Global Fiber Cement Market Size, Share, Growth Analysis By Product Type (Fiber Cement Siding, Fiber Cement Boards, Fiber Cement Roofing, Others), By Fiber Type (Cellulosic Fiber, Synthetic Fiber, Others), By Application (Exterior,[Cladding, Façades, Roofing], Interior [Partition Walls, Ceilings, Flooring], Infrastructure), By End User (Residential, Commercial, Industrial, Infrastructure & Utilities), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 176298

- Number of Pages: 275

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

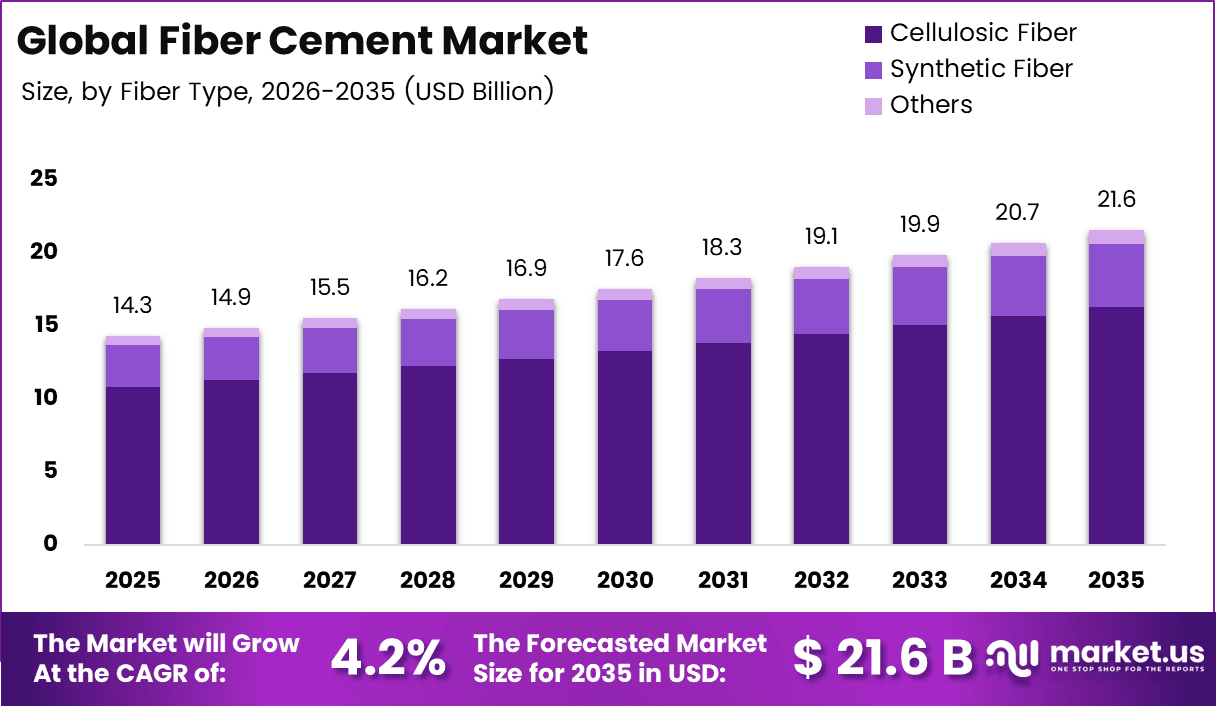

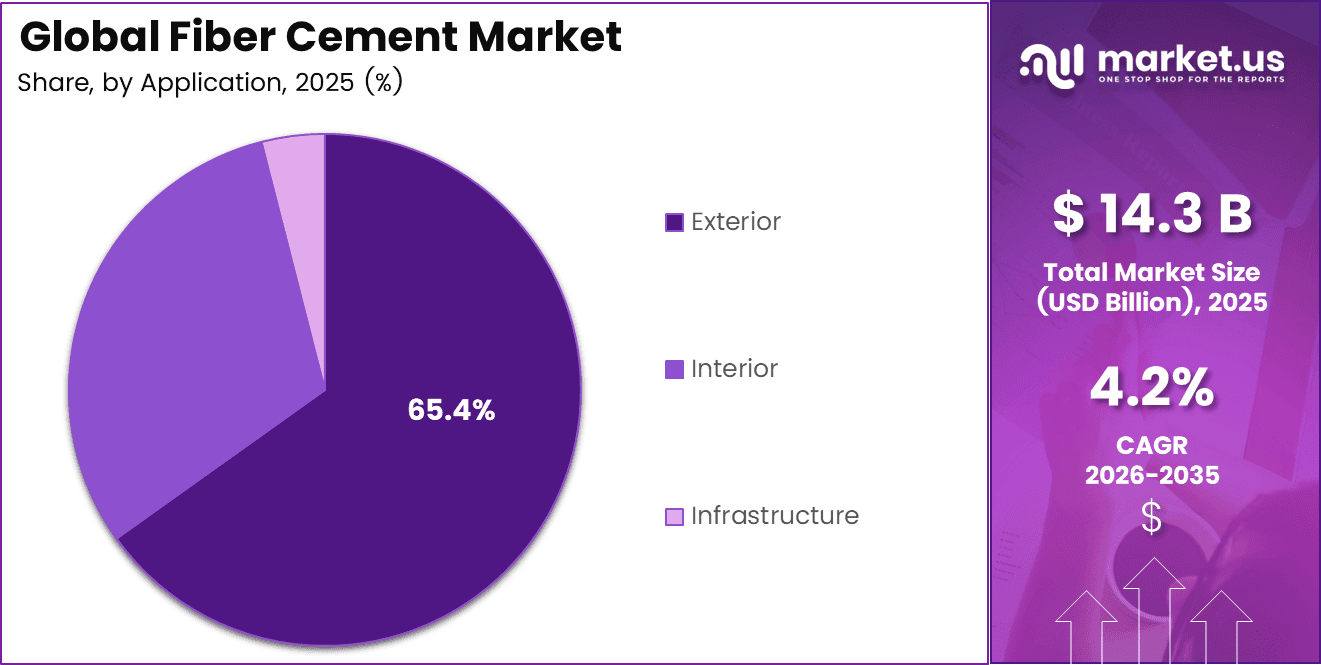

Global Fiber Cement Market size is expected to be worth around USD 21.6 Billion by 2035 from USD 14.3 Billion in 2025, growing at a CAGR of 4.2% during the forecast period 2026 to 2035.

Fiber cement represents a composite building material manufactured from cement reinforced with cellulose or synthetic fibers. This versatile construction solution combines durability, fire resistance, and aesthetic flexibility. Moreover, it serves multiple applications including exterior cladding, roofing, and interior partitions across residential and commercial sectors.

The market experiences steady growth driven by increasing urbanization and infrastructure development worldwide. Additionally, fiber cement products offer superior performance against moisture damage, termite infestation, and harsh weather conditions. Consequently, builders and architects increasingly specify these materials for both new construction and renovation projects.Government initiatives promoting sustainable construction practices further accelerate market expansion. Therefore, manufacturers continue investing in advanced formulations that enhance product performance while reducing environmental impact. However, the industry also addresses installation safety protocols and cost competitiveness challenges.

Fire safety regulations and building code requirements significantly influence fiber cement adoption across regions. Furthermore, the material’s non-combustible properties make it increasingly mandatory in high-risk areas. Additionally, low maintenance requirements appeal to cost-conscious developers and homeowners seeking long-term value.

According to Zmartbuild, construction with fiber cement boards is 4 times faster and saves up to 40% of labor cost. This efficiency advantage drives commercial project adoption rates. Moreover, time savings translate into reduced overall project costs and faster occupancy timelines for developers.

According to Emedec, fiber cement board ceiling thickness ranges from 4.0 to 6.0 mm, while flooring applications require 16 or 18 mm thickness. These specifications ensure structural integrity across various applications. Consequently, engineers can optimize designs based on specific load-bearing and performance requirements for different building components.

Key Takeaways

- Global Fiber Cement Market valued at USD 14.3 Billion in 2025, projected to reach USD 21.6 Billion by 2035 at 4.2% CAGR

- Asia Pacific dominates with 43.3% market share, valued at USD 6.19 Billion

- Fiber Cement Siding leads Product Type segment with 40.5% market share

- Cellulosic Fiber dominates Fiber Type segment holding 75.7% share

- Exterior applications account for 65.4% of total market demand

- Residential end-user segment captures 55.4% market share

- Fire resistance and low maintenance drive market adoption globally

- Construction with fiber cement boards is 4 times faster, saving 40% labor costs

Product Type Analysis

Fiber Cement Siding dominates with 40.5% due to superior weather resistance and aesthetic versatility in exterior applications.

In 2025, ‘Fiber Cement Siding’ held a dominant market position in the ‘By Product Type’ segment of Fiber Cement Market, with a 40.5% share. This segment leads due to exceptional durability, fire resistance, and design flexibility for residential and commercial exteriors. Moreover, manufacturers offer various textures and finishes that replicate wood, stone, and stucco aesthetics.

Fiber Cement Boards serve diverse construction applications including interior partitions, exterior sheathing, and underlayment systems. These products provide excellent dimensional stability and moisture resistance. Additionally, their versatility supports both traditional and modern architectural designs across multiple building types and climatic conditions.

Fiber Cement Roofing gains traction in industrial and commercial projects requiring non-combustible, weather-resistant overhead protection. These products withstand extreme temperatures and heavy precipitation. Furthermore, their longevity reduces lifecycle replacement costs compared to traditional roofing materials, appealing to infrastructure developers.

Others category encompasses specialized fiber cement products including trim boards, soffits, fascia, and decorative architectural elements. These components complete building envelope systems. Consequently, manufacturers develop innovative profiles addressing specific construction detailing requirements and enhancing overall aesthetic integration.

Fiber Type Analysis

Cellulosic Fiber dominates with 75.7% due to superior bonding characteristics and cost-effectiveness in fiber cement manufacturing.

In 2025, ‘Cellulosic Fiber’ held a dominant market position in the ‘By Fiber Type’ segment of Fiber Cement Market, with a 75.7% share. These natural fibers enhance matrix cohesion and improve tensile strength properties. Moreover, cellulosic reinforcement supports sustainable manufacturing practices by utilizing renewable resource materials in production processes.

Synthetic Fiber alternatives include polyvinyl alcohol and polypropylene fibers offering enhanced chemical resistance and dimensional stability. These materials perform exceptionally in harsh environmental conditions. Additionally, synthetic fibers enable manufacturers to develop specialized products with tailored performance characteristics for demanding applications.

Others fiber category encompasses emerging reinforcement technologies including glass fibers, carbon fibers, and hybrid fiber systems. These innovations target premium performance requirements. Furthermore, research continues exploring novel fiber combinations that optimize strength-to-weight ratios while maintaining cost competitiveness in commercial markets.

Application Analysis

Exterior applications dominate with 65.4% due to fiber cement’s exceptional weather resistance and architectural versatility in building envelopes.

In 2025, ‘Exterior’ held a dominant market position in the ‘By Application’ segment of Fiber Cement Market, with a 65.4% share. Cladding applications leverage fiber cement’s durability against moisture, UV radiation, and temperature fluctuations. Moreover, these systems provide continuous thermal protection and enhance building energy efficiency across residential and commercial projects.

Façades utilize fiber cement panels for architectural expression combining aesthetic appeal with functional performance. These systems accommodate various design styles from contemporary minimalism to traditional ornamentation. Additionally, ventilated façade configurations optimize moisture management and thermal insulation performance.

Roofing applications benefit from fiber cement’s fire resistance and structural strength under environmental stress. These products withstand heavy snow loads, wind uplift, and hail impact. Furthermore, their low maintenance requirements reduce long-term ownership costs for commercial and industrial facility managers.

Interior applications include Partition Walls offering fire-rated assemblies for commercial buildings, Ceilings providing acoustic control and moisture resistance, and Flooring substrates supporting tile and other finish materials. These products enhance interior environmental quality.

Infrastructure applications encompass tunnels, bridges, and utility installations requiring non-combustible, durable materials. These projects demand exceptional longevity and minimal maintenance. Consequently, fiber cement solutions address critical infrastructure resilience requirements across transportation and utility sectors.

End User Analysis

Residential dominates with 55.4% due to increasing housing construction and renovation activities globally.

In 2025, ‘Residential’ held a dominant market position in the ‘By End User’ segment of Fiber Cement Market, with a 55.4% share. Single-family homes and multi-family developments increasingly specify fiber cement for exterior cladding and roofing applications. Moreover, homeowners value the material’s durability, low maintenance, and aesthetic versatility for long-term property value enhancement.

Commercial end users include office buildings, retail centers, and hospitality facilities requiring durable, fire-resistant building materials. These projects prioritize lifecycle cost optimization and regulatory compliance. Additionally, fiber cement products support LEED certification and sustainable building initiatives increasingly mandated in commercial development projects.

Industrial facilities utilize fiber cement for warehouses, manufacturing plants, and logistics centers demanding robust, non-combustible construction materials. These applications withstand harsh operational environments and chemical exposure. Furthermore, rapid installation capabilities minimize construction downtime and accelerate facility commissioning timelines.

Infrastructure & Utilities sector encompasses transportation facilities, power plants, and water treatment facilities requiring exceptional durability and fire resistance. These critical installations mandate materials meeting stringent safety and longevity standards. Consequently, fiber cement solutions address demanding performance specifications across essential public infrastructure projects.

Key Market Segments

By Product Type

- Fiber Cement Siding

- Fiber Cement Boards

- Fiber Cement Roofing

- Others

By Fiber Type

- Cellulosic Fiber

- Synthetic Fiber

- Others

By Application

- Exterior

- Cladding

- Façades

- Roofing

- Interior

- Partition Walls

- Ceilings

- Flooring

- Infrastructure

By End User

- Residential

- Commercial

- Industrial

- Infrastructure & Utilities

Drivers

Rising Adoption of Fire-Resistant Building Materials Drives Market Growth

Building codes increasingly mandate non-combustible materials in residential and commercial construction projects. Fiber cement products provide Class A fire ratings, meeting stringent safety requirements. Moreover, insurance companies offer premium reductions for properties utilizing fire-resistant exterior materials, incentivizing adoption among developers and homeowners.

Rapid urbanization and infrastructure development in emerging economies create substantial demand for durable construction materials. Additionally, fiber cement withstands moisture damage, termite infestation, and extreme weather conditions better than traditional alternatives. These performance advantages reduce long-term maintenance costs and extend building lifecycle significantly.

Low-maintenance exterior cladding solutions appeal to property owners seeking reduced upkeep expenses and sustained aesthetic appeal. Furthermore, fiber cement resists rotting, warping, and degradation from environmental exposure. Consequently, developers increasingly specify these materials for projects requiring minimal maintenance interventions over extended service periods.

Restraints

High Initial Installation Costs Limit Market Adoption

Fiber cement materials command premium pricing compared to vinyl siding, wood, and traditional stucco alternatives. This cost differential discourages budget-conscious developers and homeowners. Moreover, specialized installation expertise requirements increase labor expenses, further elevating overall project costs and limiting market penetration in price-sensitive segments.

Installation processes require skilled contractors familiar with proper cutting, fastening, and finishing techniques specific to fiber cement products. Additionally, improper installation compromises performance and warranty coverage. Therefore, contractor training and certification programs remain essential but create market entry barriers in regions lacking established installer networks.

Health and safety concerns related to silica dust exposure during cutting operations require protective equipment and ventilation systems. Furthermore, regulatory compliance mandates add complexity to installation workflows. Consequently, these occupational health requirements increase labor costs and necessitate enhanced safety protocols compared to alternative cladding materials.

Growth Factors

Sustainable Construction Initiatives Accelerate Market Expansion

Green building certification programs increasingly recognize fiber cement products for sustainable material content and durability performance. These materials contribute to LEED points and other environmental rating systems. Moreover, manufacturers develop low-carbon formulations utilizing recycled content and optimized production processes, enhancing environmental credentials.

Residential renovation and remodeling activities generate substantial demand for fiber cement cladding and roofing replacement products. Additionally, aging housing stock requires exterior upgrades addressing weather damage and aesthetic modernization. Therefore, retrofit applications represent significant growth opportunities across established housing markets in developed economies.

Affordable housing initiatives and smart city development programs specify cost-effective, durable building materials meeting quality and longevity standards. Furthermore, fiber cement products align with government infrastructure investment priorities in emerging markets. Consequently, public sector construction projects increasingly adopt these materials for large-scale residential and commercial developments.

Emerging Trends

Technological Advancements Transform Product Performance and Manufacturing Efficiency

Manufacturers develop lightweight, high-strength fiber cement formulations optimizing material-to-performance ratios for structural and transportation efficiency. These innovations reduce installation labor and support larger panel dimensions. Moreover, advanced fiber reinforcement technologies enhance impact resistance and dimensional stability across diverse environmental conditions.

Aesthetic diversification drives demand for fiber cement boards replicating authentic wood grain, natural stone, and contemporary concrete finishes. Additionally, digital printing and texturing technologies enable customized designs matching architectural specifications. Therefore, product lines expand addressing diverse aesthetic preferences across residential and commercial market segments.

Digital manufacturing and prefabrication techniques streamline production workflows and enhance quality control consistency. Furthermore, modular and off-site construction methodologies increasingly incorporate fiber cement components for accelerated project delivery. Consequently, manufacturers invest in automation technologies supporting mass customization and rapid fulfillment capabilities.

Regional Analysis

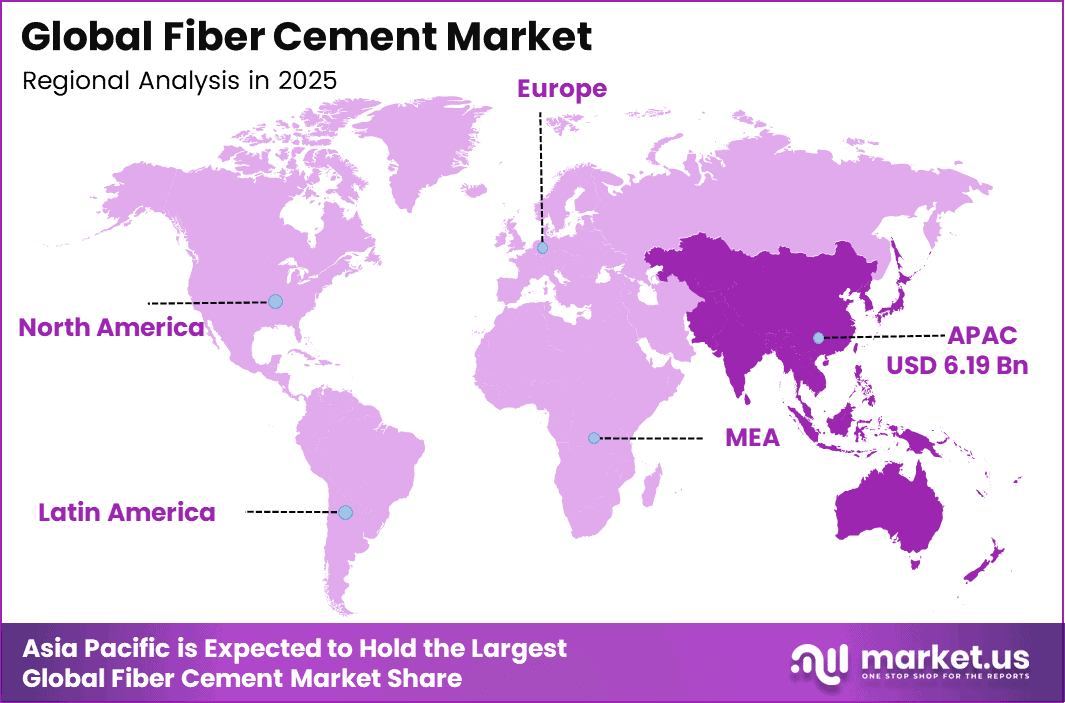

Asia Pacific Dominates the Fiber Cement Market with a Market Share of 43.3%, Valued at USD 6.19 Billion

Asia Pacific leads global fiber cement consumption driven by extensive urbanization, infrastructure development, and growing construction activities across China, India, and Southeast Asian nations. The region’s 43.3% market share reflects rapid economic growth and increasing adoption of modern building materials. Moreover, government initiatives promoting affordable housing and smart city projects significantly boost regional demand, with market value reaching USD 6.19 Billion in 2025.

North America Fiber Cement Market Trends

North America demonstrates strong market presence supported by stringent fire safety regulations and replacement demand in residential renovation sectors. Additionally, hurricane-prone coastal regions increasingly specify fiber cement for superior weather resistance. Therefore, building codes and insurance requirements drive consistent market growth across United States and Canadian construction industries.

Europe Fiber Cement Market Trends

European markets prioritize sustainable construction materials aligned with environmental regulations and energy efficiency directives. Furthermore, heritage building restoration projects utilize fiber cement for aesthetic compatibility with traditional architecture. Consequently, Western European nations lead regional adoption while Eastern European markets show accelerating growth trajectories.

Latin America Fiber Cement Market Trends

Latin American construction sectors adopt fiber cement solutions for tropical climate durability and termite resistance properties. Moreover, expanding middle-class housing demand drives residential market growth across Brazil and Mexico. Additionally, infrastructure modernization initiatives create opportunities for commercial and industrial applications throughout the region.

Middle East & Africa Fiber Cement Market Trends

Middle East and Africa regions leverage fiber cement for extreme temperature resistance and non-combustible properties in desert climates. Furthermore, large-scale infrastructure projects and urban development initiatives drive market expansion. Consequently, GCC nations lead regional demand supported by government construction investments and diversification strategies.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

James Hardie Industries maintains global market leadership through extensive product portfolios and strong brand recognition across residential and commercial sectors. The company invests significantly in research and development, advancing fiber cement technology and manufacturing efficiency. Moreover, strategic distribution partnerships expand market reach while maintaining quality standards and customer service excellence across diverse geographic markets.

Etex Group strengthens its market position through strategic acquisitions including BGC’s plasterboard and fiber cement businesses in Australia and New Zealand. This expansion enhances regional capabilities and product offerings. Additionally, the company emphasizes sustainable building solutions aligned with environmental regulations and green construction trends across European and international markets.

Nichiha Corporation leads Asian markets with advanced fiber cement manufacturing technologies and diverse architectural product lines. The company focuses on aesthetic innovation, offering premium façade solutions replicating natural materials. Furthermore, Nichiha’s quality standards and technical support services establish strong contractor and architect relationships throughout Japan and expanding international territories.

Swisspearl Group specializes in high-performance fiber cement façade systems targeting premium commercial and residential projects globally. The company differentiates through superior design capabilities and customization services. Moreover, Swisspearl’s architectural expertise and technical consultation support complex building envelope solutions across European and North American markets.

Key players

- James Hardie Industries

- Etex Group

- Nichiha Corporation

- Swisspearl Group

- Toray Industries

- Mahaphant Fibre-Cement

- Elementia Materials

- American Fiber Cement Corporation

- TPI Polene Public Company Ltd.

- Saint-Gobain

- Everest Industries Ltd.

- SCG Building Materials

- Allura USA

- Plycem USA

- Ramco Industries Ltd.

- Other Key Players

Recent Developments

- January 2024 – Etex Group completed acquisition of BGC’s plasterboard and fiber cement businesses in Australia and New Zealand, expanding sustainable construction activities in attractive markets with significant growth opportunities and strengthening regional market presence.

- Oct 2025, James Hardie Industries and Boise Cascade Company announced expanded distribution partnership, enhancing product availability and market reach across North American construction markets through improved supply chain integration and distribution network optimization.

Report Scope

Report Features Description Market Value (2025) USD 14.3 Billion Forecast Revenue (2035) USD 21.6 Billion CAGR (2026-2035) 4.2% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Fiber Cement Siding, Fiber Cement Boards, Fiber Cement Roofing, Others), By Fiber Type (Cellulosic Fiber, Synthetic Fiber, Others), By Application (Exterior, Cladding, Façades, Roofing, Interior, Partition Walls, Ceilings, Flooring, Infrastructure), By End User (Residential, Commercial, Industrial, Infrastructure & Utilities) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape James Hardie Industries, Etex Group, Nichiha Corporation, Swisspearl Group, Toray Industries, Mahaphant Fibre-Cement, Elementia Materials, American Fiber Cement Corporation, TPI Polene Public Company Ltd., Saint-Gobain, Everest Industries Ltd., SCG Building Materials, Allura USA, Plycem USA, Ramco Industries Ltd., Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- James Hardie Industries

- Etex Group

- Nichiha Corporation

- Swisspearl Group

- Toray Industries

- Mahaphant Fibre-Cement

- Elementia Materials

- American Fiber Cement Corporation

- TPI Polene Public Company Ltd.

- Saint-Gobain

- Everest Industries Ltd.

- SCG Building Materials

- Allura USA

- Plycem USA

- Ramco Industries Ltd.

- Other Key Players

Our Clients

- 176298

- Feb 2026