Global Drilling Machines Market Size, Share, Growth Analysis, Product Type (CNC Drilling Machines, Sensitive Drilling Machines, Upright Drilling Machines, Radial Drilling Machines, Gang Drilling Machines, Deep Hole Drilling Machines, Multiple Spindle Drilling Machines, Others), Automation Level (Fully Automated, Manual, Semi-Automated), Operation (Hole Drilling, Tapping, Counterboring, Reaming, Spot Facing, Others), Structure (Fixed, Portable), End Use (Automotive, Aerospace and Defense, Fabrication and Industrial Machinery, Construction, Oil and Gas and Energy, Electronics and Electricals, Shipbuilding and Marine, Others), Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 178915

- Number of Pages: 286

- Format:

-

keyboard_arrow_up

Quick Navigation

- Drilling Machines Market Overview

- Key Takeaways

- Product Type Analysis

- Automation Level Analysis

- Operation Analysis

- Structure Analysis

- End Use Analysis

- Key Market Segments

- Drivers

- Restraints

- Growth Factors

- Emerging Trends

- Regional Analysis

- Key Regions and Countries

- Key Company Insights

- Recent Developments

- Report Scope

Drilling Machines Market Overview

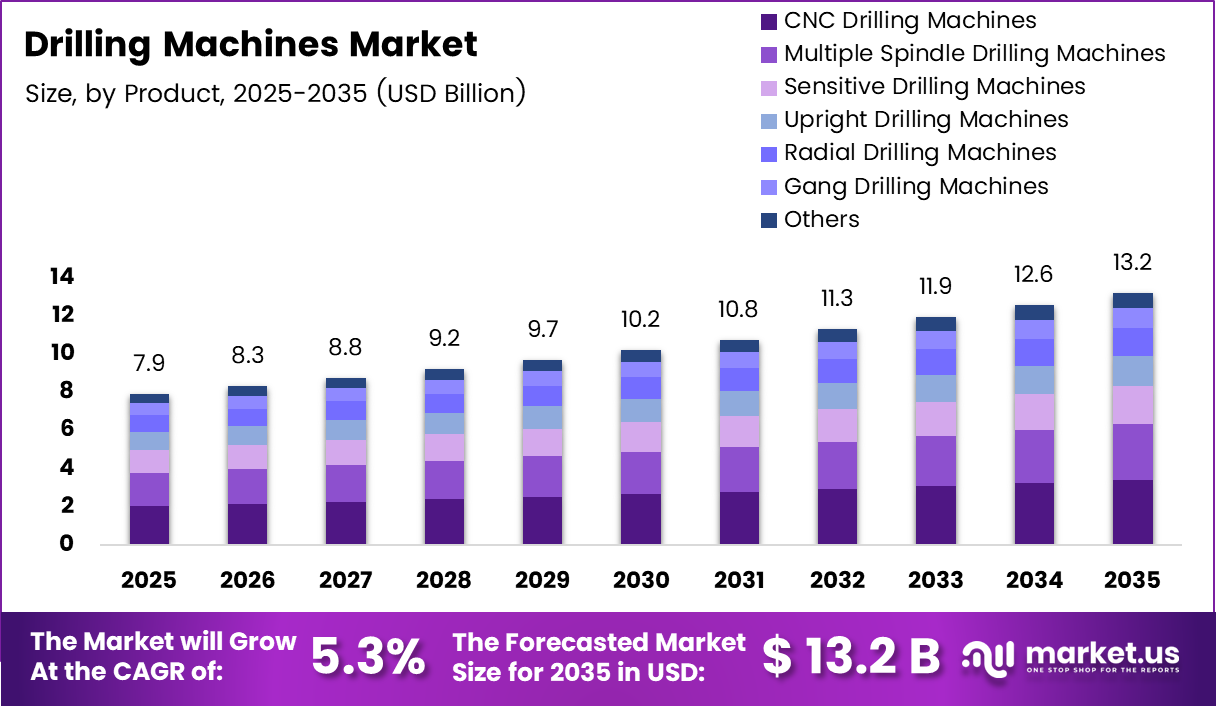

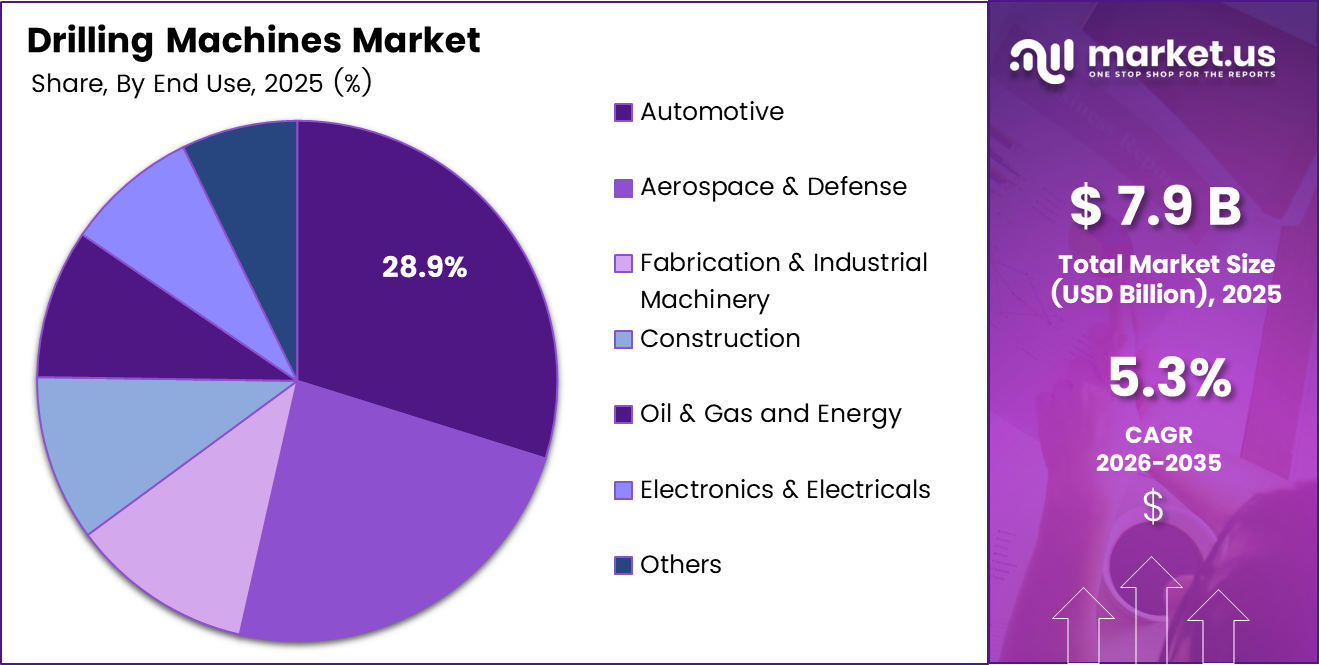

Global Drilling Machines Market size is expected to be worth around USD 13.2 Billion by 2035 from USD 7.9 Billion in 2025, growing at a CAGR of 5.3% during the forecast period 2026 to 2035.

The drilling machines market encompasses a broad range of industrial equipment used to create precise holes in materials such as metal, wood, composites, and stone. These machines are essential across manufacturing, construction, mining, and energy sectors. They range from compact portable units to large CNC-based industrial systems.

Drilling machines play a critical role in modern manufacturing by enabling precision hole-making, tapping, reaming, and counterboring operations. Moreover, their application spans automotive assembly lines, component manufacturing, and heavy fabrication workshops. Consequently, demand remains consistent across both developed and emerging economies.

Infrastructure expansion and smart city development projects are driving steady investments in construction and heavy engineering equipment worldwide. Additionally, the rise of metal fabrication workshops in emerging economies is increasing demand for both manual and automated drilling service. Governments across Asia, the Middle East, and Africa are actively funding large-scale industrial and urban development projects.

