Global Eye Mask Market Size, Share, Growth Analysis By Product (Regular, Contoured, Wrap Around, Others), By Material (Cotton, Silk, Memory Foam, Others), By Distribution Channel (Hypermarket/Supermarket, Convenience Stores, E-commerce/Online, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 181610

- Number of Pages: 205

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

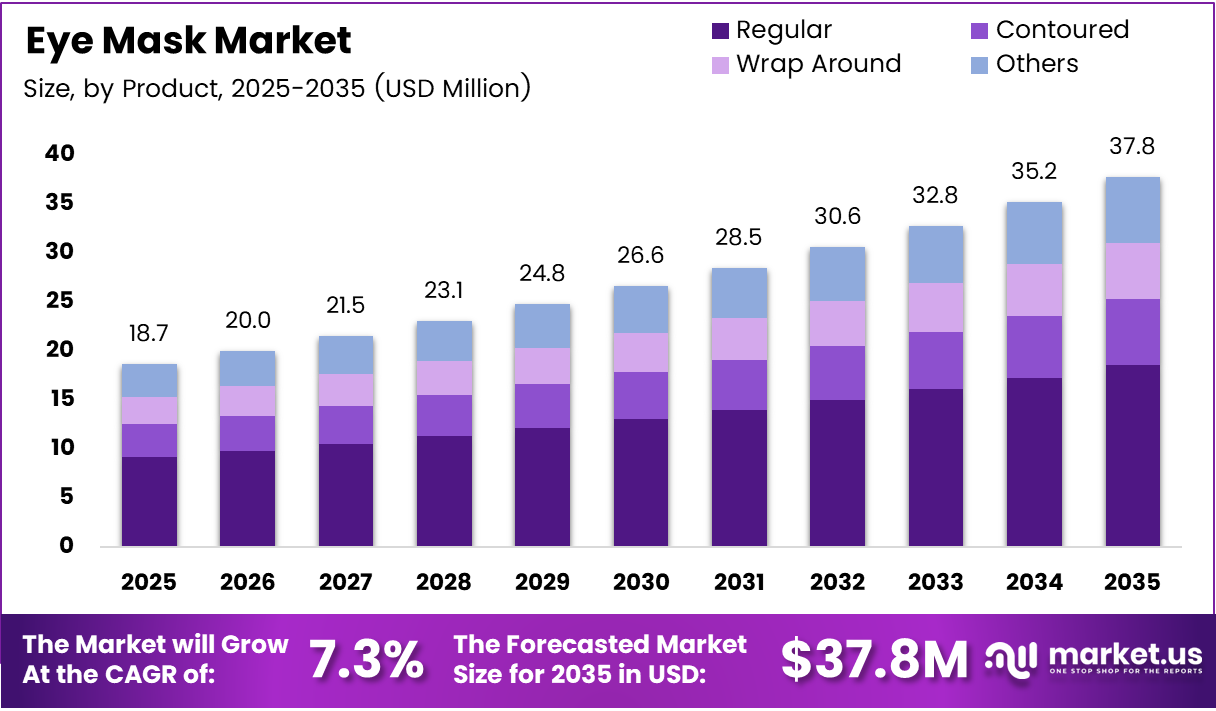

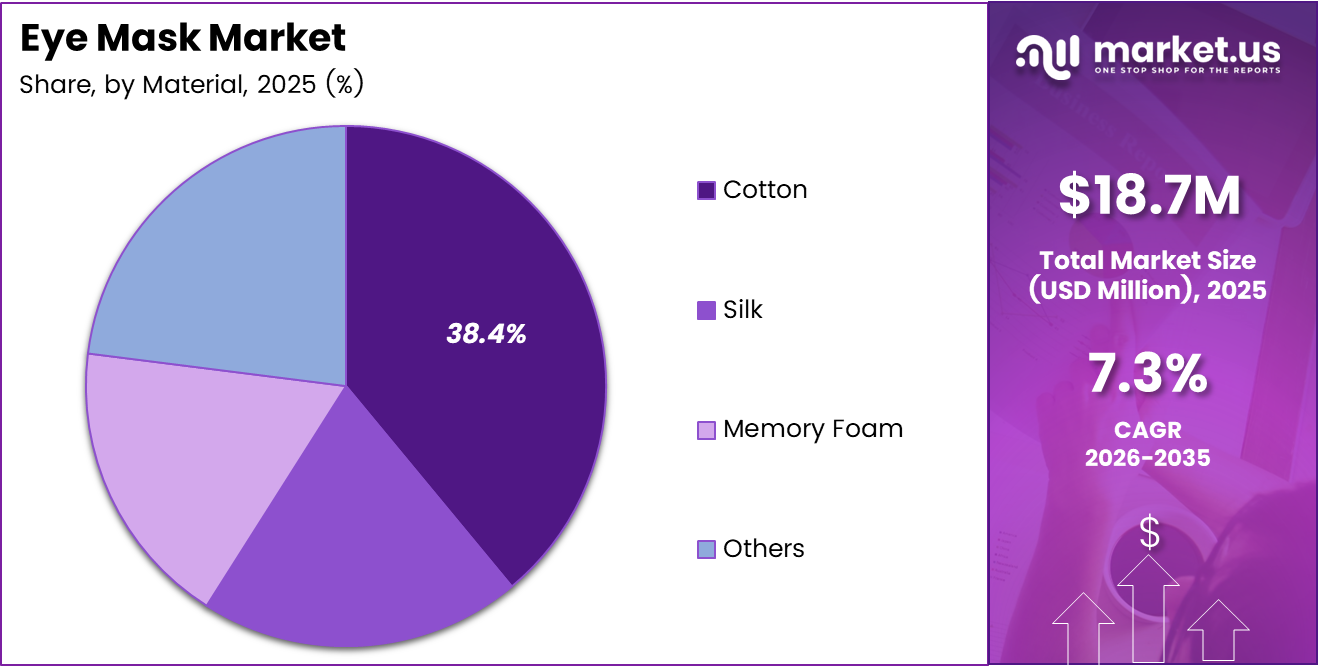

The Global Eye Mask Market size is expected to be worth around USD 37.8 Million by 2035 from USD 18.7 Million in 2025, growing at a CAGR of 7.3% during the forecast period 2026 to 2035.

The eye mask market covers products designed to block light, deliver skincare benefits, or provide therapeutic relief during sleep and rest. Formats include cotton sleep masks, silk covers, memory foam contoured designs, and emerging smart or LED-based wearables. Buyers range from everyday sleep-aid consumers to wellness-focused shoppers seeking premium self-care tools.

Sleep health now sits at the center of consumer wellness spending. Clinicians and wellness brands alike promote light elimination as a core tool for improving sleep onset and quality. This behavioral shift translates directly into repeat purchases, because sleep masks are low-cost consumables that users replace regularly — a structure that rewards brands with strong distribution and consistent quality.

The travel accessories segment also reinforces demand. Airline travelers, frequent commuters, and hotel guests treat eye masks as essential carry-on items. Hospitality brands and airlines regularly source masks in bulk, creating a B2B revenue channel that sits alongside the direct-to-consumer retail stream.

Skincare-integrated eye masks — particularly hydrogel and cooling gel variants — are pulling in a second buyer profile: beauty-conscious consumers who use masks as part of morning and evening skincare routines. This crossover into beauty broadens the addressable market beyond pure sleep wellness.

In November 2025, XWELL and Ostrichpillow co-launched the Blue Breeze Eye Mask exclusively at airport retail locations, signaling that premium travel retail is becoming a targeted distribution strategy for eye mask brands aiming to capture high-income, mobility-driven consumers.

