Quick Navigation

Report Overview

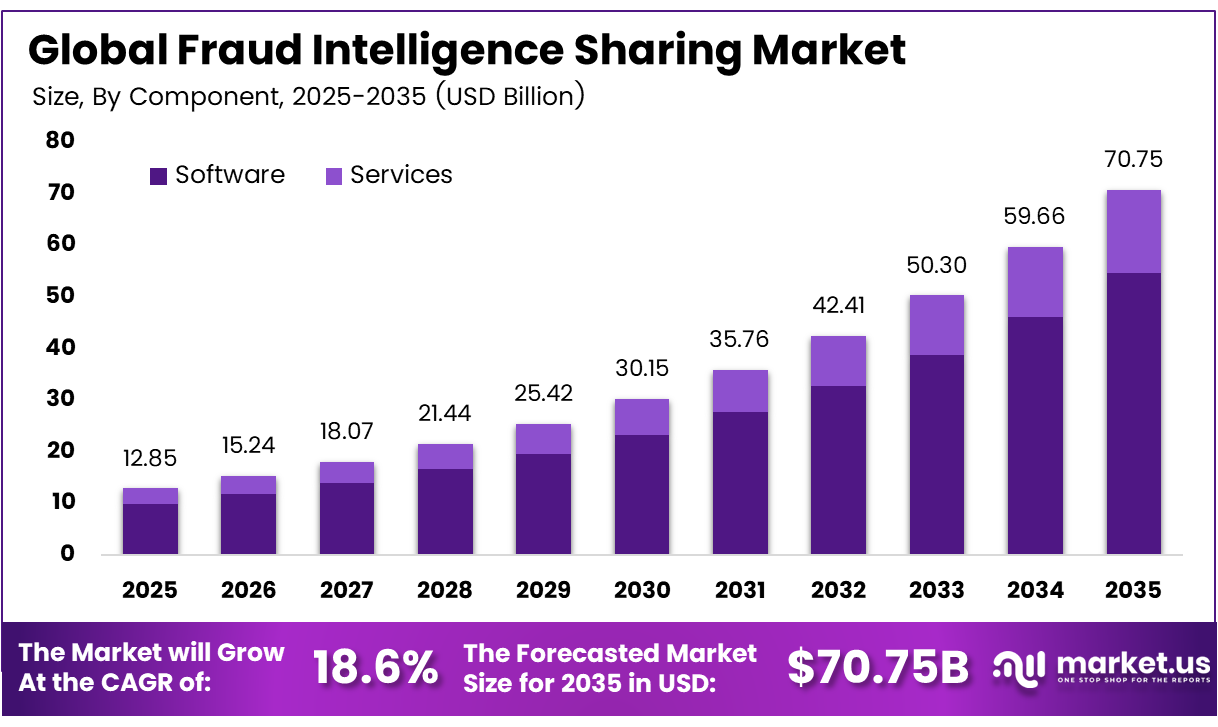

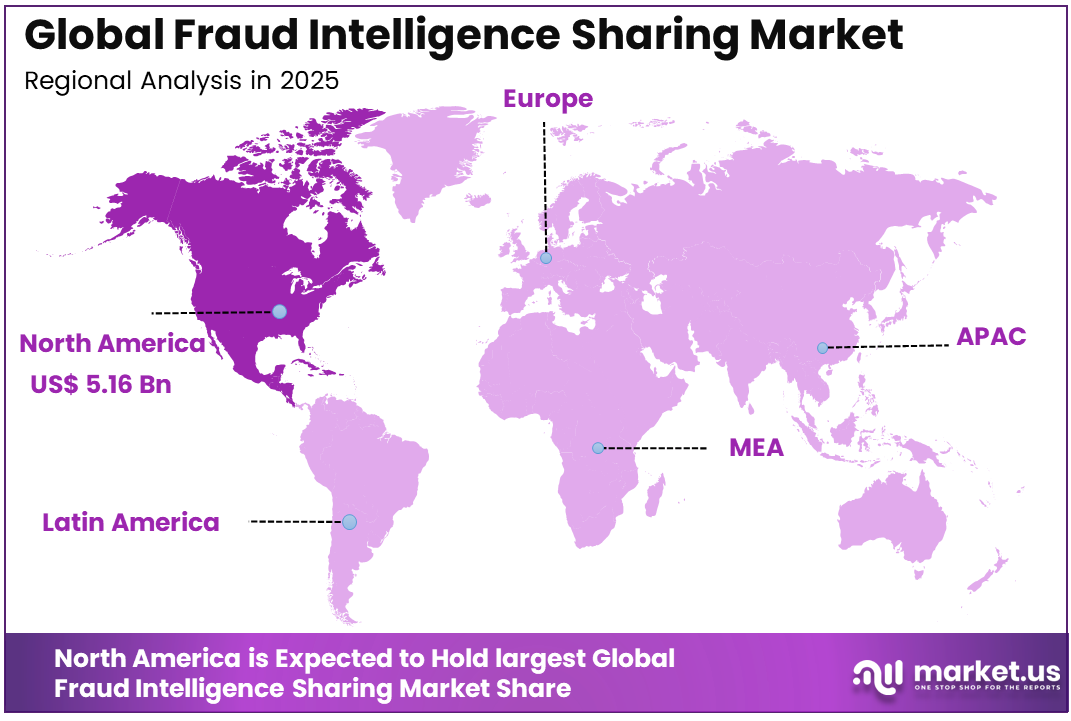

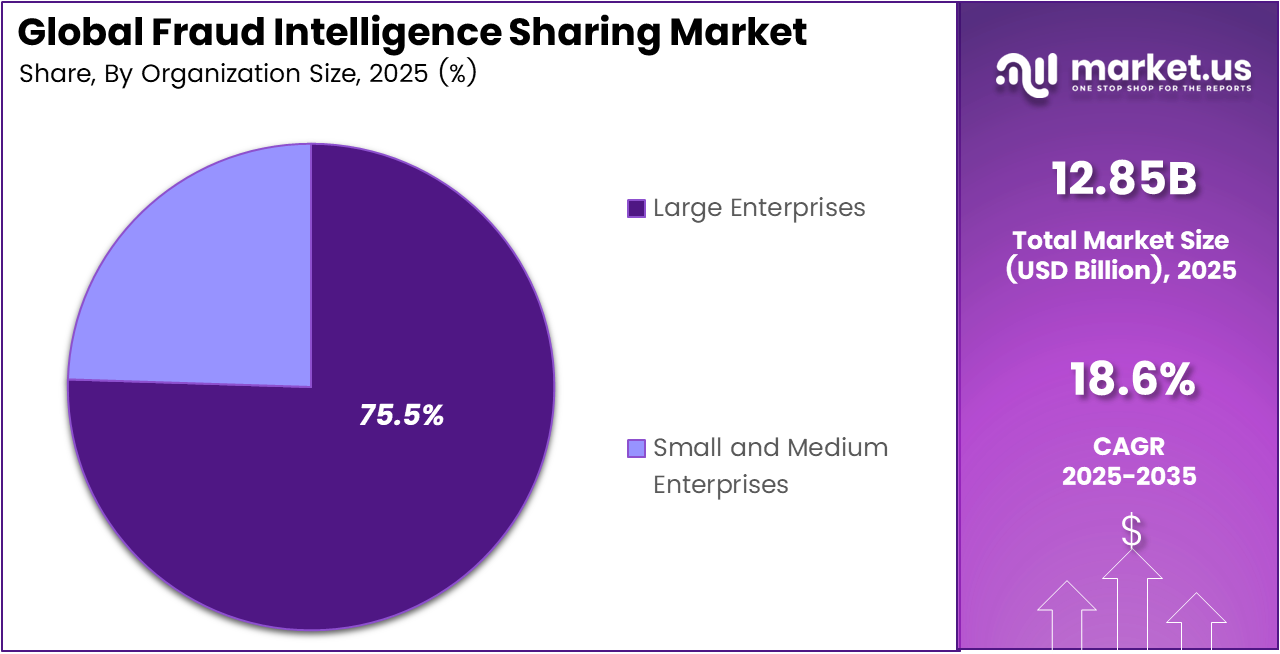

The Global Fraud Intelligence Sharing Market size is expected to be worth around USD 70.75 billion by 2035, from USD 12.85 billion in 2025, growing at a CAGR of 18.6% during the forecast period from 2025 to 2035. North America held a dominant market position, capturing more than a 40.2% share, holding USD 5.16 billion in revenue.

Fraud Intelligence Sharing refers to the secure exchange of fraud-related signals, risk patterns, and suspicious activity data between trusted organizations. It helps banks, payment firms, merchants, and public agencies detect fraud earlier, reduce repeated attacks, and make better decisions by using wider ecosystem insight instead of relying only on internal data.

Cross-border payment growth, instant payout schemes, and mule infrastructure now explain over 90% of new fraud growth in some scam types, which are key driving factors. These