Global Animal Parasiticides Market Size, Share Analysis Report By Type (Ectoparasiticides, Endoparasiticides, Endectocides), By Product Type (Over the Counter (OTC), Prescription), By Animal Type (Companion Animals, Farm Animals), By End User (Veterinary Hospitals And Clinics, Animal Farms, Home Care Settings), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 182264

- Number of Pages: 372

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

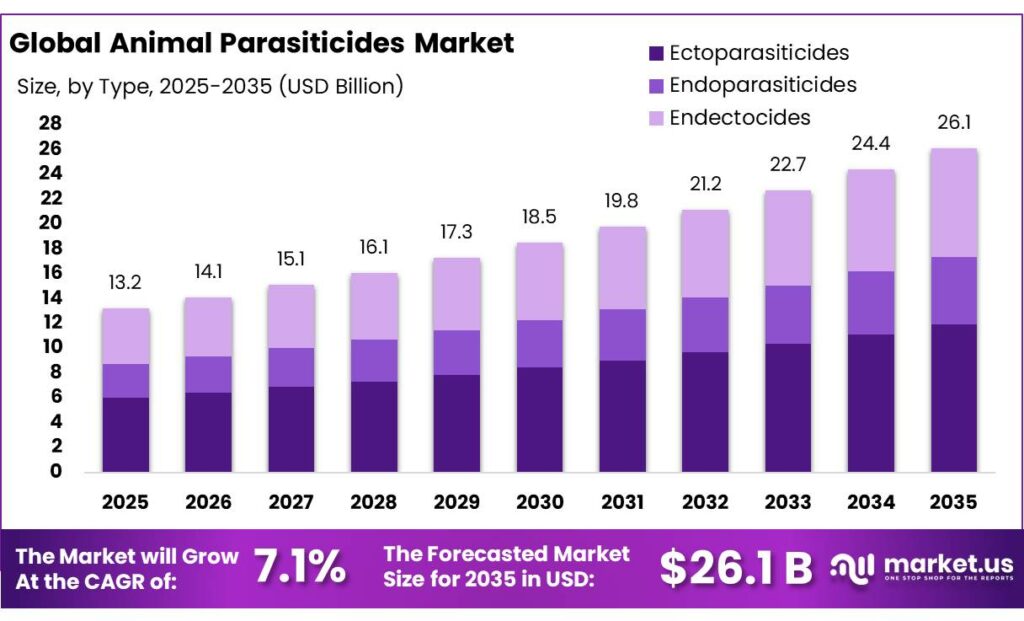

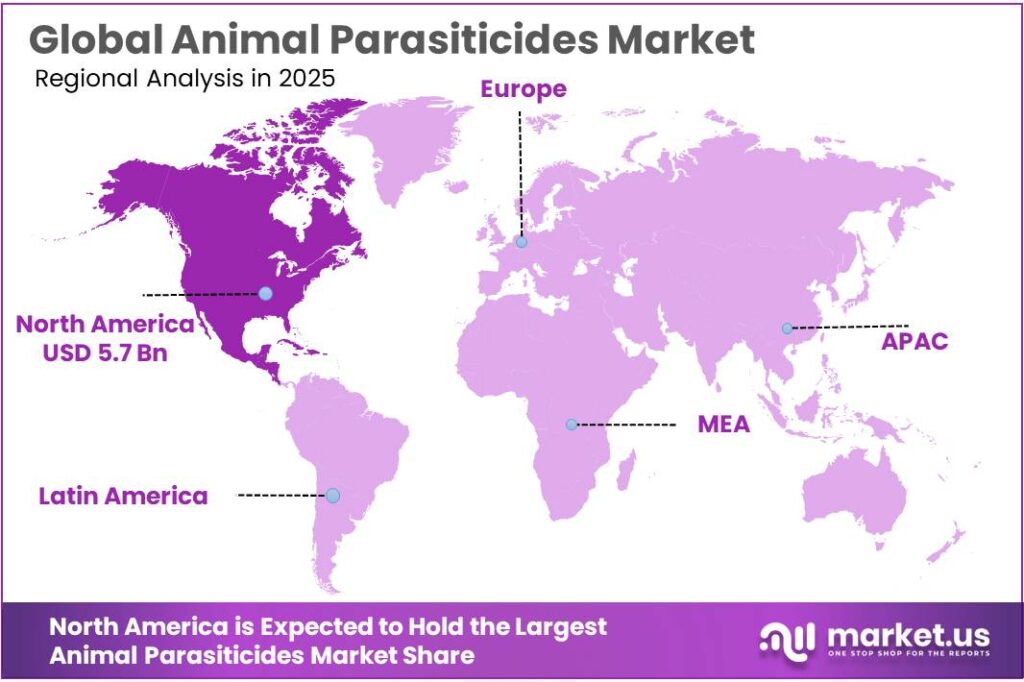

The Global Animal Parasiticides Market size is expected to be worth around USD 26.1 Billion by 2035, from USD 13.2 Billion in 2025, growing at a CAGR of 7.1% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 43.7% share, holding USD 5.7 Billion revenue.

Animal parasiticides represent a critical animal-health category used to prevent, control, and treat internal parasites such as nematodes and cestodes and external parasites such as fleas, ticks, mites, and lice across companion and food-producing animals.

The industry’s importance is tied directly to the scale of the global animal base: FAO-linked 2025 reporting shows the world had almost 1.6 billion cattle, more than 1.3 billion sheep, about 1.1 billion goats, nearly 1.0 billion pigs, and almost 27 billion chickens in 2023. The same FAO source notes that, versus 2013, global populations rose by 22% for chickens, 16% for goats, 12% for sheep, and 9% for cattle, while pigs declined by 2%, reinforcing why parasite-control demand remains structurally anchored in food security, herd productivity, and biosecurity.

From an industrial scenario standpoint, demand is being supported by both livestock economics and the premiumization of companion-animal care. FAO reported that global meat production reached 374 million tonnes in 2024, up 7 million tonnes from 2023, which indicates sustained pressure on producers to protect feed conversion, weight gain, milk yield, and reproductive performance through better parasite management.