The transition toward CNC and IoT-enabled drilling systems is reshaping the market landscape. Manufacturers are investing in precision machining to meet tighter engineering tolerances in aerospace and defense applications. Furthermore, the growing adoption of compact drilling machines in small and medium enterprises is opening new revenue streams for equipment suppliers.

Regulatory frameworks around workplace safety and energy efficiency are also influencing equipment design and procurement decisions. Governments in developed nations are enforcing stricter noise and emission standards for industrial tools. Therefore, manufacturers are increasingly developing low-noise, energy-efficient drilling solutions to comply with these evolving regulations.

Radial Drilling Machines are favored for their flexibility in drilling large and heavy workpieces without frequent repositioning. They are available in multiple configurations including V-belt driven and all-geared variants, with drilling capacities ranging from 25mm to 50mm, catering to diverse industrial and educational requirements.

V-belt driven models offer precision drilling across different metal types with varied spindle travel, while all-geared versions such as auto-feed radial drill machines deliver enhanced boring performance for heavy-duty applications. Moreover, models with a 170mm pillar diameter provide superior structural support during high-load operations, making them suitable for automotive, fabrication, and general engineering environments.

Consequently, radial drilling machines are widely adopted across both large manufacturing facilities and small workshop settings due to their versatility, durability, and cost-effectiveness.

Key Takeaways

- The global Drilling Machines Market was valued at USD 7.9 Billion in 2025 and is projected to reach USD 13.2 Billion by 2035.

- The market is growing at a CAGR of 5.3% during the forecast period 2026 to 2035.

- By Product Type, CNC Drilling Machines dominate with a 25.8% market share in 2025.

- By Automation Level, Fully Automated drilling machines hold a leading share of 35.8%.

- By Operation, Hole Drilling accounts for the largest share at 54.9%.

- By Structure, Fixed drilling machines lead with a 65.1% share.

- By End Use, the Automotive segment dominates with a 28.9% share.

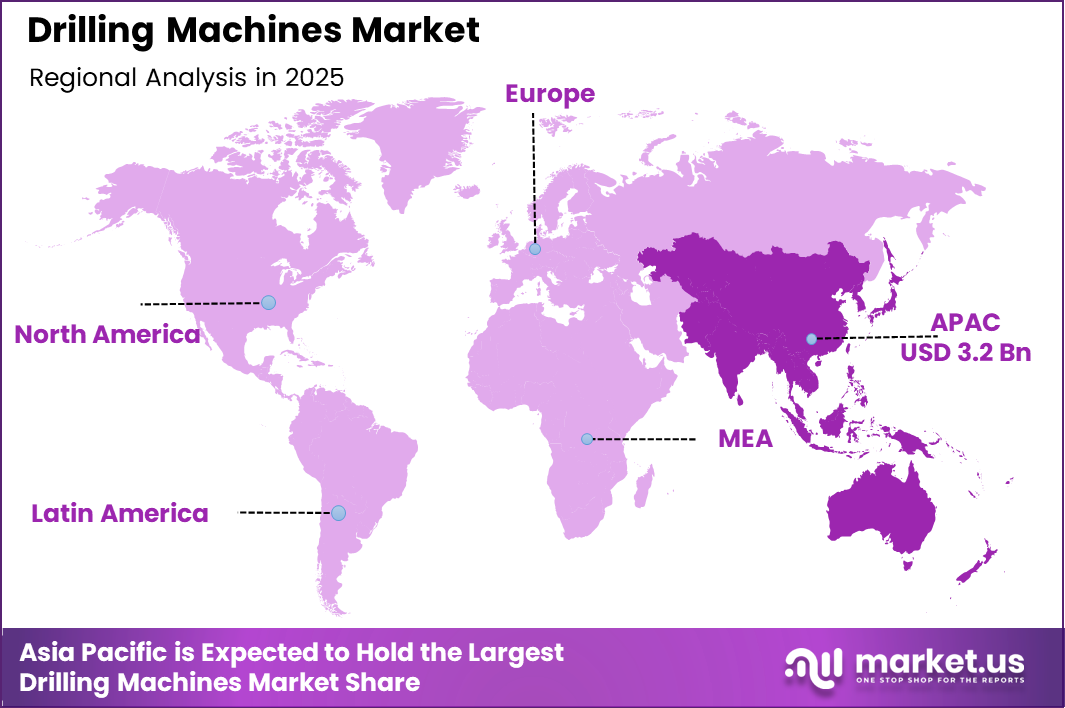

- Asia Pacific is the leading region, holding a 40.3% market share valued at USD 3.2 Billion.

