Global Esters Market Size, Share, And Industry Analysis Report By Source (Synthetic, Natural), By Product (Methyl Esters, Dibasic Esters, Phosphate Esters, Acrylic Esters, Sucrose Esters, Fatty Acid Esters), By Application (Lubricants, Solvents, Plasticizers, Fuel and Oil Additives, Explosives, Surfactants, Flavoring Agents), By End-Use (Chemicals, Food, Automotive and Aviation, Marine, Textiles, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 179848

- Number of Pages: 299

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

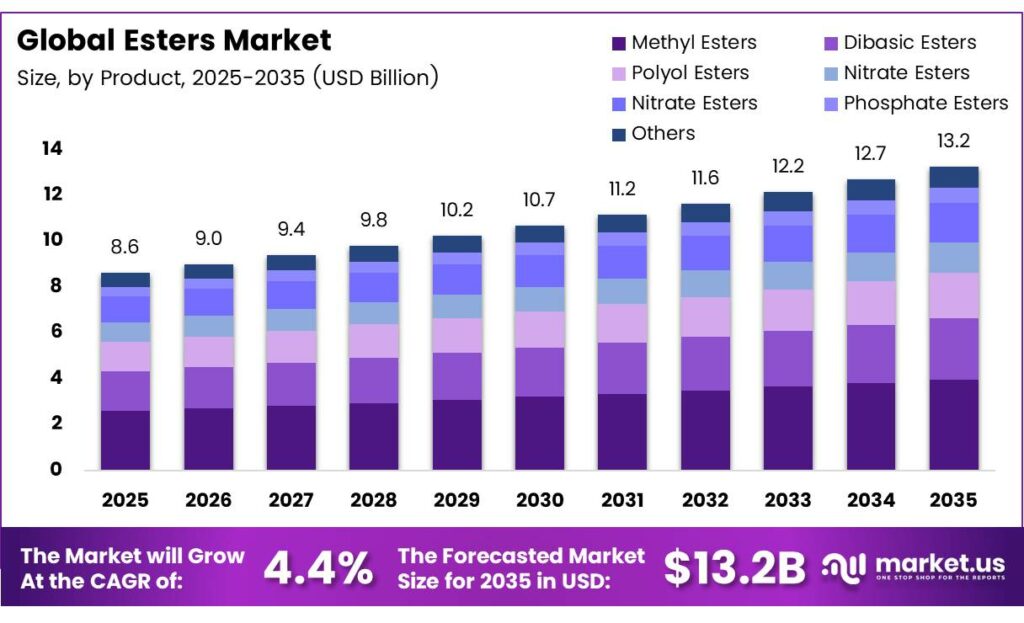

The Global Esters Market size is expected to be worth around USD 13.2 billion by 2035 from USD 8.6 billion in 2025, growing at a CAGR of 4.4% during the forecast period 2026 to 2035.

Esters are chemical compounds formed through a reaction between acids and alcohols. They serve critical roles across industries, including lubricants, plasticizers, solvents, fuel additives, and personal care products. Their versatile chemistry makes them indispensable across both industrial and consumer applications globally.

The esters market benefits from strong demand in automotive, aerospace, food processing, and chemical manufacturing. Manufacturers increasingly prefer synthetic and bio-based esters due to their superior performance characteristics. Moreover, rising environmental regulations push industries toward cleaner, biodegradable ester alternatives in multiple end-use sectors.

- Emery Oleochemicals recorded global revenue of USD 478.2 million in 2024 with 491 employees across manufacturing sites on three continents. This figure reflects the substantial commercial scale that fatty acid ester producers have achieved in a competitive global market.

- EU production of fatty acid methyl esters (FAME) reached approximately 9.8 million tonnes, far exceeding the 5.6 million tonnes of hydrotreated vegetable oil produced. This dominance confirms that FAME esters hold a leading volume position in Europe’s renewable energy pool, underscoring broad industrial reliance on ester chemistry.

