Global Educational Publishing Market Size, Share and Analysis Report By Content Type (K-12 Textbooks & Courseware, Higher Education Textbooks & Academic Titles, Test Preparation & Assessment Materials, Digital & Interactive Content (eBooks, LMS modules), Others), By Format (Print, Digital), By End-User (K-12 Schools & Districts, Higher Education Institutions, Students & Individual Learners, Corporate Training, Others), By Subject Area (STEM (Science, Technology, Engineering, Math), Humanities & Social Sciences, Language Learning, Professional & Vocational, Others), By Distribution Channel (Direct Sales to Institutions, Retail & Online Bookstores, Bulk Licensing & Subscriptions), By Regional Analysis, Global Trends and Opportunity, Future Outlook By 2025-2035

- Published date: Feb. 2026

- Report ID: 178886

- Number of Pages: 370

- Format:

-

keyboard_arrow_up

Quick Navigation

- Educational Publishing Market size

- Top Market Takeaways

- Report Overview

- By Content Type

- By Format

- By End User

- By Subject Area

- By Distribution Channel

- Regional Analysis

- Increasing Adoption Technologies

- Investment Opportunities

- Key Market Segments

- Emerging Trends Analysis

- Driver Analysis

- Restraint Analysis

- Opportunity Analysis

- Challenge Analysis

- Key Company Analysis

- Recent Developments

- Report Scope

Educational Publishing Market size

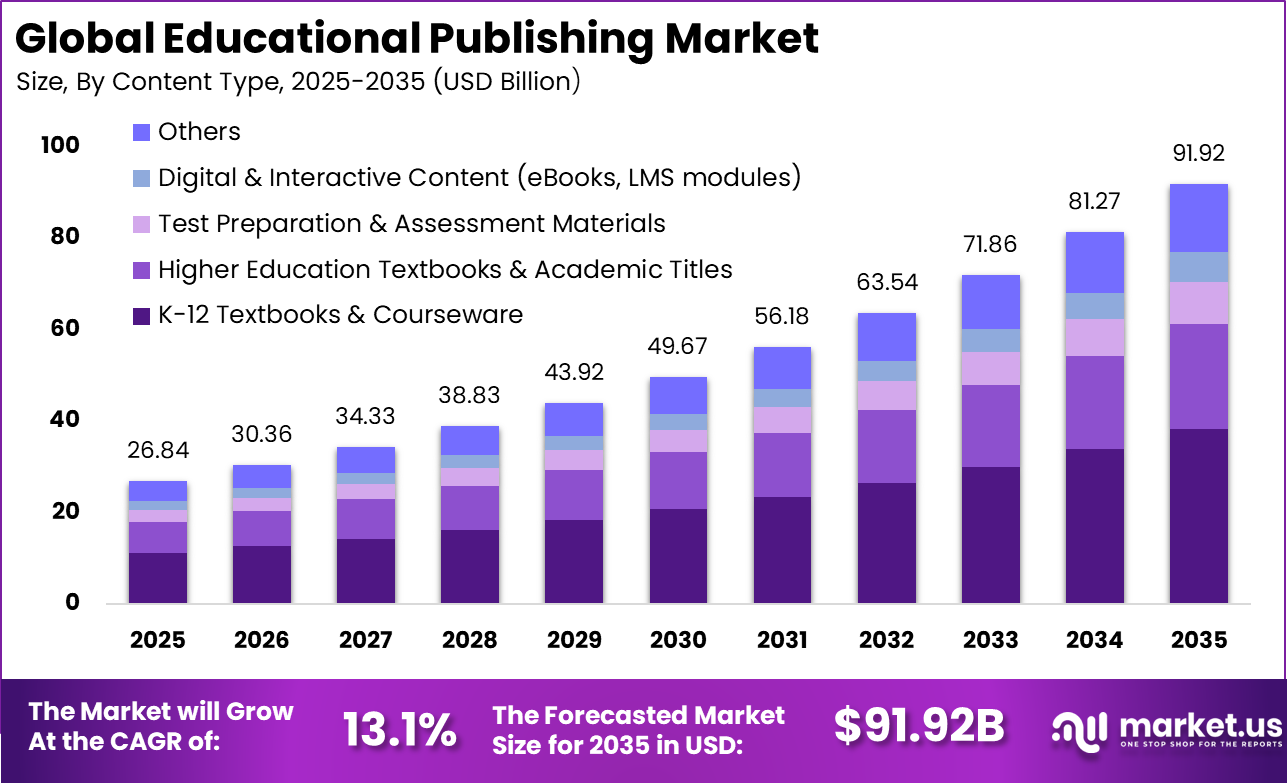

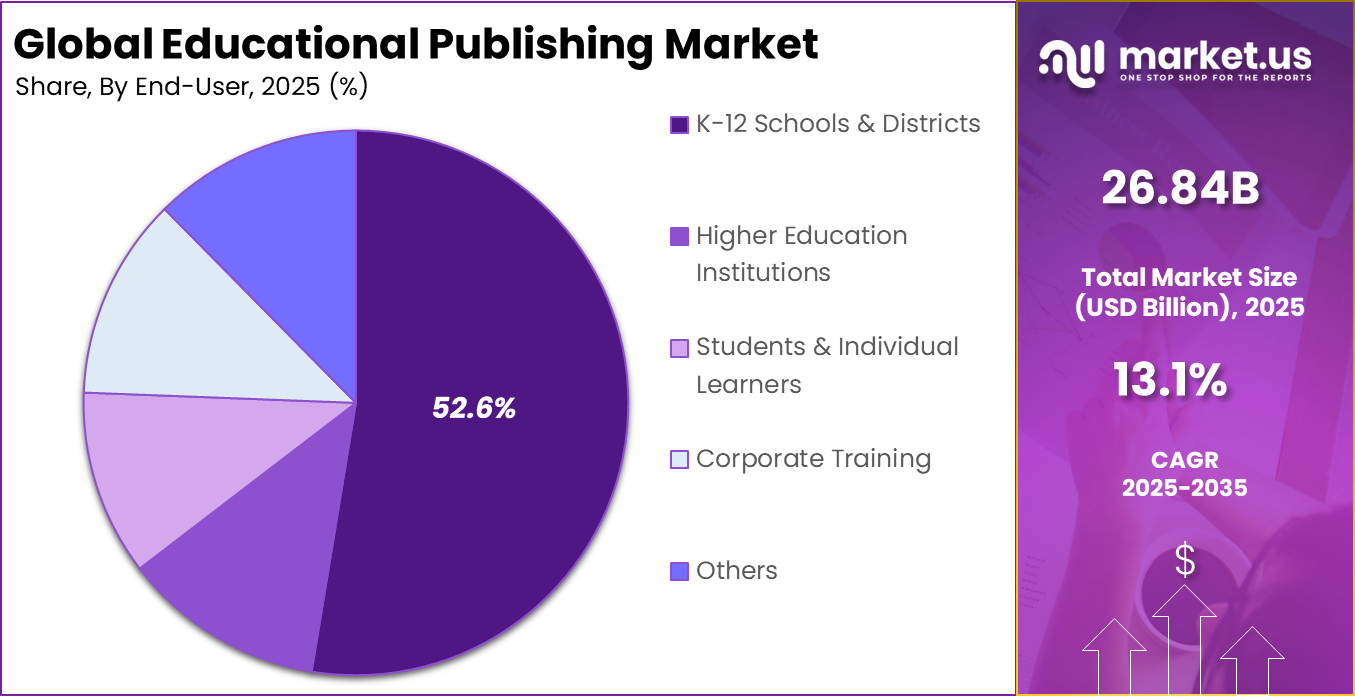

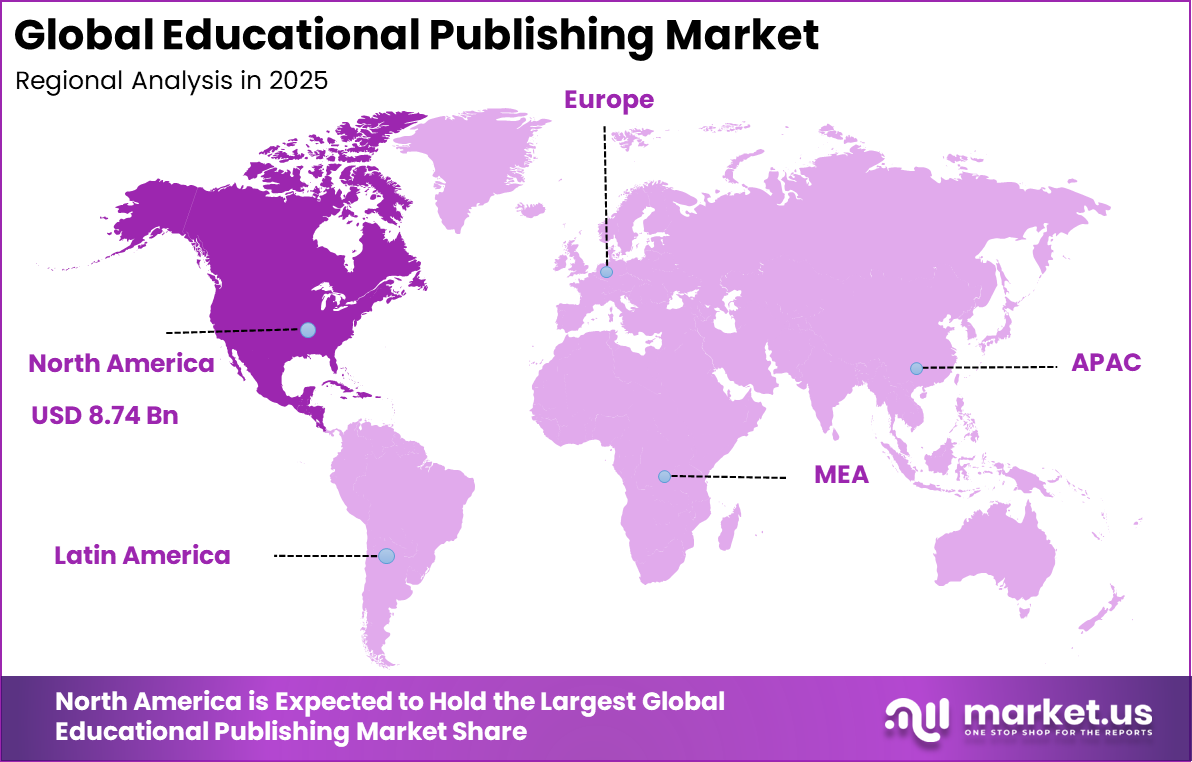

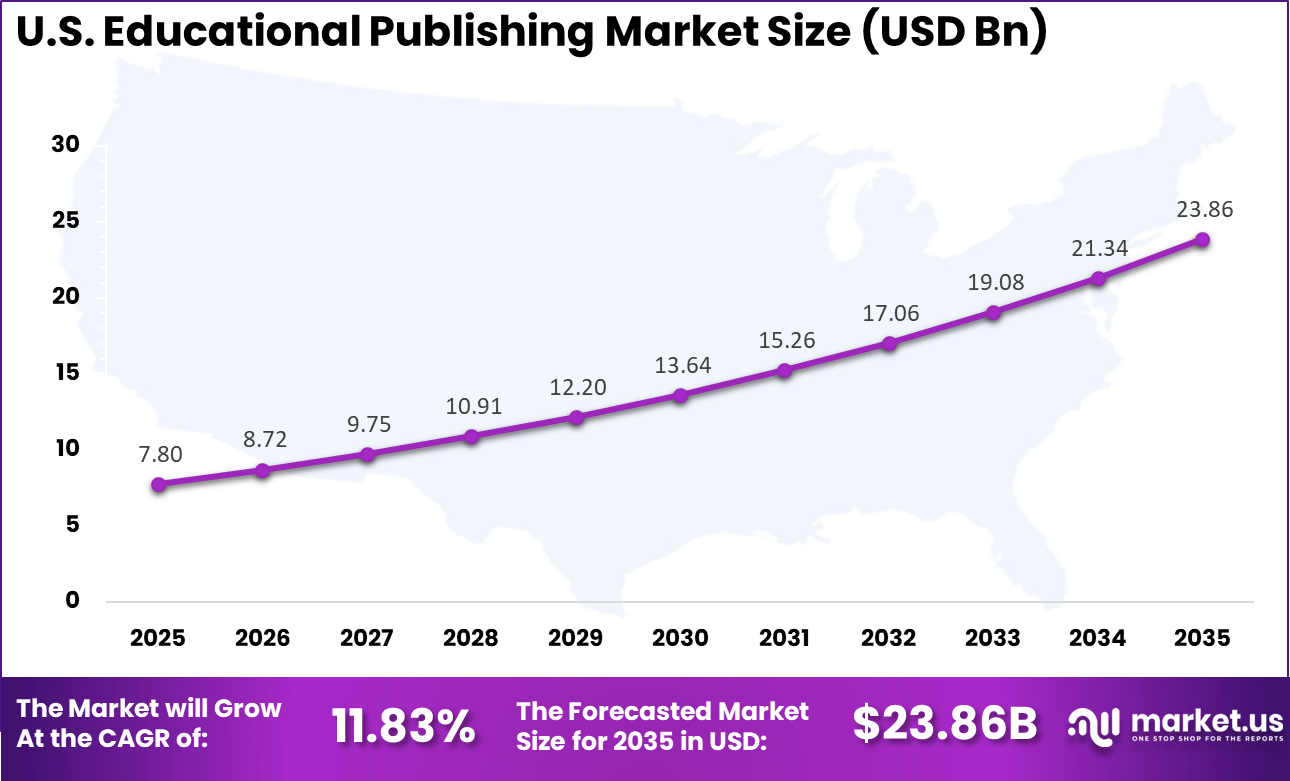

The Global Educational Publishing Market size is expected to be worth around USD 91.92 billion by 2035, from USD 26.84 billion in 2025, growing at a CAGR of 13.1% during the forecast period from 2025 to 2035. North America held a dominant market position, capturing more than a 32.6% share, holding USD 8.74 billion in revenue.

Top Market Takeaways

- K-12 textbooks and courseware accounted for 41.7% of the Educational Publishing market, supported by continuous curriculum updates and standardized learning frameworks.

- Digital formats led with 58.3% share, reflecting strong adoption of e-books, interactive content, and learning management system integration.

- K-12 schools and districts represented 52.6% of total demand, driven by institutional procurement and government-supported education programs.

- STEM subjects held 47.3% share, as science, technology, engineering, and mathematics remain priority areas in national education strategies.

- Direct sales to institutions dominated distribution with 64.8%, enabling publishers to secure long-term contracts and curriculum alignment.

- North America captured 32.6% of the market, with the United States generating USD 7.80 billion in revenue and expanding at a 11.83% CAGR, supported by digital learning investments and curriculum modernization initiatives.

Report Overview

The education publishing market has undergone structural transformation as digital learning environments expand across schools, colleges, and professional institutions. Traditional print publishing remains relevant, yet digital platforms, subscription models, and integrated courseware ecosystems are redefining content delivery. Institutions increasingly demand curriculum aligned materials that combine textbooks, assessments, analytics, and multimedia resources within unified platforms.

Content providers are adapting to changing teaching models where hybrid and remote learning remain embedded in academic systems. Interactive modules, adaptive learning engines, and cloud based content libraries are becoming part of standard instructional frameworks. As learning outcomes and measurable performance indicators gain priority, publishers are focusing on analytics driven tools that support both educators and students.

As of 2024, more than 60% of educational institutions globally have integrated digital content into teaching and learning processes. In the United States, 87% of K 12 school districts use digital resources to support individualized instruction, and 94% of public schools provide students with internet connected devices. This reflects widespread digital infrastructure development across primary and secondary education systems.

Despite high availability, 54% of students report challenges when studying from digital materials, and 67.9% indicate a preference for printed copies for note taking. At the institutional level, more than 70% have adopted Open Educational Resources to some extent, with annual usage increasing by 15% due to cost advantages. Classroom adoption of AI based tools rose from 20% in 2023 to 31% in 2024 in several regions, reflecting steady integration of intelligent learning technologies.

By Content Type

K 12 textbooks and courseware represent 41.7% of market share due to structured curriculum requirements and recurring academic cycles. School districts rely on standardized materials aligned with national and regional learning benchmarks. This segment benefits from predictable procurement schedules and large volume adoption across grade levels.

Curriculum alignment plays a central role in content selection. Educational authorities prioritize resources that meet defined academic outcomes and testing standards. As accountability frameworks strengthen, demand for comprehensive K 12 courseware packages continues to rise.

Digital supplements are increasingly bundled with printed textbooks in this segment. Interactive exercises, teacher dashboards, and assessment analytics enhance the overall value proposition. This integration supports blended learning strategies adopted by many institutions.

By Format

Digital format accounts for 58.3% of market adoption as institutions move toward flexible content delivery. Cloud based platforms allow students to access materials across devices without physical constraints. Subscription models also enable periodic updates without reprinting costs.

Digital resources offer performance tracking capabilities that print cannot provide. Teachers can monitor engagement levels, quiz performance, and assignment completion in real time. This data driven approach strengthens instructional planning.

Cost efficiency is another factor driving digital growth. Although initial licensing may require investment, long term operational savings are often realized through reduced distribution and inventory management expenses. Institutions are increasingly evaluating total lifecycle cost rather than upfront price.

By End User

K 12 schools and districts represent 52.6% of adoption because public education systems manage large student populations. Centralized procurement allows districts to negotiate multi year agreements and standardized content deployment. This scale ensures consistent curriculum delivery across schools.

Institutional accountability further strengthens demand. Schools must demonstrate measurable improvement in literacy, mathematics, and science outcomes. Integrated educational content with built in assessment tools supports this requirement.

Professional development for teachers also influences purchasing decisions. Content platforms often include training modules and instructional support resources. These features improve classroom implementation and long term engagement.

By Subject Area

STEM subjects account for 47.3% of content demand reflecting global emphasis on science, technology, engineering, and mathematics education. Governments and institutions prioritize these areas to strengthen workforce readiness and innovation capacity. Curriculum frameworks increasingly allocate greater instructional time to STEM disciplines.

Digital platforms enhance STEM learning through simulations and virtual laboratories. Interactive experiments and real time problem solving tools improve comprehension beyond traditional textbook methods. This practical learning experience drives sustained adoption.

Growing interest in coding, robotics, and applied sciences at early grade levels also contributes to expansion. Publishers are developing age appropriate STEM content to address emerging educational priorities. This sustained focus is expected to maintain segment leadership.

By Distribution Channel

Direct sales to institutions represent 64.8% of distribution because academic procurement is largely centralized. Schools and universities prefer structured agreements that include licensing, support services, and renewal terms. Direct engagement also allows customization according to curriculum needs.

Institutional sales models often involve long term contracts tied to academic cycles. This structure provides predictable revenue streams and stable content deployment. It also enables publishers to build strategic relationships with education authorities.

Digital platforms have strengthened direct distribution channels. Vendors can provide onboarding support, analytics dashboards, and periodic updates directly to institutions. This reduces reliance on intermediaries and strengthens service continuity.

Regional Analysis

North America holds 32.6% of the education publishing market due to advanced educational infrastructure and widespread digital adoption. Schools in the region have integrated technology into classroom instruction at scale. Federal and state level funding initiatives further support digital transformation.

The United States drives regional expansion with a CAGR of 11.83%, supported by curriculum reforms and technology investment in public education systems. Large school districts and higher education institutions adopt digital content platforms for blended learning models. Demand remains steady as institutions modernize assessment frameworks and improve student performance measurement systems.

Increasing Adoption Technologies

Digital learning platforms are increasingly adopted within the Educational Publishing Market due to their ability to deliver interactive content and track learner progress. These platforms support features such as multimedia content, interactive activities, and analytics that inform instructional adjustments. Cloud based delivery enhances accessibility and ensures that learners and educators can access resources from any location, reducing barriers to participation.

Artificial intelligence and adaptive learning technologies are also being integrated into educational content to personalise learning experiences. These technologies analyse learner performance data to adjust content difficulty, sequence learning activities, and recommend targeted resources. Adaptive capabilities increase learner engagement and support differentiated instruction. Mobile applications and analytics tools further enhance accessibility and provide educators with insights into student performance trends.

Organizations and educators adopt educational publishing solutions to improve instructional effectiveness and support learning outcomes. Structured content that aligns with curriculum standards provides consistent guidance for educators and ensures that learners receive comprehensive coverage of key concepts. Digital resources enhance this impact by offering dynamic, interactive experiences that support diverse learning styles.

Investment Opportunities

Investment opportunities in the Educational Publishing Market include development of adaptive learning platforms that leverage data analytics to personalise learner pathways. These platforms can improve instructional effectiveness and provide educators with actionable insights into performance trends.

Solutions that integrate multimedia, assessments, and feedback mechanisms will strengthen learner engagement and support differentiated instruction. There are also opportunities in cloud based and mobile enabled content delivery systems that improve accessibility across diverse learning environments. Investments in content authoring tools, curriculum alignment frameworks, and interoperability with learning management systems can further enhance value for institutions.

Services that support implementation, training, and content customisation can increase adoption and long term engagement. As education continues to embrace digital transformation, focused investments in scalable, adaptive, and accessible publishing solutions will shape future market growth.

Key Market Segments

By Content Type

- K-12 Textbooks & Courseware

- Higher Education Textbooks & Academic Titles

- Test Preparation & Assessment Materials

- Digital & Interactive Content (eBooks, LMS modules)

- Others

By Format

- Digital

By End-User

- K-12 Schools & Districts

- Higher Education Institutions

- Students & Individual Learners

- Corporate Training

- Others

By Subject Area

- STEM (Science, Technology, Engineering, Math)

- Humanities & Social Sciences

- Language Learning

- Professional & Vocational

- Others

By Distribution Channel

- Direct Sales to Institutions

- Retail & Online Bookstores

- Bulk Licensing & Subscriptions

Regional Analysis and Coverage

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of Latin America

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Emerging Trends Analysis

One clear trend in the education publishing market is the rapid expansion of adaptive learning technologies. Digital platforms are increasingly incorporating analytics engines that adjust content difficulty based on student performance. This allows educators to personalize instruction without redesigning the curriculum for each learner. As performance data becomes central to academic planning, adaptive tools are gaining strong institutional acceptance.

Another visible trend is the integration of multimedia and interactive simulations within core courseware. Especially in STEM subjects, virtual laboratories and scenario based modules enhance comprehension beyond static text. Institutions are prioritizing platforms that combine textbook content with video, quizzes, and progress tracking. This blended content model reflects a broader transition toward digital first instructional design.

Driver Analysis

A primary driver of the market is the continued focus on measurable learning outcomes. Schools and districts are under pressure to demonstrate improvement in standardized testing and academic performance indicators. Integrated courseware platforms provide assessment tracking and analytics that support data based instructional decisions. This accountability environment strengthens demand for structured, technology enabled content solutions.

Another strong driver is increasing digital device penetration among students. Tablets, laptops, and classroom connectivity have become standard across many developed education systems. With infrastructure in place, institutions are shifting from print heavy models toward digital platforms. This transition supports long term modernization of curriculum delivery.

Restraint Analysis

One notable restraint is budget limitation within public education systems. Although digital platforms offer long term efficiency, initial licensing and integration costs can be significant. Many school districts must balance content investment with infrastructure upgrades and teacher training requirements. Financial constraints can delay adoption cycles.

Resistance to change also affects implementation speed. Educators accustomed to traditional textbooks may require training to effectively use digital platforms. Without structured onboarding and technical support, usage rates can remain below expectations. This slows full realization of digital transformation benefits.

Opportunity Analysis

A key opportunity lies in emerging markets where digital education infrastructure is expanding rapidly. As governments invest in connectivity and device distribution, demand for structured digital courseware is expected to increase. Publishers that localize content to regional curriculum standards can strengthen market presence. Early entry into developing education ecosystems may secure long term institutional partnerships.

Another opportunity exists in lifelong and supplemental learning segments. Beyond formal K 12 systems, adult education and skill development programs are expanding. Digital publishing platforms can extend into certification courses, language training, and professional upskilling. This diversification supports broader revenue channels beyond traditional school contracts.

Challenge Analysis

A major challenge in the education publishing market is maintaining content relevance amid evolving curriculum standards. Academic frameworks are frequently updated to reflect new competencies and workforce demands. Publishers must continuously revise materials to align with regulatory and institutional expectations. This requires ongoing editorial investment and close collaboration with education authorities.

Data privacy and cybersecurity also present operational challenges. Digital platforms collect student performance data and personal information. Ensuring secure storage and compliance with regional privacy regulations is essential. Institutions demand strong safeguards to protect learners while maintaining functional analytics capabilities.

Key Company Analysis

The competitive landscape includes established academic publishers and digital learning platform providers such as Pearson plc, McGraw Hill, LLC, Cengage Learning, Inc., and Wiley. These organizations maintain extensive content portfolios across K 12 and higher education segments. Their strength lies in curriculum alignment, assessment integration, and digital platform development.

Other major participants such as Houghton Mifflin Harcourt Company, Oxford University Press, Cambridge University Press, and Springer Nature focus on academic rigor and global distribution networks. Their publishing expertise supports both institutional and professional learning markets.

Digital learning and service oriented providers including Follett Corporation, Chegg, Inc., Barnes & Noble Education, Inc., Scholastic Corporation, Kaplan, Inc., Rosetta Stone, Ltd., and Discovery Education, Inc. contribute to competitive diversity through specialized platforms and supplemental learning tools. Collectively, the market is characterized by curriculum depth, digital integration capability, and long term institutional partnerships.

Top Key Players in the Market

- Pearson, plc

- McGraw Hill, LLC

- Cengage Learning, Inc.

- Wiley

- Houghton Mifflin Harcourt Company

- Oxford University Press

- Cambridge University Press

- Springer Nature

- Follett Corporation

- Chegg, Inc.

- Barnes & Noble Education, Inc.

- Scholastic Corporation

- Kaplan, Inc.

- Rosetta Stone, Ltd.

- Discovery Education, Inc.

- Others

Recent Developments

- December, 2025 – Pearson launched its AI Tutor within Pearson+, an adaptive learning platform integrated across 1,500+ textbooks, delivering personalized study plans and real-time feedback to 15 million students worldwide, boosting completion rates by 28% in pilot programs.

- November, 2025 – McGraw Hill unveiled ALEKS 360 with generative AI for individualized math/science pathways, claiming 35% faster mastery for higher ed users and expanding adaptive assessment reach to 2.3 million students across 1,200 institutions.

- October, 2025 – Cengage rolled out Cengage Unlimited AI Companion, embedding OpenAI-powered writing assistance and concept mapping directly into digital textbooks, serving 7 million subscribers with 22% higher engagement on mobile platforms.

- September, 2025 – Wiley introduced WileyPLUS 8.0 featuring agentic AI that auto-generates practice problems from textbook content and provides step-by-step video explanations, adopted by 650 universities with 41% reduction in DFW rates for STEM courses.

Report Scope

Report Features Description Market Value (2025) USD 26.8 Bn Forecast Revenue (2035) USD 91.9 Bn CAGR(2026-2035) 13.1% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends Segments Covered By Content Type (K-12 Textbooks & Courseware, Higher Education Textbooks & Academic Titles, Test Preparation & Assessment Materials, Digital & Interactive Content (eBooks, LMS modules), Others), By Format (Print, Digital), By End-User (K-12 Schools & Districts, Higher Education Institutions, Students & Individual Learners, Corporate Training, Others), By Subject Area (STEM (Science, Technology, Engineering, Math), Humanities & Social Sciences, Language Learning, Professional & Vocational, Others), By Distribution Channel (Direct Sales to Institutions, Retail & Online Bookstores, Bulk Licensing & Subscriptions) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Pearson, plc, McGraw Hill, LLC, Cengage Learning, Inc., Wiley, Houghton Mifflin Harcourt Company, Oxford University Press, Cambridge University Press, Springer Nature, Follett Corporation, Chegg, Inc., Barnes & Noble Education, Inc., Scholastic Corporation, Kaplan, Inc., Rosetta Stone, Ltd., Discovery Education, Inc., Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Educational Publishing MarketPublished date: Feb. 2026add_shopping_cartBuy Now get_appDownload Sample

Educational Publishing MarketPublished date: Feb. 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Pearson, plc

- McGraw Hill, LLC

- Cengage Learning, Inc.

- Wiley

- Houghton Mifflin Harcourt Company

- Oxford University Press

- Cambridge University Press

- Springer Nature

- Follett Corporation

- Chegg, Inc.

- Barnes & Noble Education, Inc.

- Scholastic Corporation

- Kaplan, Inc.

- Rosetta Stone, Ltd.

- Discovery Education, Inc.

- Others

Our Clients

- 178886

- Feb. 2026