In companion animals, FEDIAF reported in 2025 that Europe had 299 million pets, with 139 million households—or 49% of households—owning at least one pet, while annual pet food sales reached €29.2 billion and volumes reached about 9.1 million tonnes. This combination of large food-animal inventories and a highly monetized pet-care ecosystem keeps parasiticides commercially resilient across oral, injectable, topical, and collar-based formats.

The main growth drivers remain rising protein demand, productivity protection, and disease-risk management. FAO’s 2025 OECD-FAO Agricultural Outlook projects global consumption growth by 2034 of roughly 21% for poultry, 16% for sheep meat, 13% for beef, and 5% for pig meat. That outlook matters because higher output targets generally require tighter parasite control to reduce morbidity and feed-conversion losses. WOAH’s 2025 State of the World’s Animal Health also highlighted the severity of parasitic burden by noting that in Zimbabwe, 65% of cattle mortality was linked to theileriosis and other tick-borne diseases.

Government and institutional action is also strengthening the sector’s outlook. In January 2025, FAO launched the second phase of its sustainable tick-control and acaricide-resistance management project, supported by a community of practice spanning 86 countries. In May 2025, Ireland confirmed that antiparasitics for food-producing animals would move toward prescription-only use from 1 September 2025 because of resistance concerns.

In the United States, USDA announced in August 2025 plans to build a sterile-fly production facility to protect the national cattle herd from New World screwworm, while FDA has continued to maintain active oversight of recent animal-drug approvals. Together, these steps favor higher-value, veterinarian-led, compliance-driven parasiticide use.

Key Takeaways

- Animal Parasiticides Market size is expected to be worth around USD 26.1 Billion by 2035, from USD 13.2 Billion in 2025, growing at a CAGR of 7.1%.

- Ectoparasiticides held a dominant market position, capturing more than a 45.8% share.

- Over the Counter (OTC) held a dominant market position, capturing more than a 62.4% share.

- Companion Animals held a dominant market position, capturing more than a 67.3% share.