trends expose major gaps when each institution sees only its own data. Remote onboarding and card-not-present transactions add further pressure, as identity errors can be reused quickly across providers.

The market for Fraud Intelligence Sharing is driven by the rapid rise in digital fraud, instant payments, remote onboarding, and identity misuse across financial channels. Banks, fintech firms, and merchants need shared risk signals to detect suspicious activity earlier. As fraud networks move across institutions, wider intelligence sharing helps reduce losses, improve investigations, and protect genuine customers from unnecessary friction.

Demand is strongest where fraud ratios on digital channels have climbed by double digits and internal teams cannot manage rising alert volumes. Collaborative intelligence networks help institutions improve risk detection, reduce false positives, and support smoother customer journeys. Wider ecosystem visibility allows decisions to be based on broader behavior patterns, rather than limited internal transaction data.

For instance, in December 2025, in updated anti-fraud and financial crime market coverage, BAE Systems continues to be profiled as a core vendor in enterprise fraud and AML platforms, especially for banks and governments. Its investments in analytics-driven, case-management tools underline how large institutions are standardising on shared intelligence hubs rather than siloed fraud tools.

Key Takeaway

- In 2025, the Software segment held a dominant market position, capturing a 77.2% share of the Global Fraud Intelligence Sharing Market.

- In 2025, the On-Premises segment held a dominant market position, capturing a 80.5% share of the Global Fraud Intelligence Sharing Market.

- In 2025, the Banking and Financial Services segment held a dominant market position, capturing a 36.9% share of the Global Fraud Intelligence Sharing Market.

- In 2025, the Large Enterprises segment held a dominant market position, capturing a 75.5% share of the Global Fraud Intelligence Sharing Market.

