Quick Navigation

Report Overview

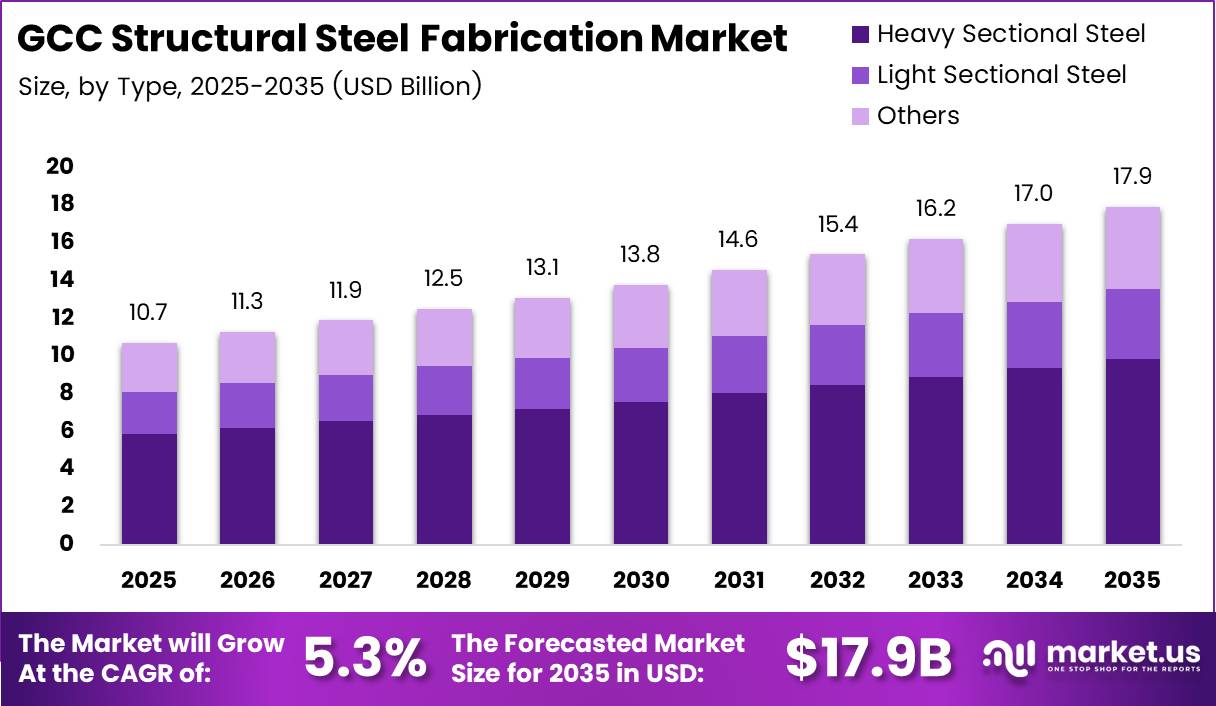

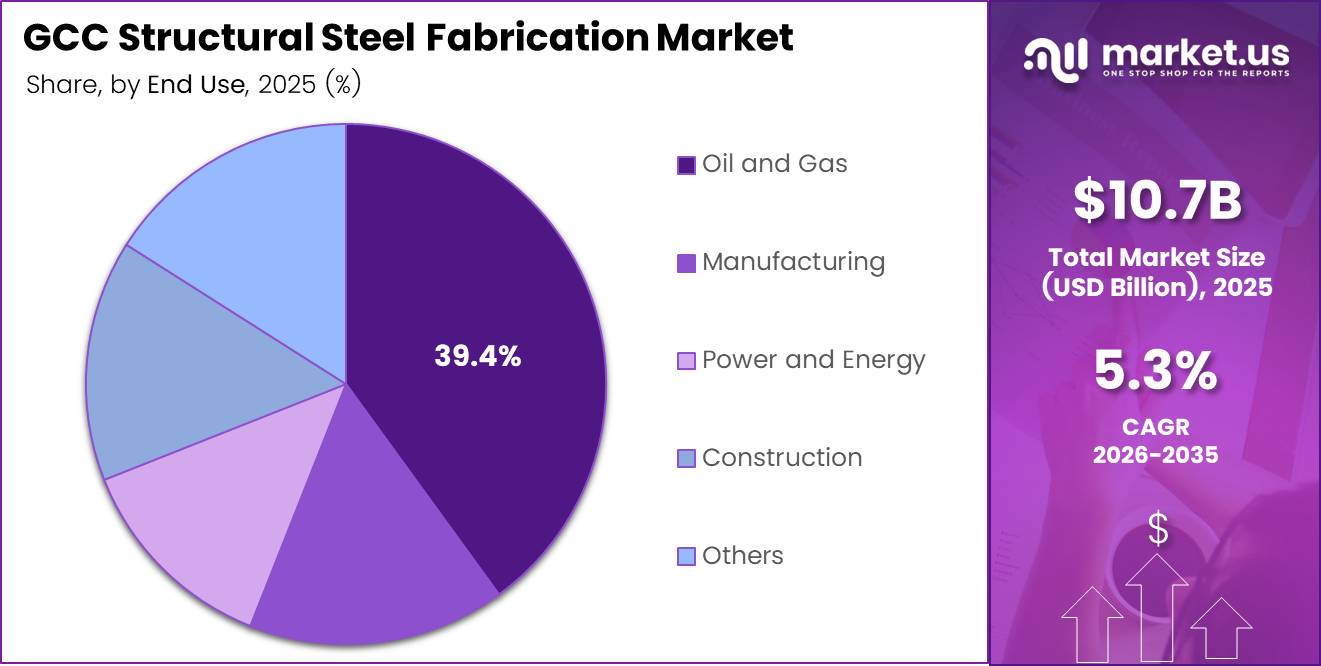

GCC Structural Steel Fabrication Market size is expected to be worth around USD 17.9 Billion by 2035 from USD 10.7 Billion in 2025, growing at a CAGR of 5.3% during the forecast period 2026 to 2035.

The GCC structural steel fabrication market covers the manufacture of steel components, frames, and assemblies used in buildings, industrial facilities, and infrastructure projects across Gulf Cooperation Council countries. Fabricators convert raw steel sections into engineered structural elements through welding, cutting, forming, and rolling processes. End products support oil and gas installations, warehouses, power plants, and commercial developments.

The market operates across a multi-tier supply chain. Primary steel producers supply raw sections to fabricators, who process them into project-specific assemblies for contractors and developers. Heavy sectional steel dominates the volume mix, while specialized fabrication processes such as metal welding and metal forming serve the most technically demanding applications in energy and industrial construction.

GCC governments have embedded structural steel fabrication within their national economic diversification programs. Saudi Arabia’s Vision 2030, the UAE’s industrial strategy, and Qatar’s infrastructure expansion all direct public investment toward sectors that rely heavily on fabricated steel. This policy alignment creates a predictable demand pipeline that reduces project-level risk for fabricators operating at scale in the region.

Oil and gas projects account for the single largest share of end-use demand, reflecting the structural importance of the energy sector in GCC economies. This concentration gives fabricators with established energy-sector credentials a durable revenue base. However, it also creates sensitivity to capital expenditure cycles in the upstream and downstream energy industries, which remain tied to global commodity prices.

