Global Direct to Satellite Market Size, Share, Growth Analysis By Device Type (Smartphones, Feature Phones, Satellite Phones, IoT Devices, Wearables), By Service (Direct-to-Device, Direct-to-IoT, Backhaul, Managed), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 183644

- Number of Pages: 327

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

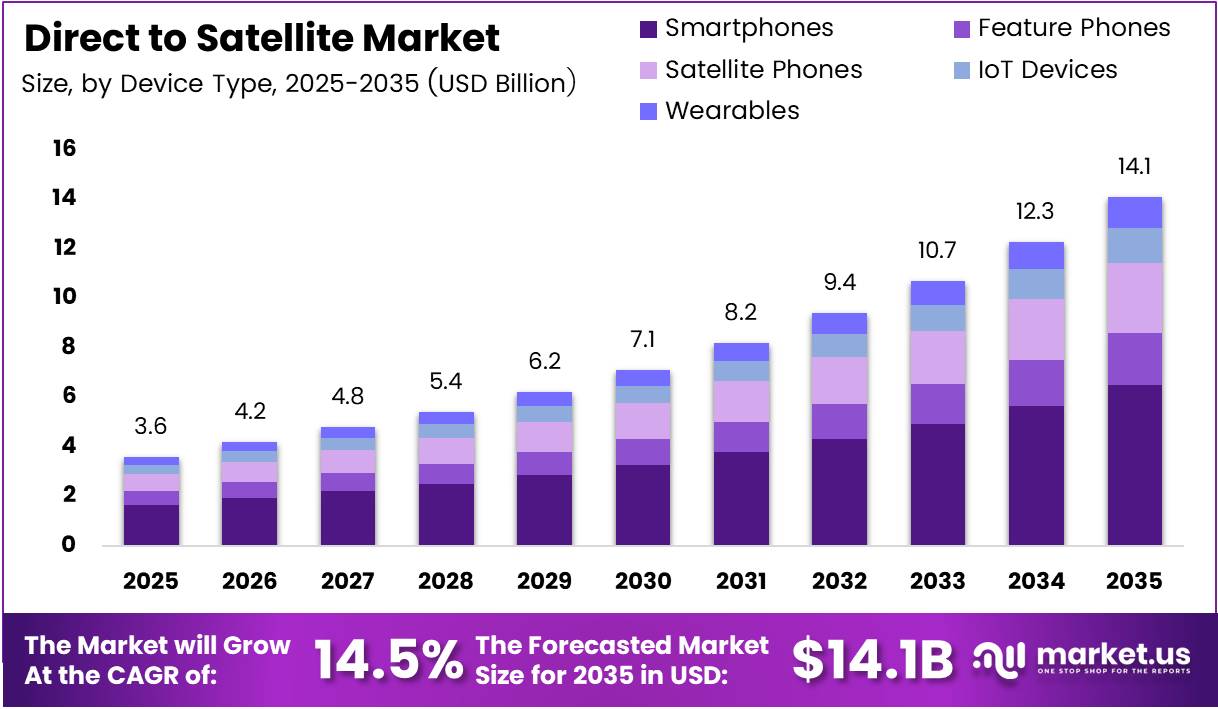

Global Direct to Satellite Market size is expected to be worth around USD 14.1 Billion by 2035 from USD 3.6 Billion in 2025, growing at a CAGR of 14.5% during the forecast period 2026 to 2035.

The direct-to-satellite market connects consumer devices — smartphones, IoT sensors, and wearables — directly to orbiting satellites, bypassing terrestrial network infrastructure entirely. This capability addresses one of telecom’s oldest unsolved problems: reliable connectivity in areas where cell towers do not exist and never will.

Low Earth Orbit constellations make this shift commercially viable. LEO satellites orbit at altitudes between 500 and 2,000 km, enabling link budgets that standard smartphones can handle without specialized hardware. That technical unlock transforms direct-to-satellite from a niche emergency tool into a mainstream connectivity layer — one that mobile operators can offer as a standard service tier.

Mobile operators recognize this shift and are accelerating commercial commitments. In February 2024, Skylo Technologies raised $30 million in an oversubscribed funding round to scale its direct-to-device satellite service worldwide — an early signal that investor confidence in commercial D2S viability was outpacing earlier skepticism about unit economics.

Government mandates for emergency connectivity and national coverage obligations further reinforce operator investment. Regulators across North America, Europe, and Asia Pacific increasingly require carriers to demonstrate coverage beyond traditional network footprints. Direct-to-satellite services offer the most scalable path to meeting those obligations without decades of tower build-out.

According to the GSA, by August 2025, there were 170 publicly announced mobile operator–satellite operator partnerships across 80 countries and territories. This figure represents a structural market inflection — when 170 operators commit publicly, the technology is no longer experimental; it is becoming procurement infrastructure.

A 2025 GSA snapshot further notes that 27 announced mobile operator partnerships are with AST SpaceMobile alone, the single highest concentration among any satellite provider. This concentration reveals that operators are making differentiated bets rather than hedging evenly — and that first-mover satellite providers with proven link performance hold a disproportionate share of operator pipeline.

Key Takeaways

- The global Direct to Satellite Market was valued at USD 3.6 Billion in 2025 and is forecast to reach USD 14.1 Billion by 2035.

- The market grows at a CAGR of 14.5% from 2026 to 2035.

- By Device Type, Smartphones dominate with a 45.7% share in 2025.

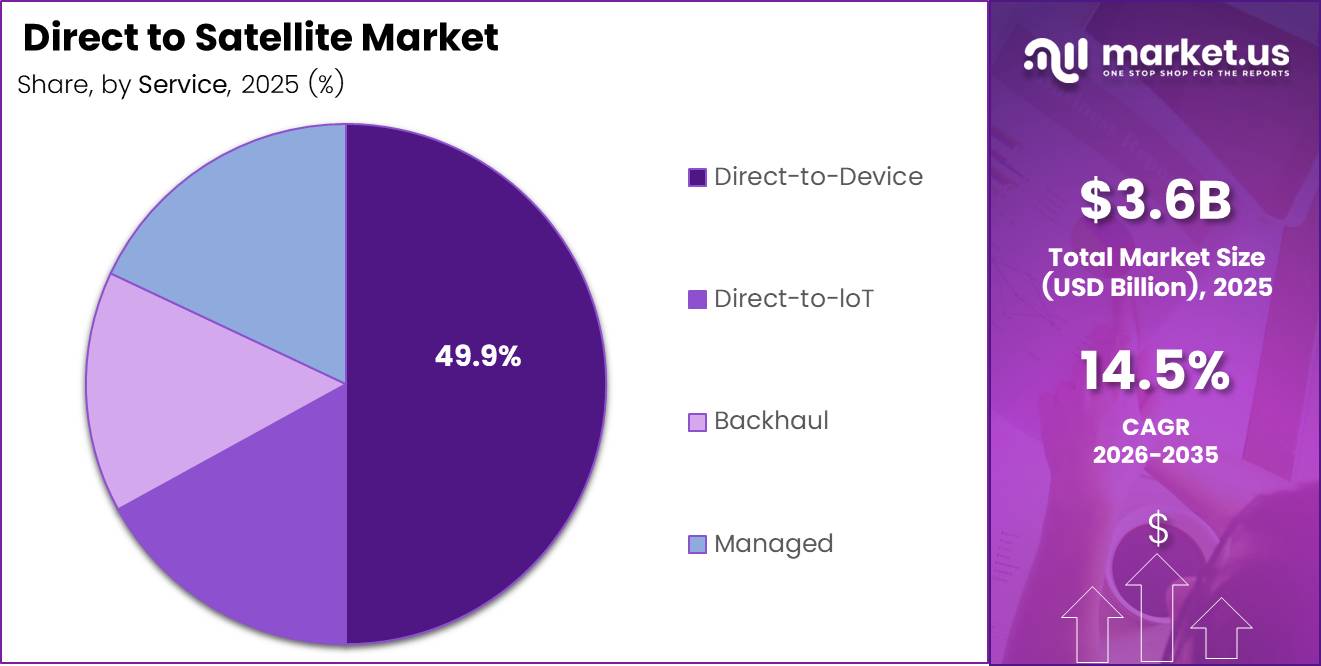

- By Service, Direct-to-Device leads with a 49.9% share.

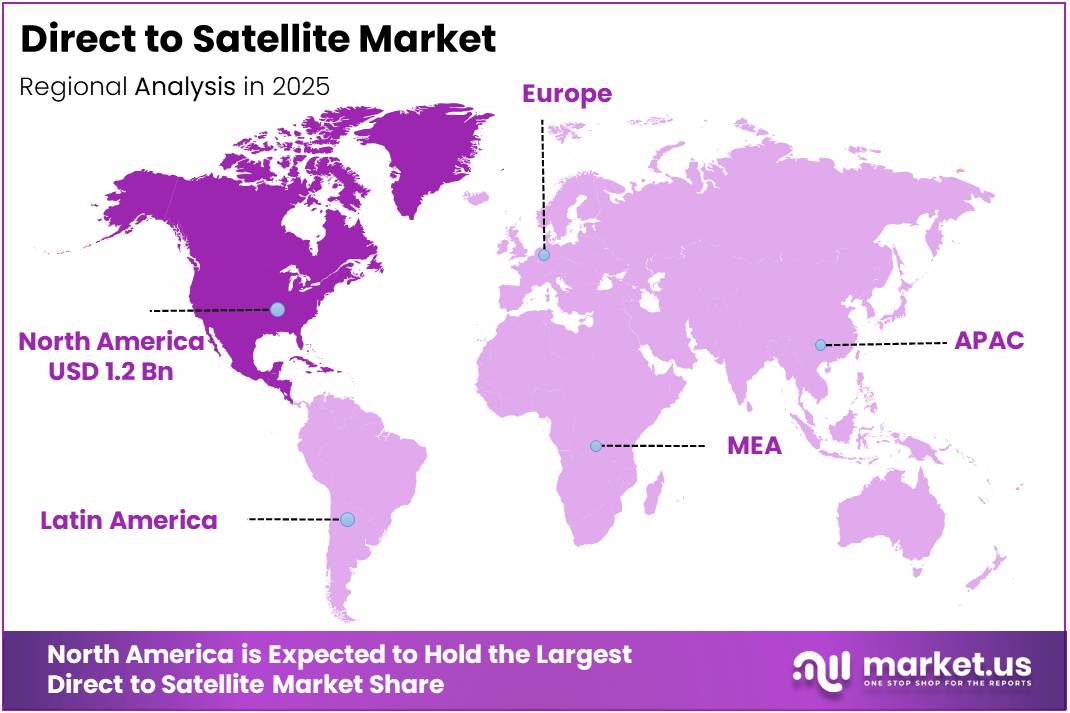

- North America holds the largest regional share at 38.90%, valued at USD 1.2 Billion.

- By August 2025, 170 mobile operator–satellite operator partnerships were active across 80 countries.

- AST SpaceMobile leads operator partnerships with 27 announced mobile operator agreements.

Product Analysis

Smartphones dominate with 45.7% due to mass consumer device base and operator integration.

In 2025, Smartphones held a dominant market position in the By Device Type segment of the Direct to Satellite Market, with a 45.7% share. Operators prioritize smartphone compatibility because it removes the need for separate hardware — service launches on existing handsets, reducing adoption friction. In February 2025, Verizon and AT&T successfully tested direct-to-satellite video calls using AST SpaceMobile’s satellites, validating commercial-grade voice and video over unmodified devices.

Feature Phones serve lower-income and rural demographics where smartphone penetration remains limited. These devices carry simpler radio architectures, which constrain satellite link performance but keep device costs accessible. Feature phone compatibility broadens the addressable subscriber base in Sub-Saharan Africa and South Asia — markets where operators see long-term growth from basic connectivity rather than data-heavy services.

Satellite Phones differentiate through purpose-built hardware designed for guaranteed two-way communication in environments where no terrestrial or LEO coverage exists. They carry the highest per-unit revenue in the device segment but address a narrow professional and government buyer base — maritime crews, expedition teams, and defense contractors — where reliability justifies premium pricing.

IoT Devices represent the fastest-expanding device category by unit volume, driven by agriculture, logistics, and utilities deploying remote sensors at scale. These devices transmit small data packets infrequently, making them well-suited to satellite access windows and low-power link designs. The business case for satellite IoT strengthens as asset-tracking mandates expand in regulated industries.

Wearables carry the highest technical challenge within the device segment due to severe antenna and battery constraints. However, safety-focused applications — personal locator beacons, lone-worker monitors, and medical alert devices — justify the engineering investment. Wearable satellite connectivity positions as a premium safety layer rather than a mass-market offering in the near term.

Service Analysis

Direct-to-Device dominates with 49.9% due to smartphone integration driving operator commercial launches.

In 2025, Direct-to-Device held a dominant market position in the By Service segment of the Direct to Satellite Market, with a 49.9% share. According to the GSA, 34 operators across 25 markets had launched commercial non-terrestrial and satellite-based services by August 2025 — confirming that D2D moved from pilot to revenue-generating activity faster than most operators anticipated when spectrum licensing began.

Direct-to-IoT services address sensor networks in agriculture, supply chain, and infrastructure monitoring where cellular coverage is absent. The service model differs structurally from D2D — operators sell connectivity on a per-device or data-volume basis rather than per subscriber — which creates more predictable recurring revenue for satellite providers deploying LEO constellations at scale.

Backhaul services use satellite capacity to extend terrestrial network reach into areas where fiber or microwave links are uneconomical. Mobile operators in frontier markets depend on satellite backhaul to connect rural cell towers, making this segment a stable revenue base for GEO and MEO satellite operators even as LEO competition intensifies in the direct-connectivity layers.

Managed services bundle satellite connectivity with network operations, monitoring, and SLA guarantees — typically for enterprise and government buyers. This segment commands higher margins because buyers pay for reliability and support rather than raw bandwidth. Managed satellite services are also less susceptible to commoditization pressure compared to direct consumer-facing service tiers.

Key Market Segments

By Device Type

- Smartphones

- Feature Phones

- Satellite Phones

- IoT Devices

- Wearables

By Service

- Direct-to-Device

- Direct-to-IoT

- Backhaul

- Managed

Drivers

Mobile Operator Partnerships and LEO Constellation Investment Accelerate Commercial Direct-to-Satellite Deployment

Mobile network operators treat direct-to-satellite connectivity as a coverage obligation, not a premium add-on. Regulators increasingly require carriers to demonstrate rural and remote coverage — and satellite links offer the only scalable solution where tower economics fail. This regulatory pressure converts operator interest into signed commercial agreements and capital commitments.

LEO constellation investment removes the technical barriers that previously confined satellite connectivity to specialized hardware. Operators can now launch D2S services on standard consumer smartphones, dramatically expanding the addressable subscriber base. In December 2024, T-Mobile opened registration for beta testing of its Starlink direct-to-cell satellite service for remote U.S. coverage — signaling that tier-one operators view this as production infrastructure, not a science project.

According to MIT’s 2025 satellite communications roadmap for 5G NTN D2D, technical targets set direct-to-device communication at 10 Mbps by 2028 and 20 Mbps by 2034 for unmodified cellular devices. These benchmarks define R&D investment priorities and give satellite vendors concrete performance gates to clear before operators commit to full commercial rollout — narrowing the window for undifferentiated providers.

Restraints

High Satellite Deployment Costs and Spectrum Barriers Restrict Market Entry and Slow Commercial Scaling

Building and launching a LEO constellation requires capital expenditures that only a small number of well-funded players can sustain. Satellite manufacturing, launch contracts, ground station infrastructure, and regulatory filings across multiple jurisdictions create a cost structure that effectively excludes mid-tier entrants. This dynamic concentrates the market around a handful of operators with existing launch relationships or government backing.

Spectrum allocation remains the most unpredictable barrier. Each country controls its own radio frequency licensing, and direct-to-device satellite services compete for spectrum already assigned to terrestrial mobile operators. Regulatory processes across major markets operate on multi-year timelines, creating launch delays that compress the commercial window between certification and market competition. In September 2025, China’s MIIT granted China Unicom a satellite mobile services license — a process that took years — illustrating how long national approvals take even in motivated regulatory environments.

A 2025 comparative study published by IJTRD found that D2D satellite links force terminals to operate at significantly higher transmit power than terrestrial cellular links to maintain link reliability over hundreds of kilometers. This elevated power draw represents a hard constraint for battery-powered consumer devices and IoT sensors, limiting session duration and requiring handset manufacturers to redesign power management — adding cost and development time across the device supply chain.

Growth Factors

Emergency Services Demand, IoT Expansion, and Telecom-Satellite Partnerships Create New Revenue Layers

Emergency communication represents one of the clearest commercial cases for direct-to-satellite services. Governments, first responders, and insurers apply sustained pressure on operators to provide connectivity during terrestrial network failures. This demand creates a service tier with pricing power — emergency-capable connectivity commands premium subscription fees from both consumers and enterprise buyers who cannot accept coverage gaps.

IoT connectivity via satellite addresses a multi-billion-device opportunity that terrestrial networks structurally cannot serve. Agriculture, maritime, mining, and energy sectors deploy sensors in locations where cellular infrastructure will never reach. In March 2025, SES and Lynk Global announced a strategic partnership for direct-to-device services, with SES providing Series B funding — validating that telecom-satellite joint ventures are becoming the preferred commercial structure for scaling IoT coverage economically.

According to a 2025 paper on satellite communication for smart grids published in IJSRA, modern LEO constellations offer roughly 15–20× lower latency (20–40 ms) and 10–50× higher bandwidth (50–300 Mbps) than legacy GEO VSAT links. These performance improvements make satellite connectivity viable for latency-sensitive industrial applications — grid control, autonomous equipment, and real-time asset monitoring — unlocking enterprise segments that rejected satellite as too slow for operational use.

Emerging Trends

Hybrid Terrestrial-Satellite Networks and AI-Driven Resource Management Redefine Connectivity Architecture

Hybrid terrestrial-satellite network architecture is displacing the historic view of satellite as a backup channel. Operators now design networks where satellite and cellular layers hand off traffic dynamically based on coverage availability and congestion. This architectural shift means satellite capacity becomes part of the primary network topology — expanding the total addressable revenue opportunity for satellite service providers beyond traditional coverage gap remediation.

Next-generation smartphone chipsets with embedded satellite modems eliminate the hardware barrier that previously separated satellite communication from mass-market devices. Handset manufacturers integrating satellite capability at the silicon level signal that D2S is becoming a standard feature rather than a premium accessory. This hardware commoditization will accelerate subscriber adoption timelines and compress the product differentiation window for device-dependent satellite services.

According to a 2025 IFIP Networking paper, deep Q-learning-based routing shifts VoIP Mean Opinion Scores from the poor-to-fair range of 1–3 into a fair-to-excellent range of 3–4.5 on satellite links. This measurable QoE improvement from AI-driven resource management demonstrates that software optimization can close the user experience gap between satellite and terrestrial services — making AI integration a competitive necessity rather than a differentiator for premium satellite network operators.

Regional Analysis

North America Dominates the Direct to Satellite Market with a Market Share of 38.90%, Valued at USD 1.2 Billion

North America holds a 38.90% share valued at USD 1.2 Billion, driven by a combination of FCC spectrum licensing momentum, established LEO operator headquarters, and tier-one carriers with the financial capacity to absorb commercial D2S rollout costs. The concentration of satellite constellation operators and consumer electronics manufacturers in the U.S. creates a supply-side cluster that reinforces North America’s lead position through faster iteration cycles.

Europe Direct to Satellite Market Trends

Europe advances direct-to-satellite deployment through regulatory harmonization under the European Electronic Communications Code and ESA-backed NTN integration programs. The region’s dense population of mobile operators creates partnership demand for satellite coverage in mountainous and maritime zones. However, fragmented national spectrum licensing slows pan-European commercial launches compared to the single-regulator environment that benefits U.S. operators.

Asia Pacific Direct to Satellite Market Trends

Asia Pacific combines the world’s largest unconnected population base with governments actively licensing satellite mobile services. China’s MIIT granted China Unicom a satellite mobile services license in September 2025 and issued guidelines promoting direct-to-satellite connectivity — converting regulatory intent into commercial authorization. India and Southeast Asian markets add further volume as operators seek coverage solutions for archipelago and rural geographies.

Middle East and Africa Direct to Satellite Market Trends

Middle East and Africa present the strongest structural case for direct-to-satellite services given the density of unserved populations relative to terrestrial network investment. Gulf Cooperation Council governments fund satellite connectivity as part of national digital infrastructure programs, while Sub-Saharan Africa relies on satellite as the primary mechanism for extending mobile access beyond urban corridors into agricultural and mining regions.

Latin America Direct to Satellite Market Trends

Latin America’s geography — the Amazon basin, Andean corridors, and remote island territories — makes terrestrial coverage extension uneconomical across large portions of the region. Operators in Brazil and Mexico have signed satellite partnership agreements to meet national broadband coverage targets. Maritime and aviation sector demand adds a premium revenue layer that improves the unit economics of satellite network investment across the region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Airbus Defence & Space positions itself at the intersection of satellite manufacturing and system integration — a combination that gives it leverage across both constellation build-out contracts and ground segment sales. Its established relationships with European defense and civil space agencies provide a procurement pipeline that pure-play commercial D2S providers cannot replicate. This dual-revenue structure insulates Airbus from the volatility of consumer-facing satellite service margins.

AST SpaceMobile has built its competitive position on a single high-conviction bet: direct-to-device connectivity on unmodified smartphones using large-aperture LEO satellites. With 27 announced mobile operator partnerships — the highest concentration in the market — AST SpaceMobile has converted technical ambition into a commercial pipeline that gives it negotiating leverage over chipset suppliers, launch providers, and spectrum holders simultaneously. The May 2025 acquisition of Ligado spectrum assets enables U.S. D2S service without requiring a terrestrial network partner, reducing dependency risk.

Viasat competes from a position of established GEO broadband infrastructure and a large installed base of enterprise and government customers. Its strategic risk in the direct-to-satellite shift is that GEO systems carry latency constraints that LEO architectures structurally eliminate. Viasat’s value proposition rests on managed service reliability and long-term government contracts rather than consumer-grade D2D performance — a defensible niche but one that narrows as LEO performance benchmarks rise.

Boeing approaches the satellite market as a systems integrator with manufacturing depth across both commercial and defense satellite programs. Boeing’s competitive moat lies in classified defense satellite contracts and long-cycle government procurement relationships that provide revenue stability independent of commercial D2S adoption curves. Its exposure to the direct-to-satellite consumer market is indirect — primarily through satellite bus manufacturing — rather than through operator partnerships or consumer service launches.

Key Players

- Airbus Defence & Space

- AST SpaceMobile

- Viasat

- Boeing

- Eutelsat OneWeb

- EchoStar

- Intelsat

- Lockheed Martin Space

- Lynk Global

- Northrop Grumman

Recent Developments

- June 2025 — Telstra launched Australia’s first direct-to-satellite text messaging service via Starlink, enabling coverage for compatible Galaxy S25 phones in areas beyond terrestrial network reach.

- August 2025 — EchoStar placed a $1.3 billion order with MDA Space for 100 satellites as the initial phase of a standards-based direct-to-device constellation, with plans to expand the fleet significantly beyond this initial deployment.

- August 2025 — Ukraine’s Kyivstar completed the first field test of Starlink direct-to-cell technology in Eastern Europe, marking a significant milestone for satellite connectivity deployment in conflict-affected and infrastructure-stressed environments.

- September 2025 — China’s MIIT granted China Unicom a license for satellite mobile services and issued national guidelines promoting direct-to-satellite phone connectivity and telecom-satellite industry partnerships across the country.

- November 2025 — Starlink secured its largest direct-to-cell commercial agreement with telecom group Veon, covering over 150 million potential customers across Veon’s multi-country operator portfolio.

Report Scope

Report Features Description Market Value (2025) USD 3.6 Billion Forecast Revenue (2035) USD 14.1 Billion CAGR (2026-2035) 14.5% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Device Type (Smartphones, Feature Phones, Satellite Phones, IoT Devices, Wearables), By Service (Direct-to-Device, Direct-to-IoT, Backhaul, Managed) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Airbus Defence & Space, AST SpaceMobile, Viasat, Boeing, Eutelsat OneWeb, EchoStar, Intelsat, Lockheed Martin Space, Lynk Global, Northrop Grumman Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Airbus Defence & Space

- AST SpaceMobile

- Viasat

- Boeing

- Eutelsat OneWeb

- EchoStar

- Intelsat

- Lockheed Martin Space

- Lynk Global

- Northrop Grumman

Our Clients

- 183644

- Mar 2026