Investment in ester production capacity continues to expand globally. Companies allocate significant capital toward sustainable manufacturing and enzymatic synthesis technologies. Additionally, growing consumer awareness around eco-friendly formulations encourages product innovation in natural and microplastic-free ester variants.

Key Takeaways

- The Global Esters Market is valued at USD 8.6 billion in 2025 and is projected to reach USD 13.2 billion by 2035, at a CAGR of 4.4% during the forecast period from 2026 to 2035.

- Synthetic esters dominate with a market share of 72.4% in 2025.

- Methyl Esters hold the leading position with a 21.6% share.

- Lubricants represent the largest application segment at 24.8%.

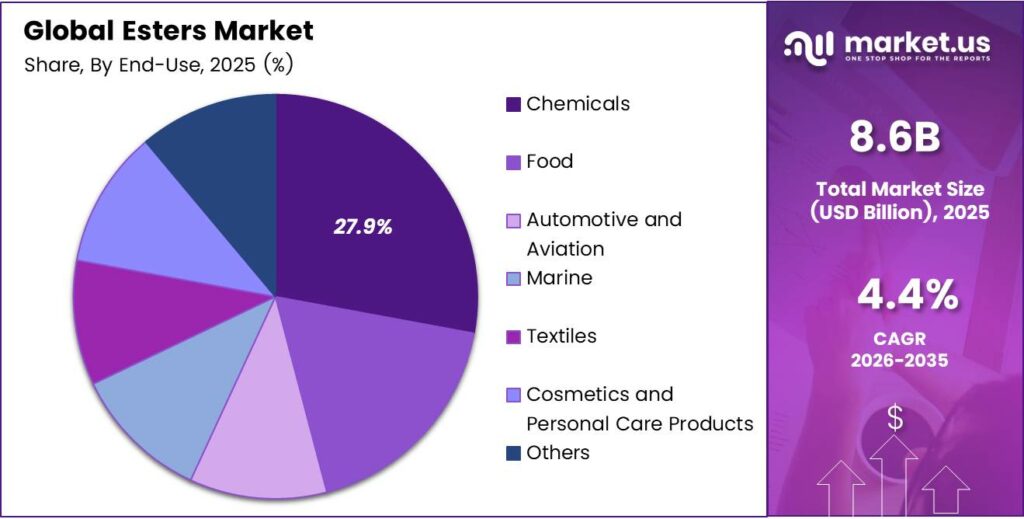

- The Chemicals sector leads with a 27.9% share of total market demand.

