Global Agriculture Drones Market Size, Share, And Enhanced Productivity By Type (Fixed Wing, Rotary Wing, Hybrid Drones), By Component (Hardware (Frames, Flight Control Systems, Navigation Systems, Propulsion Systems, Cameras, Sensors, Others), Software, Services (Professional Services, Managed Services)), By Farming Environment (Indoor Farming, Outdoor Farming), By Farm Size (Large-scale Commercial Farms, Small and Medium Farms), By Application (Crop Management, Field Mapping, Crop Spraying, Livestock Monitoring, Variable Rate Application (VRA), Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2025-2034

- Published date: February 2026

- Report ID: 178718

- Number of Pages: 366

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

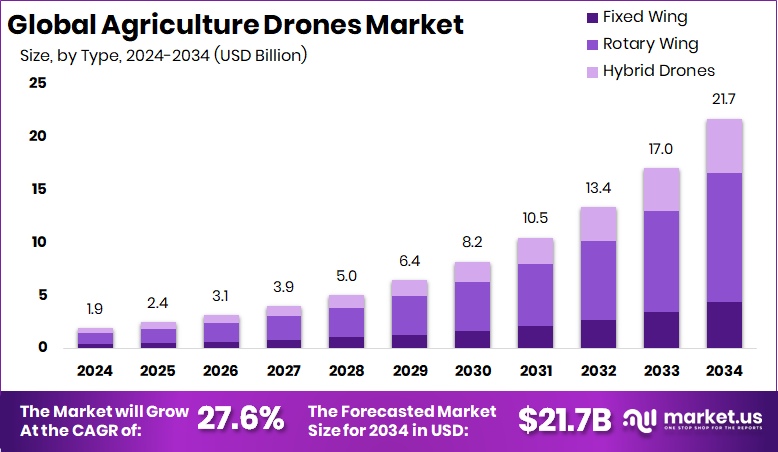

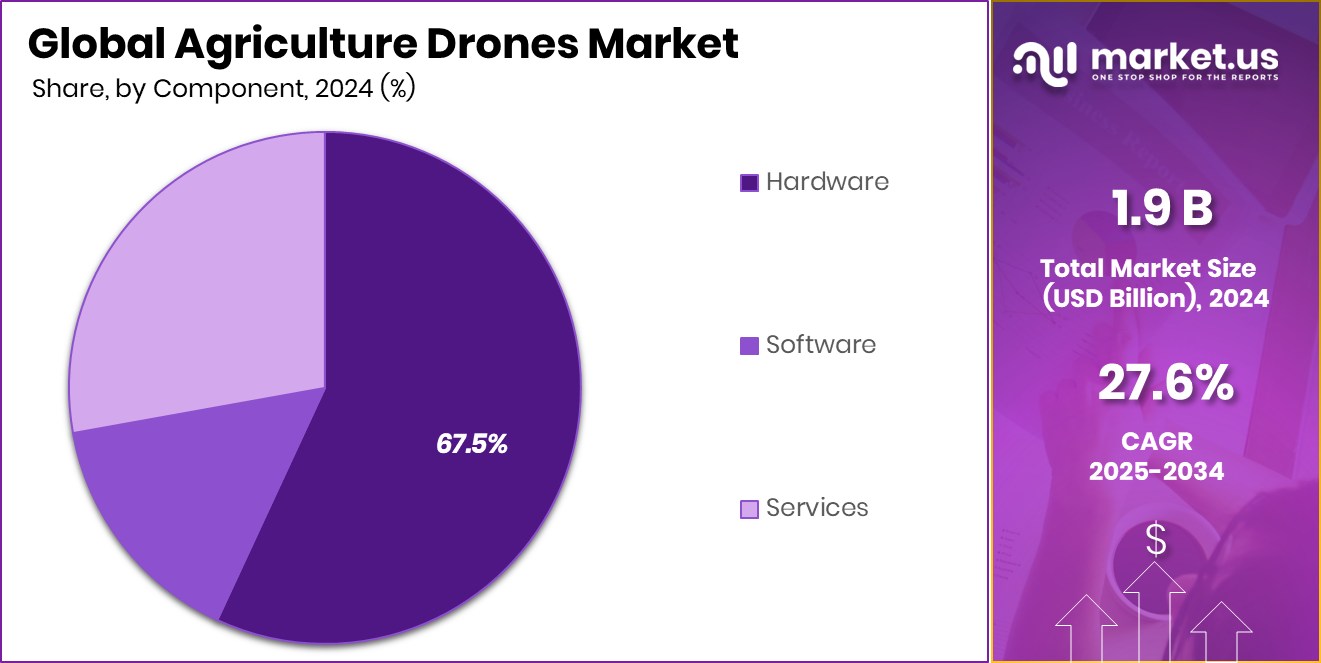

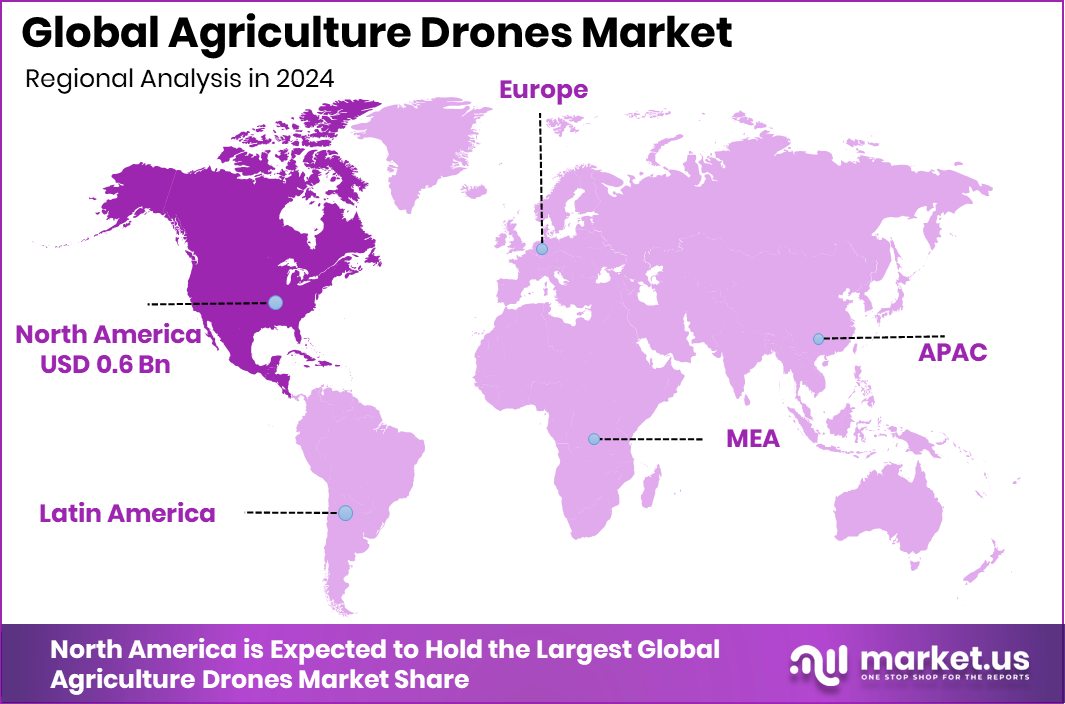

The Global Agriculture Drones Market is expected to be worth around USD 21.7 billion by 2034, up from USD 1.9 billion in 2024, and is projected to grow at a CAGR of 27.6% from 2025 to 2034. The agriculture drone market in North America was valued at USD 0.6 Bn, capturing 34.7%.

Agriculture drones are unmanned aerial systems designed to support farming tasks such as spraying, mapping, monitoring crop conditions, and capturing real-time field data. They help farmers understand plant health, soil variability, and input needs with greater accuracy than ground-based tools. The Agriculture Drones Market refers to the commercial adoption of these drone technologies across fixed-wing, rotary-wing, and hybrid platforms, supported by hardware, software, and services. It covers their use in indoor and outdoor environments, across large commercial farms as well as small and medium operations, enabling applications such as crop management, spraying, field mapping, VRA, and livestock monitoring.

Growth in this market is supported by rising interest in precision agriculture as farmers seek faster ways to analyze fields and improve input efficiency. The demand is reinforced by programs such as FETF 2025, offering grants to over 8,800 applicants, helping more growers adopt advanced technologies. New funding commitments like the Western Grains Research Foundation’s $2.71M investment further encourage the development of next-generation crop research tools that align well with drone-based monitoring.

