Quick Navigation

Report Overview

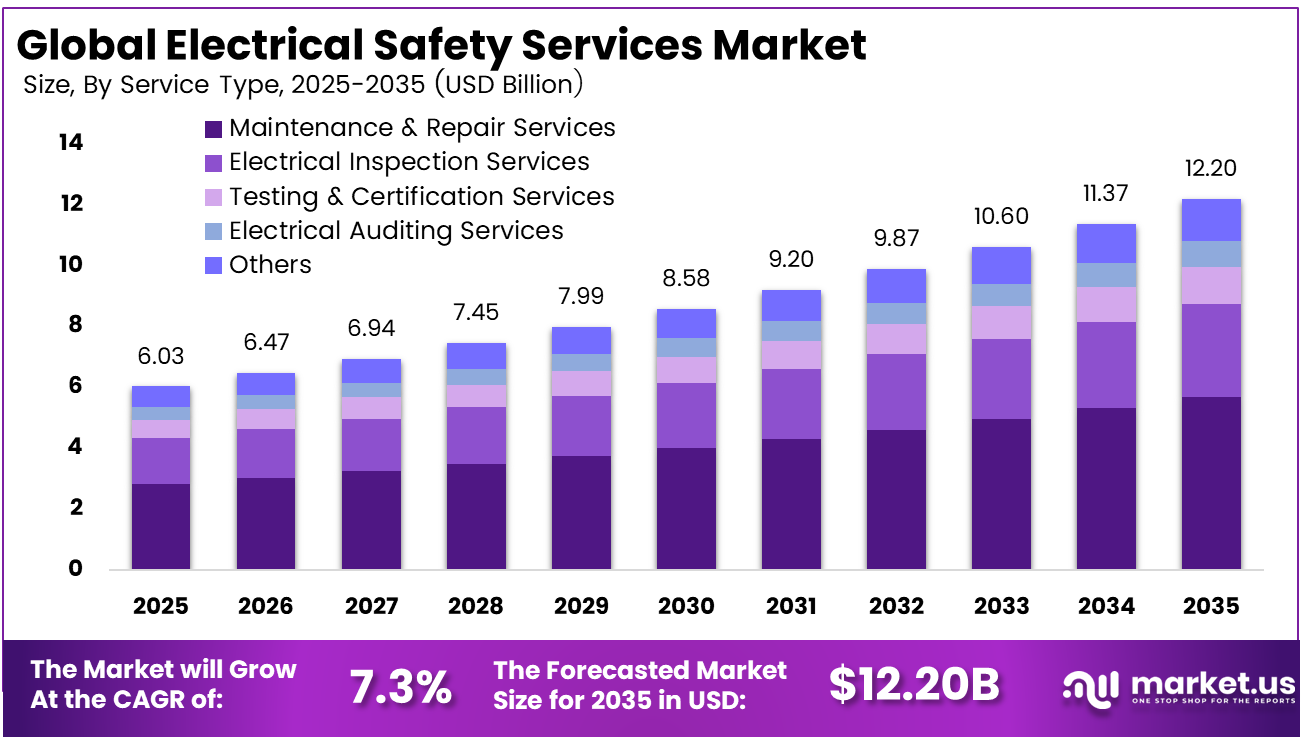

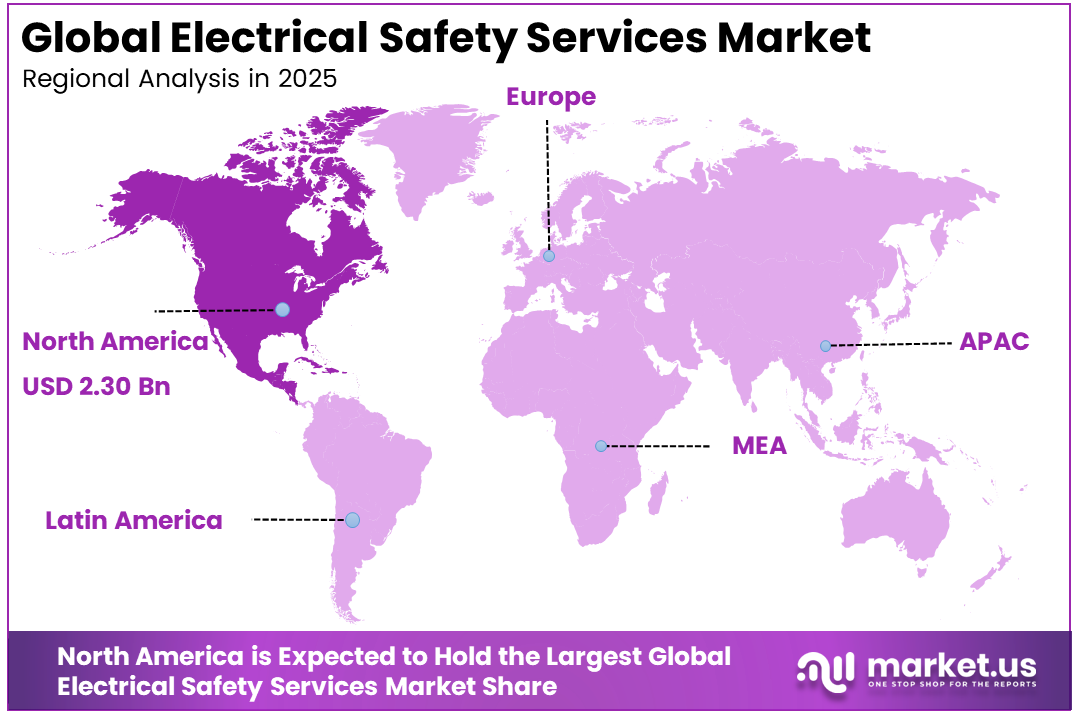

The Global Electrical Safety Services Market size is expected to be worth around USD 12.20 billion by 2035, from USD 6.03 billion in 2025, growing at a CAGR of 7.3% during the forecast period from 2025 to 2035. North America held a dominant market position, capturing more than a 38.2% share, holding USD 2.30 billion in revenue.

Electrical Safety Services refers to the inspection, testing, maintenance, and repair activities used to keep electrical systems safe and reliable. These services help identify faults, prevent accidents, reduce fire risks, and improve system performance. They are widely used across industrial, commercial, and residential settings to support safe and uninterrupted operations.

Rising industrialization and urban growth are increasing the need for reliable power systems across factories and commercial spaces. Studies show that poor electrical setups contribute to nearly 30% of industrial fires worldwide. Complex networks handling higher loads require regular inspection, while rising awareness of shock hazards after major incidents is making electrical safety a core priority for businesses.

The market for Electrical Safety Services is driven by stricter workplace safety rules, rising awareness of electrical hazards, and the growing need to prevent costly equipment failures. Businesses are investing in regular inspections, maintenance, and testing to keep operations safe and uninterrupted. Expansion of industrial facilities, commercial buildings, and energy-intensive systems is also increasing demand for reliable electrical safety support services.

Demand is rising steadily as businesses expand operations and connect more equipment, increasing pressure on existing electrical systems. Reports indicate that electrical faults account for about 25% of workplace injuries in manufacturing sectors. Aging infrastructure in residential buildings also drives service needs, as hidden wiring issues accumulate over time and prompt homeowners to seek regular inspections.

For instance, in January 2026, Schneider Electric launched its next-gen EcoStruxure Safety platform with AI-powered arc flash detection for North American data centers. This move reinforces their leadership in electrical safety services by integrating predictive analytics that cuts response times by 40%, helping industrial clients meet the latest NFPA 70E standards while preventing costly downtime.

Key Takeaway

- In 2025, the Maintenance & Repair Services segment held a dominant market position, capturing a 46.7% share of the Global Electrical Safety Services Market.

- In 2025, the Infrared Thermography segment held a dominant market position, capturing a 35.3% share of the Global Electrical Safety Services Market.

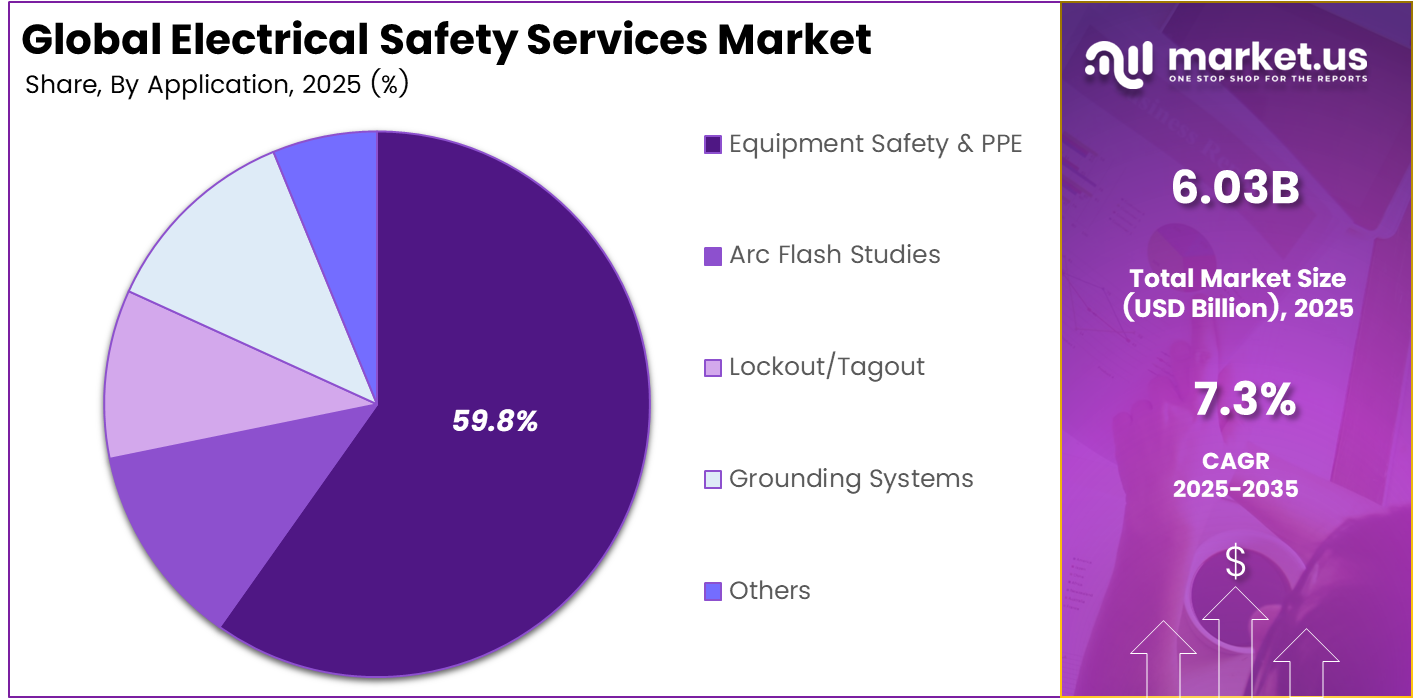

- In 2025, the Equipment Safety & PPE segment held a dominant market position, capturing a 59.8% share of the Global Electrical Safety Services Market.

- In 2025, the Industrial Manufacturing segment held a dominant market position, capturing a 43.5% share of the Global Electrical Safety Services Market.

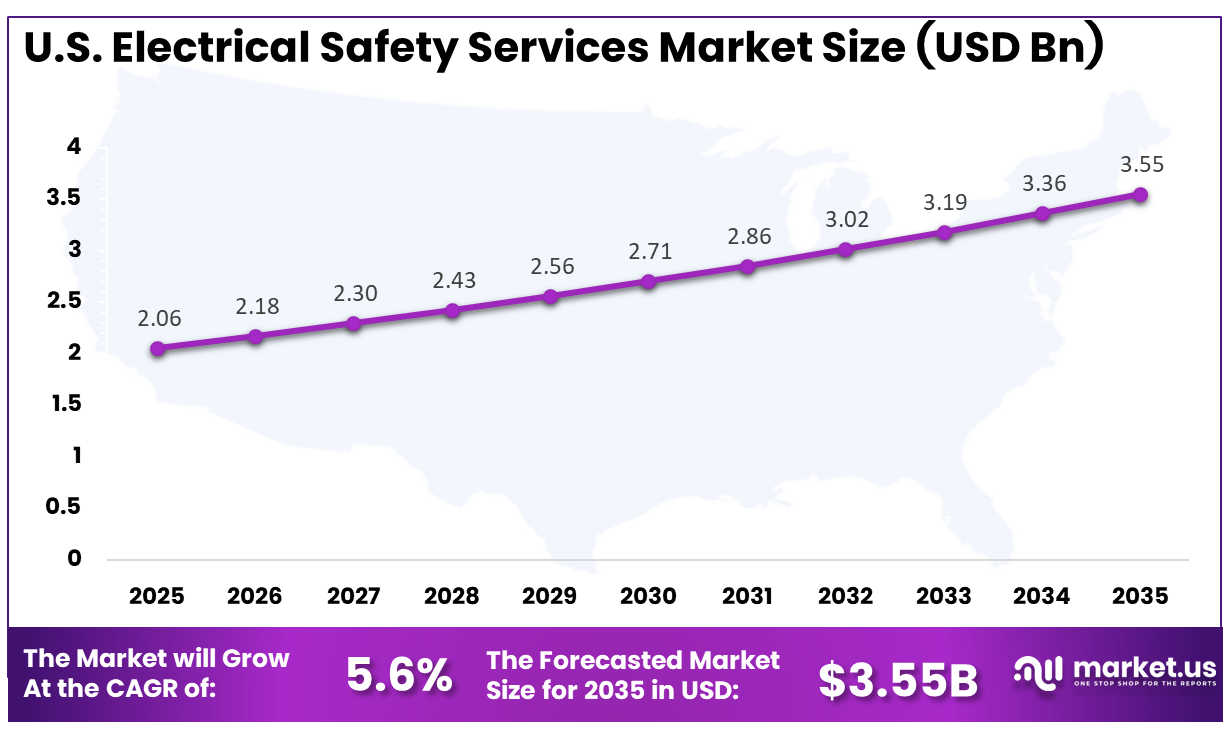

- The U.S. Electrical Safety Services Market was valued at USD 2.06 Billion in 2025, with a robust CAGR of 5.6%.

- In 2025, North America held a dominant market position in the Global Electrical Safety Services Market, capturing more than a 38.2% share.

Role of Generative AI

Generative AI is reshaping electrical safety by creating realistic training simulations based on actual site data. Teams can practice rare risks like arc flashes in virtual environments, cutting training time by 30% while improving learning retention. This makes workforce preparation more practical, efficient, and aligned with real operational challenges.

It also analyzes sensor data to generate predictive insights, helping detect equipment issues before failure. Early adopters have reported a 25% drop in unplanned downtime, as maintenance becomes more proactive. This shift reduces uncertainty in safety checks and supports better planning across industrial and commercial electrical systems.

Investment and Business Benefits

Investment opportunities are growing in training electricians with digital diagnostic skills to meet evolving industry needs. Companies are also investing in portable and user-friendly testing equipment for on-site inspections, especially in remote areas. Long-term maintenance contracts in expanding industrial zones provide stable revenue streams and help firms build consistent client relationships.

Businesses benefit from improved operational efficiency as regular electrical checks reduce unexpected breakdowns and downtime. Maintaining strong safety standards can lower insurance costs by 20-30%, offering financial advantages. A safer working environment also boosts employee confidence, improves morale, and reduces staff turnover, particularly in industries where electrical risks are a major concern.

Regional Analysis

In 2025, North America held a dominant market position in the Global Electrical Safety Services Market, capturing more than a 38.2% share, holding USD 2.30 billion in revenue. This dominance is due to strict workplace safety standards, strong industrial and commercial infrastructure, and high awareness of electrical risk prevention. The region also benefits from regular inspection practices, aging power systems that need upgrades, and rising investment in automation, data centers, and energy-intensive facilities requiring reliable electrical safety support.

For instance, in November 2025, Rockwell Automation launched enhanced safety protocols integrated into its PlantPAx system, featuring AI-driven hazard detection for industrial environments. This innovation strengthens North America’s dominance by providing cutting-edge electrical safety solutions for automated manufacturing facilities nationwide.

U.S. Electrical Safety Services Market Size

The market for Electrical Safety Services within the U.S. is growing tremendously and is currently valued at USD 2.06 billion. The market has a projected CAGR of 5.6%. This growth is driven by strict safety regulations, aging electrical infrastructure, and rising industrial automation across sectors. Increasing workplace safety awareness and frequent electrical inspections in commercial and manufacturing facilities are also supporting demand. Additionally, expansion of data centers and energy-intensive operations is pushing organizations to invest in regular testing, monitoring, and preventive maintenance services.

For instance, in February 2025, Honeywell International Inc. announced a major portfolio restructuring to separate its Automation and Aerospace Technologies businesses. This strategic move enhances focus on industrial automation safety solutions, reinforcing U.S. leadership in electrical safety services through advanced predictive maintenance and real-time monitoring technologies across North American manufacturing sectors.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Service Type Analysis

In 2025, the Maintenance & Repair Services segment held a dominant market position, capturing a 46.7% share of the Global Electrical Safety Services Market. This dominance is due to the essential role of regular upkeep in keeping electrical systems safe and dependable. Businesses depend on maintenance and repair services to prevent sudden failures, reduce safety risks, and keep operations running without disruption. These services also help extend asset life and improve day-to-day system performance.

Routine servicing is widely preferred because it supports compliance, lowers the chance of costly breakdowns, and improves workplace safety. Industrial sites, commercial facilities, and public infrastructure all need continuous monitoring and timely repairs. This makes maintenance and repair services a practical choice for organizations focused on reliability and long-term efficiency.

For Instance, in January 2026, Schneider Electric rolled out new field service protocols for electrical systems in industrial sites. Contractors now get hands-on training to spot wear in panels and wiring during routine visits. This keeps operations steady by fixing issues before they halt production lines, a real help for plants running nonstop.

Technology Analysis

In 2025, the Infrared Thermography segment held a dominant market position, capturing a 35.3% share of the Global Electrical Safety Services Market. This dominance is due to the growing need for non-contact inspection methods that can detect hidden electrical faults early. Infrared thermography helps identify overheating parts, loose connections, and abnormal heat patterns without shutting down equipment. This makes it highly useful for facilities that need safe inspections while maintaining normal operations.

The technology is also valued for supporting preventive maintenance and reducing the risk of fire or equipment damage. It gives teams a clear picture of system health before a visible failure occurs. As companies focus more on early fault detection, infrared thermography continues to gain wider acceptance across industries.

For instance, in March 2026, Siemens AG integrated thermal imaging into its automation tools for factories. Technicians use these cameras to scan live equipment, catching heat buildups without shutdowns. This boosts early detection in busy plants, making safety scans faster and more routine.

Application Analysis

In 2025, the Equipment Safety & PPE segment held a dominant market position, capturing a 59.8% share of the Global Electrical Safety Services Market. This dominance is due to the strong focus on protecting workers from electrical hazards in high-risk environments. Companies are giving more attention to equipment safety and personal protective equipment to reduce exposure to shocks, burns, and arc flash incidents. Worker protection remains a top concern in daily operational planning.

The segment also benefits from stricter safety standards and rising awareness of workplace risk management. Employers are investing in protective gear, safety checks, and training to create safer conditions for staff. This area remains important because it directly supports compliance, workforce confidence, and the prevention of serious on-site accidents.

For Instance, in December 2025, Honeywell International Inc. introduced arc-rated gloves and suits for high-voltage work. These gear pieces withstand flashes while staying flexible for daily use. Workers in risky zones appreciate the comfort, which encourages proper wear during tests and repairs.

End-Use Industry Analysis

In 2025, the Industrial Manufacturing segment held a dominant market position, capturing a 43.5% share of the Global Electrical Safety Services Market. This dominance is due to the heavy dependence of manufacturing facilities on complex electrical systems and continuous machine operation. Production sites require stable power flow, safe wiring conditions, and regular inspections to avoid unplanned stoppages. Any electrical issue can quickly affect output, worker safety, and the efficiency of the overall process.

Industrial manufacturing also faces constant pressure to maintain uptime while meeting strict safety requirements. Electrical safety services help plants reduce risks, support reliable equipment use, and improve maintenance planning. As factories become more automated and energy-intensive, the need for dependable electrical safety support continues to grow steadily.

For Instance, in March 2026, Rockwell Automation shared insights on securing factory networks against electrical glitches. Their approach hardens controls around motors and lines, vital for assembly floors. Manufacturers adopt it to keep output smooth while meeting compliance needs.

Key Market Segments

By Service Type

- Electrical Inspection Services

- Testing & Certification Services

- Electrical Auditing Services

- Maintenance & Repair Services

- Others

By Technology

- Infrared Thermography

- Partial Discharge Detection

- Circuit Analysis

- Electrical Safety Training

- Others

By Application

- Equipment Safety & PPE

- Arc Flash Studies

- Lockout/Tagout

- Grounding Systems

- Others

By End-Use Industry

- Industrial Manufacturing

- Construction & Infrastructure

- Commercial Buildings

- Residential

- Others

Emerging trends

Real-time monitoring tools, such as wearable detectors, are transforming how workers handle electrical risks. These devices provide instant alerts for voltage exposure, replacing traditional periodic inspections. Adoption has increased by 40% in high-risk environments over the past two years, showing strong industry movement toward continuous safety monitoring.

Smart PPE with embedded sensors is gaining traction, tracking current flow and vibrations to prevent accidents before they occur. Early trials show a 35% reduction in on-site incidents, highlighting their effectiveness. This trend reflects a growing focus on combining safety gear with intelligent technology for better worker protection.

Growth Factors

Stricter safety regulations worldwide are pushing companies to adopt certified electrical safety services. Regions with consistent compliance practices have seen violations drop by 25%, reducing operational risks. These measures not only improve safety standards but also help companies avoid costly downtime, legal issues, and financial penalties.

Increasing accident rates in construction and industrial sectors are further driving demand for safety solutions. Greater awareness after workplace incidents is encouraging firms to invest in training and preventive services. Surveys indicate that structured safety programs have improved worker confidence by 35%, strengthening overall productivity and workplace reliability.

Market Dynamics

Drivers - Stricter Safety Compliance

Stricter safety compliance is pushing organizations to adopt regular electrical inspections and preventive maintenance practices. Governments and regulatory bodies are focusing more on workplace safety, especially in high-risk industries. This is encouraging companies to follow structured safety protocols and ensure their electrical systems meet required standards at all times.

Businesses are also becoming more proactive in avoiding accidents, downtime, and legal issues linked to electrical failures. Regular audits and testing help reduce risks and improve system reliability. As safety becomes a core operational priority, demand for electrical safety services continues to strengthen across industrial, commercial, and institutional sectors.

For instance, in September 2025, Schneider Electric rolled out fresh training sessions for contractors at the NECA show, zeroing in on the latest 2026 electrical code changes. They walked folks through practical steps to meet these tougher rules without missing a beat. It’s the kind of hands-on help that keeps sites running safe and smooth, easing worries for teams on the ground.

Restraint - High Service Complexity

High service complexity remains a challenge as modern electrical systems are becoming more advanced and interconnected. Facilities often operate a mix of old and new technologies, which makes inspection and maintenance more difficult. Technicians must understand multiple system layers, increasing the time and effort required for proper safety checks.

In addition, many operations cannot afford long shutdown periods for maintenance activities. This creates pressure to perform inspections without disrupting workflows. The need for specialized skills and careful planning makes service execution more demanding, limiting how quickly providers can scale operations or handle large volumes of projects.

For instance, in April 2025, Rockwell Automation showed off its new ControlLogix system at SPS, tackling the mess of old and new wiring in plants. It pulls everything into one platform, so techs spend less time untangling issues. For shops with layered setups, this feels like a breath of fresh air amid growing system headaches.

Opportunities - Predictive Monitoring Adoption

Predictive monitoring is creating strong opportunities by allowing businesses to detect electrical issues before they turn into major failures. With the help of sensors and data analysis, companies can track equipment performance in real time. This approach supports smarter maintenance decisions and reduces unexpected breakdowns across critical systems.

Organizations are increasingly interested in moving from reactive repairs to planned maintenance strategies. Predictive tools help improve efficiency, extend equipment life, and reduce operational risks. This shift is opening new service models where providers offer continuous monitoring and long-term support instead of only periodic inspections.

For instance, in August 2025, Siemens AG brought edge AI sensors to factories, watching motors and lines for early warning signs like odd heat or vibes. The system tweaks settings on its own to head off breakdowns, saving hours of downtime. Managers love how it turns data into action without needing a PhD to follow along.

Challenges - Skilled Workforce Shortage

The shortage of skilled workers is a major challenge for the electrical safety services market. Electrical work requires proper training, certifications, and hands-on experience, which takes time to develop. Many experienced professionals are nearing retirement, while fewer new workers are entering the field to replace them.

This gap makes it difficult for service providers to meet growing demand and maintain consistent service quality. Projects may face delays due to the limited availability of qualified technicians. Companies also need to invest more in training programs, which adds to operational costs and slows down workforce expansion efforts.

For instance, in March 2026, Honeywell International Inc. teamed up with IIT Bombay on a center to train thousands in green tech skills by 2030, eyeing the gap in electrical know-how. With industries short on hands for safety checks, this pushes fresh talent into the mix. It’s a smart play to keep pace as demand outstrips supply.

Key Players Analysis

One of the leading players in February 2026, Siemens AG partnered with U.S. utility giants to roll out advanced electrical safety auditing programs across 25 states. Their new digital twin technology simulates fault scenarios in real-time, giving facility managers unprecedented visibility into risks and slashing compliance audit times by 30%.

Top Key Players in the Market

- Schneider Electric

- Siemens AG

- Honeywell International Inc.

- Rockwell Automation

- ABB Ltd.

- Emerson Electric Co.

- Eaton Corporation

- UL LLC

- Bureau Veritas

- Intertek Group plc

- CSA Group

- TUV Rheinland

- DEKRA SE

- Exida

- Phoenix Contact GmbH & Co. KG

- R&M Technologies

- Others

Recent Developments

- In January 2026, Bureau Veritas expanded its U.S. electrical safety division with 12 new regional labs, focusing on EV charging infrastructure certification. This $25M investment addresses the infrastructure bill’s safety mandates, positioning BV as the preferred inspector for America’s electrification push.

- In December 2025, Eaton Corporation launched its Brightlayer Safety Hub for commercial buildings, featuring IoT-enabled circuit monitoring that predicts failures 72 hours in advance. Deployed across 500 U.S. properties already, this platform cuts electrical fire risks by 45% and sets new benchmarks for predictive maintenance.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 6.03 Billion |

| Forecast Revenue (2035) | USD 12.20 Billion |

| CAGR (2026-2035) | 7.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Service Type (Electrical Inspection Services, Testing & Certification Services, Electrical Auditing Services, Maintenance & Repair Services, Others), By Technology (Infrared Thermography, Partial Discharge Detection, Circuit Analysis, Electrical Safety Training, Others), By Application (Equipment Safety & PPE, Arc Flash Studies, Lockout/Tagout, Grounding Systems, Others), By End-Use Industry (Industrial Manufacturing, Construction & Infrastructure, Commercial Buildings, Residential, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Schneider Electric, Siemens AG, Honeywell International Inc., Rockwell Automation, ABB Ltd., Emerson Electric Co., Eaton Corporation, UL LLC, Bureau Veritas, Intertek Group plc, CSA Group, TUV Rheinland, DEKRA SE, Exida, Phoenix Contact GmbH & Co. KG, R&M Technologies, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |