Global Endoscopy Visualization Systems Market By Product Type (Visualization Systems and Visualization Components), By Resolution (4K (UHD/DCI) and FHD/HD), By End-User (Hospitals and ASCs & Specialty Clinics), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 178952

- Number of Pages: 374

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

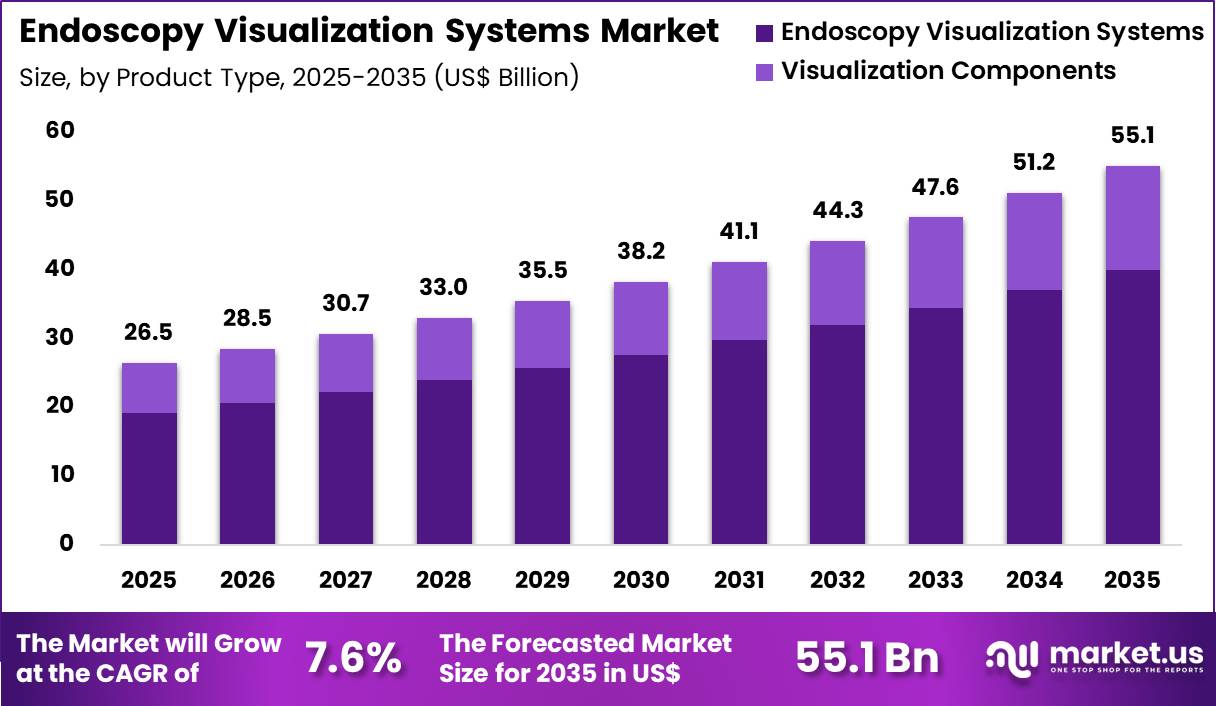

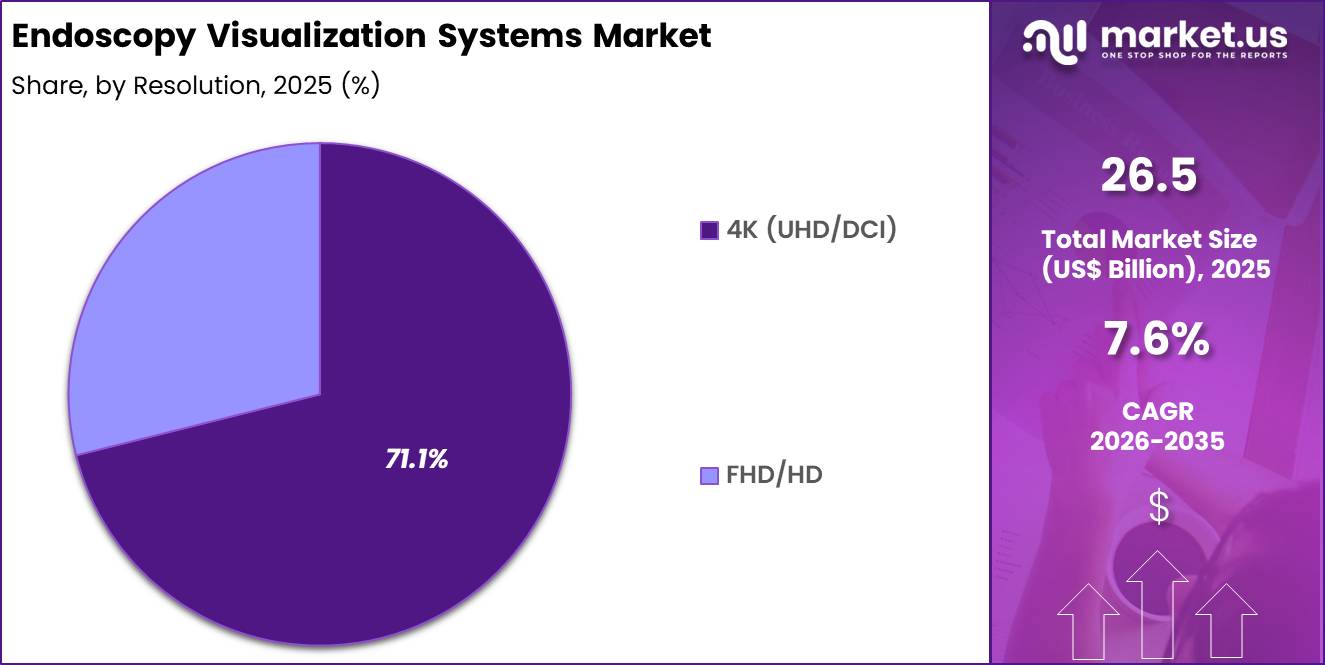

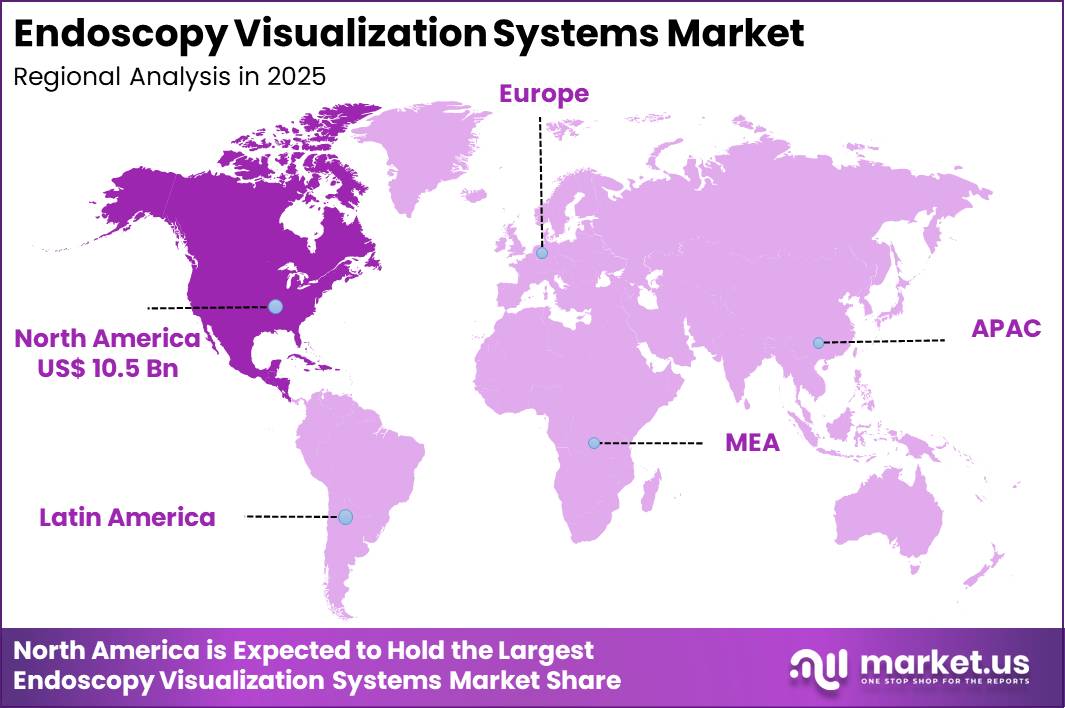

The Global Endoscopy Visualization Systems Market size is expected to be worth around US$ 55.1 Billion by 2035 from US$ 26.5 Billion in 2025, growing at a CAGR of 7.6% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 39.6% share with a revenue of US$ 10.5 Billion.

Rising adoption of minimally invasive surgical techniques propels the endoscopy visualization systems market as surgeons and gastroenterologists demand high-resolution imaging that enhances procedural accuracy and patient outcomes.

Gastrointestinal endoscopists increasingly utilize advanced visualization systems during colonoscopies and upper endoscopies to detect subtle mucosal abnormalities, guiding polypectomy and biopsy in colorectal cancer screening.

These systems support therapeutic interventions in urology, where high-definition cystoscopes and ureteroscopes enable precise resection of bladder tumors and stone fragmentation with reduced recurrence rates. Thoracic surgeons apply video-assisted thoracoscopic surgery platforms equipped with 4K imaging to perform lung resections and mediastinal lymph node sampling, improving staging accuracy in non-small cell lung cancer.