Opportunity also expands as digital platforms scale. Investments such as Fieldin’s $30M Series B and Orchard Robotics securing $22M highlight strong momentum in precision crop systems that often integrate aerial insights. Additionally, robotics-focused funding like Ecorobotix raising $52M shows growing confidence in automated crop protection, creating wider space for drones to support accurate spraying and field targeting.

Key Takeaways

- The Global Agriculture Drones Market is expected to be worth around USD 21.7 billion by 2034, up from USD 1.9 billion in 2024, and is projected to grow at a CAGR of 27.6% from 2025 to 2034.

- Agriculture Drones Market is dominated by rotary wing systems, holding a strong 56.2% share globally.

- In the Agriculture Drones Market, hardware dominated the component segment with an impressive 67.5% share.

- Agriculture Drones Market growth is dominated by outdoor farming applications, capturing a leading 83.1% share.

- Large-scale commercial farms dominated the Agriculture Drones Market landscape, accounting for a significant 69.4% operational share.

- Agriculture Drones Market application trends show crop spraying dominated usage patterns, securing a notable 32.8% share.

- In North America, the Agriculture Drones Market achieved USD 0.6 Bn with a 34.7% share.

By Type Analysis

Agriculture Drones Market share was dominated by the rotary wing segment at 56.2%.

In 2024, the agriculture drones market was strongly shaped by rotary-wing platforms, which dominated the segment with a 56.2% share due to their maneuverability and suitability for uneven farmlands. Farmers favored these drones because they can hover precisely over target areas, making them ideal for localized spraying, plant health monitoring, and tight-space operations. Their flexible take-off and landing needs made them popular in regions lacking open fields.

The rising adoption of multi-rotor systems for precision farming activities further reinforced market leadership. As growers increasingly demand quick-response drone solutions for small and mid-sized fields, rotary-wing models continued to lead the market, supported by ease of use, maintenance efficiency, and compatibility with advanced imaging sensors.

By Component Analysis

Agriculture Drones Market share remained dominated as hardware components captured a strong 67.5%.

In 2024, hardware dominated the agriculture drones market with a 67.5% share, driven by rapid upgrades in airframes, sensors, batteries, and propulsion systems. Farmers increasingly invested in higher-end drone bodies that deliver longer flight endurance, higher payload capacity, and better stability during spraying and mapping operations. Imaging components such as multispectral and hyperspectral cameras supported stronger adoption, helping detect stress, nutrient variations, and moisture differences across fields.

Battery innovation and modular designs also contributed to hardware leadership. As commercial farms and service providers focused on reliable field performance, hardware expenditures outweighed software and service components. This dominance continued as producers emphasized durability, ruggedness, and advanced payload systems that directly enhance operational output.

By Farming Environment Analysis

Agriculture Drones Market share was strongly dominated by outdoor farming at 83.1%.

In 2024, outdoor farming dominated the agriculture drones market with an 83.1% share, reflecting widespread drone usage across open farmlands for spraying, mapping, seeding, and surveillance. Large crop zones required scalable aerial monitoring, pushing farmers to deploy drones for rapid coverage and time-saving decision-making. Weather-resistant drones with stable flight controls enabled efficient use across varied climates.

The strong presence of cereal, oilseed, and plantation farms further supported the dominance of outdoor applications. As growers sought real-time field health insights over a wide geography, drones became indispensable for detecting early stress indicators. Outdoor farming remained the largest environment, reinforced by increasing mechanization and adoption of precision agricultural practices across emerging and developed markets.

By Farm Size Analysis

Agriculture Drones Market share stayed dominated as large-scale farms reached 69.4%.

In 2024, large-scale commercial farms dominated the agriculture drones market with a 69.4% share, driven by their need for high-coverage, time-efficient, and cost-effective field operations. These farms adopted drones for wide-area mapping, advanced analytics, resource planning, and optimized spraying cycles. The ability to reduce chemical waste and labor effort strengthened drone usage, especially across cereal, cotton, sugarcane, and horticulture plantations.

Commercial growers prioritized drones capable of carrying heavier payloads, longer flight durations, and advanced imaging systems. Their budgets for digital farming tools exceeded those of smaller farms, supporting stronger integration of autonomous drones. This dominance continued as large operators scaled precision agriculture to boost productivity and overcome labor shortages.

By Application Analysis

Agriculture Drones Market share was dominated by crop spraying applications, holding 32.8%.

In 2024, crop spraying dominated the agriculture drones market with a 32.8% share, becoming one of the most widely adopted applications due to its ability to reduce labor, chemical usage, and operational time. Drones enabled uniform distribution of pesticides, nutrients, and foliar treatments across fields, even in areas inaccessible to traditional machinery.

Farmers preferred aerial spraying to improve precision, lower operator exposure to chemicals, and increase application accuracy on tall or dense crops. The rise of autonomous flight paths and smart tank-mix systems strengthened usage in spraying-intensive regions. As demand grew for faster and more targeted farm operations, crop spraying remained the leading application, supported by strong regulatory acceptance and farmer training programs.

Key Market Segments

By Type

- Fixed Wing

- Rotary Wing

- Hybrid Drones

By Component

- Hardware

- Frames

- Flight Control Systems

- Navigation Systems

Propulsion Systems - Cameras

- Sensors

- Others

- Software

- Services

- Professional Services

- Managed Services

By Farming Environment

- Indoor Farming

- Outdoor Farming

By Farm Size

- Large-scale Commercial Farms

- Small and Medium Farms

By Application

- Crop Management

- Field Mapping

- Crop Spraying

- Livestock Monitoring

- Variable Rate Application (VRA)

- Others

Driving Factors

Rising demand for precise crop monitoring

Rising demand for precise crop monitoring continues to push the Agriculture Drones Market forward as farmers look for better visibility across large fields and faster decision-making tools. This momentum is strengthened by new funding activity that supports drone-based research and adoption.

Agriculture drone startup Suind raising Rs 5 Cr in a seed round highlights growing confidence in field-level drone solutions, while Missouri State receiving a $300K grant for a drone-assisted pastureland study reinforces the push toward scientific validation of aerial monitoring. Together, these developments show a market moving toward wider use of drones for health assessment, real-time mapping, and routine farm operations, especially where detailed crop insights are essential.

Restraining Factors

High initial cost limits adoption

High initial cost remains a major barrier for many growers, particularly smaller operations that struggle with the upfront expenses of professional drones, sensors, and supporting software. This challenge persists even as the sector attracts large investments.

ABZ Innovation securing $8.2 million to scale heavy-duty agricultural drones demonstrates the rising cost of building advanced equipment, while XAG raising $182 million from major investors like Baidu and SoftBank reflects the capital-intensive nature of drone development. Although these investments drive innovation, they also underline why affordability concerns continue to slow wider market penetration.

Growth Opportunity

Expanding use in large commercial farms

Expanding use in large commercial farms presents strong growth opportunities as these operations benefit most from time savings, wider coverage, and improved input management. Larger farms often adopt drones earlier due to higher capacity requirements and the need for scalable monitoring tools. This potential is supported by investment trends, such as XAG closing a $183 million funding round, demonstrating growing confidence in agricultural automation. Additionally, projections tied to climate-focused innovation—like ‘nature tech’ expected to grow by $6 billion after COP27—create room for drones to play a central role in sustainable crop systems, resource optimization, and environmental monitoring across global farmlands.

Latest Trends

Rising integration of AI-powered analytics

Rising integration of AI-powered analytics remains a defining trend as drones evolve from simple imaging tools to fully intelligent field assistants capable of identifying crop stress, mapping variability, and guiding field interventions. This shift is echoed by financial activity, including XAG’s $183 million funding round, which reinforces the push toward smarter autonomous systems.

At the same time, logistics-driven innovation influences agriculture, as shown by Zipline expanding its drone delivery operations with $600 million in new funding. While focused on delivery, such advancements accelerate drone navigation, autonomy, and fleet management technologies that eventually enhance agricultural drone capabilities.

Regional Analysis

North America held 34.7% share in the Agriculture Drones Market, reaching USD 0.6 Bn.

In 2024, the Agriculture Drones Market showed varied growth across major global regions, with North America dominating at 34.7% and USD 0.6 Bn, driven by large-scale adoption of precision farming practices and strong commercial farm penetration.

Europe followed with steady uptake supported by expanding digital agriculture programs and rising demand for automated spraying and mapping solutions across high-value crop areas. The Asia Pacific region experienced rapid expansion as countries increased drone usage to address labor shortages, larger cultivation zones, and efficiency needs across rice, wheat, and horticulture farms.

The Middle East & Africa displayed growing interest in agricultural drones for water-scarce farming environments, where aerial monitoring helped optimize irrigation and input use. Latin America continued to adopt drones across soybean, sugarcane, and corn farms as growers sought better field visibility and reduced chemical costs.

Across all regions, demand increased for drones capable of improving accuracy, reducing operational time, and supporting wider field assessments. North America remained the leading regional contributor due to strong commercial infrastructure, advanced farm mechanization levels, and faster integration of high-payload drone platforms that enhanced operational productivity across large agricultural landscapes.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

DJI continued to play a leading role with its agriculture-focused drone range that emphasized long flight endurance, high-capacity spraying systems, and reliable imaging tools aligned with growers’ demand for precision and speed. Its focus on expanding operational efficiency for large fields helped the company maintain strong adoption among professional users.

Parrot Drone SAS demonstrated progress by enhancing data-centric features and sensor-driven insights that supported mapping, crop health monitoring, and field-level analytics. Its commitment to compact, easy-to-deploy platforms strengthened its relevance among small and mid-sized farms seeking accessible digital tools.

AgEagle Aerial Systems Inc. continued building traction with its emphasis on agricultural imaging, autonomous flight capabilities, and solutions designed to deliver actionable field intelligence. Its technology remained well-aligned with precision agriculture tasks such as plant counting, stress detection, and targeted monitoring.

Collectively, these companies advanced the market by addressing farmers’ needs for accuracy, time savings, and simplified field operations. Their product specialization and consistent focus on agricultural applications ensured strong competitiveness and growing user trust across global farming environments.

Top Key Players in the Market

- DJI

- Parrot Drone SAS

- AgEagle Aerial Systems Inc.

- AeroVironment, Inc.

- Trimble Inc.

- DroneDeploy

- Autel Robotics

- Draganfly Inc.

- Pix4D SA

- Sky-Drones Technologies Ltd

Recent Developments

- In June 2025, Parrot introduced the ANAFI UKR micro-UAV at the Paris Air Show. This is a new professional small drone designed with stronger navigation and better sensors for demanding operations. Although primarily aimed at defense and public safety, it shows Parrot’s advanced drone engineering progress.

- In April 2024, DJI unveiled the Agras T25 and T50 agricultural drones, designed for improved spraying, larger payloads, and safer operations, helping farmers cover fields faster and more efficiently with better spray systems and higher capacity.

Report Scope

Report Features Description Market Value (2024) USD 1.9 Billion Forecast Revenue (2034) USD 21.7 Billion CAGR (2025-2034) 27.6% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Fixed Wing, Rotary Wing, Hybrid Drones), By Component (Hardware (Frames, Flight Control Systems, Navigation Systems, Propulsion Systems, Cameras, Sensors, Others), Software, Services (Professional Services, Managed Services)), By Farming Environment (Indoor Farming, Outdoor Farming), By Farm Size (Large-scale Commercial Farms, Small and Medium Farms), By Application (Crop Management, Field Mapping, Crop Spraying, Livestock Monitoring, Variable Rate Application (VRA), Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape DJI, Parrot Drone SAS, AgEagle Aerial Systems Inc., AeroVironment, Inc., Trimble Inc., DroneDeploy, Autel Robotics, Draganfly Inc., Pix4D SA, Sky-Drones Technologies Ltd Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Agriculture Drones MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample

Agriculture Drones MarketPublished date: February 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- DJI

- Parrot Drone SAS

- AgEagle Aerial Systems Inc.

- AeroVironment, Inc.

- Trimble Inc.

- DroneDeploy

- Autel Robotics

- Draganfly Inc.

- Pix4D SA

- Sky-Drones Technologies Ltd

Our Clients

- 178718

- February 2026