Product Type Analysis

CNC Drilling Machines dominate with 25.8% due to rising demand for precision and automation in industrial manufacturing.

In 2025, CNC Drilling Machines held a dominant market position in the Product Type segment of the Drilling Machines Market, with a 25.8% share. These machines are widely preferred for their high accuracy, repeatability, and compatibility with automated production lines. Moreover, their adoption is growing rapidly across automotive, aerospace, and precision engineering sectors.

Sensitive Drilling Machines are commonly used for light-duty drilling tasks in small workshops, tool rooms, and educational institutions. Their hand-feed mechanism allows operators to maintain tactile control over drilling depth and pressure, making them suitable for precise, small-diameter hole-making. Moreover, their compact size, low cost, and minimal maintenance requirements make them a practical choice for entry-level and training environments.

Upright Drilling Machines remain a staple in general manufacturing environments where medium-capacity drilling tasks are performed on a regular basis. These machines are floor-mounted and capable of handling a wider range of workpiece sizes and material types compared to sensitive variants. Additionally, their robust construction, adjustable spindle speeds, and compatibility with various drill bit sizes make them a versatile and reliable choice across fabrication and machining workshops.

Radial Drilling Machines are favored for their flexibility in drilling large and heavy workpieces without frequent repositioning. Their adjustable arm and spindle head allow operators to cover a wide work area from a single setup. Consequently, they are widely used in heavy engineering, shipbuilding, and large-part fabrication environments where mobility of the drill head is essential.

Gang Drilling Machines support high-volume production by enabling multiple holes to be drilled simultaneously across a workpiece. These machines are designed with several drill heads mounted on a single table, significantly reducing cycle times in mass manufacturing. Moreover, they are commonly deployed in automotive component production and electronics assembly lines where repetitive drilling operations are performed at scale.

Deep Hole Drilling Machines are engineered specifically for creating holes with high depth-to-diameter ratios in precision components such as gun barrels, hydraulic cylinders, and aerospace parts. They use specialized tooling and coolant systems to maintain accuracy over extended drilling depths. Additionally, growing demand from defense and energy sectors is expanding the addressable market for these high-performance machines.

Multiple Spindle Drilling Machines are designed to drill several holes at once using a configurable spindle arrangement, making them ideal for repetitive, high-accuracy production tasks. They deliver consistent hole patterns across large production batches with minimal setup time. Furthermore, the Others category includes specialized variants such as micro-drilling and gun-drilling machines that serve distinct industrial niches requiring tailored hole-making solutions.

Automation Level Analysis

Fully Automated drilling machines dominate with 35.8% due to increasing demand for precision, speed, and reduced labor dependency.

In 2025, Fully Automated drilling machines held a dominant market position in the Automation Level segment of the Drilling Machines Market, with a 35.8% share. These systems are integral to high-throughput manufacturing environments where consistency and speed are critical. Consequently, adoption is accelerating across automotive plants and large-scale fabrication facilities.

Manual drilling machines continue to hold relevance in small workshops, repair units, and cost-sensitive markets. They remain widely used in developing regions due to their lower capital cost and minimal maintenance requirements. However, their market share is gradually declining as automation becomes more accessible to mid-sized manufacturers.

Semi-Automated drilling machines bridge the gap between manual control and full automation. They offer operators greater flexibility while still improving production efficiency. Additionally, semi-automated systems are increasingly popular among small and medium enterprises seeking productivity gains without the full investment of CNC or fully automated solutions.

Operation Analysis

Hole Drilling dominates with 54.9% due to its fundamental role across all industrial manufacturing and construction applications.

In 2025, Hole Drilling held a dominant market position in the Operation segment of the Drilling Machines Market, with a 54.9% share. This operation forms the foundation of most machining and fabrication processes. Moreover, it is indispensable in automotive, construction, aerospace, and general engineering applications worldwide.

Here is the revised section with each sub-segment written as its own 3-line paragraph:

Tapping is a widely used secondary operation that creates internal threads within pre-drilled holes, enabling secure fastener assembly in mechanical and structural components. It is an essential process in automotive, machinery, and electronics manufacturing where threaded connections are critical to product integrity. Moreover, the growing complexity of engineered assemblies is driving demand for machines capable of combining drilling and tapping in a single setup.

Counterboring supports precision bolt-seating in engineering assemblies by enlarging the upper portion of a drilled hole to accommodate bolt heads or nuts flush with the workpiece surface. This operation is widely used in structural fabrication, heavy equipment manufacturing, and precision machining applications. Additionally, its role in ensuring clean and stable fastener placement makes it an indispensable operation in high-tolerance manufacturing environments.

Reaming is valued for finishing operations that require superior hole accuracy, tight dimensional tolerances, and improved surface quality beyond what standard drilling can achieve. It is commonly applied in aerospace, automotive, and hydraulic component manufacturing where fit and finish are critical. Furthermore, the increasing demand for high-precision components across advanced manufacturing sectors is sustaining steady growth in reaming operation requirements.

Spot Facing is used to create flat, smooth surfaces around drilled holes to ensure proper and stable seating of fasteners, washers, and bearing surfaces. This operation is particularly common in aerospace structures, heavy machinery, and industrial equipment manufacturing. Additionally, the Others category includes specialized operations such as boring and chamfering, which address specific industrial requirements where standard drilling operations alone are insufficient.

Structure Analysis

Fixed drilling machines dominate with 65.1% due to their superior stability, power, and suitability for heavy industrial applications.

In 2025, Fixed drilling machines held a dominant market position in the Structure segment of the Drilling Machines Market, with a 65.1% share. These machines are preferred in production environments where precision, rigidity, and consistent performance are essential. Consequently, they are widely deployed in automotive plants, metal fabrication shops, and large manufacturing facilities.

Portable drilling machines are gaining traction across construction sites, maintenance operations, and field service environments. Their compact design and ease of transportation make them highly suitable for tasks that require on-site drilling. Moreover, increasing adoption among SMEs and repair service providers is steadily expanding the portable segment’s market footprint.

End Use Analysis

Automotive dominates with 28.9% due to high-volume precision drilling requirements in vehicle component manufacturing.

In 2025, Automotive held a dominant market position in the End Use segment of the Drilling Machines Market, with a 28.9% share. The sector demands high-speed, precise, and repeatable drilling operations for engine components, Automotive chassis, and body panels. Moreover, the shift toward electric vehicles is introducing new drilling requirements for battery housings and lightweight materials.

Aerospace and Defense is a high-value end-use segment requiring ultra-precise drilling for aircraft fuselages, engine components, and defense equipment structures. The sector demands specialized drilling solutions capable of working with advanced materials such as titanium alloys, carbon fiber composites, and high-strength steel. Moreover, increasing global defense budgets and expanding commercial aviation fleets are sustaining strong and consistent demand for precision drilling equipment in this segment.

Fabrication and Industrial Machinery encompasses a broad range of general metalworking applications where drilling machines of varied sizes and capabilities are routinely deployed. Workshops and job shops in this segment require flexible equipment that can handle diverse materials, hole sizes, and production volumes. Additionally, growth in contract manufacturing and the expansion of industrial parks in emerging economies are driving procurement of both standard and advanced drilling systems.

Construction drives demand for portable and heavy-duty drilling equipment used in foundation work, concrete drilling, and structural steel assembly across large infrastructure projects. The segment requires robust machines capable of operating in demanding outdoor and on-site conditions. Furthermore, rapid urbanization and government-funded infrastructure development programs in Asia Pacific, the Middle East, and Africa are generating sustained demand for construction-grade drilling equipment.

Oil and Gas and Energy relies on specialized deep-hole and rotary drilling systems for well exploration, extraction, and pipeline installation operations. These applications demand high-performance equipment engineered for extreme operating conditions and extended operational cycles. Consequently, growth in energy infrastructure investment and offshore drilling activity is supporting continued demand for advanced drilling solutions in this segment.

Electronics and Electricals requires micro-precision drilling for printed circuit boards, electronic enclosures, and miniaturized component assemblies where accuracy at very small scales is critical. The increasing complexity and miniaturization of electronic devices is pushing demand for high-speed, fine-tolerance drilling machines. Moreover, expansion of electronics manufacturing in Asia Pacific is creating significant volume opportunities for precision drilling equipment suppliers serving this segment.

Shipbuilding and Marine utilizes heavy-duty drilling equipment for hull construction, structural assembly, and fitting of mechanical systems across large vessel manufacturing projects. The sector demands machines capable of operating on large steel plates and complex curved surfaces. Additionally, the Others category captures residual end-use industries such as medical device manufacturing and furniture production, which collectively contribute to diversified and stable demand across the global drilling machines market.

Key Market Segments

Product Type

- CNC Drilling Machines

- Sensitive Drilling Machines

- Upright Drilling Machines

- Radial Drilling Machines

- Gang Drilling Machines

- Deep Hole Drilling Machines

- Multiple Spindle Drilling Machines

- Others

Automation Level

- Fully Automated

- Manual

- Semi-Automated

Operation

- Hole Drilling

- Tapping

- Counterboring

- Reaming

- Spot Facing

- Others

Structure

- Fixed

- Portable

End Use

- Automotive

- Aerospace and Defense

- Fabrication and Industrial Machinery

- Construction

- Oil and Gas and Energy

- Electronics and Electricals

- Shipbuilding and Marine

- Others

Drivers

Rapid Infrastructure Expansion and Rising Precision Manufacturing Demand Drive Drilling Machines Market Growth

Large-scale infrastructure development, smart city projects, and construction activities worldwide are generating consistent demand for industrial drilling equipment. Governments across Asia, the Middle East, and Africa are investing heavily in roads, bridges, and urban structures. Consequently, contractors and fabricators are procuring advanced drilling machines to meet project timelines and quality standards.

The automotive and heavy engineering industries require highly precise hole-making operations for critical components such as engine blocks, transmission parts, and structural assemblies. Rising vehicle production volumes and stricter engineering tolerances are pushing manufacturers toward high-performance drilling systems. Moreover, the transition to electric vehicle platforms is introducing new drilling challenges that favor CNC and automated solutions.

Growth of metal fabrication and machining workshops in emerging economies is expanding the addressable market for mid-range and entry-level drilling machines. Additionally, increasing adoption of power tools in small-scale manufacturing units and repair workshops is broadening market access beyond large industrial buyers. Therefore, both industrial and SME demand channels are contributing to steady market growth.

Restraints

High Capital Costs and Skilled Workforce Shortages Limit Broader Adoption of Advanced Drilling Machines

Industrial drilling machines, particularly CNC and fully automated systems, require significant upfront capital investment that many small and medium enterprises find difficult to justify. Additionally, ongoing maintenance, spare parts procurement, and calibration costs add to the total cost of ownership. Consequently, price-sensitive buyers in developing markets often defer upgrades or opt for lower-capability manual alternatives.

The shortage of skilled operators and technicians capable of programming and maintaining advanced CNC-based drilling machines poses a significant barrier to market expansion. Training qualified personnel requires time, cost, and institutional support that is not always available in emerging industrial regions. Moreover, high employee turnover in manufacturing further compounds the challenge of building consistent operational expertise.

These combined restraints slow the rate of technology adoption, particularly in regions where industrial infrastructure and vocational training ecosystems are still developing. However, vendors are responding by offering simplified interfaces, remote diagnostics, and operator training packages to reduce adoption barriers. Therefore, while restraints exist, strategic product and service adaptations are helping to mitigate their impact over time.

Growth Factors

CNC Integration, Aerospace Demand, and Renewable Energy Projects Accelerate Drilling Machines Market Expansion

The rising integration of CNC systems, automation, and IoT connectivity into drilling machines is significantly enhancing operational efficiency and precision. Smart drilling platforms equipped with sensors and real-time monitoring allow manufacturers to reduce downtime and improve output quality. Moreover, these technological upgrades are making advanced machines more accessible and cost-effective for mid-scale industrial buyers.

Growing demand from aerospace and defense manufacturing sectors is creating high-value opportunities for precision drilling equipment suppliers. These industries require specialized drilling capabilities for composite materials, titanium alloys, and high-strength steel. Additionally, expanding defense budgets in North America, Europe, and Asia Pacific are translating into sustained procurement of advanced machining and drilling systems.

Renewable energy projects, including wind farms and solar installations, require precision drilling for foundations, mounting structures, and mechanical assemblies. Furthermore, increasing penetration of compact and portable drilling machines among small and medium enterprises is expanding the market base. Consequently, the combination of industrial-scale and SME-level demand is creating a well-diversified growth trajectory for the global drilling machines market.

Emerging Trends

Energy Efficiency, Smart Sensors, and Ergonomic Design Are Reshaping the Drilling Machines Market

A clear shift toward energy-efficient and low-noise drilling equipment is emerging across developed industrial markets. Regulatory pressure and sustainability commitments are prompting manufacturers to redesign motors, gearboxes, and cooling systems for lower energy consumption. Moreover, quieter machines are increasingly preferred in urban manufacturing environments where noise pollution regulations apply.

Multi-spindle and high-speed drilling machines are gaining popularity in high-volume production settings where cycle time reduction is a priority. These systems enable simultaneous drilling of multiple holes, significantly improving throughput in automotive and electronics manufacturing. Additionally, the adoption of smart sensors for predictive maintenance is reducing unplanned downtime and extending machine service life across industrial applications.

Lightweight and ergonomic drill designs are receiving growing attention as manufacturers prioritize operator safety and comfort on the shop floor. Reducing machine weight and improving handle design lowers fatigue and the risk of musculoskeletal injuries. Furthermore, this trend aligns with broader workplace safety regulations that are becoming more stringent in North America, Europe, and parts of Asia Pacific.

Regional Analysis

Asia Pacific Dominates the Drilling Machines Market with a Market Share of 40.3%, Valued at USD 3.2 Billion

Asia Pacific leads the global drilling machines market with a dominant share of 40.3%, valued at USD 3.2 Billion in 2025. The region benefits from a large and rapidly expanding manufacturing base in China, India, Japan, and South Korea. Moreover, government-led infrastructure programs, growing automotive production, and the proliferation of metal fabrication workshops are reinforcing Asia Pacific’s market leadership.

North America Drilling Machines Market Trends

North America represents a mature and technologically advanced market for drilling machines, driven by strong demand from aerospace & defense, automotive manufacturing sectors. The United States leads regional adoption of CNC and automated drilling systems. Additionally, reshoring initiatives and manufacturing investment incentives are supporting sustained equipment procurement across key industrial states.

Europe Drilling Machines Market Trends

Europe maintains a significant share of the global drilling machines market, supported by precision engineering industries in Germany, Italy, and France. The region’s focus on Industry 4.0 adoption is accelerating the integration of smart and connected drilling systems. Furthermore, stringent energy efficiency and workplace safety regulations are driving demand for next-generation low-noise and ergonomic drilling equipment.

Middle East and Africa Drilling Machines Market Trends

The Middle East and Africa region is witnessing growing demand for drilling machines driven by construction activity, oil and gas operations, and industrial diversification programs. Gulf Cooperation Council countries are investing in manufacturing capabilities as part of economic diversification strategies. Consequently, demand for both heavy-duty and portable drilling equipment is rising across the region.

Latin America Drilling Machines Market Trends

Latin America presents a developing market for drilling machines, with Brazil and Mexico leading regional demand through their automotive assembly and industrial manufacturing sectors. Growth in construction and energy infrastructure projects is also contributing to equipment procurement. However, economic volatility and currency risks remain factors that moderate the pace of capital equipment investment across the region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Atlas Copco is a globally recognized industrial equipment leader with a strong presence in the drilling machines market. The company offers a broad portfolio of pneumatic and hydraulic drilling solutions serving mining, construction, and manufacturing end-users. Its commitment to innovation and sustainability has enabled it to maintain a competitive position across multiple geographies and application sectors.

Epiroc AB, spun off from Atlas Copco, has established itself as a leading supplier of drilling and rock excavation equipment for the mining and infrastructure industries. The company focuses on automation, digitalization, and electrification of its drilling platforms. Moreover, Epiroc’s global service network and application expertise make it a trusted partner for large-scale industrial and underground drilling projects.

Sandvik AB is a prominent player in the drilling machines market, offering advanced rock drilling tools, equipment, and automation systems primarily for the mining and construction sectors. The company invests significantly in research and development to deliver high-performance and durable drilling solutions. Additionally, Sandvik’s digital tools and remote monitoring capabilities are aligned with the growing industry shift toward smart manufacturing.

Caterpillar is a leading manufacturer of heavy equipment including industrial drilling machines used across construction, mining, and energy sectors. The company leverages its global distribution network and strong aftermarket services to maintain long-term customer relationships. Furthermore, Caterpillar’s ongoing investment in autonomous and semi-autonomous drilling technologies positions it well for the evolving demands of large infrastructure and resource extraction projects.

Key Players

- Atlas Copco

- Bauer Maschinen GmbH

- Beretta S.r.l.

- Boart Longyear

- Caterpillar

- Cheto Corporation SA

- Dezhou Hongxin Machine Tool Co Ltd

- Epiroc AB

- ERLO Group

- Ingersoll Rand

- Liebherr Group

- Minitool

- Mitsubishi Heavy Industries Ltd.

- Sandvik AB

- Shenyang Machine Tool Co Ltd

- Other Key Players

Recent Developments

- January 2026 – Borr Drilling completed the acquisition of five premium jack-up rigs, significantly expanding its operational fleet and offshore drilling capacity. This strategic move strengthens the company’s position in the global jack-up rig market and enhances its ability to serve international energy clients.

- January 2025 – Drilling Tools International Corp completed the acquisition of a UK-based company, bolstering its technological capabilities and service offerings. The transaction creates a comprehensive solution provider for the global drilling industry, expanding DTI’s reach and product portfolio across international markets.

Report Scope

Report Features Description Market Value (2025) USD 7.9 Billion Forecast Revenue (2035) USD 13.2 Billion CAGR (2026-2035) 5.3% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered Product Type (CNC Drilling Machines, Sensitive Drilling Machines, Upright Drilling Machines, Radial Drilling Machines, Gang Drilling Machines, Deep Hole Drilling Machines, Multiple Spindle Drilling Machines, Others), Automation Level (Fully Automated, Manual, Semi-Automated), Operation (Hole Drilling, Tapping, Counterboring, Reaming, Spot Facing, Others), Structure (Fixed, Portable), End Use (Automotive, Aerospace and Defense, Fabrication and Industrial Machinery, Construction, Oil and Gas and Energy, Electronics and Electricals, Shipbuilding and Marine, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Atlas Copco, Bauer Maschinen GmbH, Beretta S.r.l., Boart Longyear, Caterpillar, Cheto Corporation SA, Dezhou Hongxin Machine Tool Co Ltd, Epiroc AB, ERLO Group, Ingersoll Rand, Liebherr Group, Minitool, Mitsubishi Heavy Industries Ltd., Sandvik AB, Shenyang Machine Tool Co Ltd, Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Atlas Copco

- Bauer Maschinen GmbH

- Beretta S.r.l.

- Boart Longyear

- Caterpillar

- Cheto Corporation SA

- Dezhou Hongxin Machine Tool Co Ltd

- Epiroc AB

- ERLO Group

- Ingersoll Rand

- Liebherr Group

- Minitool

- Mitsubishi Heavy Industries Ltd.

- Sandvik AB

- Shenyang Machine Tool Co Ltd

- Other Key Players

Our Clients

- 178915

- Feb 2026