According to a BIM implementation study focused on steel structures, using an integrated BIM workflow in 2025 reduced design-phase clashes by 35% and cut rework from coordination errors by 15%. For fabricators, this translates into measurable cost recovery on complex projects and a clear competitive case for digital investment. Firms that delay BIM adoption risk cost overruns that erode margins on fixed-price contracts.

Data from a 2026 UAE fabrication article shows that automated welding cells lowered labour requirements on high-volume weld lines by approximately 25 to 30% while increasing overall line throughput by around 20%. This productivity shift changes the economics of large-volume orders. Fabricators who automate retain margin on commodity steel work; those who do not face direct cost pressure from competitors who have already upgraded their production lines.

Key Takeaways

- The GCC Structural Steel Fabrication Market was valued at USD 10.7 Billion in 2025.

- The market is forecast to reach USD 17.9 Billion by 2035, growing at a CAGR of 5.3%.

- By Type, Heavy Sectional Steel dominates with a 54.8% share.

- By Fabrication Process, Metal Welding leads with a 28.5% share.

- By End-use, Oil and Gas holds the largest share at 39.4%.

- The GCC region is the primary demand base, driven by government-led infrastructure and energy investment programs.

- Saudi Arabia leads within the GCC, supported by Vision 2030 industrial expansion and new fabrication facility investments.

Type Analysis

Heavy Sectional Steel dominates with 54.8% due to load-bearing requirements in energy and infrastructure.

In 2025, Heavy Sectional Steel held a dominant market position in the By Type segment of the GCC Structural Steel Fabrication Market, with a 54.8% share. This segment supplies the primary structural frames and load-bearing components used across oil and gas facilities, industrial plants, and large-scale commercial developments. Buyers in the energy sector require heavy sections that meet stringent load and seismic design standards, which limits the ability of lighter alternatives to displace volume in these applications.

Light Sectional Steel serves secondary framing, mezzanines, and modular building applications where weight reduction and faster assembly are design priorities. This segment benefits from the rise of pre-engineered building systems and modular construction methods across GCC commercial and logistics markets. A 2025 Saudi Arabia BIM adoption analysis reported that more than 60% of surveyed large AEC organisations in the Kingdom had adopted BIM at Level 2 or higher for structural and architectural projects, including steel structures. This digital shift accelerates design coordination for light-section modular projects and reduces fabrication errors, giving producers who support BIM-compatible detailing a clear procurement advantage over those who do not.

Others in the Type segment includes specialty profiles, hollow sections, and custom-fabricated components for niche structural and architectural applications. Demand in this category responds to project-specific specifications rather than standard construction cycles. In June 2025, Mahmood Saeed Steel Industries secured a contract from Hyundai Engineering & Construction for the Hyundai Motor Manufacturing Middle East project in Saudi Arabia, covering fabrication and installation of structural steel components. This contract illustrates how specialty fabrication assignments are tied directly to major industrial investment decisions, making this sub-segment more sensitive to foreign direct investment flows than to broad construction cycles.

Fabrication Process Analysis

Metal Welding dominates with 28.5% due to structural integrity demands in energy sector assemblies.

In 2025, Metal Welding held a dominant market position in the By Fabrication Process segment of the GCC Structural Steel Fabrication Market, with a 28.5% share. Welding remains the primary joining method for primary structural frames and pressure-bearing components across oil and gas, power, and industrial construction. The technical requirements of energy-sector work, including weld certification standards and third-party inspection protocols, raise entry barriers and favour established fabricators with certified welding capabilities.

Metal Forming covers rolling, bending, and pressing operations that shape steel sections into curved or angular profiles for structural applications. This process serves architectural steel, bridge components, and industrial framing where standard flat sections cannot meet geometric requirements. Demand for formed steel grows alongside the construction of complex industrial and commercial structures that require non-standard profiles to satisfy engineering specifications.

Metal Cutting, which includes plasma, laser, and oxy-fuel cutting, is used to size raw steel to project dimensions across nearly all fabrication workflows. This process underpins every downstream fabrication step and therefore scales directly with overall market volume. Fabricators who invest in high-speed automated cutting equipment gain throughput advantages on high-volume projects where cut precision and speed determine delivery timelines.

Metal Shearing is used primarily for thin plate and sheet steel work in cladding, secondary panels, and light framing applications. This process supports the commercial construction and warehousing segments, where demand for fast, cost-effective sheet preparation is highest. Shearing capacity is often integrated into broader fabrication lines to reduce handling time between process steps.

Metal Stamping serves repetitive component production such as connection plates, brackets, and base plates used across all structural steel assemblies. High-volume stamping reduces unit cost on standard connection hardware and supports the industrialisation of fabrication workflows. Fabricators who standardise connection details across project types can leverage stamping economies to improve margin on commodity scope.

Metal Rolling produces hot-rolled and cold-rolled sections that form the raw material input for fabrication operations. Within the fabrication context, rolling processes cover the reshaping of purchased sections into non-standard profiles or the production of proprietary section sizes. Fabricators with in-house rolling capacity reduce raw material lead times and gain the ability to produce custom profiles without dependence on steel mill delivery schedules.

End-use Analysis

Oil and Gas dominates with 39.4% due to continuous capital expenditure in upstream and downstream energy infrastructure.

In 2025, Oil and Gas held a dominant market position in the By End-use segment of the GCC Structural Steel Fabrication Market, with a 39.4% share. GCC national oil companies and international energy operators maintain large capital programs for refinery upgrades, LNG terminals, and offshore platform fabrication that require certified structural steel components. Fabricators with proven track records in energy-sector quality standards hold a defensible position in this segment against new entrants who lack equivalent certification histories.

Manufacturing end-users require structural steel for factory shells, production floors, overhead crane systems, and equipment support frames. Demand in this segment is directly linked to industrial investment across GCC special economic zones and manufacturing parks. Saudi Arabia’s industrial diversification program and the UAE’s advanced manufacturing initiatives create a sustained pipeline of manufacturing facility projects that require structural steel packages.

Power and Energy projects, including thermal and renewable power plants, use structural steel for turbine support structures, transformer pads, transmission towers, and plant buildings. This sub-segment is expanding alongside GCC renewable energy targets, where solar and wind farms require substantial quantities of galvanised structural steel for mounting systems and substation structures. Fabricators who position early in the renewable steel supply chain gain volume access ahead of the segment’s acceleration.