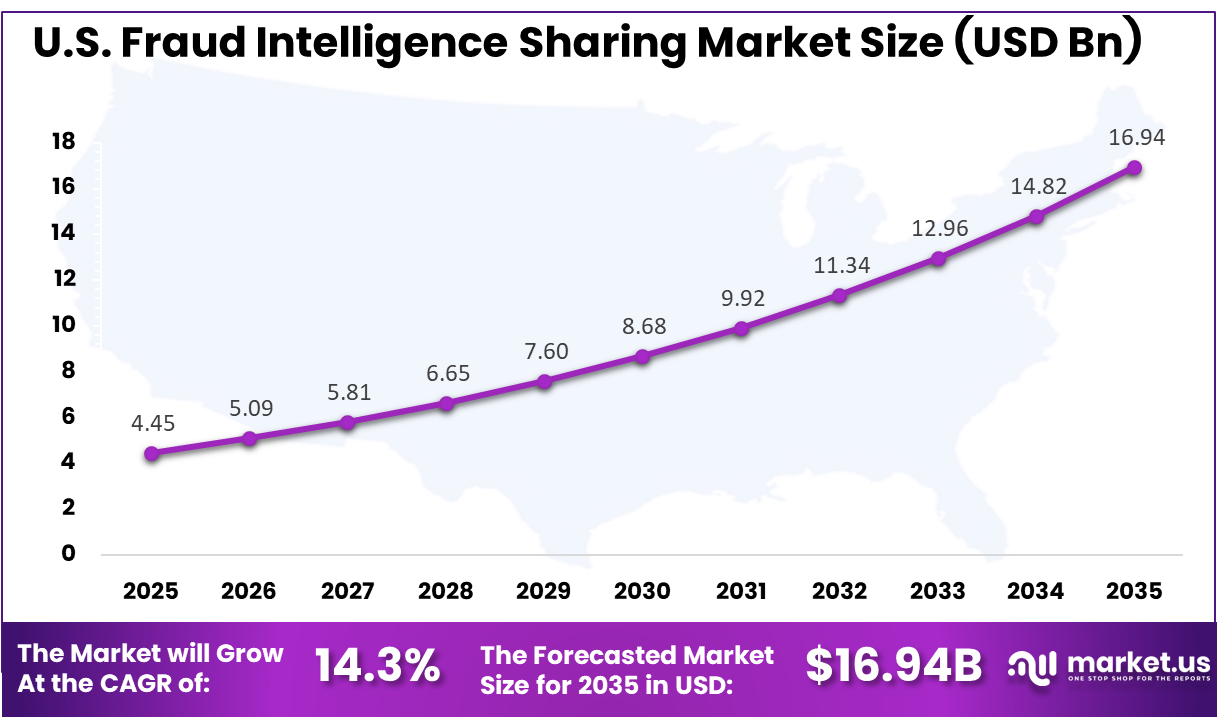

- The U.S. Fraud Intelligence Sharing Market was valued at USD 4.45 billion in 2025, with a robust CAGR of 14.3%.

- In 2025, North America held a dominant market position in the Global Fraud Intelligence Sharing Market, capturing more than a 40.2% share.

Role of Generative AI

Generative AI is changing fraud prevention and fraud execution at the same time. Banks use it to simulate attacker behaviour, test control gaps, and create synthetic data for rare fraud events. This helps machine learning models behind shared fraud networks become more stable, especially when real fraud samples are limited.

Fraudsters are also using generative AI to scale phishing, fake identities, and deepfake interactions. Professional bodies have listed generative AI-powered scams and synthetic IDs among the top fraud trends heading into 2025. Some AI-based fraud engines can reach detection accuracy in the mid 90s when trained on rich datasets.

Investment and Business Benefits

Investment opportunities are growing around platforms that support privacy-preserving queries, cross-rail coverage, and explainable risk indicators instead of simple yes or no outputs. These tools help address fragmented coverage and high latency. Specialist providers also have room to combine telecom data, behavioral biometrics, and open source intelligence for banking, e-commerce, and government systems.

Business benefits go beyond fraud loss reduction, as shared intelligence can reduce investigation time, improve alert prioritisation, and support more targeted authentication. These improvements lower operating costs and reduce customer friction. Over time, a richer view of behavior also helps firms sharpen product pricing, set better risk-based limits, and identify safer customer segments.

Regional Analysis

In 2025, North America held a dominant market position in the Global Fraud Intelligence Sharing Market, capturing more than a 40.2% share, holding USD 5.16 billion in revenue. This dominance is due to its advanced digital banking ecosystem, high card and online payment usage, and strong focus on financial crime prevention. The region has broad adoption of AI-based fraud analytics, shared risk databases, and real-time payment monitoring. Strong regulatory oversight, mature banking infrastructure, and active collaboration among banks, fintech firms, and payment networks further support market leadership.

For instance, in January 2026, NICE Actimize launched the Actimize Insights Network from its Hoboken base, a real-time fraud and financial-crime intelligence network that lets U.S. and global institutions securely share counterparty-risk signals, turning fragmented data into a unified defense layer and underscoring North American leadership in collaborative fraud intelligence sharing.

U.S. Fraud Intelligence Sharing Market Size

The market for Fraud Intelligence Sharing within the U.S. is growing tremendously and is currently valued at USD 4.45 billion; the market has a projected CAGR of 14.3%. The market is growing due to rising digital payment fraud, faster instant payment adoption, and stronger pressure on banks to detect mule accounts and identity misuse earlier. Financial institutions are increasing investment in shared risk data, AI-based scoring, and real-time monitoring to reduce losses and false alerts. The U.S. also benefits from strict compliance needs and wider cooperation between banks, fintech firms, and regulators.

For instance, in March 2026, IBM introduced new agentic AI-enabled capabilities in its Safer Payments platform to accelerate fraud detection, investigation, and response while preserving accuracy and regulatory transparency in high-volume U.S. payment environments, reinforcing North America’s edge in advanced fraud intelligence and counter-crime analytics.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Component Analysis

In 2025, the Software segment held a dominant market position, capturing a 77.2% share of the Global Fraud Intelligence Sharing Market. This dominance is due to the need for fast fraud detection, secure data sharing, and better case handling across institutions. Software platforms help banks and payment firms connect fraud signals, review risky activity, and improve response quality without depending only on internal alerts.

Software also supports flexible rule setting, automated checks, and clearer risk scoring for fraud teams. As fraud patterns move quickly across channels, institutions need systems that can combine different data sources and present useful insights for faster action.

For instance, in May 2025, IBM expanded its counter fraud software services, focusing on using big data and advanced analytics to help banks and governments detect complex financial crime patterns across channels. The initiative highlighted how integrated software platforms can turn diverse internal and external signals into a single investigative view, improving response to emerging fraud schemes.

Deployment Mode Analysis

In 2025, the On-Premises segment held a dominant market position, capturing a 80.5% share of the Global Fraud Intelligence Sharing Market. This dominance is due to the sensitive nature of fraud data, customer identity records, and transaction information. Many financial institutions prefer keeping these systems within their own infrastructure to maintain stronger control over security, access, and compliance.

On-premises deployment also supports internal governance needs in highly regulated sectors. It allows organizations to manage data handling, audit trails, and system updates under strict internal policies, which is important when fraud intelligence is shared across trusted networks.

For instance, in October 2025, IBM announced that ACI Worldwide’s payment and fraud detection solutions will run natively on IBM Z systems starting in late 2025, keeping mission-critical workloads close to core banking data. This move shows how many institutions still favor on-premises mainframe environments for high-volume payments and fraud analytics that need tight security and reliability.

Application Analysis

In 2025, the Banking and Financial Services segment held a dominant market position, capturing a 36.9% share of the Global Fraud Intelligence Sharing Market. This dominance is due to the high fraud exposure faced by banks, payment providers, and financial institutions. These organizations deal with account takeover, phishing, mule activity, card fraud, and suspicious transactions, which makes shared intelligence highly important for early risk detection.

Banking and financial services also operate across large customer bases and multiple payment channels. Fraud signals often appear in one institution before spreading to another, so wider intelligence sharing helps improve prevention, reduce losses, and protect customer trust.

For instance, in May 2025, Experian reported that banks and financial providers were blocking rising levels of identity fraud using more advanced prevention technology and analytics. The update showed how financial institutions are strengthening layered controls, including biometric and behavioral tools, to better protect digital banking customers.

Organization Size Analysis

In 2025, the Large Enterprises segment held a dominant market position, capturing a 75.5% share of the Global Fraud Intelligence Sharing Market. This dominance is due to the larger transaction volumes, broader digital operations, and complex fraud risks handled by large enterprises. These organizations usually have stronger budgets, dedicated fraud teams, and advanced compliance functions, making the adoption of fraud intelligence sharing platforms easier.

Large enterprises also need faster alert prioritisation and coordinated investigations across business units. Shared intelligence helps them identify repeat fraud patterns, improve authentication decisions, and reduce manual review pressure, while supporting better risk control across banking, e-commerce, and digital service operations.

For instance, in May 2025, NICE Actimize announced its ENGAGE 2025 event, focused on how large financial institutions can use AI and collective intelligence to manage fraud and financial crime more effectively. Sessions with banks, regulators, and law enforcement emphasized the need for scalable platforms that can support complex operations and global footprints.

Key Market Segments

By Component

- Software

- Services

By Deployment Mode

- On-Premises

- Cloud

By Application

- Banking and Financial Services

- Insurance

- E-commerce

- Government

- Telecom

- Healthcare

- Others

By Organization Size

- Large Enterprises

- Small and Medium Enterprises

Emerging Trends

A major trend is the shift from single institution monitoring to collaborative, network-level fraud intelligence. Mule accounts and funnel structures are now being tracked across banks in near real time. In one large market, mule-related filings grew over 20% year on year and caused more than 90% of fraud report growth.

Shared intelligence is also improving detection performance for financial institutions. Banks connected to one vendor-led network reported about a 68% uplift in fraud detection. They also identified bad counterparties roughly two months earlier on average than internal models, showing how wider data visibility can improve response speed and fraud prevention quality.

Growth Factors

The rise of digital and instant payments is a key growth factor, as it has expanded fraud exposure faster than many traditional controls can manage. This pressure is pushing banks, payment firms, and regulators toward collaborative defences that can detect suspicious activity across accounts, channels, and institutions more effectively.

Regulatory pressure around authorised push payment fraud is also strengthening the adoption of shared databases. Fraud analytics solutions already account for a majority share of deployments, and more platforms are moving toward real-time, multi-channel scoring. As AI tools connect with cross-institution feeds, each new participant improves model quality and risk scoring accuracy.

Market Dynamics

Drivers - Rising Digital Fraud

Rising digital fraud is increasing the need for stronger intelligence sharing across banks, payment firms, and digital platforms. Fraud attempts often move across multiple accounts and channels, making it difficult for one institution to detect the full pattern on its own.

Shared fraud intelligence helps organizations identify suspicious behaviour earlier and respond with better accuracy. It allows fraud teams to connect warning signs from wider sources, reduce repeated attacks, and protect customers without adding unnecessary friction to genuine transactions.

For instance, in April 2026, IBM worked with a major UK bank on a quantum fraud detection experiment to identify money mule patterns hidden in complex transaction graphs. By using a quantum device to analyze large networks of payments, IBM targeted new mule tactics that exploit rising instant and digital transfer volumes.

Restraint - Data Privacy Concerns

Data privacy concerns remain a major restraint for the Fraud Intelligence Sharing Market. Institutions handle sensitive customer records, payment details, and identity information, so any data exchange must meet strict privacy, security, and compliance requirements before it can be trusted.

Many organizations hesitate to share fraud signals because of legal risk, customer confidentiality, and internal governance rules. This slows collaboration and increases the need for privacy-preserving methods that allow useful fraud detection without exposing raw personal or financial data.

For instance, in November 2025, LexisNexis Risk Solutions won a regional award for its ThreatMetrix and IDVerse offerings, which combine device, behavioral, and identity data while operating fraud intelligence consortiums in Asia. The recognition emphasized that strong privacy controls and compliant data sharing are critical to expanding cross-institution fraud networks.

Opportunities - Real-Time Risk Networks

Real-time risk networks create a strong opportunity for the Fraud Intelligence Sharing Market. These networks allow institutions to share risk signals quickly, helping them detect mule accounts, suspicious transactions, and identity misuse before fraud spreads across the ecosystem.

As digital payments become faster, delayed fraud detection can increase losses and investigation pressure. Real-time networks support quicker decisions, better alert prioritisation, and smoother customer verification, making them valuable for banks, fintech firms, e-commerce platforms, and public sector agencies.

For instance, in September 2025, ACI Worldwide detailed its real-time payments fraud management solution, which screens transactions instantly and integrates network intelligence from schemes and partner data sources. The platform shows how shared signals across payment rails can help banks act within milliseconds to stop high-velocity digital fraud.

Challenges - Talent Shortages

Talent shortages are a key challenge for the Fraud Intelligence Sharing Market. Effective fraud intelligence requires skilled teams that understand financial crime, data analytics, cybersecurity, compliance, and investigation workflows. Many institutions struggle to find professionals who can manage these areas together.

Limited talent can slow platform adoption, reduce model quality, and weaken investigation outcomes. Organizations may have access to advanced tools, but without trained analysts and technical specialists, it becomes difficult to interpret shared signals, tune risk models, and act on fraud alerts effectively.

For instance, in April 2026, Experian’s Future of Fraud material pointed out that as agentic AI raises both attack and defense capabilities, many organizations struggle to keep fraud skills and analytics expertise up to date. The company encourages clients to use its platforms to fill internal gaps in modeling and monitoring.

Key Players Analysis

One of the leading players in the market, in February 2026, Experian acquired AtData, a specialist in identity and data intelligence, to deepen its fraud-detection and identity-verification capabilities. The deal gives Experian richer email and identity signals that can be shared across clients, strengthening consortium-style intelligence and improving detection of synthetic identities and account takeovers.

Top Key Players in the Market

- BAE Systems

- IBM Corporation

- NICE Actimize

- FICO

- Experian

- ACI Worldwide

- SAS Institute

- Oracle Corporation

- LexisNexis Risk Solutions

- Refinitiv

- FIS (Fidelity National Information Services)

- Featurespace

- Feedzai

- NICE Ltd.

- BioCatch

- ThreatMetrix

- RSA Security

- Kount (an Equifax company)

- Cybersource (a Visa solution)

- FRISS

- Others

Recent Developments

- In April 2026, new fraud detection and prevention market studies highlight large platform vendors such as IBM as key beneficiaries of the shift to unified fraud and AML stacks. Banks are increasingly asking for integrated data lakes and shared risk-intelligence layers, an area where IBM’s hybrid-cloud and analytics portfolio is being actively positioned.

- In February 2026, industry analysts listing the best fraud platforms for 2026 place NICE Actimize among the top offerings for banks looking to converge fraud and AML operations. The platform’s focus on real-time behavioural analytics and cross-institution intelligence feeds is helping large financial institutions cut false positives and investigate complex mule networks more efficiently.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 12.85 Billion |

| Forecast Revenue (2035) | USD 70.75 Billion |

| CAGR (2026-2035) | 18.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Component (Software, Services), By Deployment Mode (On-Premises, Cloud), By Application (Banking and Financial Services, Insurance, E-commerce, Government, Telecom, Healthcare, Others), By Organization Size (Small and Medium Enterprises, Large Enterprises) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | BAE Systems, IBM Corporation, NICE Actimize, FICO, Experian, ACI Worldwide, SAS Institute, Oracle Corporation, LexisNexis Risk Solutions, Refinitiv, FIS (Fidelity National Information Services), Featurespace, Feedzai, NICE Ltd., BioCatch, ThreatMetrix, RSA Security, Kount (an Equifax company), Cybersource (a Visa solution), FRISS, Others |

| Customization Scope | Customization at the segment and region/country levels will be provided. Moreover, customization can be tailored to the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |