North America’s advanced technological infrastructure and the presence of major automotive players like General Motors, Ford, and Tesla, alongside tech giants such as Google and Apple, foster IoT innovation and adoption. The region’s automotive industry, with its high levels of vehicle connectivity and automation, provides a strong foundation for IoT advancements.

Additionally, regulatory support in the U.S. and Canada has significantly propelled the market forward. Regulations and government initiatives aimed at enhancing road safety and reducing vehicle emissions encourage manufacturers to incorporate IoT technologies that support these goals.

Additionally, North America’s robust wireless network infrastructure and the push towards 5G technology provide the bandwidth and security needed to handle the large data transfers in automotive IoT. This foundation enables real-time data processing and communication, while also paving the way for future innovations in the automotive sector.

Component Analysis

In 2024, the Hardware segment held a dominant position in the Automotive Internet of Things (IoT) market, capturing more than 52.7% of the market share. This leadership can be attributed to the essential role that physical devices such as sensors, onboard computers, and connectivity modules play in enabling IoT functionality within vehicles.

The prominence of the Hardware segment is further reinforced by continuous advancements in sensor technology and vehicle telematics. Automakers are increasingly investing in sophisticated sensors that provide critical data for safety features, such as collision avoidance systems and automatic emergency braking.

The Hardware segment’s dominance is driven by the integration of connectivity modules that enable communication between vehicles and external networks. This supports features like real-time traffic updates, remote diagnostics, and cloud services, essential for connected and autonomous vehicles requiring reliable data exchange.

Regulatory pressures and safety standards are driving the adoption of technologies that rely on hardware components. Stricter regulations require vehicles to have advanced safety systems, increasing the demand for high-performance automotive IoT hardware. This regulatory environment ensures continued investment in hardware development, solidifying its dominance in the Automotive IoT market.

System Analysis

In 2024, the Embedded segment held a dominant market position within the Automotive Internet of Things (IoT) market, capturing more than a 38.6% share. This segment leads primarily due to its ability to provide robust and reliable connectivity solutions that are essential for the seamless operation of advanced vehicle systems.

The Embedded segment’s superiority lies in its direct integration with vehicle hardware, enabling deeper customization and control. This creates a cohesive interface between internal functions and external communications, providing a stable platform for seamless digital experiences and enhancing user engagement through advanced telematics and infotainment systems.

The Embedded segment also benefits from long-term partnerships between automakers and tech companies, driving the development of advanced, tailored IoT solutions. These collaborations allow the integration of cutting-edge IoT technologies into vehicles from the manufacturing stage, ensuring systems are optimized for the vehicle’s specifications.

Regulatory influences play a key role in strengthening the Embedded segment. Stricter safety and emissions regulations push automakers to adopt reliable, compliant IoT solutions. Embedded systems, with their superior data handling and integration, are better suited to meet these regulations, ensuring their continued dominance in the Automotive IoT market.

Application Analysis

In 2024, the Telematics segment held a dominant market position within the Automotive Internet of Things (IoT) industry, capturing more than a 58.7% share. This substantial market share can be attributed to several pivotal factors that underscore the importance of telematics in modern automotive applications.

Telematics systems, which combine telecommunications and informatics, are increasingly integral to enhancing vehicle safety, efficiency, and connectivity. These systems leverage IoT technology to provide real-time monitoring of vehicle conditions, including diagnostics and prognostics, which help in predictive maintenance and reducing downtime for vehicles.

Telematics enhances driver safety and regulatory compliance with features like automatic crash notifications, emergency calling, and stolen vehicle recovery. As regulatory bodies mandate these safety features, telematics becomes essential for safety-conscious consumers and enterprises, fueling the segment’s growth.

Consumer demand for seamless connectivity and mobile app integration drives the telematics market. Vehicle owners expect features like real-time traffic updates, remote operation, and route guidance. As manufacturers innovate with enhanced connectivity, the demand for automotive telematics will continue to grow, reinforcing its dominance in the Automotive IoT market.

Key Market Segments

By Component

- Hardware

- Software

- Services

By System

- Embedded

- Tethered

- Integrated

By Application

- Navigation

- Telematics

- Infotainment

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver

Growing shift to electric and hybrid vehicles aims to cut CO₂ emissions.

The automotive industry’s shift towards electric and hybrid vehicles (EVs and HEVs) is a significant driver for the integration of Internet of Things (IoT) technologies. This transition is primarily motivated by the need to reduce greenhouse gas emissions and adhere to stringent environmental regulations.

IoT facilitates this shift by enabling advanced features such as real-time monitoring of vehicle performance, predictive maintenance, and efficient energy management. These capabilities not only enhance the efficiency of EVs and HEVs but also contribute to a reduction in operational costs, thereby encouraging consumer adoption. Governments worldwide are supporting this transition through incentives and subsidies, further propelling the integration of IoT in the automotive sector.

Restraint

Lack of Infrastructure for Proper Functioning of Connected Vehicles

The effectiveness of IoT in vehicles heavily relies on the availability of robust infrastructure, including high-speed internet connectivity and advanced telematics. In many regions, especially in developing countries, such infrastructure is either lacking or inadequate, hindering the seamless operation of connected vehicles.

Applications such as real-time traffic updates, vehicle-to-vehicle communication, and over-the-air software updates require consistent and reliable connectivity. The absence of such infrastructure can lead to suboptimal performance of IoT features, thereby limiting their adoption and effectiveness. Connected vehicles generate vast amounts of data, including location and driving patterns, which are vulnerable to cyberattacks, threatening privacy and public safety.

Opportunity

Development of Advanced Driver Assistance Systems (ADAS)

The advancement of IoT technologies presents a significant opportunity in the development of Advanced Driver Assistance Systems (ADAS). These systems utilize IoT sensors and connectivity to enhance vehicle safety and driving experience by providing features such as adaptive cruise control, lane departure warnings, and automated parking.

The growing consumer demand for safety and convenience, coupled with regulatory mandates for vehicle safety standards, drives the adoption of ADAS. The integration of IoT in ADAS enables real-time data processing and communication, leading to more responsive and intelligent systems. This development not only improves road safety but also accelerates the progression towards fully autonomous vehicles.

Challenge

High Implementation Costs and Lack of Standardization

Implementing IoT technologies in vehicles involves substantial costs related to research and development, infrastructure upgrades, and the integration of sophisticated hardware and software components. These high initial investments can be a deterrent for manufacturers, especially smaller enterprises.

Additionally, the lack of standardization in IoT protocols and communication standards across the automotive industry poses a significant challenge. This fragmentation leads to compatibility issues, increased complexity in system integration, and hinders the seamless interoperability of IoT devices and platforms.

Emerging Trends

A prominent trend is the development of connected cars equipped with advanced communication capabilities, enabling real-time data exchange with external systems. This connectivity facilitates services such as navigation assistance, traffic updates, and in-car entertainment, enhancing the overall driving experience.

Another notable trend is the implementation of Vehicle-to-Everything (V2X) communication technologies, including Vehicle-to-Vehicle (V2V) and Vehicle-to-Infrastructure (V2I) interactions. These technologies allow vehicles to communicate with each other and with roadway infrastructure, providing timely information about road conditions, hazards, and traffic signals.

The integration of artificial intelligence (AI) into automotive IoT is also gaining momentum. Advanced driver-assistance systems (ADAS) utilize AI to process data from various sensors, assisting with functions like lane-keeping, adaptive cruise control, and emergency braking. For instance, Goodyear has developed smart tires capable of sensing road conditions, such as rain and ice, to improve emergency braking performance.

Business Benefits

One significant benefit is the optimization of fleet management. IoT-enabled telematics systems provide real-time tracking of vehicles, allowing businesses to monitor routes, fuel consumption, and driver behavior. This data-driven approach leads to reduced operational costs and improved logistics planning.

In manufacturing, IoT facilitates the concept of the smart factory, where interconnected machines and sensors enable predictive maintenance and automation. By collecting and analyzing data from production equipment, manufacturers can anticipate maintenance needs, reducing downtime and extending machinery lifespan.

Automotive IoT also enhances product offerings and customer satisfaction. Connected vehicles can provide personalized services, such as predictive maintenance alerts and tailored infotainment options, improving the user experience. Additionally, the ability to perform over-the-air software updates ensures that vehicles remain up-to-date with the latest features and security patches, reducing the need for physical recalls and associated costs.

Key Player Analysis

NXP Semiconductors is a global leader in providing solutions for the automotive industry, especially in the IoT space. They specialize in developing microcontrollers, sensors, and connectivity solutions, which enable vehicles to communicate with their environment. NXP’s automotive solutions are pivotal in ensuring secure, efficient, and seamless connectivity.

HARMAN International is another significant player in the automotive IoT space. The company focuses on providing in-car connected experiences and advanced infotainment systems, offering a wide range of products from audio systems to connected car platforms. HARMAN has expanded its expertise to include smart cabin technologies, cloud services, and AI to enhance the driver and passenger experience.

Robert Bosch GmbH is a renowned global technology company that plays a major role in the automotive IoT sector. Bosch is involved in various aspects of IoT, from advanced sensors and controllers to software solutions that enhance vehicle connectivity. The company’s expertise lies in developing technologies for autonomous driving, advanced driver assistance systems (ADAS), and electric vehicles.

Top Key Players in the Market

- NXP Semiconductors N.V.

- HARMAN International Industries, Inc.

- Robert Bosch GmbH

- Thales S.A.

- IBM Corporation

- Texas Instruments Incorporated

- Microsoft Corporation

- Intel Corporation

- Verizon Communications Inc.

- QUALCOMM Incorporated

- Others

Top Opportunities Awaiting for Players

The Automotive Internet of Things (IoT) market is experiencing rapid evolution, presenting numerous opportunities for industry stakeholders.

- Advanced Driver Assistance Systems (ADAS) and Autonomous Driving: The integration of IoT technologies into vehicles facilitates the development of ADAS and autonomous driving capabilities. By enabling real-time data exchange between vehicles and infrastructure, IoT enhances safety and efficiency on the roads.

- Vehicle-to-Everything (V2X) Communication: V2X communication encompasses Vehicle-to-Vehicle (V2V), Vehicle-to-Infrastructure (V2I), and Vehicle-to-Pedestrian (V2P) interactions. This connectivity allows vehicles to communicate with each other and their surroundings, enhancing traffic management and reducing accidents. The European Commission’s plan to propose legislation granting fair access to vehicle data underscores the importance of V2X in the connected car ecosystem.

- In-Vehicle Infotainment and Connectivity Services: The demand for enhanced in-car experiences is driving the integration of IoT-based infotainment systems. These systems offer real-time navigation, streaming services, and seamless smartphone integration. For instance, collaborations between automotive and technology companies are leading to the development of advanced infotainment solutions, enriching the driving experience.

- Predictive Maintenance and Vehicle Health Monitoring: IoT enables continuous monitoring of vehicle components, allowing for predictive maintenance strategies. By analyzing data from sensors, potential issues can be identified before they lead to breakdowns, reducing maintenance costs and improving vehicle reliability. The AA’s development of data-driven predictive maintenance systems exemplifies the application of IoT in this area.

- Over-the-Air (OTA) Updates and Cybersecurity: IoT facilitates OTA software updates, ensuring vehicles remain up-to-date with the latest features and security patches. This capability reduces the need for physical recalls and enhances vehicle performance. However, it also necessitates robust cybersecurity measures to protect against potential threats, highlighting the need for ongoing investment in secure IoT infrastructures.

Recent Developments

- In January 2025, ENIGMA, a cybersecurity platform, announced an agreement to acquire Dellfer Inc., a firmware security company serving the automotive and broader IoT markets, to enhance its zero-trust cybersecurity platform.

- In December 2024, NXP announced an agreement to acquire Aviva Links, a provider of Automotive SerDes Alliance (ASA) compliant in-vehicle connectivity solutions. This acquisition aims to enhance NXP’s automotive networking portfolio, facilitating the development of software-defined vehicles.

- In December 2024, Bosch agreed to sell its security and communications technology product business to private equity firm Triton. The deal includes units specializing in video, access and intrusion, and communication technologies.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 142.8 Bn |

| Forecast Revenue (2034) | USD 1,197 Bn |

| CAGR (2025-2034) | 23.70% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Component (Hardware, Software, Services), By System (Embedded, Tethered, Integrated), By Application (Navigation, Telematics, Infotainment) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | NXP Semiconductors N.V., HARMAN International Industries, Inc., Robert Bosch GmbH, Thales S.A., IBM Corporation, Texas Instruments Incorporated, Microsoft Corporation, Intel Corporation, Verizon Communications Inc., QUALCOMM Incorporated, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |