Global Edible Cosmetics Market Size, Share, Growth Analysis By Product (Skin Care, Hair Care, Makeup, Nail Polish), By Distribution Channel (Online, Hypermarkets & Supermarkets, Specialty Stores, Pharmacies & Drugstores), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 182121

- Number of Pages: 248

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

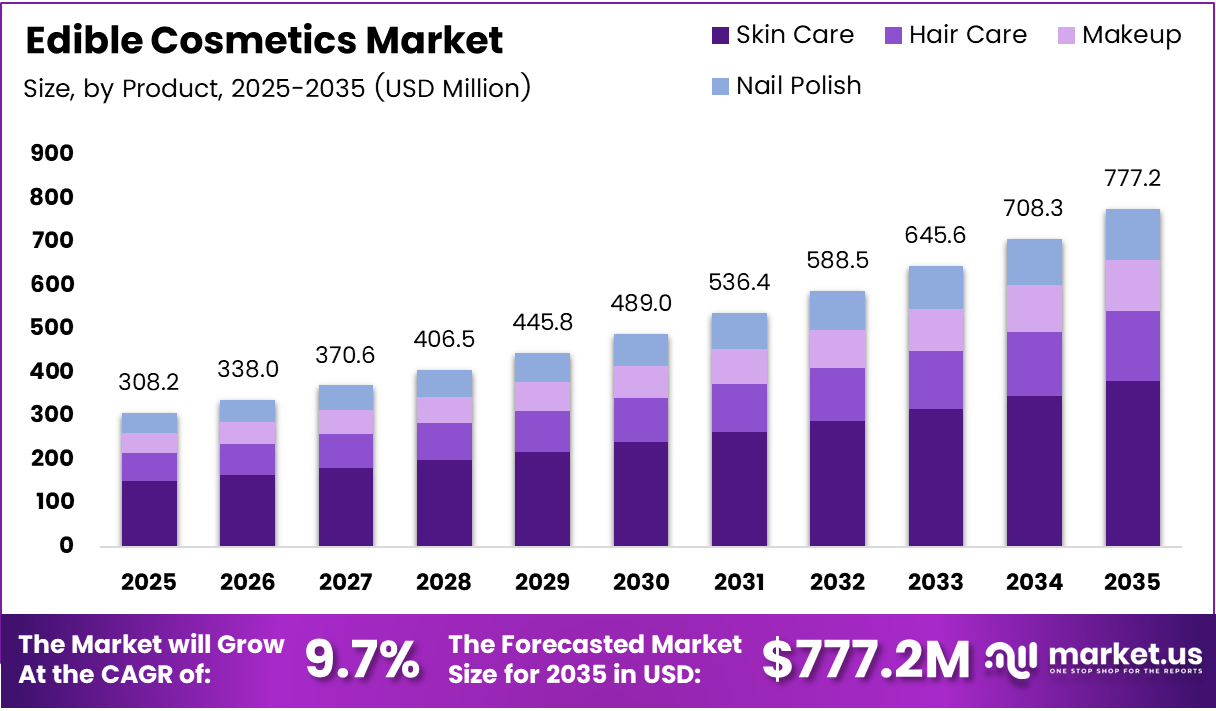

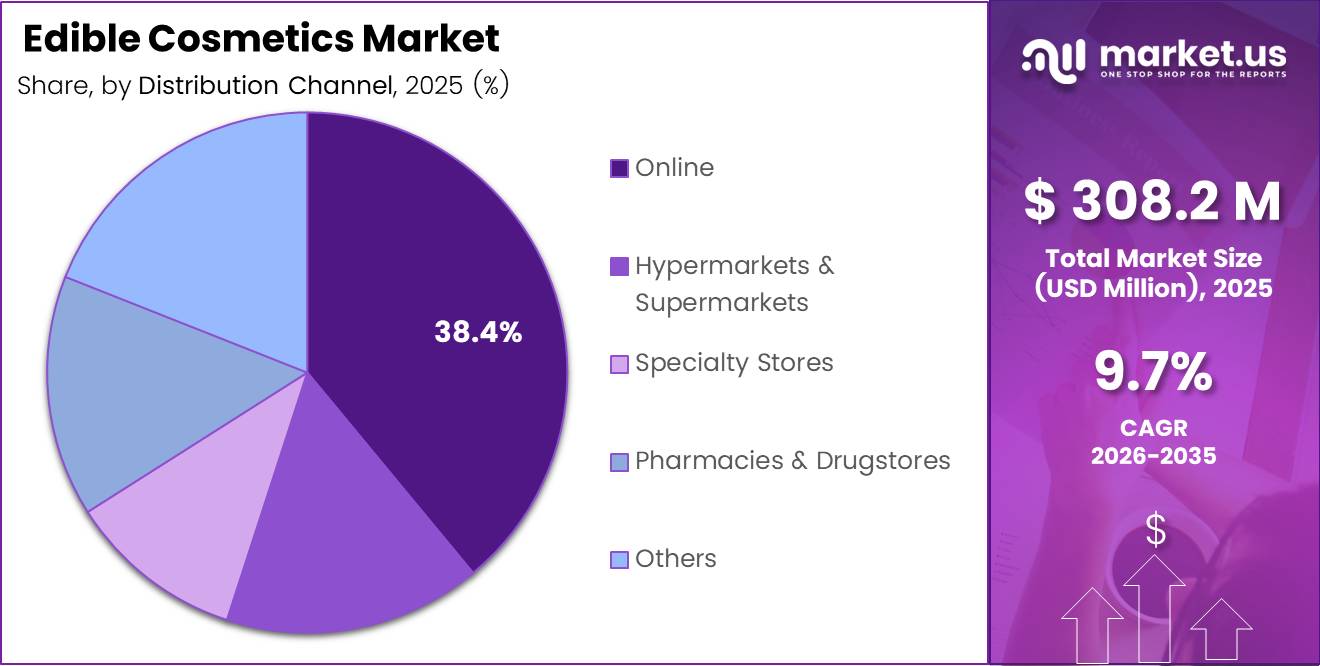

Global Edible Cosmetics Market size is expected to be worth around USD 777.2 Million by 2035 from USD 308.2 Million in 2025, growing at a CAGR of 9.7% during the forecast period 2026 to 2035.

Edible cosmetics are beauty and personal care products formulated with food-grade, non-toxic, and safe-to-consume ingredients. These products span skin care, lip care, hair care, and makeup categories. Consumers choose them because they eliminate exposure to synthetic chemicals that conventional cosmetics often contain.

The market sits at the intersection of two converging forces: the clean beauty movement and the functional food industry. Buyers no longer separate what they put on their bodies from what they put in them. This behavioral shift creates durable demand that goes beyond trend cycles and reflects a structural change in how consumers evaluate beauty products.

Skin care leads product adoption, with lip care serving as the category entry point for most first-time edible cosmetics buyers. Food-grade ingredients such as cocoa butter, honey, plant oils, and herbal extracts form the core of most formulations. These ingredients deliver functional performance while satisfying ingredient transparency requirements that modern consumers now treat as non-negotiable.

Social media platforms have accelerated product discovery in this market at a pace that traditional retail channels cannot replicate. Dessert-inspired and fruit-based formulations generate high visual engagement, driving trial purchases among Gen Z and Millennial consumers. This makes digital distribution channels not just a sales tool but a primary product education mechanism.

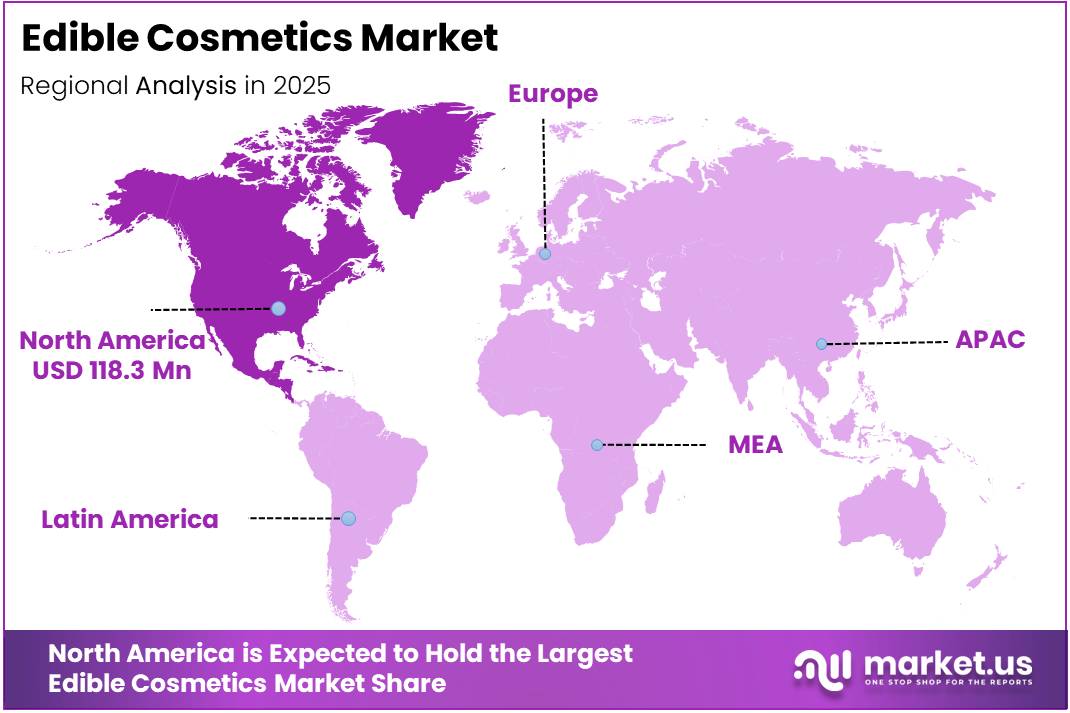

North America holds the largest regional share, accounting for 38.4% of the global market, valued at approximately USD 118.3 Million in the base year. Mature retail infrastructure, high consumer spending on premium beauty, and strong regulatory clarity around cosmetic ingredient labeling all reinforce this leadership position.

According to Enterco Group, 80 new cosmetic ingredients were publicly disclosed globally in the first half of 2025, representing a 73.9% increase compared with 2024. This acceleration in ingredient innovation signals that formulators are investing heavily in edible-compatible actives, which directly expands the product development runway for brands competing in this segment.

According to a study published in the Journal of Applied Microbiology, fermentation of plant-derived edible cosmetic ingredients increased antioxidant activity by 35% in laboratory testing. This performance advantage gives fermentation-based formulations a measurable edge over conventional alternatives, and brands that can validate these efficacy claims will command stronger price premiums in premium retail channels.

Key Takeaways

- The Global Edible Cosmetics Market was valued at USD 308.2 Million in 2025 and is forecast to reach USD 777.2 Million by 2035.

- The market is projected to grow at a CAGR of 9.7% during the forecast period 2026 to 2035.

- By Product, Skin Care dominates with a 48.2% share in 2025.

- By Distribution Channel, Online leads with a 38.4% share in 2025.

- North America is the dominant region with a 38.4% share, valued at USD 118.3 Million.

Product Analysis

Skin Care dominates with 48.2% due to broad daily-use application across demographics.

In 2025, Skin Care held a dominant market position in the By Product segment of the Edible Cosmetics Market, with a 48.2% share. Daily application frequency, combined with high consumer willingness to pay for clean-label ingredients, makes skin care the segment where edible formulations deliver the most commercially visible differentiation.

Hair Care serves as the second-largest product category, driven by consumer demand for sulfate-free and food-grade alternatives to conventional hair treatments. Ingredients such as plant oils and herbal extracts are well-established in edible-compatible hair formulations. Moreover, this category attracts buyers who prioritize scalp health alongside cosmetic performance.

Makeup carries strong growth potential within the edible cosmetics space because lip products represent the most direct safety concern for ingestion. Consequently, food-grade formulations in lip makeup command premium positioning and higher consumer trust. Additionally, this category benefits from growing social media attention on clean makeup alternatives.

Nail Polish occupies a niche but strategically important position, as it targets the most chemically sensitive segment of conventional cosmetics buyers. Formulations free from traditional solvents and synthetic colorants remain technically complex. However, brands that successfully launch validated edible nail products can establish first-mover positioning in an underdeveloped category.

Moisturizers represent the highest-volume sub-segment within Skin Care, as daily hydration is the most consistent consumer habit across all age groups. According to Symrise Sustainability Report, upcycled food by-products used in cosmetic ingredient manufacturing reduced raw-material waste by 30% in formulation supply chains, making moisturizer production more sustainable and cost-competitive for brands investing in circular ingredient sourcing.

Sunscreen within edible-compatible skin care occupies a premium tier because food-grade UV-active ingredients require advanced formulation science. Brands that deliver clinically validated SPF performance using edible actives create a defensible product category that conventional clean beauty players cannot easily replicate.

Cleansers serve as the entry-level purchase for consumers transitioning into edible skin care routines. Low price points and high repurchase frequency make cleansers a strategic acquisition product for building long-term customer relationships in this market.

Serums carry the highest margin within the Skin Care sub-category because concentrated active delivery justifies premium pricing. According to Givaudan Sustainability Report, biotechnology-derived natural cosmetic actives improved ingredient stability in formulations by up to 25% compared with conventional plant extracts, directly strengthening the efficacy case for edible serum formulations.

Face Products within the Makeup category anchor brand identity for most edible cosmetics labels because foundation and tinted moisturizers are high-engagement daily-use items. Consumers evaluate these products on both performance and ingredient safety, making edible formulations particularly compelling in this sub-segment.

Eye Makeup presents specific formulation challenges because periocular skin is highly sensitive and regulatory scrutiny of ingredients used near eyes is stricter. However, brands that clear this hurdle gain strong credibility across their broader product portfolios.

Lip Makeup differentiates through direct ingestion risk, making food-grade formulations not just a preference but a genuine functional requirement. This sub-segment has the clearest consumer rationale for choosing edible over conventional cosmetics, which makes conversion rates from awareness to purchase higher than in other makeup categories.

Shampoos within Hair Care lead the sub-category in unit volume because hair washing frequency is higher than most other hair care routines. Edible-compatible shampoo formulations appeal to consumers who have already adopted clean personal care habits in skin care and are now extending those preferences to hair.

Conditioners complement shampoo adoption and benefit from the same clean-label demand. Ingredient overlap between edible conditioners and leave-in treatments creates product line extension opportunities for brands looking to increase basket size.

Hair Oils and Serums command premium pricing within the Hair Care category because concentrated nutrient-dense oils directly align with edible ingredient narratives. Plant-derived oils such as argan, jojoba, and marula are already food-grade by nature, lowering the formulation barrier in this sub-segment.

Hair Masks offer an intensive treatment format that justifies higher price points and creates experiential differentiation. This sub-segment overlaps with the spa and wellness treatment channel, expanding its distribution beyond conventional retail.

Distribution Channel Analysis

Online dominates with 38.4% due to ingredient transparency demands driving digital research behavior.

In 2025, Online held a dominant market position in the By Distribution Channel segment of the Edible Cosmetics Market, with a 38.4% share. Digital platforms allow brands to communicate complex ingredient stories that physical shelf space cannot convey. Therefore, online channels are structurally better suited to edible cosmetics than to conventional beauty categories.

Hypermarkets and Supermarkets provide the broadest consumer reach but impose strict shelf-space competition that disadvantages smaller edible cosmetic brands. However, category placement near natural food sections gives edible cosmetics an opportunity for contextual positioning that reinforces their food-grade identity to mainstream shoppers.

Specialty Stores serve as the highest-trust channel for edible cosmetics because curated assortments signal category credibility. Store staff education plays a decisive role in purchase conversion at this channel, and brands that invest in retail training programs gain disproportionate share at specialty retail.

Pharmacies and Drugstores provide access to health-conscious consumers who approach beauty purchases through a therapeutic lens. This channel is particularly important for edible skin care products positioned around clinical or dermatological benefits, as pharmacist endorsement carries high credibility with these buyers.

Key Market Segments

By Product

- Skin Care

- Moisturizers

- Sunscreen

- Cleansers

- Serums

- Others

- Hair Care

- Shampoos

- Conditioners

- Hair Oils and Serums

- Hair Masks

- Others

- Makeup

- Face Products

- Eye Makeup

- Lip Makeup

- Others

- Nail Polish

By Distribution Channel

- Online

- Hypermarkets & Supermarkets

- Specialty Stores

- Pharmacies & Drugstores

- Others

Drivers

Consumer Demand for Safe, Food-Grade Beauty Ingredients Reshapes Product Formulation Standards

Consumers now read cosmetic ingredient labels with the same scrutiny they apply to food packaging. This behavioral shift reflects a fundamental change in how buyers evaluate product safety. Brands that cannot demonstrate food-grade or chemical-free formulations face growing purchasing resistance, particularly among younger demographic groups who research ingredients before buying.

Social media has converted edible skincare from a niche concept into a mainstream beauty category. Platforms amplify novel formulations — particularly dessert-inspired and fruit-based products — reaching audiences that traditional marketing channels cannot. According to a study in the International Journal of Cosmetic Science, lip care formulations using food-grade cocoa butter and plant oils improved moisture retention by 24% after 4 weeks of testing, giving brands a performance data point that validates ingredient choices beyond marketing claims.

Multi-functional beauty products that combine nutritional and cosmetic benefits attract buyers seeking efficiency in their personal care routines. This convergence of wellness and beauty creates a purchase justification that single-function cosmetics cannot match. Consequently, brands that position edible cosmetics as both performance products and health investments capture a wider and more loyal customer base than conventional beauty brands.

Restraints

Regulatory Complexity and Ingredient Stability Challenges Constrain Edible Cosmetic Product Launches

Edible cosmetics occupy a regulatory grey area between food safety standards and cosmetic ingredient regulations. Brands must satisfy compliance requirements from both domains simultaneously, which increases formulation costs and extends time-to-market. Smaller brands with limited regulatory resources face disproportionate barriers, which consolidates category leadership among well-funded players.

Food-based ingredients introduce shelf life and stability challenges that synthetic cosmetic actives do not present. Natural oils, botanical extracts, and food-grade preservatives degrade faster under standard retail storage conditions. According to ScienceDirect, edible and biodegradable packaging materials used in cosmetic applications can reduce plastic packaging waste by up to 60%, but these packaging solutions add cost complexity that further strains formulation economics for brands already managing shorter product shelf lives.

The combined pressure of stricter safety dossiers and shorter product cycles forces brands to invest heavily in R&D and stability testing before launch. This investment threshold delays revenue and discourages product line expansion among mid-market players. Consequently, the pipeline of new edible cosmetic entrants remains constrained even as consumer demand for the category continues to outpace available supply options.

Growth Factors

Premium Organic, Vegan, and Personalized Beauty Segments Open High-Value Revenue Channels for Edible Cosmetics

The premium organic beauty segment commands price points that directly reward the higher ingredient costs inherent in edible cosmetic formulations. Brands positioned at this tier attract consumers who treat beauty spending as a health investment. Additionally, vegan certification requirements align naturally with plant-based edible ingredient sourcing, giving this sub-segment a dual compliance advantage.

Product innovation in edible lip balms, face masks, and beauty supplements creates new shelf positions within established retail categories. According to the Society of Cosmetic Scientists, cosmetic formulations using fermented botanical extracts improved skin hydration performance by 18% compared with non-fermented extracts in controlled testing. This efficacy differential gives innovators a concrete clinical argument for premium pricing and retailer ranging decisions.

Personalized beauty products made with functional food ingredients represent the highest-margin growth channel because customization commands a structural price premium. According to a study published in MDPI Cosmetics, honey-based cosmetic formulations demonstrated antimicrobial inhibition rates of up to 90% against common skin bacteria in laboratory testing. This clinical performance data positions honey-based personalized formulations as medically credible options, expanding the addressable buyer base beyond fashion-driven consumers into health-focused demographics.

Emerging Trends

Nutraceutical Ingredients, DIY Formats, and Clean-Label Marketing Redefine the Edible Cosmetics Category

Dessert-inspired formulations — particularly chocolate, honey, and fruit-based products — are converting the edible cosmetics concept from a novelty into a repeatable purchase behavior. These formats generate high social media engagement and drive trial among consumers who might not otherwise explore functional beauty. Moreover, the sensory experience of indulgent formulations creates emotional brand attachment that conventional skin care cannot replicate.

Collagen, honey, and herbal extracts have transitioned from nutraceutical supplements into topical cosmetic formulations, blurring the boundary between the ingestible wellness and beauty markets. According to MDPI Cosmetics, probiotic fermentation increased the bioavailability of polyphenols in plant extracts used for cosmetic formulations by 28%. This bioavailability advantage strengthens the performance case for fermented botanical actives and signals that the convergence between supplement science and cosmetic formulation will deepen over the next decade.

DIY edible skincare kits are gaining adoption among Gen Z and Millennial consumers who prioritize ingredient transparency and personalized routines. Clean-label marketing — where brands disclose every ingredient with food-standard detail — is becoming a competitive requirement rather than a differentiator. Brands that have not yet adopted transparent sourcing and ingredient communication practices face a growing credibility gap relative to market leaders already operating at this standard.

Regional Analysis

North America Dominates the Edible Cosmetics Market with a Market Share of 38.4%, Valued at USD 118.3 Million

North America leads the global edible cosmetics market with a 38.4% share, valued at USD 118.3 Million. High consumer spending on premium personal care, mature clean beauty retail infrastructure, and strong social media-driven product discovery combine to sustain this position. Additionally, well-established regulatory frameworks for cosmetic ingredient disclosure give North American consumers higher baseline confidence in edible product claims.

Europe Edible Cosmetics Market Trends

Europe represents the second-largest market, supported by long-standing consumer preference for natural and organic personal care products. EU cosmetic ingredient regulations are among the strictest globally, which inadvertently accelerates adoption of food-grade formulations by limiting synthetic alternatives. Germany, France, and the UK anchor European demand, with specialty retail and pharmacy channels serving as the primary distribution infrastructure.

Asia Pacific Edible Cosmetics Market Trends

Asia Pacific presents the strongest structural growth trajectory of any region, driven by large beauty-conscious consumer bases in China, Japan, South Korea, and India. K-beauty and J-beauty cultural influence normalizes novel cosmetic formats, including edible and food-inspired products. Moreover, the region’s robust manufacturing base for botanical and fermented ingredients creates a cost advantage for locally produced edible formulations.

Latin America Edible Cosmetics Market Trends

Latin America shows early-stage but structurally sound adoption, anchored by Brazil and Mexico where natural ingredient cosmetics carry strong cultural resonance. Abundant local supply of tropical plant-based actives — including fruit oils and botanical extracts — gives regional brands a formulation cost advantage. However, distribution infrastructure outside major urban centers limits category penetration in the short term.

Middle East and Africa Edible Cosmetics Market Trends

The Middle East and Africa market operates on two distinct tracks: premium edible cosmetics in GCC luxury retail, and entry-level natural beauty products in broader African markets. Halal-certified formulations align naturally with edible cosmetic ingredient standards, creating a product compliance advantage for brands targeting the GCC consumer base. South Africa serves as the primary African distribution hub for international edible cosmetic brands.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Kendo Holdings operates as a brand incubator model within the edible and clean beauty space, giving it a structural advantage in testing niche formulations across multiple brand identities simultaneously. This portfolio architecture allows Kendo to absorb early-stage category risk at the brand level rather than the corporate level. Consequently, the company can experiment with edible cosmetic concepts without exposing its core business to single-product performance risk.

Burt’s Bees built its competitive position on food-grade and natural ingredient credibility before the clean beauty movement became mainstream retail. This early positioning gives the brand a trust equity that newer entrants cannot quickly replicate. Its dominance in the lip care category — where food-grade ingredients carry the highest consumer relevance — creates a defensible revenue base as the broader edible cosmetics category expands.

Tarte Inc differentiates through ingredient storytelling tied to specific sourcing origins, positioning its formulations as both performance-driven and ethically transparent. This dual-positioning strategy targets consumers who evaluate brands on both efficacy and values alignment. Additionally, Tarte’s strong social media presence in Millennial and Gen Z demographics provides direct access to the consumer segments driving edible cosmetics trial and adoption.

Eminence Organic Skin Care grounds its market position in certified organic and food-grade ingredient standards, with a distribution model that prioritizes spa and professional wellness channels. This channel strategy is strategically significant because spa and wellness operators serve as credibility validators for edible cosmetic formulations. Professional endorsement accelerates premium consumer adoption faster than retail shelf placement alone can achieve.

Key Players

- Kendo Holdings

- Burt’s Bees

- Tarte Inc

- Eminence Organic Skin Care

- Kiehl’s

- Dr. Dennis Gross Skincare LLC

- L’Oréal Paris

- Herbivore Botanicals, LLC

- Sappho New Paradigm Cosmetics Inc.

- Tata Harper Skincare

- Juice Beauty

- Fenty Beauty by Rihanna

Recent Developments

- March 2025 — Wellness Beauty Group acquired GlowVita, a fast-growing edible skincare brand specializing in nutrient-infused supplements and plant-based beauty gummies. The acquisition signals consolidation activity in the edible beauty nutrition segment and reflects growing strategic interest from established wellness groups in owning direct-to-consumer edible cosmetic platforms.

Report Scope

Report Features Description Market Value (2025) USD 308.2 Million Forecast Revenue (2035) USD 777.2 Million CAGR (2026-2035) 9.7% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product (Skin Care [Moisturizers, Sunscreen, Cleansers, Serums, Others], Hair Care [Shampoos, Conditioners, Hair Oils and Serums, Hair Masks, Others], Makeup [Face Products, Eye Makeup, Lip Makeup, Others], Nail Polish), By Distribution Channel (Online, Hypermarkets & Supermarkets, Specialty Stores, Pharmacies & Drugstores, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Kendo Holdings, Burt’s Bees, Tarte Inc, Eminence Organic Skin Care, Kiehl’s, Dr. Dennis Gross Skincare LLC, L’Oréal Paris, Herbivore Botanicals LLC, Sappho New Paradigm Cosmetics Inc., Tata Harper Skincare, Juice Beauty, Fenty Beauty by Rihanna Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Kendo Holdings

- Burt's Bees

- Tarte Inc

- Eminence Organic Skin Care

- Kiehl's

- Dr. Dennis Gross Skincare LLC

- L'Oréal Paris

- Herbivore Botanicals, LLC

- Sappho New Paradigm Cosmetics Inc.

- Tata Harper Skincare

- Juice Beauty

- Fenty Beauty by Rihanna

Our Clients

- 182121

- Mar 2026