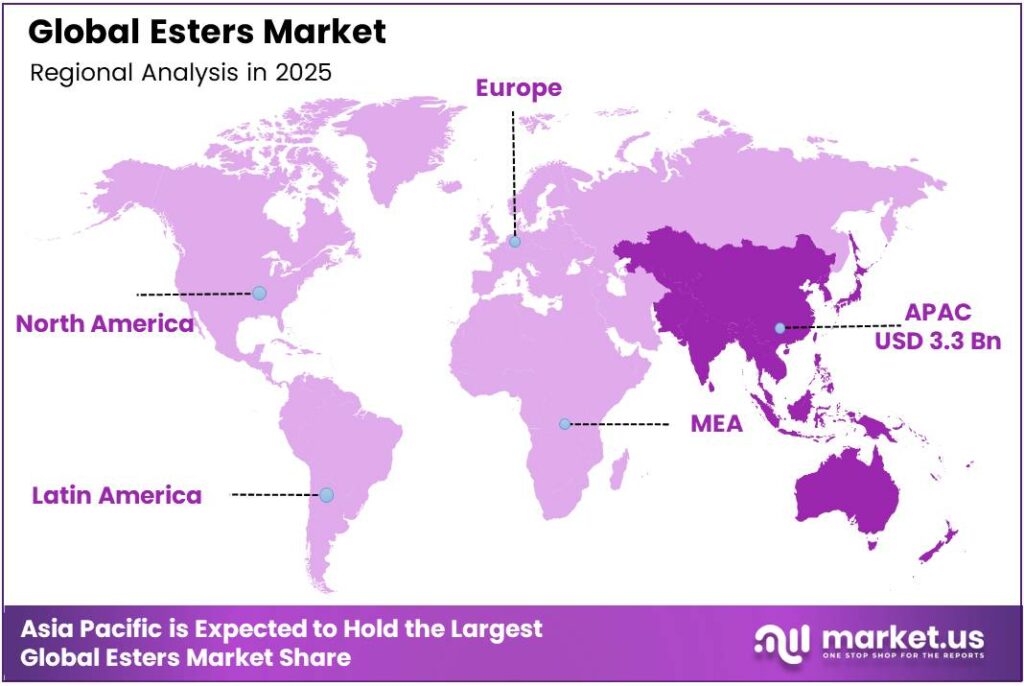

- Asia Pacific dominates the regional landscape with a 38.5% share, valued at USD 3.3 billion in 2025.

By Source Analysis

Synthetic dominates with 72.4% due to superior performance and wide industrial applicability.

In 2025, Synthetic esters held a dominant market position in the By Source segment of the Esters Market, with a 72.4% share. Synthetic esters deliver superior thermal stability, oxidation resistance, and lubricity compared to natural alternatives. Moreover, they meet strict performance requirements across automotive, aerospace, and industrial applications, making them the preferred choice for high-demand end-use sectors globally.

Natural esters occupy a smaller but growing share of the source segment. Derived from vegetable oils and animal fats, natural esters attract demand due to their biodegradability and renewable origin. However, their limited thermal range and higher cost restrain broader adoption. Consequently, natural esters find greatest use in food-grade, cosmetic, and environmentally sensitive industrial applications.

By Product Analysis

Methyl Esters dominate with 21.6% due to extensive use in biodiesel and oleochemical industries.

In 2025, Methyl Esters held a dominant market position in the By Product segment of the Esters Market, with a 21.6% share. Methyl esters serve as the primary component in biodiesel production and industrial solvent applications. Their cost-effectiveness and straightforward synthesis make them widely accessible. Additionally, expanding renewable energy mandates across Europe and Asia support sustained demand for fatty acid methyl esters.

Dibasic Esters function as key solvents in paint, coating, and adhesive formulations. Their low toxicity and excellent solvency power make them preferred in low-VOC product lines. Polyol Esters serve high-performance lubricant applications, especially in aviation and refrigeration equipment. Their outstanding thermal and oxidative stability support use in extreme operating environments.

Nitrate Esters find application primarily in explosives and pharmaceutical intermediates. Vinyl Esters serve as critical resins in marine, construction, and aerospace composite manufacturing. Phosphate Esters act as flame retardants and hydraulic fluids in industrial and aviation sectors. Additionally, Acrylic Esters support coatings, adhesives, and superabsorbent polymer production at a significant commercial scale.

Sucrose Esters serve as food-grade emulsifiers in baked goods, beverages, and confectionery products. Their safety profile and functionality drive adoption in the food and personal care industries. Fatty Acid Esters provide versatile performance across lubricants, cosmetics, and pharmaceutical formulations. Therefore, their broad compatibility and bio-based sourcing potential make them commercially significant across multiple end-use segments.

By Application Analysis

Lubricants dominate with 24.8% due to high demand in automotive, aerospace, and industrial machinery.

In 2025, Lubricants held a dominant market position in the By Application segment of the Esters Market, with a 24.8% share. Ester-based lubricants outperform mineral oils in high-temperature and high-pressure environments. Moreover, growing electrification of vehicles and energy-efficient machinery drives demand for synthetic ester lubricants with superior thermal management properties.

Solvents represent the second major application, serving the paint, coatings, adhesives, and cleaning product industries. Their low toxicity and strong solvency profiles support regulatory compliance in eco-friendly formulations. Plasticizers enhance the flexibility and durability of PVC and other polymers. Demand grows specifically for non-phthalate ester plasticizers as safety regulations tighten across consumer product industries.

Fuel and Oil Additives improve combustion efficiency and engine protection in automotive and marine applications. Flame Retardants based on phosphate esters provide fire safety in electronics, textiles, and construction materials. Insecticides and Explosives represent specialized chemical applications for ester compounds. Furthermore, Surfactants and Flavoring Agents expand ester use into food processing and personal care formulation industries.

By End-Use Analysis

Chemicals dominate with 27.9% due to extensive ester use in specialty chemical manufacturing processes.

In 2025, Chemicals held a dominant market position in the By End-Use segment of the Esters Market, with a 27.9% share. The chemical industry consumes esters as intermediates, solvents, and reaction components across hundreds of manufacturing processes. Consequently, growth in specialty chemicals and fine chemicals production directly amplifies ester consumption at an industrial scale.

Food applications include emulsifiers, flavor compounds, and preservatives that rely on food-grade esters for safety and functionality. The Automotive and Aviation sectors depend on high-performance synthetic esters for lubricants, hydraulic fluids, and fuel additives. Marine applications similarly require ester-based lubricants and composite resins for vessel performance and environmental compliance.

Textiles use esters in finishing agents, softeners, and dye carriers during fiber processing. The Cosmetics and Personal Care Products sector adopts fatty acid esters and sucrose esters for moisturizers, emollients, and skin conditioning formulations. Additionally, the Others category includes construction, electronics, and healthcare applications that collectively consume meaningful volumes of ester compounds across diverse product lines.

Key Market Segments

By Source

- Synthetic

- Natural

By Product

- Methyl Esters

- Dibasic Esters

- Polyol Esters

- Nitrate Esters

- Vinyl Esters

- Phosphate Esters

- Acrylic Esters

- Sucrose Esters

- Fatty Acid Esters

By Application

- Lubricants

- Solvents

- Plasticizers

- Fuel and Oil Additives

- Flame Retardants

- Insecticides

- Explosives

- Surfactants

- Flavoring Agents

By End-Use

- Chemicals

- Food

- Automotive and Aviation

- Marine

- Textiles

- Cosmetics and Personal Care Products

- Others

Emerging Trends

Sustainability and Innovation Reshape the Global Esters Market Landscape

Polymer industries are rapidly shifting away from phthalate-based plasticizers toward safer, non-phthalate ester alternatives. Regulatory pressure in Europe and North America accelerates this transition significantly. Moreover, manufacturers reformulate flexible PVC products to meet stringent chemical safety standards, creating consistent demand for bio-based and specialty ester plasticizers in consumer and industrial applications.

- Technological advancements improve ester synthesis efficiency and sustainability at a commercial scale. Enzymatic production methods reduce energy consumption and waste generation during manufacturing. Additionally, Oleon commissioned a technical review contract of up to USD 70,000 to optimize its North American esterification operations, reflecting industry investment in cleaner and more cost-effective production technologies across key manufacturing regions.

Industrial formulators reformulate products toward low-VOC and eco-friendly chemistries to meet environmental compliance standards. Ester-based solvents replace conventional alternatives in paints, coatings, and adhesives. Furthermore, premiumization trends in skincare drive ester adoption for their sensory and emollient properties. Consumers and brands increasingly favor natural ester ingredients that deliver luxury texture while aligning with clean beauty formulation standards.

Drivers

High-Performance Applications and Green Chemistry Demand Drive Esters Market Growth

Automotive and aerospace manufacturers increasingly demand high-performance synthetic ester lubricants to meet efficiency and emission targets. Ester-based lubricants outperform mineral oils under extreme thermal conditions. Moreover, Polynt Group’s Specialty Additives division, which includes specialty esters, generated revenue of €414.7 million in 2024, reflecting robust commercial demand for ester-based performance additives across industrial end markets.

- EU fatty acid methyl ester production reached 9.8 million tonnes, underscoring the large-scale industrial adoption of ester chemistry in renewable fuels. This scale demonstrates how bio-based ester demand accelerates alongside decarbonization targets set by governments and industry bodies across major energy-consuming markets worldwide.

Personal care and cosmetics brands adopt fatty acid esters and sucrose esters extensively in premium skincare and haircare formulations. Their emollient, spreading, and conditioning properties enhance product performance. Additionally, growing consumer preference for natural and plant-derived ingredients strengthens demand for bio-based esters in cosmetic applications, particularly across the Asia Pacific and European premium beauty markets.

Restraints

Raw Material Volatility and High Production Costs Restrain Esters Market Expansion

Raw material price volatility significantly challenges ester manufacturers across global supply chains. Feedstocks such as fatty acids, acrylic acid, and alcohols experience frequent price fluctuations tied to crude oil and agricultural commodity markets. Consequently, producers struggle to maintain consistent margins, especially when passing cost increases to price-sensitive industrial buyers in developing regions.

- High manufacturing costs compared to conventional chemical alternatives limit ester adoption in cost-competitive segments. Specialty ester production requires advanced processing equipment and strict quality controls. Furthermore, European imports of FAME biodiesel fell from nearly 4 million tonnes in 2019 to just over 2 million tonnes in 2024, partly reflecting domestic capacity pressures and trade-cost sensitivities that affect ester market economics at the regional scale.

Smaller manufacturers face significant barriers when attempting to scale up ester production capabilities. Capital-intensive infrastructure requirements restrict market entry for new players. Moreover, meeting increasingly complex regulatory compliance standards across multiple geographies adds further cost burden. Therefore, these combined financial and regulatory pressures slow the pace of capacity expansion in several developing and emerging ester production markets globally.

Growth Factors

Sustainability Regulations and Technological Innovation Accelerate Esters Market Expansion

The development of biodegradable synthetic ester lubricants creates significant market opportunities across automotive, marine, and industrial sectors. Formulators replace mineral oil-based lubricants with environmentally compliant ester alternatives. Additionally, LANXESS, a major supplier of synthetic ester lubricants, recorded sales of EUR 6.4 billion in 2024 across 32 countries, demonstrating the commercial scale achievable by companies that specialize in high-performance ester chemistry portfolios.

- Croda International, whose portfolio includes numerous ester-based specialty ingredients, reported 2024 Group sales of £1,628.1 million with an adjusted operating margin of 17.2%. This performance highlights how premium ester ingredients command strong profitability. Moreover, expanding demand for multifunctional and enzymatically synthesized esters in food, pharmaceutical, and personal care markets supports continued revenue growth for specialty producers.

European REACH regulations increasingly favor high-purity bio-based esters over conventional chemical alternatives. Manufacturers reformulate products to achieve regulatory compliance and sustainability certifications. Furthermore, growing adoption of microplastic-free formulations in cosmetics and personal care accelerates natural ester demand. This regulatory and consumer-driven shift creates durable long-term growth opportunities for producers investing in sustainable esterification technologies and capacity.

Regional Analysis

Asia Pacific Dominates the Esters Market with a Market Share of 38.5%, Valued at USD 3.3 Billion

Asia Pacific leads the global esters market with a dominant 38.5% share, valued at approximately USD 3.3 billion in 2025. China, India, Japan, and South Korea drive demand through large-scale chemical manufacturing, automotive production, and rapidly expanding personal care industries. Moreover, competitive production costs and strong domestic demand make the region the most attractive hub for ester manufacturing and consumption globally.

North America represents a significant esters market driven by advanced manufacturing in automotive, aerospace, and specialty chemicals. The United States leads regional demand for high-performance synthetic ester lubricants and bio-based plasticizers. Additionally, stringent environmental regulations accelerate the adoption of non-phthalate and low-VOC ester alternatives across multiple industrial and consumer product categories throughout the region.

Europe holds a strong position in the global esters market, supported by robust demand from chemicals, automotive, and personal care sectors. REACH regulations drive formulators toward sustainable, high-purity bio-based esters. Furthermore, Germany, France, and the UK remain key consumption centers, while expanding biodiesel mandates sustain large-volume demand for fatty acid methyl esters across the European renewable fuels industry.