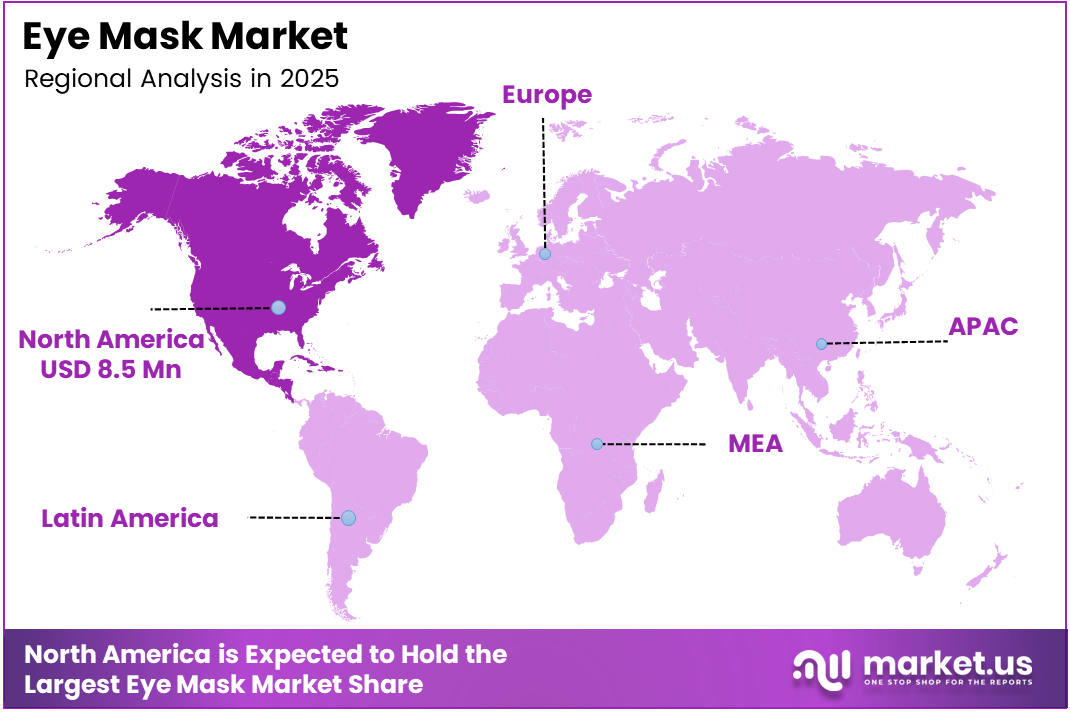

North America leads the global eye mask market, holding a 45.70% share valued at USD 8.5 Million. This reflects deep consumer familiarity with sleep health products, a mature direct-to-consumer e-commerce channel, and premium pricing power that supports higher average order values than most other regions.

The market’s doubling from USD 18.7 Million to USD 37.8 Million over ten years signals steady but structurally sound expansion. This pace rewards brands that invest in product differentiation — through materials innovation, smart features, or clinical positioning — rather than those competing purely on price.

Key Takeaways

- The Global Eye Mask Market was valued at USD 18.7 Million in 2025 and is projected to reach USD 37.8 Million by 2035.

- The market grows at a CAGR of 7.3% during the forecast period 2026 to 2035.

- By Product, Regular eye masks dominate with a 48.2% share in 2025.

- By Material, Cotton leads with a 38.4% share, driven by affordability and broad consumer preference.

- By Distribution Channel, Hypermarket/Supermarket holds the largest share at 39.6%.

- North America dominates the regional landscape with a 45.70% share, valued at USD 8.5 Million.

Product Analysis

Regular eye masks dominate with 48.2% due to low cost and universal consumer familiarity.

In 2025, Regular eye masks held a dominant market position in the By Product segment of the Eye Mask Market, with a 48.2% share. Their flat, lightweight design meets the core need — light blocking — at the lowest price point. This broad accessibility drives mass-market volume and makes regular masks the default first purchase for new users entering the category.

Contoured eye masks carry a meaningful structural advantage over flat designs. The raised interior cup prevents fabric contact with eyelids, making them the preferred option for users who wear lash extensions or apply overnight eye creams. Contoured masks command higher retail prices, giving brands a clear margin improvement opportunity within the same distribution footprint.

Wrap Around eye masks serve users who require full peripheral light elimination — a segment that includes side sleepers and shift workers with irregular schedules. Their design wraps around the head with wider coverage than standard formats. However, the bulkier profile limits travel convenience, which constrains volume in the portable accessories channel.

Others in the product category include gel-filled, heated, and LED-integrated masks. These formats target therapeutic and premium wellness buyers rather than everyday sleep aid consumers. Their higher price points and specific use cases mean they represent a smaller share today, but innovation activity in this tier is the highest across the entire product portfolio.

Material Analysis

Cotton dominates with 38.4% due to breathability, washability, and cost accessibility.

In 2025, Cotton held a dominant market position in the By Material segment of the Eye Mask Market, with a 38.4% share. Cotton’s washable, hypoallergenic properties align with hygiene-conscious buyers who prioritize reusability. Its cost advantage over silk and foam keeps it accessible across mass-market retail and value-oriented e-commerce channels, making it the default material for mainstream sleep mask formats.

Silk occupies the premium tier of the material segment, appealing to consumers who cite reduced friction as a benefit for both skin and hair. The beauty crossover narrative — silk masks marketed alongside skincare routines — has expanded the buyer base beyond pure sleep wellness into personal care. Silk commands higher average selling prices and supports stronger brand margins when positioned in specialty and beauty retail channels.

Memory Foam differentiates through structure rather than surface feel. The foam conforms to individual facial contours, reducing pressure points and creating a more customized fit. This property makes it particularly relevant for users who experience discomfort with flat or contoured fabric masks. Memory foam masks also carry naturally higher price anchors, supporting premium positioning without requiring additional material inputs like infusions or coatings.

Others in the material segment include gel, charcoal-infused fabric, and silk-cotton blends. These hybrids target specific functional claims — cooling, detoxifying, or softness-optimized — that allow brands to differentiate without restructuring their full product line. As the skincare-integrated eye mask category grows, blended and functional materials are likely to capture a larger share of premium product launches.

Distribution Channel Analysis

Hypermarket/Supermarket dominates with 39.6% due to high foot traffic and broad product visibility.

In 2025, Hypermarket/Supermarket held a dominant market position in the By Distribution Channel segment of the Eye Mask Market, with a 39.6% share. Physical retail gives eye masks immediate visibility alongside complementary personal care products — a placement advantage that drives impulse purchases. Buyers who encounter sleep masks near pharmacy or beauty aisles convert at higher rates than those who actively search online.

Convenience Stores serve the impulse and travel-driven buyer who needs a mask for immediate use — on a flight, overnight trip, or during an unplanned stay. The smaller assortment typical of convenience formats means only the most recognizable, low-complexity products succeed here. This channel rewards brands with strong packaging recognition and compact, individually wrapped formats over those with complex product propositions.

E-commerce/Online channels remove geographic constraints and allow brands to present detailed product information — materials, clinical claims, user reviews — that physical shelf space cannot accommodate. This channel is particularly effective for premium, therapeutic, and smart eye mask formats that require buyer education to justify higher price points. Direct-to-consumer online sales also give brands first-party customer data, enabling repeat purchase targeting and subscription models.

Others in distribution include specialty wellness retailers, airport travel stores, hotel amenity programs, and beauty subscription boxes. These channels often carry curated selections at premium prices. The November 2025 XWELL and Ostrichpillow launch specifically at XpresSpa airport locations illustrates how specialty placement can create a high-income, captive audience that is underserved by mass retail formats.

Key Market Segments

By Product

- Regular

- Contoured

- Wrap Around

- Others

By Material

- Cotton

- Silk

- Memory Foam

- Others

By Distribution Channel

- Hypermarket/Supermarket

- Convenience Stores

- E-commerce/Online

- Others

Drivers

Sleep Disorder Prevalence and Wellness Routines Combine to Build Sustained Eye Mask Demand

Sleep disorders and chronic insomnia are pushing consumers toward affordable, non-pharmaceutical interventions. Eye masks address the core symptom — unwanted light exposure — without medication. This positions them as a credible first-response sleep aid for a large and growing population of light-sensitive sleepers who prefer accessible, reusable solutions over clinical alternatives.

The expansion of daily wellness and self-care routines has turned eye masks from occasional accessories into regular-use products. Consumers who build structured morning and evening rituals incorporate cooling, hydrating, or relaxation masks as active skincare steps. In September 2025, Ulike launched the ReGlow LED face mask targeting multiple skin concerns, illustrating how therapeutic positioning extends routine-based demand beyond sleep into dermatological self-care.

Travel remains a structural demand driver. Portable comfort products — particularly compact sleep masks — are standard inclusions in travel kits for frequent flyers and commuters. Airlines and hospitality operators source masks in bulk, creating stable B2B procurement volume that runs parallel to retail sales. This dual-channel demand structure reduces market exposure to any single consumer segment.

Restraints

Low-Cost Alternatives and Hygiene Concerns Limit Repeat Purchase Rates and Category Expansion

DIY alternatives — folded cloths, pillow covers, or repurposed fabric scraps — satisfy the basic light-blocking need without any purchase required. For price-sensitive buyers, the functional gap between a homemade solution and a basic retail eye mask is small enough to suppress conversion. This substitution ceiling keeps average selling prices constrained in the mass-market tier.

