Global Electromyography Devices Market By Product Type (Surface EMG Devices, Wearable / Portable EMG Systems, Needle EMG Devices, High-Density EMG Systems and EMG Electrodes & Accessories), By Modality (Stand-alone and Integrated), By Application (Neuromuscular Disorder Diagnosis, Research & Academia, Pain Management & Rehabilitation, Orthopedics & Sports Medicine and Intraoperative Monitoring), By End-user (Hospitals, Sports Rehabilitation Centers, Specialty Clinics, Ambulatory Surgical Centers and Academic & Research Institutes), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2034

- Published date: Jan 2026

- Report ID: 175981

- Number of Pages: 205

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

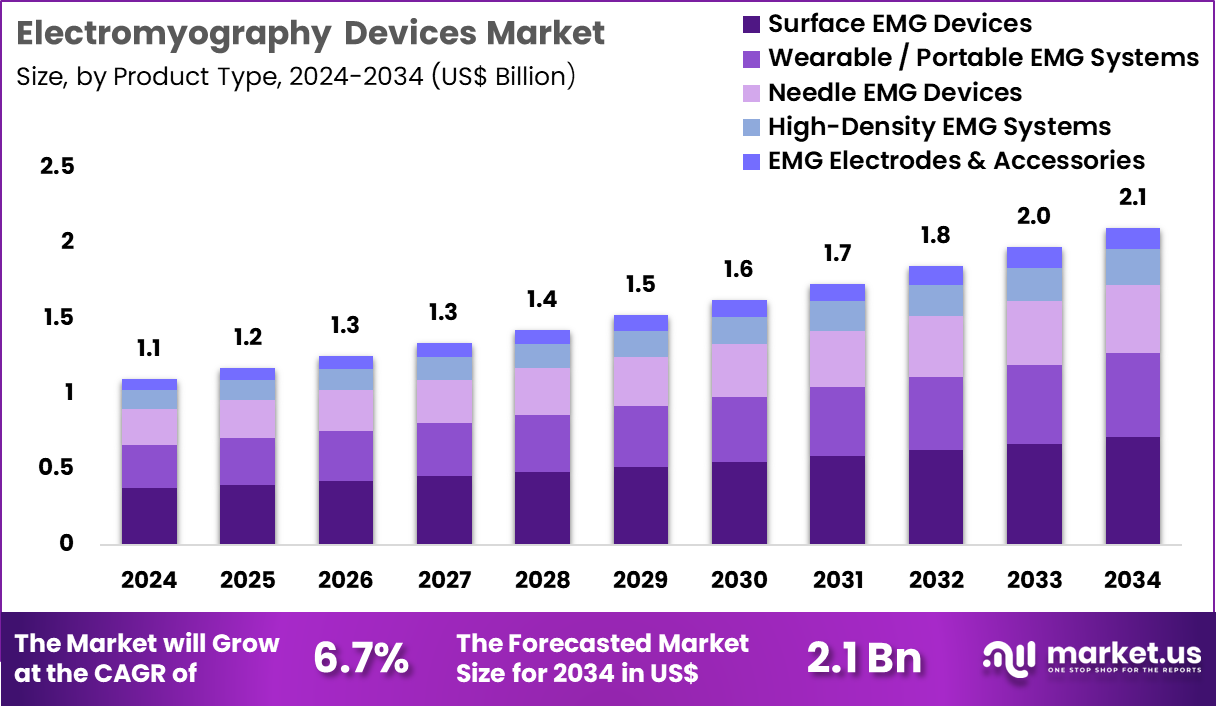

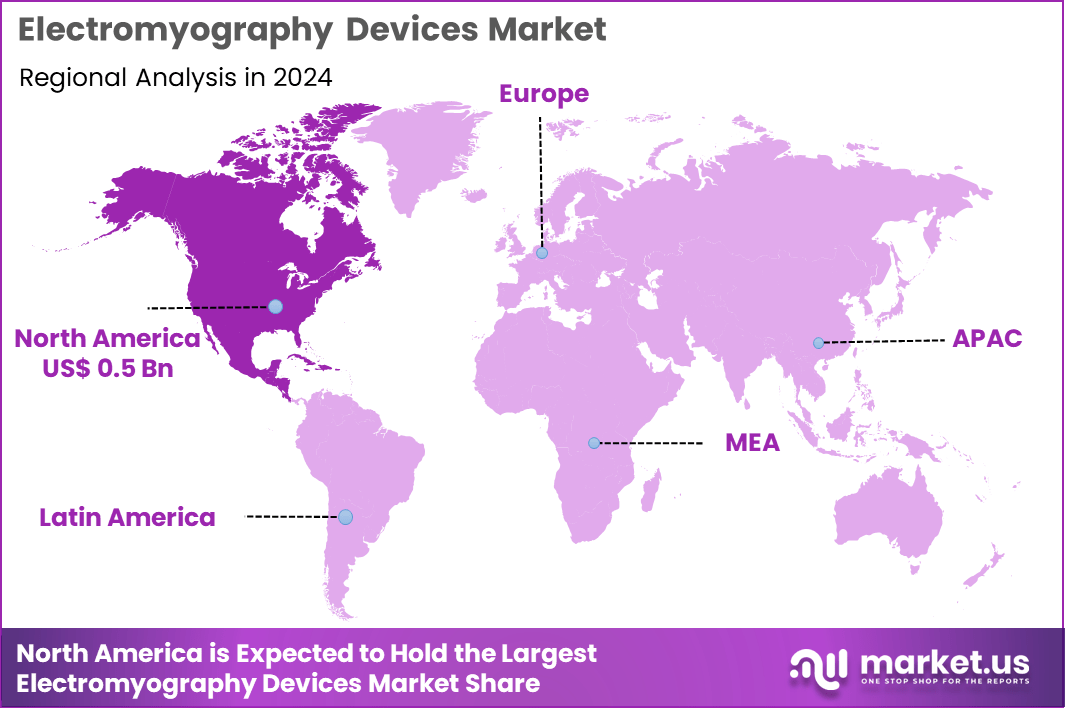

Global Electromyography Devices Market size is expected to be worth around US$ 2.1 Billion by 2034 from US$ 1.1 Billion in 2024, growing at a CAGR of 6.7% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 43.1% share with a revenue of US$ 0.5 Billion.

Increasing adoption of neuromuscular diagnostics in clinical and research settings drives the electromyography devices market as healthcare providers seek precise tools to evaluate muscle and nerve function across diverse patient populations. Neurologists increasingly utilize surface electromyography systems to assess muscle activation patterns in movement disorders, identifying abnormal synergies in Parkinson’s disease and dystonia for targeted rehabilitation strategies.

These devices support nerve conduction studies in peripheral neuropathies, measuring conduction velocities and amplitudes to diagnose carpal tunnel syndrome and diabetic polyneuropathy with high reproducibility. Clinicians apply needle electromyography in myopathy evaluations, detecting spontaneous activity and motor unit potentials to differentiate inflammatory from metabolic muscle disorders.