Construction end-users encompass commercial buildings, residential towers, hotels, and mixed-use developments where structural steel competes with reinforced concrete as the primary framing material. Steel’s advantage in high-rise and long-span applications, combined with faster erection cycles, drives adoption in urban development projects across Dubai, Riyadh, and Doha. The commercial construction segment is highly sensitive to real estate market cycles and government infrastructure spending timelines.

Others in the end-use category includes transport infrastructure, marine structures, and utility installations that require fabricated steel components outside the primary sector classifications. This segment responds to government infrastructure programs covering ports, airports, and road networks. GCC government spending commitments in these areas provide a demand floor for fabricators capable of meeting transport and civil infrastructure specifications.

Key Market Segments

By Type

- Heavy Sectional Steel

- Light Sectional Steel

- Others

By Fabrication Process

- Metal Welding

- Metal Forming

- Metal Cutting

- Metal Shearing

- Metal Stamping

- Metal Rolling

By End-use

- Oil and Gas

- Manufacturing

- Power and Energy

- Construction

- Others

Drivers

GCC mega-project pipeline sustains structural steel volumes through 2035

GCC governments are executing the largest infrastructure investment programs in the region’s history. Saudi Arabia’s giga-projects, the UAE’s urban expansion, and Qatar’s post-tournament infrastructure upgrades all require fabricated structural steel at scale. This pipeline gives fabricators with established regional capacity a multi-year order base that reduces the revenue volatility typically associated with project-based construction markets.

According to a BIM implementation study on steel structures, using an integrated BIM workflow in 2025 reduced design-phase clashes by 35% and cut coordination rework by 15%. For fabricators working on GCC mega-projects, this means that adopting BIM directly reduces the cost of errors on large, complex scopes. Firms that embed BIM into their pre-fabrication detailing workflows will deliver projects with fewer change orders and better margin outcomes than competitors still relying on manual coordination.

Industrial facility and logistics park construction across GCC free zones and industrial cities is accelerating. Saudi Arabia’s Sudair Industrial City, where Alghanim Industries through Kirby Building Systems broke ground on a new 100,000-metric-ton annual capacity structural steel facility in February 2025, illustrates how private investment is expanding fabrication supply to serve this demand. This investment signals that major players expect sustained industrial construction volumes through the mid-term forecast period.

Restraints

Steel price volatility increases project cost risk for GCC fabricators

Global steel price cycles directly affect fabricator margins on fixed-price contracts. When raw material costs rise after a contract is signed, the cost increase sits with the fabricator unless escalation clauses are included. GCC fabricators serving government-led infrastructure programs often face rigid procurement rules that limit their ability to pass through cost increases, making price risk management a critical operational discipline.

A 2025 industry article on steel fabrication trends noted that AI-powered inspection systems in steel fabrication can detect dimensional or weld defects with an accuracy exceeding 95%, leading to rework and scrap reductions of 20 to 30% in automated fabrication shops. For fabricators facing steel price pressure, reducing scrap rates by up to 30% is a direct margin recovery lever. Firms that invest in AI-based quality control convert material waste into recoverable cost savings, partially offsetting the impact of raw steel price increases on overall project profitability.

The shortage of certified welders and advanced fabrication technicians constrains production throughput at peak demand periods. GCC fabricators compete for a limited regional pool of skilled workers qualified to meet energy-sector weld standards. As reported by a 2026 UAE fabrication article, robotic welding reduced weld defect rates by up to 60% relative to manual welding in local steel fabrication shops. This evidence shows that automation is not just a cost strategy; it is a direct response to the workforce gap, replacing scarce certified labour on repetitive weld lines with consistent robotic output.

Growth Factors

Renewable energy projects create new structural steel demand streams in GCC

GCC renewable energy targets require structural steel for solar mounting systems, wind turbine foundations, and substation frameworks at a scale the market has not previously addressed. Saudi Arabia’s National Renewable Energy Program and the UAE’s clean energy commitments are converting these targets into active project pipelines. Fabricators who develop certified renewable-energy steel specifications now will capture first-mover positions in a segment that will scale materially through the forecast period.

Based on data from a 2025 BIM-driven modular steel construction study, the use of BIM for prefabricated steel modules reduced on-site assembly time by 20 to 30% compared with conventional methods. This efficiency directly reduces on-site labour and crane time costs for contractors, making BIM-enabled prefabrication a procurement priority for cost-conscious project owners. Fabricators who invest in BIM-linked pre-fabrication workflows will win contracts from contractors who need to meet compressed project schedules.

Worldsteel climate-action guidance updated in 2025 stated that switching to low-carbon steel technologies could reduce CO₂ emissions intensity by 50% or more per tonne of crude steel. GCC governments are beginning to embed embodied carbon metrics in large infrastructure procurement specifications. Fabricators who source low-carbon steel and document their emissions performance will hold a tender advantage over competitors as green procurement rules tighten across the region.