Hygiene concerns create a second friction point. Reusable masks accumulate skin oils, cosmetic residue, and allergens between washes. Consumers with sensitive skin or acne-prone skin face a real risk of irritation from infrequent cleaning. This perception issue raises the replacement threshold — some buyers abandon the category rather than invest in premium or dedicated cleaning routines.

Skin sensitivity concerns also limit trial among consumers who have had reactions to synthetic fabrics, elastic bands, or material coatings. Brands that do not clearly communicate material composition and testing credentials lose potential buyers at the point of consideration. The absence of standardized labeling for allergen-free or hypoallergenic claims makes it harder for buyers to self-screen products without prior experience.

Growth Factors

Smart Features, Sustainable Materials, and Therapeutic Positioning Open Higher-Value Market Tiers

Smart eye masks with integrated Bluetooth audio and sleep-tracking sensors represent the highest-value expansion opportunity in this market. These devices move the category from a commodity product to a health technology platform. Brands that establish early credibility in clinical sleep monitoring can command subscription revenue models alongside hardware sales — a structural shift that dramatically improves lifetime customer value.

Consumer preference for organic and eco-friendly materials is reshaping sourcing and product development priorities. Brands that certify organic cotton, sustainably harvested silk, or biodegradable packaging gain access to a premium buyer segment that actively filters for credentials before purchasing. This segment also demonstrates stronger brand loyalty, reducing customer acquisition costs over time compared to price-driven buyers.

Therapeutic positioning — specifically for dry eye treatment and digital eye strain relief — connects eye masks to the growing healthcare-adjacent wellness market. As screen time increases across all demographics, products with clinical or near-clinical claims attract healthcare professional endorsements. Expansion through e-commerce and direct-to-consumer channels gives brands a cost-effective path to reach these buyers without dependence on mass retail placement.

Emerging Trends

Aromatherapy, Social Media Influence, and Premium Materials Shift Eye Masks from Utility to Lifestyle

Gel-based cooling masks for migraine and stress relief represent a functional upgrade that justifies premium pricing without requiring electronics integration. These products sit at the intersection of pain management and relaxation, attracting buyers who would not ordinarily shop the sleep accessories aisle. The migraine relief use case specifically benefits from strong word-of-mouth advocacy among sufferers who find clinical relief.

Aromatherapy integration — particularly lavender-infused sleep masks — transforms a functional product into a multi-sensory ritual item. Social media and beauty content creators have normalized this positioning, driving trial among younger consumers who engage with sleep and wellness content online. In September 2025, Amorepacific unveiled the ONFACE micro-LED mask at IFA 2025, signaling that premium brands now treat eye mask launches as major consumer technology events.

Silk and satin masks benefit directly from beauty influencer culture, where the material’s anti-crease and hair-friction-reducing properties are documented in video content across platforms. This earned media reduces paid acquisition costs for brands that build influencer partnerships early. The crossover from sleep utility to beauty accessory is now a proven commercial pathway, not a speculative one.

Regional Analysis

North America Dominates the Eye Mask Market with a Market Share of 45.70%, Valued at USD 8.5 Million

North America commands a 45.70% share of the global eye mask market, valued at USD 8.5 Million. The region benefits from a mature sleep wellness culture, high per-capita wellness spending, and a robust direct-to-consumer e-commerce infrastructure. Premium product positioning succeeds here at price points that would underperform in most other regions.

Europe Eye Mask Market Trends

Europe holds a structurally significant position driven by strong consumer demand for certified organic and sustainable personal care products. Regulatory frameworks that govern material safety and labeling standards create a natural filter that rewards quality-positioned brands. The UK, Germany, and France represent the core premium markets where silk and therapeutic-grade masks find the strongest buyer receptivity.

Asia Pacific Eye Mask Market Trends

Asia Pacific presents the highest long-term volume potential, anchored by China, Japan, and South Korea’s well-established beauty and skincare culture. Japanese consumers in particular have historically driven domestic eye mask innovation — gel, steam, and aromatherapy formats originated in this market. Rising disposable incomes across Southeast Asia are expanding the addressable buyer base beyond the established Northeast Asian core.

Latin America Eye Mask Market Trends

Latin America represents an early-stage opportunity where affordable cotton and basic sleep masks serve the primary entry point. Brazil and Mexico lead regional consumption, supported by expanding modern retail formats and growing urban wellness awareness. The price-sensitive structure of both markets means volume growth will precede premiumization, making distribution scale the priority for brands entering this region.

Middle East and Africa Eye Mask Market Trends

The Middle East and Africa market develops along two distinct tracks. Gulf Cooperation Council countries show appetite for premium and luxury wellness accessories, consistent with broader regional spending on personal care. Sub-Saharan African markets remain nascent, with growth tied to urban retail expansion and rising middle-class household formation in countries like Nigeria, Kenya, and South Africa.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Nidra Sleep has built its market position around contoured deep-rest mask design, targeting the specific buyer who finds flat masks inadequate for total blackout. Their molded cup structure addresses a documented product gap that competitors with standard flat formats cannot fill. This functional differentiation allows Nidra to sustain premium retail pricing in a category where most products compete on price alone.

Chirag Group of Company operates with a supply-side advantage, leveraging manufacturing scale to serve both private-label clients and branded retail simultaneously. This dual-channel structure insulates the company from single-channel revenue concentration. Brands dependent on only retail or only private label face higher margin volatility — Chirag’s model distributes that risk while building production volume that reduces per-unit cost.

Loftie positions at the intersection of sleep technology and consumer wellness, targeting buyers who invest in structured sleep improvement rather than one-off comfort accessories. Their product ecosystem approach — pairing devices with sleep content and routines — raises switching costs above those of standalone mask brands. Buyers who integrate Loftie into a broader sleep ritual are significantly less likely to switch on price.

HEPTAGON HEALTHCARE PRIVATE LIMITED approaches the eye mask category from a healthcare and therapeutic angle, differentiating on clinical credibility rather than lifestyle appeal. This positioning targets a buyer — medical professionals, dry eye patients, post-surgical recovery users — who is underserved by mainstream wellness brands. Healthcare positioning also opens institutional procurement channels, including hospitals and optical chains, that lifestyle brands cannot easily access.

Key Players

- Nidra Sleep

- Chirag Group of Company

- Loftie

- HEPTAGON HEALTHCARE PRIVATE LIMITED

- EcoTools Beauty

- The Luxury Bed Collection

- Lumos Sleep

- Earth Therapeutics

- Wild Essentials LLC

- Sonoma Lavender

- Alaska Bear

Recent Developments

- July 2025 – Megrhythm released its latest Steamy Hot Eye Mask in collaboration with Pokémon Sleep, featuring themed packaging with characters including Pikachu and Snorlax. The co-branded release targeted younger, digitally engaged consumers to expand the eye mask category beyond traditional wellness buyers.

- August 2025 – Sisley launched the Neurae Harmonie Sleeping Mask, incorporating a botanical blend designed to restore skin elasticity. The product pairs wearable mask formats with topical skincare formulations, positioning sleep masks as active treatment tools within premium beauty regimens.

- November 2025 – SELEPU announced the DreamPilot, introduced as the first consumer AI-guided sleep mask featuring adaptive EEG technology for deeper and more stable sleep. The product launched via a Kickstarter campaign, signaling strong early market validation from a consumer funding model before retail distribution.

Report Scope

Report Features Description Market Value (2025) USD 18.7 Million Forecast Revenue (2035) USD 37.8 Million CAGR (2026-2035) 7.3% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product (Regular, Contoured, Wrap Around, Others), By Material (Cotton, Silk, Memory Foam, Others), By Distribution Channel (Hypermarket/Supermarket, Convenience Stores, E-commerce/Online, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Nidra Sleep, Chirag Group of Company, Loftie, HEPTAGON HEALTHCARE PRIVATE LIMITED, EcoTools Beauty, The Luxury Bed Collection, Lumos Sleep, Earth Therapeutics, Wild Essentials LLC, Sonoma Lavender, Alaska Bear Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Nidra Sleep

- Chirag Group of Company

- Loftie

- HEPTAGON HEALTHCARE PRIVATE LIMITED

- EcoTools Beauty

- The Luxury Bed Collection

- Lumos Sleep

- Earth Therapeutics

- Wild Essentials LLC

- Sonoma Lavender

- Alaska Bear

Our Clients

- 181610

- Mar 2026