Physical therapists employ wireless EMG sensors during gait analysis, quantifying muscle recruitment in stroke survivors to guide individualized neurorehabilitation programs. Sports medicine specialists use high-density surface arrays to monitor fatigue and neuromuscular coordination in athletes, optimizing training protocols and injury prevention measures.

In January 2025, Natus Medical Incorporated announced the launch of a new portable EMG system tailored for mobile diagnostic use. Equipped with advanced software, the system enables real-time muscle activity tracking and seamless EHR integration, improving workflow efficiency and diagnostic accuracy across outpatient and remote care settings.

Manufacturers pursue opportunities to integrate artificial intelligence algorithms that automate waveform interpretation, expanding applications in high-volume neuromuscular clinics where rapid analysis accelerates diagnosis of amyotrophic lateral sclerosis and myasthenia gravis. Developers advance wearable EMG patches with extended battery life, facilitating continuous monitoring of muscle activity in chronic pain syndromes and spasticity management.

These innovations enable tele-EMG consultations, supporting remote evaluation of neuromuscular junction disorders and reducing the need for in-person visits in stable patients. Opportunities emerge in biofeedback-enabled devices that provide real-time visual cues to patients during pelvic floor therapy, improving outcomes in urinary incontinence and pelvic pain rehabilitation.

Companies invest in multi-channel systems with enhanced signal-to-noise ratios, enhancing precision in intraoperative neuromonitoring during spinal and cranial surgeries. Recent trends emphasize compact, cloud-connected platforms that streamline data sharing among multidisciplinary teams, positioning electromyography devices as essential tools in value-based neuromuscular care models.

Key Takeaways

- In 2024, the market generated a revenue of US$ 1.1 Billion, with a CAGR of 6.7%, and is expected to reach US$ 2.1 Billion by the year 2034.

- The product type segment is divided into surface EMG devices, wearable / portable EMG systems, needle EMG devices, high-density EMG systems and EMG electrodes & accessories, with surface EMG devices taking the lead with a market share of 33.9%.

- Considering modality, the market is divided into stand-alone and integrated. Among these, stand-alone held a significant share of 58.6%.

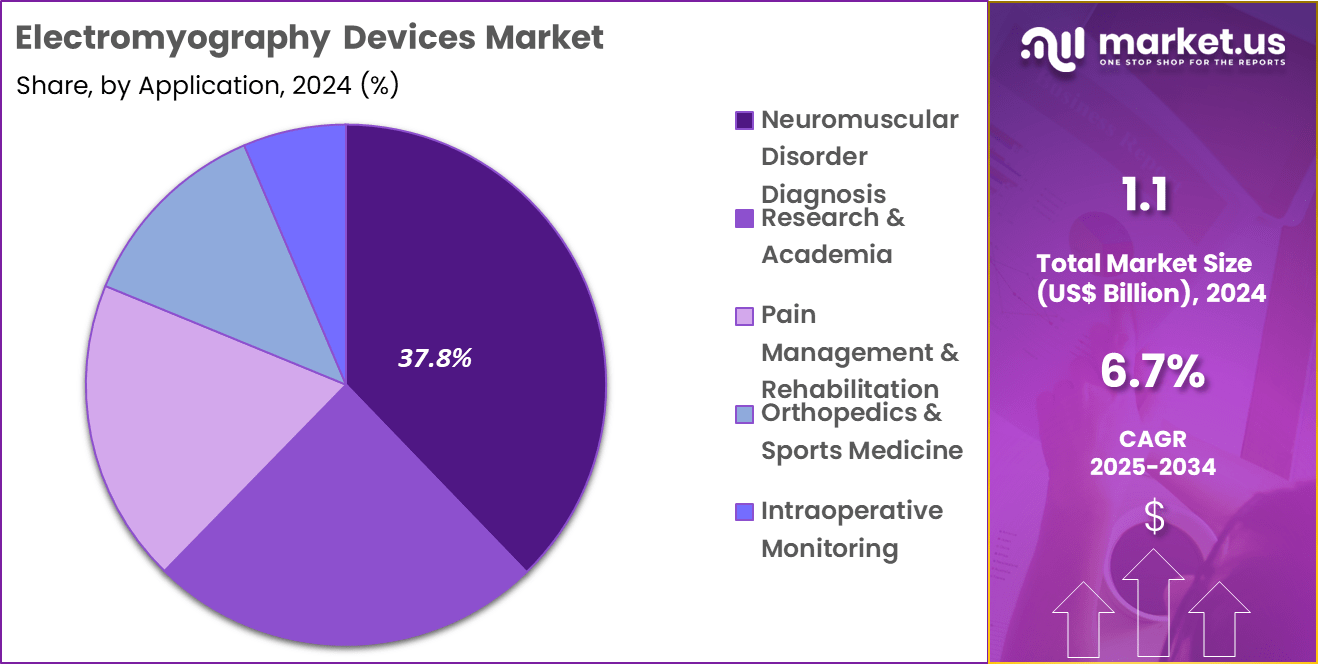

- Furthermore, concerning the application segment, the market is segregated into neuromuscular disorder diagnosis, research & academia, pain management & rehabilitation, orthopedics & sports medicine and intraoperative monitoring. The neuromuscular disorder diagnosis sector stands out as the dominant player, holding the largest revenue share of 37.8% in the market.

- The end-user segment is segregated into hospitals, sports rehabilitation centers, specialty clinics, ambulatory surgical centers and academic & research institutes, with the hospitals segment leading the market, holding a revenue share of 42.3%.

- North America led the market by securing a market share of 43.1%.

Product Type Analysis

Surface EMG devices contributed 33.9% of growth within product type and led the electromyography devices market due to their non-invasive nature and broad clinical acceptance. Clinicians prefer surface systems because they enable muscle activity assessment without needle insertion, which improves patient comfort and compliance.

Rising diagnosis of neuromuscular and musculoskeletal disorders increases demand for repeat testing, where surface EMG offers operational simplicity. Hospitals and rehabilitation centers adopt these devices to support routine evaluations and therapy monitoring across diverse patient groups.

Technological improvements further strengthen growth through enhanced signal processing and noise reduction capabilities. Compact designs and improved electrode adhesion expand usability in outpatient and bedside settings. Physical therapy programs increasingly rely on surface EMG for biofeedback-driven rehabilitation.

Training requirements remain lower compared to invasive alternatives, which supports faster deployment. The segment is projected to remain dominant as non-invasive diagnostics gain priority across neurology and rehabilitation workflows.

Modality Analysis

Stand-alone systems accounted for 58.6% of growth within modality and dominated the electromyography devices market due to their flexibility and ease of deployment. Healthcare facilities favor stand-alone units because they function independently without reliance on integrated hospital platforms. Smaller clinics and diagnostic centers adopt these systems to avoid complex IT dependencies.

Stand-alone devices support rapid setup, which suits high patient throughput environments. Growth accelerates as manufacturers introduce portable stand-alone units with advanced analytics and data storage. Hospitals value redundancy and operational continuity, which stand-alone systems provide during system upgrades or downtime.

Training and maintenance costs remain manageable compared to integrated solutions. Expansion of decentralized care models further supports adoption. The segment is expected to sustain leadership as providers prioritize operational autonomy and cost control.

Application Analysis

Neuromuscular disorder diagnosis generated 37.8% of growth within application and emerged as the leading segment due to increasing prevalence of nerve and muscle-related conditions. EMG testing plays a critical role in diagnosing disorders such as neuropathies, myopathies, and motor neuron diseases. Aging populations increase diagnostic demand as neuromuscular conditions rise with age.

Physicians rely on EMG to guide treatment decisions and monitor disease progression. Advances in diagnostic protocols strengthen reliance on electrophysiological testing. Early detection initiatives encourage timely evaluation of muscle weakness and nerve dysfunction.

EMG supports differentiation between neurological and muscular causes, improving diagnostic accuracy. Hospital neurology departments expand testing capacity to meet rising referrals. The segment is anticipated to grow steadily as clinical emphasis on precise neuromuscular assessment increases.

End-User Analysis

Hospitals contributed 42.3% of growth within end-user and dominated the electromyography devices market due to centralized diagnostic infrastructure and high patient volumes. Hospitals handle complex neurological cases that require comprehensive EMG evaluation.

Multidisciplinary care models increase coordination between neurology, orthopedics, and rehabilitation departments, which raises device utilization. Teaching hospitals also drive demand through continuous clinical training and research activity.

Investment in advanced diagnostic equipment supports hospital-led adoption. Integration of EMG testing into inpatient and outpatient pathways increases testing frequency. Regulatory emphasis on accurate diagnosis reinforces hospital procurement decisions. Expansion of neurology departments and specialty care units further strengthens demand. The hospital segment is projected to remain the primary growth driver due to its scale, expertise, and diagnostic responsibility.

Key Market Segments

By Product Type

- Surface EMG Devices

- Wearable / Portable EMG Systems

- Needle EMG Devices

- High-Density EMG Systems

- EMG Electrodes & Accessories

By Modality

- Stand-alone

- Integrated

By Application

- Neuromuscular Disorder Diagnosis

- Research & Academia

- Pain Management & Rehabilitation

- Orthopedics & Sports Medicine

- Intraoperative Monitoring

By End-user

- Hospitals

- Sports Rehabilitation Centers

- Specialty Clinics

- Ambulatory Surgical Centers

- Academic & Research Institutes

Drivers

Increasing prevalence of neurological disorders is driving the market.

The growing incidence of neurological disorders globally has significantly increased the demand for diagnostic tools such as electromyography devices to assess neuromuscular function. Enhanced awareness and improved diagnostic capabilities contribute to earlier identification of conditions like neuropathies and myopathies.

According to the World Health Organization, in 2021, more than 3 billion people worldwide were living with a neurological condition, as detailed in a 2024 report. This substantial figure illustrates the escalating health challenge and the need for precise EMG assessments in clinical practice. Electromyography devices enable detailed evaluation of muscle and nerve activity, essential for managing progressive disorders.

The association between aging populations and higher neurological risks further intensifies the requirement for these technologies. Public health initiatives prioritize neurological care, supporting the adoption of advanced diagnostic equipment.

Key manufacturers are responding by refining device accuracy to address this expanding patient population. This driver promotes investments in healthcare systems focused on neuromuscular diagnostics. Ultimately, the prevalence trend underpins continuous market development in medical diagnostics.

Restraints

High development costs are restraining the market.

The considerable investment required for researching and producing electromyography devices limits innovation and accessibility in competitive sectors. Complex engineering for signal accuracy and patient safety elevates overall production expenditures.

Medtronic reported research and development expenses of $2.735 billion in fiscal year 2024, an increase from $2.696 billion in the previous year. This escalation highlights the financial pressures on manufacturers developing advanced EMG systems. Regulatory requirements for clinical validation further amplify development budgets.

In resource-constrained environments, these costs restrict upgrades to existing diagnostic tools. Clinicians may rely on conventional methods to manage financial limitations. This restraint impacts scalability for smaller diagnostic facilities worldwide. Collaborative strategies aim to distribute costs, though challenges remain. Consequently, addressing expenditure efficiencies is crucial for mitigating this market barrier.

Opportunities

Expansion into emerging markets is creating growth opportunities.

The rapid advancement of healthcare systems in emerging regions provides pathways for electromyography device adoption in underserved areas. Governmental investments in medical infrastructure support the integration of diagnostic technologies for neurological assessments. Medtronic’s emerging markets revenue reached $5.823 billion in fiscal year 2024, reflecting a 6.9% increase as reported. This growth indicates rising demand for advanced devices in these dynamic economies.

Local partnerships facilitate regulatory adherence and distribution in diverse markets. The increasing burden of chronic conditions in populous nations amplifies the need for EMG solutions. Educational programs for healthcare providers enhance proficiency in utilizing these devices.

This opportunity allows global firms to diversify beyond established regions. Key corporations are establishing operations to optimize supply and reduce costs. Overall, emerging market expansions align with efforts to improve global diagnostic equity.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic forces shape the electromyography devices market through hospital capital budgets, outpatient volumes, and reimbursement discipline that executives monitor closely. Inflation and higher borrowing costs strain purchasing decisions for clinics and academic centers, which slows upgrades of diagnostic systems and accessories. Geopolitical friction disrupts supplies of sensors, microelectronics, and cables, increasing lead times and raising procurement risk.

Current US tariffs on imported electronic components and finished devices lift input costs for manufacturers and distributors, compressing margins and prompting selective price adjustments. These headwinds challenge smaller vendors and delay adoption in cost-sensitive settings. On the positive side, trade pressure encourages domestic sourcing, contract manufacturing in North America, and tighter supplier diversification.

Rising demand for neuromuscular diagnostics in sports medicine, rehabilitation, and outpatient care supports steady utilization. With disciplined cost control, product differentiation, and service-led models, the market can navigate volatility and sustain confident growth.

Latest Trends

Integration of artificial intelligence with surface electromyography is a recent trend in the market.

In 2024, the combination of surface electromyography with artificial intelligence has advanced predictive capabilities for neuromuscular assessments. AI algorithms process sEMG signals to identify subtle patterns indicative of muscle dysfunction. This integration facilitates real-time analysis for applications in elderly care and rehabilitation.

Studies emphasize AI’s role in enhancing signal interpretation for fall risk prediction in vulnerable populations. Wearable sEMG devices equipped with AI enable continuous monitoring of key muscle groups. The trend supports personalized interventions by detecting compensatory mechanisms during movement. Regulatory considerations are evolving to accommodate these hybrid technologies.

Industry collaborations focus on refining models for higher diagnostic accuracy. These developments address limitations in traditional EMG methods for dynamic evaluations. This evolution positions AI-sEMG as integral to future neuromuscular diagnostics.

Regional Analysis

North America is leading the Electromyography Devices Market

North America maintains a 43.1% share of the global Electromyography Devices market, exhibiting remarkable growth in 2024 propelled by heightened demand for advanced diagnostic tools in neurology and rehabilitation sectors. Major companies, including Natus Medical and Cadwell Industries, have rolled out upgraded portable EMG systems that integrate AI for faster and more accurate muscle and nerve assessments, catering to rising cases of peripheral neuropathies and muscular dystrophies.

The region’s extensive network of specialized clinics and hospitals has embraced these innovations to improve patient outcomes in sports medicine and geriatric care. Federal policies emphasizing early intervention for neurological conditions have spurred investments in research, leading to novel electrode designs and wireless monitoring capabilities.

An uptick in clinical trials focusing on EMG-guided therapies for chronic pain management has further stimulated market expansion. Partnerships between universities and manufacturers have accelerated product development, yielding FDA-cleared devices with enhanced sensitivity.

Moreover, increased awareness among physicians about the benefits of EMG in precise diagnosis has driven widespread adoption across outpatient facilities. The National Institutes of Health allocated $10.5 billion to neuroscience-related projects in 2024, directly supporting advancements in diagnostic technologies like EMG.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Experts project substantial progress in the neuromuscular diagnostics field throughout the Asia Pacific over the forecast period, as healthcare providers integrate cutting-edge tools to address escalating chronic conditions. Authorities in nations such as China and Japan allocate resources to upgrade medical infrastructure, which accelerates the introduction of sophisticated monitoring equipment.

Local manufacturers partner with global entities to customize solutions that meet regional needs for affordable and reliable assessments. Universities and research centers conduct studies that refine techniques for nerve conduction evaluations, enhancing clinical precision. Clinicians adopt these innovations to manage disorders like diabetic neuropathy more effectively, while economic expansion enables broader access to specialized care.

International aid organizations contribute expertise that strengthens local capabilities in device calibration and data analysis. Venture capital flows into startups that pioneer compact systems for remote applications, fostering competition and quality improvements. China’s National Medical Products Administration approved 138 innovative medical devices since 2022, bolstering the sector’s momentum in the region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the Electromyography Devices market pursue growth by advancing signal processing technologies, enhancing user interfaces, and integrating wireless capabilities that support streamlined clinical workflows and remote diagnostics. They pursue targeted partnerships with rehabilitation centers, neurology clinics, and academic hospitals to deepen adoption across specialty care settings.

Expanding geographic footprints in emerging regions enables them to tap unmet demand while balancing competitive pressures in developed healthcare markets. Companies also diversify revenue streams by bundling training services, software upgrades, and consumables into comprehensive customer solutions.

Natus Medical Incorporated serves as a prominent example with its broad portfolio of neurodiagnostic and newborn care products, strong sales channels, and a strategy that emphasizes clinical support and product reliability. The firm reinforces its competitive position through disciplined innovation investment, responsive customer engagement, and scalable distribution networks.

Top Key Players

- Natus Medical Incorporated

- Nihon Kohden Corporation

- Cadwell Industries

- Compumedics Limited

- Medtronic

- Neurosoft

- Noraxon USA

- OT Bioelettronica

- Electrical Geodesics Inc.

- Biometrics Ltd.

Recent Developments

- In June 2025, Firefly Neuroscience completed the acquisition of Evoke Neuroscience for USD 6 million. The transaction strengthens Firefly’s FDA-cleared brain analytics database and expands its capabilities in quantitative neuroassessment.

- In May 2024, the FDA granted approval to Boston Scientific for its WaveWriter spinal cord stimulation systems. The approval supports the use of these systems in the treatment of chronic pain, reinforcing Boston Scientific’s position in neuromodulation therapies.

Report Scope

Report Features Description Market Value (2024) US$ 1.1 Billion Forecast Revenue (2034) US$ 2.1 Billion CAGR (2025-2034) 6.7% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product Type (Surface EMG Devices, Wearable / Portable EMG Systems, Needle EMG Devices, High-Density EMG Systems and EMG Electrodes & Accessories), By Modality (Stand-alone and Integrated), By Application (Neuromuscular Disorder Diagnosis, Research & Academia, Pain Management & Rehabilitation, Orthopedics & Sports Medicine and Intraoperative Monitoring), By End-user (Hospitals, Sports Rehabilitation Centers, Specialty Clinics, Ambulatory Surgical Centers and Academic & Research Institutes) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Natus Medical Incorporated, Nihon Kohden Corporation, Cadwell Industries, Compumedics Limited, Medtronic, Neurosoft, Noraxon USA, OT Bioelettronica, Electrical Geodesics Inc., Biometrics Ltd. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Electromyography Devices MarketPublished date: Jan 2026add_shopping_cartBuy Now get_appDownload Sample

Electromyography Devices MarketPublished date: Jan 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Natus Medical Incorporated

- Nihon Kohden Corporation

- Cadwell Industries

- Compumedics Limited

- Medtronic

- Neurosoft

- Noraxon USA

- OT Bioelettronica

- Electrical Geodesics Inc.

- Biometrics Ltd.

Our Clients

- 175981

- Jan 2026