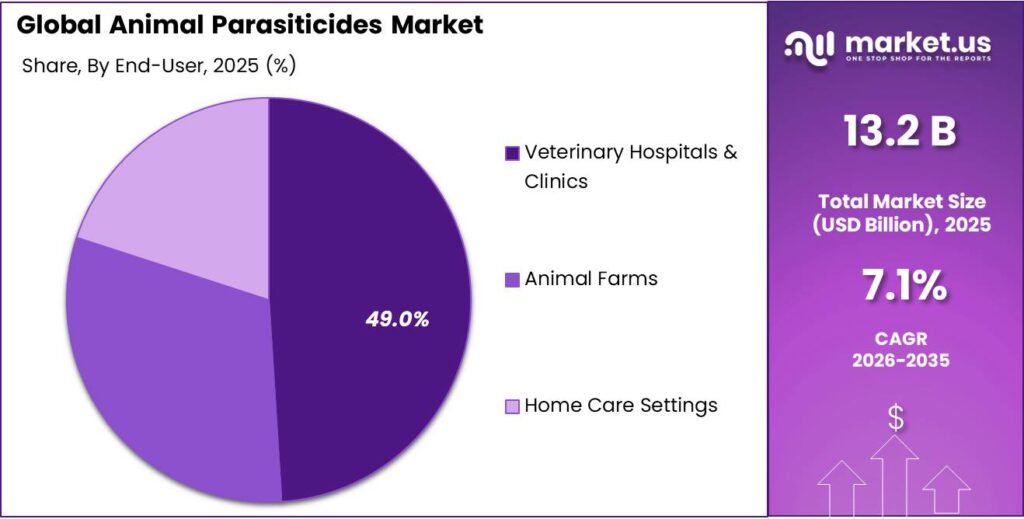

- Veterinary Hospitals & Clinics held a dominant market position, capturing more than a 49.6% share.

- North America represents the dominating regional market for animal parasiticides, accounting for approximately 43.7% share with an estimated value of USD 5.7 billion.

By Type Analysis

Ectoparasiticides dominate with 45.8% driven by rising external parasite control needs

In 2025, Ectoparasiticides held a dominant market position, capturing more than a 45.8% share. This strong position was mainly due to the increasing need to control external parasites such as fleas, ticks, mites, and lice in both companion and livestock animals. Pet owners are becoming more aware of preventive care, especially in urban areas, which has led to higher use of spot-on treatments, sprays, and medicated collars. At the same time, livestock farmers are focusing more on animal health to avoid production losses caused by parasite infestations.

By Product Type Analysis

Over the Counter (OTC) leads with 62.4% as easy access drives everyday use

In 2025, Over the Counter (OTC) held a dominant market position, capturing more than a 62.4% share. This growth was largely supported by the convenience these products offer, as pet owners and farmers can purchase them without a prescription. Many common parasitic treatments, especially for fleas, ticks, and worms, are widely available in local stores, veterinary outlets, and online platforms, making them a go-to choice for routine care. Consumers prefer OTC options for quick and affordable solutions, particularly for regular prevention rather than severe infections.

By Animal Type Analysis

Companion Animals lead with 67.3% as pet care spending continues to rise

In 2025, Companion Animals held a dominant market position, capturing more than a 67.3% share. This was mainly driven by the growing number of pet owners and the strong focus on keeping pets healthy and parasite-free. Dogs and cats, in particular, require regular treatments for fleas, ticks, and internal parasites, which keeps demand steady throughout the year. Many pet owners now treat their animals as part of the family, which has increased spending on preventive healthcare products.

By End User Analysis

Veterinary Hospitals & Clinics lead with 49.6% as trusted care drives treatment choices

In 2025, Veterinary Hospitals & Clinics held a dominant market position, capturing more than a 49.6% share. This was mainly because animal owners rely heavily on professional guidance when it comes to parasite treatment and prevention. Many parasiticides, especially for severe infestations, are recommended and administered through veterinarians, which naturally increases demand in clinical settings. These facilities also ensure correct diagnosis, dosage, and follow-up care, making them a preferred choice for both pet owners and livestock handlers.

Key Market Segments

By Type

- Ectoparasiticides

- Pour-ons and spot-ons

- Oral tablets

- Sprays

- Dips

- Ear tags

- Collars

- Others

- Endoparasiticides

- Oral liquids

- Oral solids

- Injectables

- Feed additives

- Others

- Endectocides

By Product Type

- Over the Counter (OTC)

- Prescription

By Animal Type

- Companion Animals

- Dogs

- Cats

- Horses

- Others

- Farm Animals

- Swine

- Cattle

- Poultry

- Sheep and goats

- Others

By End User

- Veterinary Hospitals & Clinics

- Animal Farms

- Home Care Settings

Emerging Trends

Shift toward long-acting and combination parasiticides is shaping the market

One clear trend in the animal parasiticides market is the growing shift toward long-acting and combination treatments. Instead of using multiple products for different parasites, farmers and pet owners now prefer single solutions that can handle both internal and external parasites at once. Recent industry data shows that over 65% of new parasiticide products are now combination therapies, designed to target multiple parasites together. At the same time, around 52% of new formulations are long-acting, meaning they provide protection for extended periods and reduce the need for frequent dosing.

This change is happening because managing parasites has become more complex. Parasites are evolving, and farmers need solutions that are both effective and easy to use. Long-acting treatments help reduce stress on animals and lower labor costs, especially in large farms where handling animals frequently is difficult.

Global push for sustainable parasite control is encouraging innovation

Another important part of this trend is the move toward more sustainable parasite control. Organizations like the Food and Agriculture Organization are encouraging farmers to reduce over-reliance on chemicals and adopt balanced approaches. FAO highlights the need to move beyond only drug-based treatments and focus on integrated parasite management, combining hygiene, monitoring, and controlled use of medicines.

This shift is pushing companies to develop safer and more efficient products. There is also a growing focus on reducing environmental impact and slowing down resistance. Governments and veterinary bodies are supporting these efforts through awareness programs and better guidelines for drug usage.

Drivers

Rising livestock losses due to parasites are pushing demand for effective treatments

Parasitic infections are one of the biggest reasons why farmers and animal owners are actively using parasiticides today. These infections quietly reduce animal health, which directly affects milk, meat, and overall productivity. According to the Food and Agriculture Organization, around 80% of the world’s cattle population is exposed to tick infestation, showing how common parasite problems are across farms globally.

There is also a larger global impact. Animal diseases, including parasitic infections, are responsible for over 20% of global animal production losses, which is a major concern for food supply chains. This means a large portion of potential food production is lost every year, making parasite control not just a farm issue but a food security issue as well.

Government and global efforts to control parasites support market growth

Governments and global organizations are taking this problem seriously. Many countries are strengthening veterinary services, promoting regular deworming programs, and supporting farmers with awareness campaigns. Organizations like the Food and Agriculture Organization continue to push for better parasite management practices and affordable treatment access, especially in rural areas.

These initiatives are helping farmers understand that prevention is cheaper than loss. When animals are treated regularly, they grow better, produce more, and stay healthier. This shift in mindset is steadily increasing the use of animal parasiticides. As livestock demand continues to rise globally, controlling parasites has become a basic need rather than an option, which is strongly driving the growth of this market.

Restraints

Growing resistance to parasiticides is reducing treatment effectiveness

One of the biggest challenges in the animal parasiticides market today is the rising resistance of parasites to commonly used drugs. Over time, frequent and sometimes improper use of the same treatments has made many parasites less responsive, which means the products don’t work as well as they used to. According to the Food and Agriculture Organization, resistance to antiparasitic drugs has been reported in multiple livestock systems worldwide, especially in sheep and cattle farming.

This creates a serious issue for farmers. When treatments stop working, animals remain infected for longer periods, which affects their health and productivity. It also forces farmers to either use higher doses or switch to more expensive alternatives, increasing overall costs. In many developing areas, farmers may not have access to newer treatments, which makes the problem worse.

Global efforts highlight need for controlled and responsible usage

Governments and international bodies are now encouraging better parasite management practices to slow down resistance. The Food and Agriculture Organization and other global groups are promoting responsible drug use, regular monitoring, and rotation of treatment types. These steps are important to keep existing medicines effective for a longer time.

There is also a push toward integrated parasite management, where farmers combine hygiene, nutrition, and controlled treatment instead of relying only on medicines. While these efforts are helping, changing long-standing farming habits takes time. Resistance is not something that can be fixed quickly, and it continues to hold back the full potential of the parasiticides market.

Opportunity

Rising global demand for animal protein is creating strong growth opportunities

One of the biggest opportunities in the animal parasiticides market comes from the steady rise in demand for meat, milk, and other animal-based products. As population grows and incomes improve, especially in developing countries, more people are including animal protein in their diets. According to the Food and Agriculture Organization, global demand for food is expected to grow by around 60% by 2050, with meat production projected to rise by nearly 70% during the same period.

This increase directly pushes farmers to produce more, which means keeping animals healthy becomes even more important. Parasites can slow down growth and reduce output, so farmers are now more careful about prevention rather than waiting for problems to appear. In 2025, global meat production already showed steady growth, supported by strong demand and expanding poultry output, highlighting how quickly the livestock sector is evolving.

Government support and sustainable farming practices are strengthening adoption

Governments and global organizations are also supporting this growth by promoting better livestock health management. The Food and Agriculture Organization highlights that livestock production is expanding rapidly due to population growth and changing food habits, especially in developing regions.

To support this expansion, many countries are investing in veterinary services, awareness programs, and disease control initiatives. These efforts encourage farmers to adopt preventive healthcare practices, including regular use of parasiticides. There is also a growing push toward sustainable farming, where healthy animals are seen as key to efficient and responsible production.

Regional Insights

North America Animal Parasiticides Market (Dominating Region – 43.7%, USD 5.7 Billion)

North America represents the dominating regional market for animal parasiticides, accounting for approximately 43.7% share with an estimated value of USD 5.7 billion, driven by a highly advanced veterinary healthcare ecosystem, strong livestock base, and premium companion animal expenditure. The region consistently maintains leadership due to early adoption of preventive healthcare practices and structured regulatory frameworks led by agencies such as the U.S. FDA and USDA, ensuring product safety and efficacy.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Boehringer Ingelheim International holds a strong position in the animal parasiticides market, supported by its wide veterinary portfolio and global reach. The company operates in over 130 countries and invests around 20% of its animal health revenue into research and development. Its parasiticide products are widely used in both companion and livestock segments. With thousands of employees in animal health alone and continuous product launches, the company maintains steady growth and strong distribution networks across key regions.

Ceva Sante Animal is a global veterinary company present in more than 110 countries, offering a broad range of parasiticides and animal health products. The company employs over 7,000 people worldwide and focuses heavily on innovation, investing a significant share of its revenue into R&D. Its parasiticide portfolio supports both companion animals and livestock. Ceva continues to expand through strategic collaborations and product development, strengthening its position in emerging and developed markets alike.

Bimeda is a growing player in the animal health sector, with operations spanning more than 75 countries worldwide. The company focuses on affordable and accessible parasiticides, especially for livestock farmers. It offers a portfolio of over 300 veterinary products, including dewormers and ectoparasitic treatments. Bimeda continues to expand through acquisitions and partnerships, strengthening its manufacturing presence across multiple regions. Its focus on cost-effective solutions helps it gain traction in developing markets where price sensitivity is high.

Top Key Players Outlook

- Boehringer Ingelheim International

- Bimeda

- Biogenesis Bago

- Ceva Sante Animal

- Dechra Pharmaceuticals

- Elanco Animal Health

- Norbrook Laboratories

- Neogen Corporation

- Ourofino Saúde Animal

- Phibro Animal Health

Recent Industry Developments

In 2025, Boehringer Ingelheim International total revenue reached around EUR 27.8 billion, showing a growth of nearly 7.3%, with parasiticides being one of the key contributors in its animal health portfolio.

In 2025, Ceva Santé Animale remained a solid participant in the animal parasiticides sector, supported by its broad global animal health network and its continued focus on farm and companion animal care. The company reported about €1.77 billion in revenue, employed around 7,000 people, and operated directly in 47 countries, giving it a strong base to supply veterinary products across major markets.

Report Scope

Report Features Description Market Value (2025) USD 13.2 Bn Forecast Revenue (2035) USD 26.1 Bn CAGR (2026-2035) 7.1% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Ectoparasiticides, Endoparasiticides, Endectocides), By Product Type (Over the Counter (OTC), Prescription), By Animal Type (Companion Animals, Farm Animals), By End User (Veterinary Hospitals And Clinics, Animal Farms, Home Care Settings) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape Boehringer Ingelheim International, Bimeda, Biogenesis Bago, Ceva Sante Animal, Dechra Pharmaceuticals, Elanco Animal Health, Norbrook Laboratories, Neogen Corporation, Ourofino Saúde Animal, Phibro Animal Health Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Animal Parasiticides MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample

Animal Parasiticides MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Boehringer Ingelheim International

- Bimeda

- Biogenesis Bago

- Ceva Sante Animal

- Dechra Pharmaceuticals

- Elanco Animal Health

- Norbrook Laboratories

- Neogen Corporation

- Ourofino Saúde Animal

- Phibro Animal Health

Our Clients

- 182264

- Mar 2026