Otolaryngologists leverage narrow-band imaging and high-magnification endoscopes for laryngeal and pharyngeal evaluations, facilitating early detection of precancerous lesions during voice-preserving procedures. In arthroscopy, orthopedic surgeons rely on these systems to visualize joint surfaces and perform ligament reconstructions with minimal tissue disruption.

Manufacturers pursue opportunities to integrate artificial intelligence algorithms that provide real-time lesion detection and characterization, expanding applications in polyp identification and Barrett’s esophagus surveillance during routine screenings. Developers advance 3D and augmented reality visualization that enhances depth perception in robotic-assisted and laparoscopic procedures, broadening utility in complex hepatobiliary and gynecologic surgeries.

These innovations facilitate fluorescence-guided endoscopy with indocyanine green for sentinel lymph node mapping and vascular assessment. Opportunities emerge in portable, wireless systems that support point-of-care diagnostics in ambulatory settings.

Companies invest in ultra-high-definition and hyperspectral imaging to improve tissue differentiation in oncology applications. Recent trends emphasize seamless integration with robotic platforms and cloud-based analytics, positioning endoscopy visualization systems as essential enablers of precision surgery and value-based care.

Key Takeaways

- In 2025, the market generated a revenue of US$ 5 billion, with a CAGR of 7.6% , and is expected to reach US$ 55.1 billion by the year 2035.

- The product type segment is divided into visualization systems and visualization components, with endoscopy visualization systems taking the lead with a market share of 72.4%.

- Considering resolution, the market is divided into 4K (UHD/DCI) and FHD/HD. Among these, 4k held a significant share of 71.1%.

- Furthermore, concerning the end-user segment, the market is segregated into hospitals and ASCs & specialty clinics. The hospitals sector stands out as the dominant player, holding the largest revenue share of 48.7% in the market.

- North America led the market by securing a market share of 39.6%.

Product Type Analysis

Endoscopy visualization systems accounted for 72.4% of growth within product type and led the endoscopy visualization systems market due to their comprehensive integration of camera heads, processors, light sources, and display units into a unified platform. Hospitals prioritize full-system upgrades to ensure compatibility, image consistency, and workflow efficiency across operating rooms.

Integrated systems improve surgical precision by delivering enhanced color accuracy and tissue differentiation. Rising adoption of minimally invasive procedures further increases demand for advanced visualization platforms.

Growth strengthens as healthcare providers modernize operating theaters with digital integration capabilities. System-level procurement supports long-term service agreements and standardized maintenance.

Surgeons prefer cohesive platforms that reduce technical variability during procedures. Technological innovation in image enhancement and recording features reinforces replacement cycles. The segment is expected to remain dominant as hospitals continue to invest in complete visualization ecosystems rather than standalone components.

Resolution Analysis

4K resolution generated 71.1% of growth within resolution and emerged as the leading segment due to superior image clarity and depth perception. Surgeons rely on ultra-high-definition imaging to identify fine anatomical structures and subtle tissue variations during complex procedures.

Enhanced pixel density improves visualization in laparoscopic, arthroscopic, and gastrointestinal interventions. Clinical demand for precision strengthens transition from HD to 4K platforms.

Growth accelerates as 4K systems increasingly replace HD as the surgical standard. Training programs and academic centers emphasize high-definition imaging for improved outcomes. Equipment manufacturers expand 4K-compatible accessories, which enhances system adoption.

Rising expectations for documentation and recording quality further reinforce 4K upgrades. The segment is anticipated to maintain leadership as high-resolution imaging becomes integral to advanced minimally invasive surgery.

End-User Analysis

Hospitals contributed 48.7% of growth within end-user and dominated the endoscopy visualization systems market due to high procedural volumes and complex surgical case loads. Large tertiary centers perform diverse minimally invasive surgeries that require advanced imaging infrastructure.

Hospitals invest in next-generation visualization systems to improve patient outcomes and reduce operative time. Centralized procurement and capital budgets support comprehensive system upgrades.

Growth continues as hospitals expand specialty departments such as gastroenterology, urology, and orthopedics. Accreditation and quality benchmarks encourage adoption of advanced imaging technologies. Teaching hospitals further drive utilization through surgical training and research activities.

Referral networks concentrate advanced cases within hospital settings. The segment is projected to remain a primary growth driver as hospitals continue to anchor high-complexity endoscopic procedures.

Key Market Segments

By Product Type

- Visualization Systems

- Visualization Components

By Resolution

- 4K (UHD/DCI)

- FHD/HD

By End-User

- Hospitals

- ASCs & Specialty Clinics

Drivers

Increasing prevalence of gastrointestinal diseases is driving the market.

The global rise in gastrointestinal diseases has significantly boosted the demand for endoscopy visualization systems to enable accurate diagnosis and treatment of conditions such as inflammatory bowel disease and colorectal cancer. Enhanced screening programs and lifestyle factors have led to more frequent detections of GI disorders, expanding the application of advanced visualization in clinical settings.

Healthcare providers are increasingly deploying these systems to support minimally invasive procedures that improve patient outcomes in gastroenterology. The correlation between aging populations and higher GI disease rates further amplifies the need for high-resolution imaging solutions. Government health organizations emphasize early detection to reduce mortality from digestive disorders, supporting broader adoption.

Endoscopy visualization systems offer superior image quality for identifying lesions and guiding interventions. National health statistics document the growing burden of these diseases, prompting greater investment in diagnostic infrastructure.

Key manufacturers are refining systems to meet this escalating clinical requirement. This driver fosters innovation in camera technology and light sources for better visualization. According to the Centers for Disease Control and Prevention, the number of visits to physician offices with diseases of the digestive system as the primary diagnosis was 35.4 million in 2022.

Restraints

High Capital Cost of Advanced Visualization Systems restrains the market

The high acquisition cost of advanced endoscopy visualization platforms remains a key market restraint. Premium 4K cameras, image processors, and integrated software modules significantly increase upfront investment requirements, particularly for facilities operating under tight capital budgets.

Complex manufacturing processes, precision optics, and compliance with stringent regulatory standards further elevate system pricing. As a result, smaller hospitals and public healthcare institutions frequently delay upgrades and continue using standard-definition infrastructure to preserve financial flexibility.

Operational expenses also contribute to the economic burden, including maintenance contracts, sterilization protocols, and system integration costs. Public procurement frameworks often prioritize lower-cost alternatives, slowing adoption of cutting-edge imaging technologies.

A micro-costing study published in BMJ Open Gastroenterology estimated that reprocessing gastrointestinal endoscopes cost the NHS approximately £107.34 per procedure in 2024, highlighting the cumulative economic pressures associated with endoscopy services. These financial considerations limit scalability, particularly across developing healthcare systems with constrained funding allocations.

Opportunities

Rising Medical Imaging Revenue Momentum creates opportunities

Sustained growth in global medical imaging revenues is creating favorable conditions for expanded adoption of advanced endoscopy visualization systems. Increasing investments in imaging infrastructure support the integration of high-definition endoscopic platforms within multidisciplinary procedural suites. Large hospital networks are strengthening digital connectivity between radiology and endoscopy units, enhancing image-sharing capabilities and clinical decision workflows.

Financial disclosures from leading manufacturers underscore this upward trajectory. GE HealthCare reported imaging revenues rising from $8,855 million in 2023 to $9,245 million in 2024. Siemens Healthineers recorded imaging segment adjusted revenues increasing from €11.9 billion in fiscal year 2023 to €12.3 billion in fiscal year 2024.

This sustained revenue expansion signals institutional willingness to invest in advanced imaging ecosystems, creating opportunities for vendors to position next-generation visualization platforms as part of integrated diagnostic strategies across developed and emerging markets.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic dynamics influence the endoscopy visualization systems market through hospital capital discipline, procedure volumes, and reimbursement clarity across surgical departments. Elevated inflation increases the cost of optics, cameras, processors, and displays, which prompts facilities to defer upgrades of high definition and 4K platforms.

Higher interest rates tighten access to financing for large tower systems and integrated operating room investments. Geopolitical tensions disrupt the flow of precision lenses, semiconductors, and imaging chips, creating supply variability and longer installation timelines.

Current US tariffs on imported electronic assemblies and optical components raise acquisition and service expenses, which pressures vendor margins and extends budget approvals. These constraints can delay technology refresh cycles, particularly in community hospitals.

On the positive side, trade exposure drives regional manufacturing, stronger supplier diversification, and closer integration of service contracts. Growing demand for minimally invasive procedures and enhanced visualization quality sustains steady adoption and positions the market for resilient long term growth.

Latest Trends

Integration of artificial intelligence in endoscopy visualization is a recent trend in the market.

In 2024, the incorporation of AI algorithms in endoscopy visualization systems has advanced lesion detection during procedures. These systems utilize machine learning to highlight abnormalities in real-time, improving diagnostic precision. Manufacturers focused on regulatory clearance for AI modules to ensure clinical safety.

Clinical studies in 2024 demonstrated reduced miss rates for polyps in colonoscopy. Medtronic unveiled ColonPRO in April 2024, the latest AI software for its GI Genius intelligent endoscopy system. This innovation facilitates early heart failure screening in primary care settings without additional equipment.

Industry emphasis on integration with electronic records streamlines clinical workflows. The trend responds to demands for proactive gastrointestinal management. Regulatory pathways have become clearer for AI-enabled endoscopy devices, accelerating approvals. Sector synergies concentrate on refining models for superior pattern recognition in endoscopic images.

Regional Analysis

North America is leading the Endoscopy Visualization Systems Market

North America held a 39.6% share of the Endoscopy Visualization Systems market in 2024, supported by rising adoption of advanced imaging platforms across hospitals and specialty clinics. Healthcare providers accelerated the shift toward ultra high definition, narrow band imaging, and enhanced light technologies to improve diagnostic precision.

Growing preference for minimally invasive gastrointestinal and pulmonary procedures increased demand for reliable visualization towers and camera systems. Screening initiatives for colorectal and upper GI disorders further elevated procedural volumes in both hospital and ambulatory settings.

Providers also replaced legacy analog equipment with digitally integrated systems that enable image capture, storage, and real time collaboration. Expansion of outpatient endoscopy centers strengthened recurring procurement cycles.

A credible indicator of underlying procedure demand comes from the Centers for Disease Control and Prevention, which reported in 2023 that colorectal cancer remains one of the most commonly diagnosed cancers in the US, reinforcing the importance of high quality endoscopic imaging.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

The Endoscopy Visualization Systems market in Asia Pacific is expected to witness strong progress during the forecast period as healthcare systems scale diagnostic capabilities and modernize operating suites. Governments prioritize cancer detection and early intervention programs, encouraging hospitals to invest in high clarity imaging platforms.

Physicians increasingly adopt minimally invasive techniques to shorten recovery time and improve patient outcomes. Rising disposable income enables broader access to private diagnostic services across metropolitan areas. Regional training initiatives strengthen clinician expertise in advanced endoscopic procedures.

Equipment manufacturers expand local service networks to support installation and maintenance. A verifiable signal of regional disease burden appears in 2023 data from the International Agency for Research on Cancer, which highlights Asia as accounting for a significant proportion of global gastrointestinal cancer cases, underscoring sustained need for modern visualization technologies.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key competitors in the endoscopy visualization systems market grow by advancing high-resolution imaging, 3D and fluorescence capabilities, and seamless integration with surgical information systems that help clinicians improve procedural accuracy and diagnostic confidence.

They also strengthen their value propositions by offering bundled solutions that combine cameras, displays, and software analytics with training, service contracts, and workflow optimization support for hospitals and ambulatory surgical centers. Firms pursue strategic alliances with leading healthcare providers and research institutions to align product roadmaps with emerging clinical needs and evidence-based practice.

Geographic expansion into North America, Europe, and fast-growing Asia Pacific broadens addressable demand amid rising minimally invasive surgery volumes and healthcare infrastructure investments. Olympus Corporation exemplifies a global leader in medical visualization with a comprehensive portfolio of endoscopic imaging platforms, deep clinical partnerships, and coordinated global commercial operations that support broad procedural coverage.

The company advances its competitive agenda through disciplined R&D funding, targeted acquisitions that extend complementary capabilities, and a customer-centric approach that translates technological enhancements into meaningful clinical and operational value.

Top Key Players

- Olympus Corporation

- FUJIFILM Holdings Corporation

- KARL STORZ SE & Co. KG

- Stryker

- Smith & Nephew plc

- Medtronic

- Boston Scientific Corporation

- Richard Wolf GmbH

- PENTAX Medical

- CONMED Corporation

- Arthrex Inc.

- Aohua Endoscopy Co. Ltd.

Recent Developments

- In March 2024, FUJIFILM Corporation finalized the acquisition of the diagnostic imaging–related business from Hitachi, Ltd., strengthening its capabilities in advanced medical imaging technologies and expanding its global healthcare portfolio.

- In November 2024, Stryker Corp. completed its previously announced purchase of Wright Medical Group N.V., a global medical device manufacturer. The transaction enhances Stryker’s presence in orthopedic and extremities markets, reinforcing its position within the broader medical technology sector.

Report Scope

Report Features Description Market Value (2025) US$ 26.5 Billion Forecast Revenue (2035) US$ 55.1 Billion CAGR (2026-2035) 7.6% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product Type (Visualization Systems and Visualization Components), By Resolution (4K (UHD/DCI) and FHD/HD), By End-User (Hospitals and ASCs & Specialty Clinics) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Olympus, FUJIFILM, KARL STORZ, Stryker, Smith & Nephew, Medtronic, Boston Scientific, Richard Wolf, PENTAX Medical, CONMED, Arthrex, Aohua Endoscopy, Machida Endoscope, Ethicon. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Endoscopy Visualization Systems MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample

Endoscopy Visualization Systems MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Olympus Corporation

- FUJIFILM Holdings Corporation

- KARL STORZ SE & Co. KG

- Stryker

- Smith & Nephew plc

- Medtronic

- Boston Scientific Corporation

- Richard Wolf GmbH

- PENTAX Medical

- CONMED Corporation

- Arthrex Inc.

- Aohua Endoscopy Co. Ltd.

Our Clients

- 178952

- Feb 2026