Latin America presents moderate growth potential in the esters market, led by Brazil and Mexico. Growing automotive production, agricultural chemical use, and expanding food processing industries drive ester consumption. Moreover, rising consumer demand for personal care and cosmetic products in Brazil creates new opportunities for fatty acid ester suppliers targeting premium skincare and haircare formulation applications.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Mitsubishi Chemical Group Corporation operates as one of the most diversified chemical companies in the world, with a strong presence in ester-based specialty chemicals, plasticizers, and acrylic ester production. The company invests significantly in sustainable chemistry and advanced material development. Its broad product portfolio and global manufacturing network position it competitively across multiple high-growth ester application segments worldwide.

Croda International Plc. focuses on specialty ester ingredients for personal care, life sciences, and industrial markets. Croda’s consistent investment in bio-based and sustainable ester innovation supports its premium market positioning and long-term growth trajectory.

BASF SE maintains a comprehensive ester chemistry portfolio that spans acrylic esters, polyol esters, and specialty ester intermediates. The company continuously expands its Verbund production capacity to integrate upstream and downstream ester value chains efficiently. Its global research network and sustainability commitments, including greenhouse gas reduction programs, enable BASF to develop next-generation ester solutions across diverse industrial and consumer end markets.

Exxon Mobil Corporation leverages its large-scale petrochemical infrastructure to supply ester feedstocks and specialty lubricant esters for automotive and industrial applications. The company’s technical expertise in synthetic lubricant formulation supports strong positioning in high-performance ester lubricant segments.

Top Key Players in the Market

- Mitsubishi Chemical Group Corporation

- Esters and Solvents LLP

- Croda International Plc.

- BASF SE

- Estelle Chemicals Pvt. Ltd.

- Exxon Mobil Corporation

- The Dow Chemical Company

- Arkema

- Solvay

- Evonik Industries AG

Recent Developments

- In 2025, Mitsubishi Chemical Group Corporation published an article highlighting how Sugar Esters address food industry challenges, such as improving processing and product quality for items like baked goods and dairy. They announced an extension of their partnership with ChemPoint to distribute RYOTO Sugar Esters, expanding their food ingredient portfolio.

- In 2025, Croda launched Natrineo CR8, a PEG-free phosphate ester emulsifier that enables water-in-oil-in-water (W/O/W) emulsions with a single ingredient, thereby enhancing formulation simplicity in beauty products. Croda, a UK-based company, focuses on high-performance ingredients, including esters for personal care, beauty, and industrial applications.

Report Scope

Report Features Description Market Value (2025) USD 8.6 Billion Forecast Revenue (2035) USD 13.2 Billion CAGR (2026-2035) 4.4% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Source (Synthetic, Natural), By Product (Methyl Esters, Dibasic Esters, Polyol Esters, Nitrate Esters, Vinyl Esters, Phosphate Esters, Acrylic Esters, Sucrose Esters, Fatty Acid Esters), By Application (Lubricants, Solvents, Plasticizers, Fuel and Oil Additives, Flame Retardants, Insecticides, Explosives, Surfactants, Flavoring Agents), By End-Use (Chemicals, Food, Automotive and Aviation, Marine, Textiles, Cosmetics and Personal Care Products, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Mitsubishi Chemical Group Corporation, Esters and Solvents LLP, Croda International Plc., BASF SE, Estelle Chemicals Pvt. Ltd., Exxon Mobil Corporation, The Dow Chemical Company, Arkema, Solvay, Evonik Industries AG Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- Mitsubishi Chemical Group Corporation

- Esters and Solvents LLP

- Croda International Plc.

- BASF SE

- Estelle Chemicals Pvt. Ltd.

- Exxon Mobil Corporation

- The Dow Chemical Company

- Arkema

- Solvay

- Evonik Industries AG

Our Clients

- 179848

- March 2026