Emerging Trends

Robotic welding raises GCC fabrication productivity by up to 50%

As reported by a 2026 article on robotic welding in UAE fabrication workshops, robotic welding systems can increase welding productivity by 30 to 50% compared with manual welding on repetitive structural steel joints while maintaining consistent quality. This productivity gain is not marginal. It restructures the economics of high-volume fabrication by reducing the number of certified welders required per output unit and improving delivery reliability on large-scale orders.

Digital twin technology is entering GCC fabrication operations as a tool for monitoring production processes, tracking component status, and simulating assembly sequences before physical execution. Fabricators who deploy digital twins on complex projects reduce the risk of sequencing errors and give project owners real-time visibility into fabrication progress. This capability is becoming a differentiator in competitive tender processes for mega-project structural steel packages.

A 2025 environmental assessment of hydrogen-based direct-reduction iron with electric arc furnace routes for steelmaking reported potential reductions in greenhouse-gas emissions of roughly 80 to 90% per tonne of steel compared with conventional blast-furnace routes when powered by renewable electricity. For GCC fabricators, this signals that the upstream steel industry is moving toward low-carbon production methods. Fabricators who align their procurement strategies with low-carbon steel supply chains now will meet emerging green tender requirements ahead of competitors who have not yet addressed embodied emissions in their supply base.

Key Company Insights

Mabani Steel LLC operates from a 125,000-square-meter campus in Ras Al Khaimah with annual capacity of 72,000 metric tons of pre-engineered buildings and 48,000 metric tons of hot-rolled structural steel. This dual-product capability lets the company serve both standard building markets and technically demanding structural projects within a single production facility, reducing the overhead cost of maintaining separate fabrication lines for each product type.

Al Shahin Company for Metal Industries positions itself in the GCC market as a specialist in custom structural steel fabrication for industrial and commercial clients. Data from a 2025 digital fabrication study shows that mobile robotic fabrication technologies could reduce on-site fabrication labour time by approximately 25% and total fabrication-related costs by around 15% compared with conventional manual processes. Fabricators who adopt these technologies gain a direct cost advantage on competitive tenders, and Al Shahin’s industrial client base creates a natural testing ground for robotic fabrication deployment.

IMCC serves the GCC structural steel market with fabrication capabilities targeted at oil and gas and industrial construction segments. The company’s positioning in the energy sector aligns with the highest-value end-use category in the market, where certified welding standards and project track record create defensible barriers against lower-cost competitors. This sector focus limits volume exposure to commodity construction cycles while retaining access to the market’s premium-margin project categories.

Standard Steel Fabrication Co. LLC operates across the GCC with a structural steel portfolio covering construction, industrial, and infrastructure end-uses. This diversified end-use spread reduces the company’s dependency on any single sector’s capital expenditure cycle. However, covering multiple end-use segments without a dominant specialisation can limit the depth of technical certification and client relationships in high-specification markets such as offshore oil and gas fabrication.

Key Players

- Mabani Steel LCC

- Al Shahin Company for Metal Industries

- IMCC

- Standard Steel Fabrication Co. LLC

- Techno Steel

- Aarya Engineering

- Vogue Steel LLC

- AGE Steel

- Attieh Steel

- Gulf Specialized Works

- Station Contracting Ltd.

Recent Developments

- July 2025 – NMDC Energy commenced fabrication operations at its new Ras Al-Khair fabrication yard in Saudi Arabia, a 400,000-square-meter facility designed to manufacture structural steel modules and offshore structures for major GCC energy and infrastructure projects.

- July 2025 – WASI Steel Industries announced the development of a new headquarters and fabrication facility in Dammam 3rd Industrial City, expanding its structural steel fabrication capabilities to serve industrial and infrastructure projects in Saudi Arabia.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 10.7 Billion |

| Forecast Revenue (2035) | USD 17.9 Billion |

| CAGR (2026-2035) | 5.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Heavy Sectional Steel, Light Sectional Steel, Others), By Fabrication Process (Metal Welding, Metal Forming, Metal Cutting, Metal Shearing, Metal Stamping, Metal Rolling), By End-use (Oil and Gas, Manufacturing, Power and Energy, Construction, Others) |

| Competitive Landscape | Mabani Steel LCC, Al Shahin Company for Metal Industries, IMCC, Standard Steel Fabrication Co. LLC, Techno Steel, Aarya Engineering, Vogue Steel LLC, AGE Steel, Attieh Steel, Gulf Specialized Works, Station Contracting Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |