Global Fire Door Market Size, Share, Growth Analysis By Material Type (Steel, Timber/Wood, Glass, Aluminum, Composite, Others), By Mechanism (Swinging, Sliding, Rolling, Folding), By Fire Rating (30 Minutes, 60 Minutes, 90 Minutes, 120 Minutes, 180 Minutes), By End User (Commercial, Residential, Industrial), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 181169

- Number of Pages: 306

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

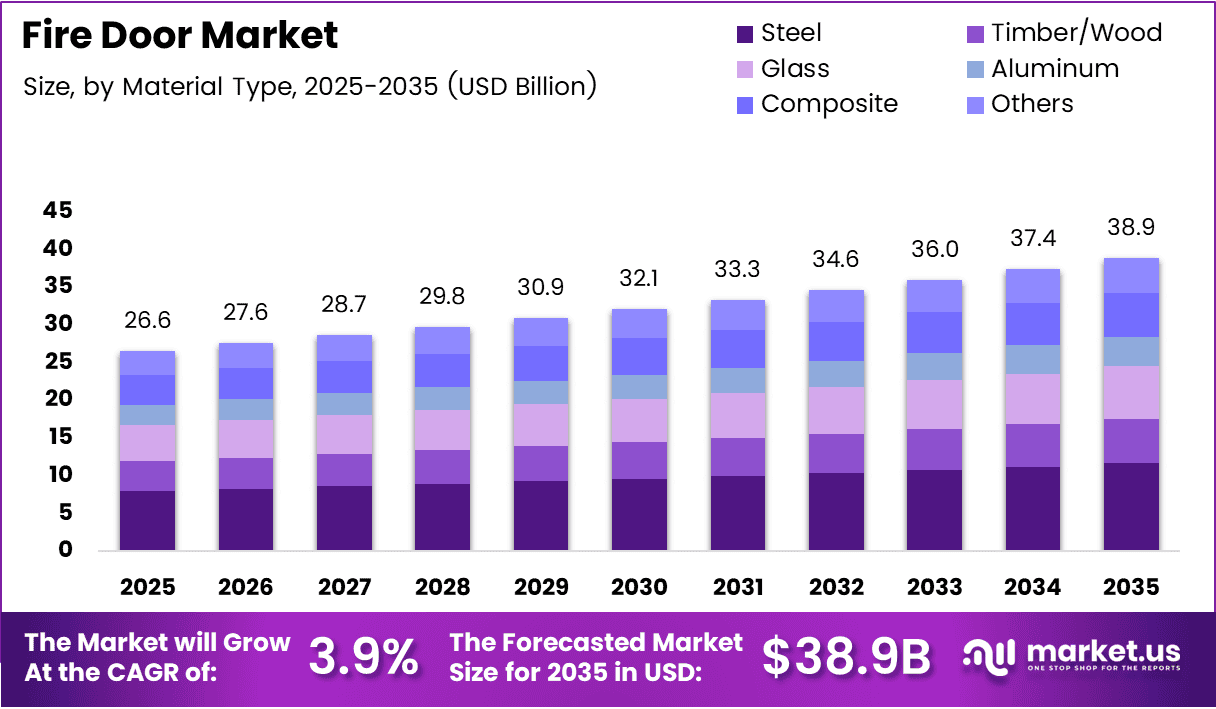

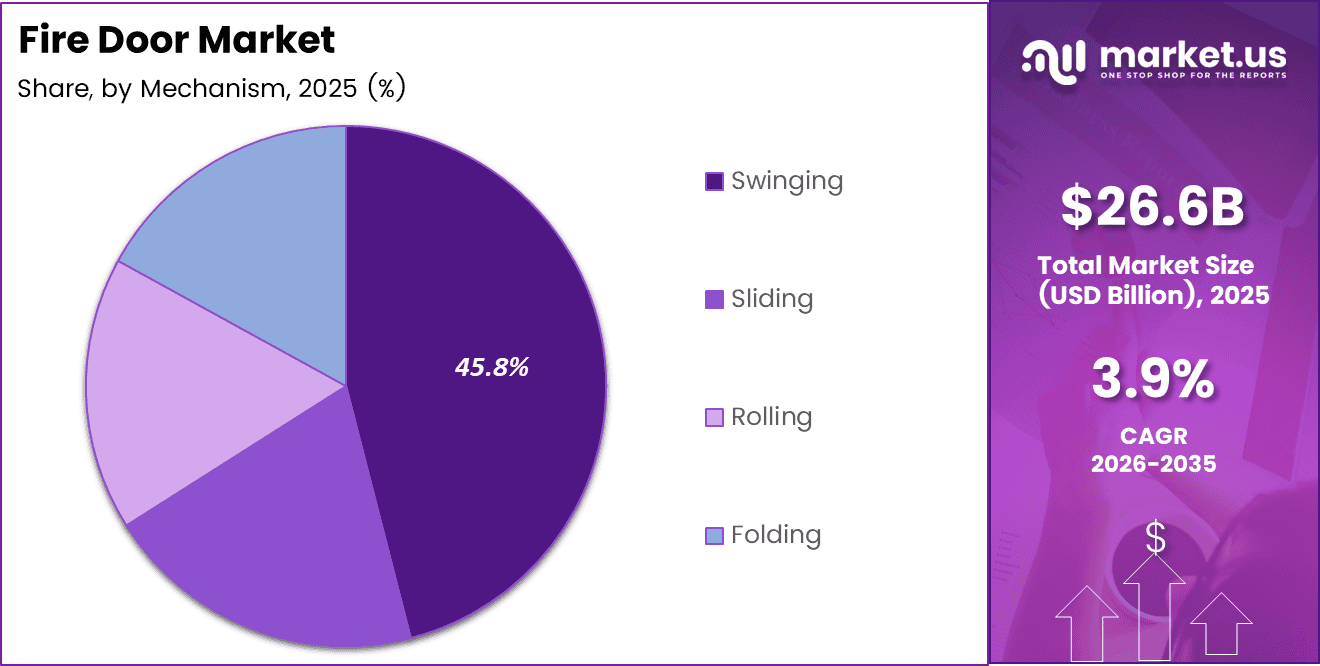

Global Fire Door Market size is expected to be worth around USD 38.9 Billion by 2035 from USD 26.6 Billion in 2025, growing at a CAGR of 3.9% during the forecast period 2026 to 2035.

Fire doors form the structural backbone of passive fire protection in buildings. These fire-rated assemblies contain the spread of fire and smoke, giving occupants time to evacuate while limiting structural damage. Commercial buildings, industrial facilities, hospitals, and high-rise residential complexes all depend on certified fire door systems to meet mandatory safety standards.

Mandatory building codes across North America, Europe, and Asia Pacific now require fire-rated door assemblies in nearly all new commercial construction. Governments are raising the bar on compliance enforcement, converting what was once a discretionary safety measure into a non-negotiable procurement line item. This shift fundamentally changes the buyer base from risk-aware early adopters to a far broader pool of mandatory purchasers.

Urban expansion and smart city development worldwide are creating consistent demand for fire-rated door systems in airports, metro stations, hotels, and data centers. The commercial construction pipeline in Asia Pacific alone signals multi-year forward demand for certified fire door products and installation services, making this a structurally supported market rather than one dependent on cyclical project activity.

Rising retrofit activity in aging commercial and public infrastructure adds a second revenue channel alongside new construction. Buildings built before modern fire codes were enacted now face regulatory pressure to upgrade passive fire protection systems. This retrofit cycle is particularly visible in Western Europe and North America, where building stock is older and compliance timelines are tightening.

Industrial facilities, hospitals, and educational institutions represent a buyer segment actively increasing investment in fire protection infrastructure. These end users operate in environments where fire risk carries severe human and financial consequences. Their procurement decisions prioritize certified performance over cost minimization — a dynamic that supports premium pricing and longer vendor relationships.

According to the Fire Door Inspection Scheme, as reported by Fire Door Journal in February 2026, care and maintenance issues appear in 54% of fire door inspections. This figure reveals that installation and maintenance quality remain the market’s most persistent structural gap — creating a recurring service revenue opportunity for compliant suppliers and inspection-led businesses.

According to YK manufacturer technical blog analysis from March 2026, over 30% of fire door prototypes fail their initial lab certification test. This failure rate signals that technical compliance barriers are high enough to concentrate market share among manufacturers with mature testing capabilities — raising the competitive floor and limiting entry for under-resourced suppliers.

Key Takeaways

- The Global Fire Door Market was valued at USD 26.6 Billion in 2025 and is forecast to reach USD 38.9 Billion by 2035.

- The market grows at a CAGR of 3.9% during the forecast period 2026 to 2035.

- By Material Type, Steel dominates with a 28.5% share in 2025.

- By Mechanism, Swinging doors hold the largest share at 45.8% in 2025.

- By Fire Rating, the 60-Minute segment leads with 31.6% share in 2025.

- By End User, the Commercial segment accounts for 45.6% of total market share in 2025.

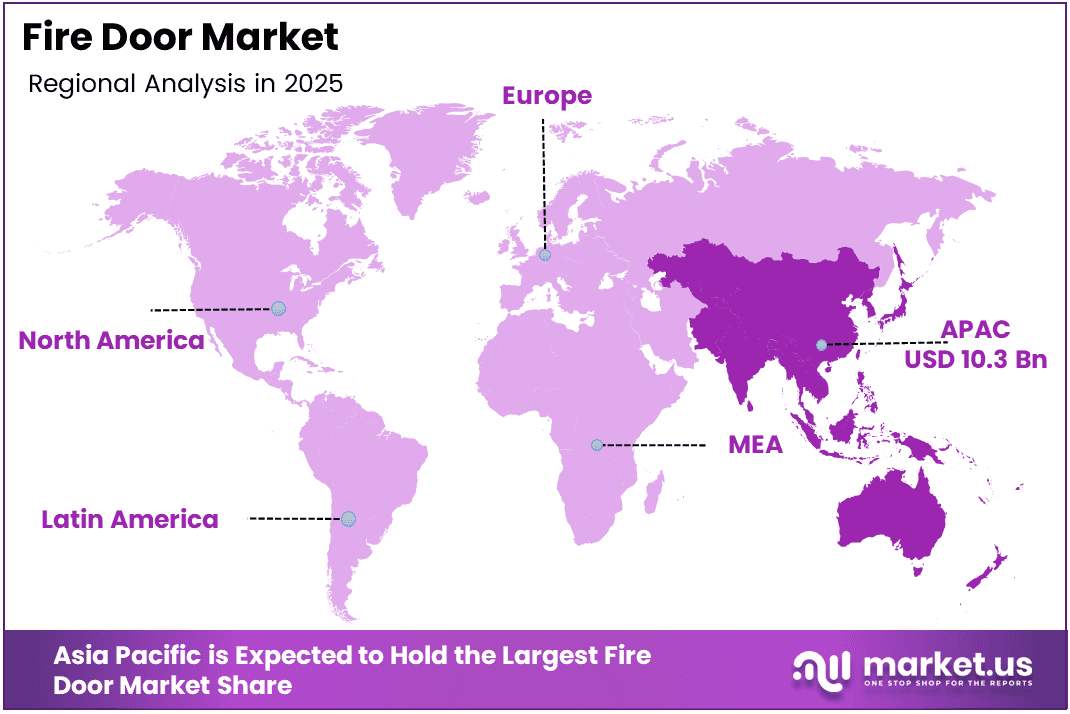

- Asia Pacific dominates regionally with 38.8% market share, valued at USD 10.3 Billion in 2025.

Material Type Analysis

Steel dominates with 28.5% due to superior fire resistance and structural durability.

In 2025, Steel held a dominant market position in the By Material Type segment of the Fire Door Market, with a 28.5% share. Steel fire doors offer the highest structural integrity under sustained heat exposure, making them the default specification in commercial, industrial, and high-security environments. This material preference reflects buyer willingness to pay a premium for certified performance over lower-cost alternatives.

Timber/Wood serves as the preferred material for residential and heritage building applications where aesthetic compatibility matters alongside fire resistance. Wood-core fire doors offer design flexibility that steel cannot match, making them the dominant choice in hospitality, upscale residential, and renovation projects. However, timber door performance depends heavily on core construction quality and moisture management, creating variability in field compliance outcomes.

Glass fire doors differentiate through transparency and architectural integration in commercial interiors, particularly in office lobbies, corridors, and retail environments. Their adoption reflects the convergence of safety requirements with modern open-plan design preferences. Fire-rated glass technology has advanced to enable larger glazed panels without compromising integrity ratings, expanding the addressable application base for this material segment.

Aluminum carries structural advantages in terms of weight-to-strength ratio, making it relevant for large-format sliding and folding fire door applications. However, research published in the MDPI Fire journal in 2026 shows that stainless steel frames outperform aluminum alloy by achieving a 25% lower maximum frame temperature — a performance gap that may gradually shift specifications away from aluminum in high-criticality installations.

Composite fire doors combine multiple materials to balance fire resistance, acoustic performance, thermal insulation, and cost. Their growing specification in healthcare and education facilities reflects end user demand for multi-attribute performance within a single door assembly. Composite construction also allows manufacturers to optimize intumescent seal performance and core density without being constrained by single-material limitations.

Others in the material segment include specialty configurations using fiberglass, gypsum-core assemblies, and hybrid constructions for niche industrial environments. These represent a small share of total volume but carry higher unit value due to custom engineering requirements. Specialized applications in chemical plants and data centers drive specification of non-standard materials where standard steel or timber products cannot meet environmental or operational demands.

Mechanism Analysis

Swinging doors dominate with 45.8% due to simplicity, low cost, and universal code acceptance.

In 2025, Swinging doors held a dominant market position in the By Mechanism segment of the Fire Door Market, with a 45.8% share. Single and double-leaf swinging configurations satisfy fire door requirements across the widest range of building types and fire ratings. Their mechanical simplicity reduces installation cost, minimizes maintenance complexity, and meets certification requirements under nearly all major fire codes globally.

Sliding fire doors address space-constrained environments where a swinging leaf would obstruct pedestrian flow or equipment movement. Their adoption is concentrated in hospitals, manufacturing facilities, and large commercial buildings where corridor widths demand a compact door solution. Sliding mechanisms add mechanical complexity compared to swinging variants, which creates both a higher price point and a larger maintenance requirement for building operators.

Rolling fire doors provide large-opening protection for warehouse bays, loading docks, and industrial access points where standard door leaf sizes are insufficient. These systems typically operate on fusible link or motorized closure mechanisms that activate automatically under heat or smoke detection triggers. Their application is almost entirely industrial and commercial, with minimal residential use.

Folding fire doors offer wide-opening capability with compact storage when open, making them applicable in auditoriums, conference centers, and large public spaces. Their specification is niche but consistent across hospitality and institutional building types. Folding mechanism complexity demands rigorous maintenance scheduling to ensure reliable emergency closure, which adds to total cost of ownership for building operators.

Fire Rating Analysis

60-Minute rated doors dominate with 31.6% due to balanced performance and broad code applicability.

In 2025, 60-Minute fire-rated doors held a dominant market position in the By Fire Rating segment of the Fire Door Market, with a 31.6% share. The 60-minute rating satisfies the minimum requirement for most commercial corridor and stairwell applications under international fire codes, creating the broadest addressable demand base. This rating tier represents the optimal cost-performance balance for the majority of commercial building developers and contractors.

30-Minute rated doors serve lower-risk internal partition applications where the primary function is containing early-stage fire spread rather than providing extended compartmentation. Their specification is common in residential buildings and low-rise commercial structures. While they carry the lowest unit price within the fire rating hierarchy, volume demand remains consistent because they satisfy requirements in the largest number of low-to-medium risk occupancy types.

90-Minute rated doors address mid-tier compartmentation requirements in buildings where occupancy risk or building height triggers enhanced fire resistance specifications. Their specification is common in healthcare, education, and government facilities. According to YK manufacturer technical blog analysis from March 2026, an 18% non-compliance rate was identified in post-installation field integrity checks of 90-minute rated assemblies — highlighting that this rating tier demands particularly rigorous installation quality control.

120-Minute fire-rated doors serve high-risk commercial and industrial environments where extended fire resistance is mandated by code or risk assessment. These products command a significant price premium over 60-minute equivalents and are typically specified by fire engineers rather than general contractors. Demand concentration is in high-rise buildings, data centers, and critical infrastructure where evacuation timelines require extended passive protection.

180-Minute fire-rated door assemblies represent the highest performance tier and are specified almost exclusively for industrial hazard environments, nuclear facilities, and specialized government infrastructure. Their production volume is limited, but unit value is substantially higher than lower-rated products. Procurement involves bespoke engineering, extended lead times, and dedicated certification processes — creating high barriers for both buyers and suppliers.

End User Analysis

Commercial end users dominate with 45.6% due to mandatory compliance in high-occupancy buildings.

In 2025, Commercial end users held a dominant market position in the By End User segment of the Fire Door Market, with a 45.6% share. Office buildings, retail complexes, hotels, hospitals, airports, and educational institutions all fall within this category and operate under the most stringent fire door installation and inspection mandates globally. Commercial buyers also drive recurring demand through mandatory annual inspection and remediation cycles.

Residential end users represent a structurally different demand profile, driven by national building regulations that increasingly require fire doors in multi-family housing, social housing blocks, and high-rise apartment buildings. Following high-profile building fire incidents across Europe and Asia, regulatory bodies have strengthened requirements for residential fire door installation and inspection. This enforcement shift is converting a historically under-penetrated segment into a consistent revenue contributor.

Industrial end users specify fire doors for manufacturing plants, warehouses, chemical storage facilities, and utility infrastructure where fire risk is elevated by process hazards and stored materials. Industrial buyers prioritize functional performance, durability, and compatibility with automated closure and access control systems over aesthetic considerations. This segment supports premium product specifications and generates strong demand for large-format rolling and sliding fire door configurations.

Key Market Segments

By Material Type

- Steel

- Timber/Wood

- Glass

- Aluminum

- Composite

- Others

By Mechanism

- Swinging

- Sliding

- Rolling

- Folding

By Fire Rating

- 30 Minutes

- 60 Minutes

- 90 Minutes

- 120 Minutes

- 180 Minutes

By End User

- Commercial

- Residential

- Industrial

Drivers

Mandatory Fire Safety Codes and Urban Infrastructure Expansion Force Structural Demand Across All Building Types

Building fire safety codes now mandate certified fire door installation across commercial, residential, and industrial construction in most major economies. Governments are moving from guidance-based frameworks to enforceable standards with penalties for non-compliance. This regulatory shift converts fire door procurement from an optional upgrade into a compulsory budget line — fundamentally broadening the buyer base beyond safety-conscious early adopters.

The rapid expansion of high-rise buildings, smart cities, and large-scale urban infrastructure creates a pipeline of projects that require fire door systems by code. Airports, metro stations, hotels, and data centers each carry specific fire compartmentation requirements that generate substantial unit volumes per project. In March 2024, IK Partners acquired Checkmate Fire, a UK passive fire protection specialist, signaling that institutional capital recognizes the structural demand underpinning this market.

According to YK manufacturer technical blog analysis from March 2026, a 98.5% first-pass acceptance rate during AHJ inspections — a 23.5 percentage point improvement over the industry average of 75% — is achievable through structured quality systems. This gap between best practice and industry average tells buyers and regulators that compliance outcomes vary significantly by supplier, raising the commercial value of certified, quality-controlled manufacturing.

Restraints

High Certification Costs and Complex Compliance Procedures Limit Market Accessibility for Smaller Operators

Certified fire-rated door systems carry substantially higher installation and maintenance costs than standard door products. Building owners face recurring expenditure on mandatory inspections, remediation of non-conformances, and component replacement to maintain certification status. These costs create budget pressure particularly in residential and public sector projects where capital allocation for passive fire protection competes with other construction priorities.

Manufacturing and installing fire doors requires navigating multi-layered certification requirements that vary by jurisdiction, fire rating class, and end use. Obtaining and maintaining product certification under standards such as NFPA 80 or EN 1634 demands significant investment in testing, documentation, and quality management. According to YK manufacturer technical blog analysis from March 2026, a single re-test cycle for failed fire door prototypes can easily exceed $100,000 — a cost barrier that limits the supplier pool and slows product innovation cycles.

Complex compliance procedures also create friction at the installation stage. Non-compliant anchor types, insufficient anchor quantities, and improper frame-to-wall connections are documented failure points that generate costly remediation. The average remediation cost for major non-conformances stands at $3,500 per opening according to YK manufacturer technical blog analysis from March 2026 — a figure that accumulates rapidly across large commercial projects and deters smaller contractors from entering the certified installation space.

Growth Factors

Smart Technology Integration and Emerging Market Expansion Open New Revenue Streams for Fire Door Suppliers

Fire doors integrated with building automation systems, access control, and IoT-based safety monitoring represent a higher-value product category than standard fire-rated assemblies. Building operators increasingly specify smart fire doors that provide real-time status monitoring, automated closing on alarm activation, and digital audit trails for compliance reporting. This integration premium creates a margin expansion opportunity for manufacturers that invest in connectivity capabilities.

Emerging economies across Asia, the Middle East, and Latin America are building fire safety infrastructure to meet the demands of rapid urbanization and new commercial construction activity. These markets are earlier in their regulatory maturity cycle, meaning adoption of certified fire door systems will accelerate as local building codes align with international standards. Suppliers with established certification credentials in mature markets hold a structural advantage in capturing early share in these developing regulatory environments.

Retrofit and renovation activity in aging commercial and public infrastructure generates a recurring demand channel independent of new construction cycles. According to YK manufacturer technical blog analysis from March 2026, implementing a QR-code-based digital tracking system for fire door assemblies yields a 25% reduction in reported field defects and a 15% acceleration in commissioning approval. This efficiency gain makes technology-enabled installation services more commercially attractive — opening a services revenue layer alongside product sales.

Emerging Trends

Material Science Advances and Digital Integration Redefine Fire Door Performance Standards

Steel and glass fire-rated doors are displacing traditional timber assemblies in modern commercial architectural designs that prioritize visibility, light transmission, and contemporary aesthetics without compromising fire resistance. This material shift reflects architects and developers specifying fire doors as design elements rather than purely functional safety components. Manufacturers that offer compliant glass and steel configurations gain access to higher-specification commercial projects with premium pricing.

Integration of fire doors with access control systems and automated closing mechanisms is becoming a standard specification requirement in hospitals, data centers, and government facilities. These buyers require fire doors to function as components of broader building safety and security ecosystems. According to an academic research paper published in the MDPI Fire journal in 2026, using a stainless steel frame instead of aluminum alloy achieves a 25% reduction in maximum frame temperature — a performance improvement that supports the push toward more precisely engineered fire door specifications in high-criticality environments.

Development of environment-friendly and sustainable fire-resistant door materials is shaping product roadmaps as construction sector sustainability mandates tighten. Building certification frameworks such as LEED and BREEAM now evaluate material sourcing and lifecycle impact alongside functional performance. Manufacturers that develop fire-rated assemblies using low-carbon materials or recycled content position themselves to capture demand from environmentally focused developers and public sector procurement programs.

Regional Analysis

Asia Pacific Dominates the Fire Door Market with a Market Share of 38.8%, Valued at USD 10.3 Billion

Asia Pacific leads the global fire door market with a 38.8% share, valued at USD 10.3 Billion in 2025. China, India, Japan, and South Korea are executing large-scale urban construction programs that mandate certified passive fire protection systems. Rapid high-rise development, expanding metro networks, and government-enforced building codes create consistent procurement volume across the region’s largest economies.

North America Fire Door Market Trends

North America holds a strong position in the global fire door market, underpinned by mature enforcement of NFPA 80 and IBC requirements across commercial, industrial, and residential construction. The United States generates the majority of regional demand, driven by ongoing commercial retrofits, healthcare facility upgrades, and data center construction. In December 2025, Investcorp completed its acquisition of Guardian Fire Services, a leading U.S. fire and life safety provider — signaling continued private equity confidence in North American fire protection infrastructure.

Europe Fire Door Market Trends

Europe maintains a substantial share of the global fire door market, supported by EN 1634 certification requirements and post-incident regulatory tightening following high-profile building fires in the UK and across continental Europe. Germany, France, and the UK represent the region’s largest individual markets. Retrofit demand in aging building stock and tightening social housing fire safety mandates are sustaining volume across the region independent of new construction cycles.

Middle East and Africa Fire Door Market Trends

The Middle East and Africa region is expanding its fire safety infrastructure as Gulf Cooperation Council nations accelerate commercial and hospitality construction under their respective national development programs. Saudi Arabia and the UAE represent the primary demand centers, where building codes are converging toward international fire safety standards. Africa’s contribution remains limited but is building as urban construction activity intensifies in South Africa and Nigeria.

Latin America Fire Door Market Trends

Latin America represents an earlier-stage market where fire door adoption is advancing alongside regulatory modernization in Brazil and Mexico — the region’s two largest economies. Commercial construction growth in São Paulo, Mexico City, and other major urban centers creates forward demand for certified fire door systems. Regional adoption will accelerate as local building code enforcement strengthens and awareness of passive fire protection requirements expands among contractors and building owners.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Ahmarra Door Solutions positions itself as a specialist in high-performance timber and composite fire door manufacturing for commercial and public sector clients. Their strategy centers on bespoke product engineering and certified performance, targeting specification-led procurement channels where technical compliance is the primary selection criterion. This approach insulates them from price-driven competition in commodity fire door segments and supports stronger margin retention.

Sentry Doors builds its competitive position around certified fire door supply for residential and commercial markets in the UK, operating in a regulatory environment where post-Grenfell enforcement has materially raised compliance standards. Their focus on fully certified assemblies — including frame, hardware, and intumescent components — addresses the market’s increasing scrutiny of complete door assembly performance rather than leaf-only specification. This whole-assembly positioning reduces client compliance risk and strengthens their value proposition.

Vicaima competes through a broad portfolio of timber fire doors that spans commercial, hospitality, and residential applications across European and international markets. Their manufacturing scale and product range breadth enable them to serve both specification architects and volume commercial contractors — two buyer segments with distinct but complementary procurement requirements. This dual-channel strategy supports revenue stability across construction cycle fluctuations.

Dortek differentiates through specialty fire door manufacturing for hygienic and controlled environments, including pharmaceutical facilities, cleanrooms, food processing plants, and healthcare buildings. Their product engineering targets applications where standard fire door materials and constructions are unsuitable due to sanitation, chemical resistance, or impact durability requirements. This niche focus commands premium pricing and generates long-term replacement relationships with institutional end users.

Key Players

- Ahmarra Door Solutions

- Sentry Doors

- Vicaima

- Dortek

- ASSA ABLOY

- Jeld-Wen

- Masonite International

- Halspan

- Noberne Doors

- EBL Fire Doors

- Pacific Doors

- Vista Panels

- Zhejiang Xinxing Doors

- Republic Doors & Frames

- Metaflex

- Other Key Players

Recent Developments

- December 2025 — Investcorp completed its acquisition of Guardian Fire Services, a leading U.S. provider of fire and life safety services, from Northern Lakes Capital. This major private equity transaction in the North American fire and life safety sector signals continued institutional confidence in the structural long-term demand for certified fire protection services.

- September 2024 — Tufwud unveiled the FD120 ID at the Fire & Security India Expo 2024 in Mumbai — India’s first ISI-certified fully insulated fire door. This product launch marks a significant milestone for the Indian fire door market, establishing a domestic benchmark for fully insulated, ISI-certified fire door manufacturing.

Report Scope

Report Features Description Market Value (2025) USD 26.6 Billion Forecast Revenue (2035) USD 38.9 Billion CAGR (2026-2035) 3.9% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Material Type (Steel, Timber/Wood, Glass, Aluminum, Composite, Others), By Mechanism (Swinging, Sliding, Rolling, Folding), By Fire Rating (30 Minutes, 60 Minutes, 90 Minutes, 120 Minutes, 180 Minutes), By End User (Commercial, Residential, Industrial) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Ahmarra Door Solutions, Sentry Doors, Vicaima, Dortek, ASSA ABLOY, Jeld-Wen, Masonite International, Halspan, Noberne Doors, EBL Fire Doors, Pacific Doors, Vista Panels, Zhejiang Xinxing Doors, Republic Doors & Frames, Metaflex, Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Ahmarra Door Solutions

- Sentry Doors

- Vicaima

- Dortek

- ASSA ABLOY

- Jeld-Wen

- Masonite International

- Halspan

- Noberne Doors

- EBL Fire Doors

- Pacific Doors

- Vista Panels

- Zhejiang Xinxing Doors

- Republic Doors & Frames

- Metaflex

- Other Key Players

Our Clients

- 181169

- Mar 2026