Quick Navigation

- Report Overview

- Key Takeaways

- Analysts’ Viewpoint

- Strategic Importance of AI

- US Economic Market Expansion

- North America Market Size

- By Content Type Analysis

- By End-User Analysis

- Key Market Segments

- Driver

- Restraint

- Opportunity

- Challenge

- Growth Factors

- Emerging Trends

- Business Benefits

- Key Player Analysis

- Recent Developments

- Report Scope

Report Overview

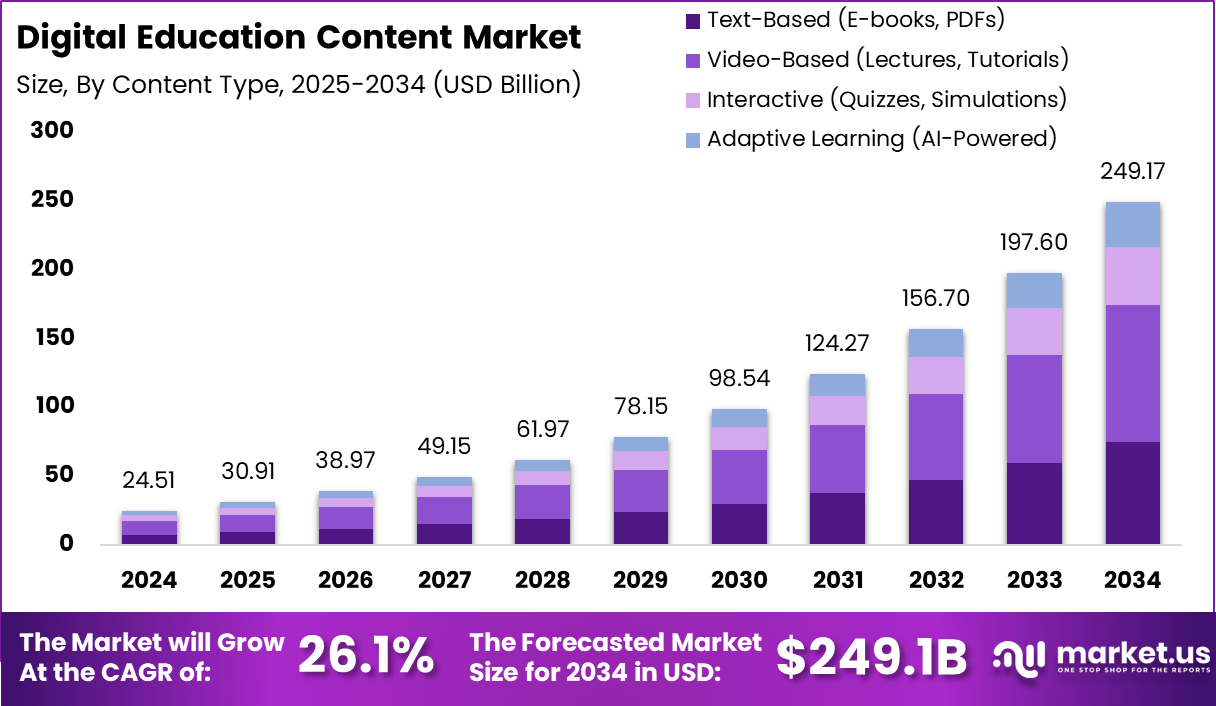

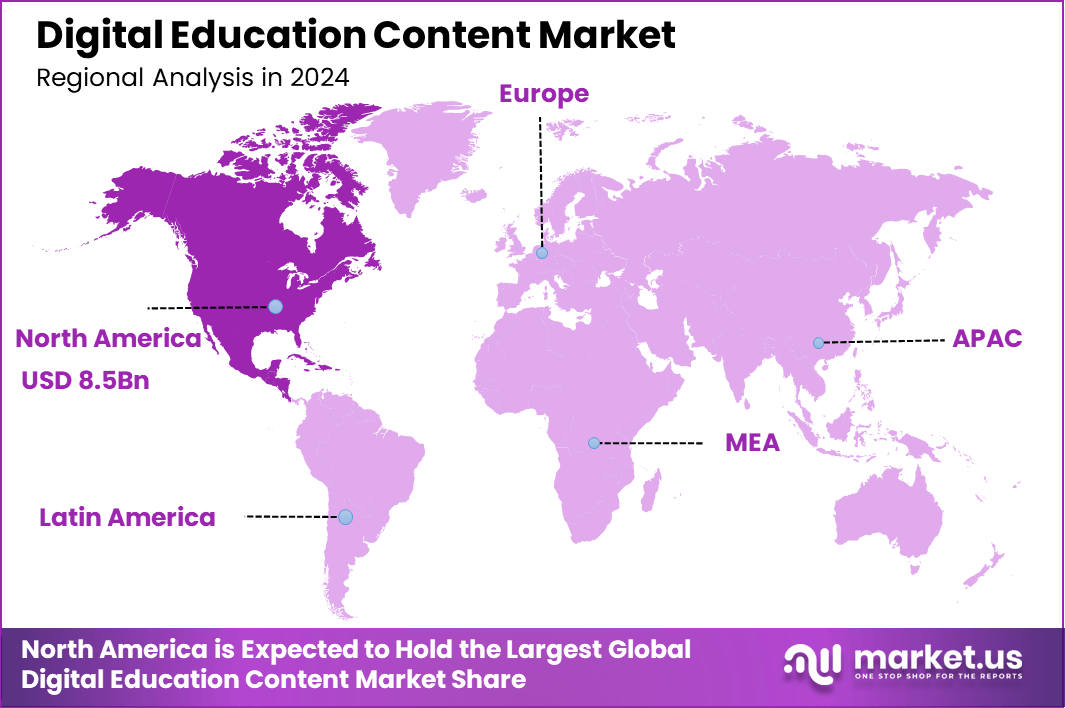

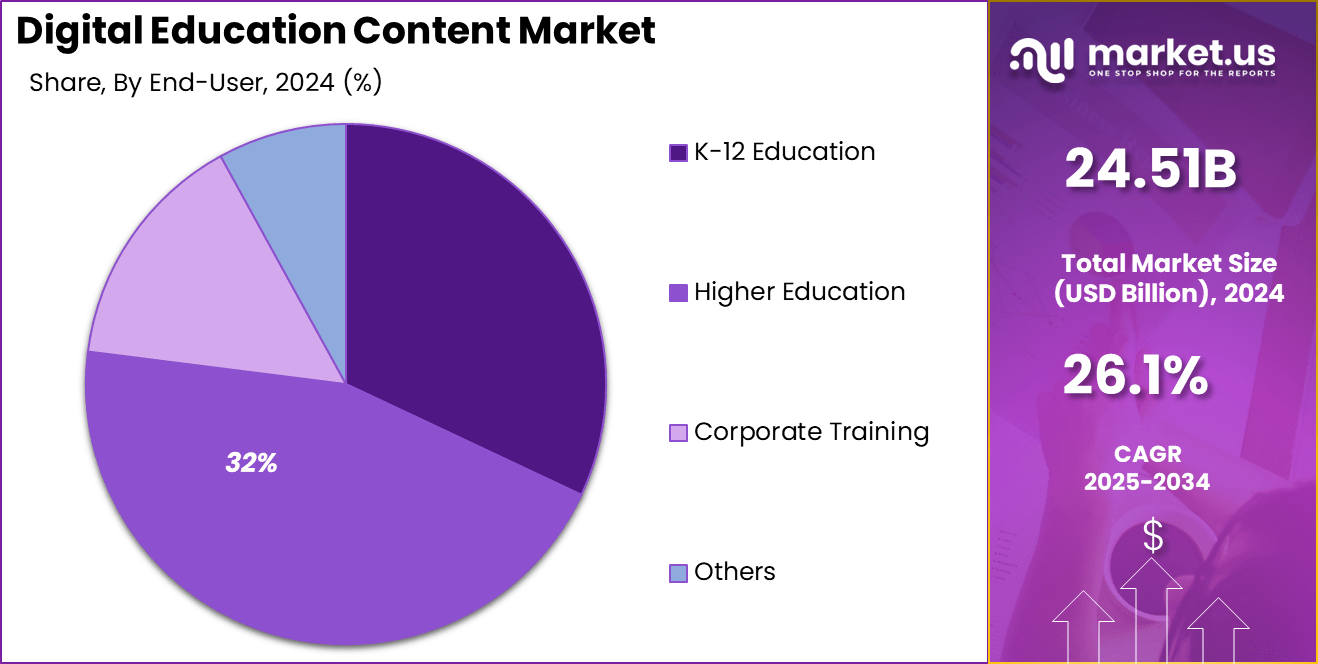

The Global Digital Education Content Market size is expected to be worth around USD 249.17 Billion By 2034, from USD 24.51 billion in 2024, growing at a CAGR of 26.1% during the forecast period from 2025 to 2034. In 2024, North America held a dominant market position, capturing more than a 35% share, holding USD 8.5 Billion revenue.

Digital Education Content refers to educational materials that are created, delivered, and consumed through digital platforms. These materials encompass a wide range of formats, including text, audio, video, interactive simulations, and assessments. Designed to be accessible across various devices such as computers, tablets, and smartphones, digital education content aims to enhance learning experiences by providing flexibility and interactivity.

The Digital Education Content Market has witnessed significant growth over recent years, driven by the increasing adoption of technology in education. Top Driving Factors contributing to the market’s expansion include the increasing need for flexible learning solutions, advancements in digital infrastructure, and the growing emphasis on lifelong learning. Educational institutions and corporate organizations are investing in digital content to enhance accessibility and engagement.

Several factors are driving the expansion of this market. The widespread availability of high-speed internet and the proliferation of smart devices have made digital learning more accessible. Additionally, the need for personalized learning experiences and the integration of advanced technologies like artificial intelligence (AI) and virtual reality (VR) have enhanced the appeal of digital education content.

The demand for digital education content is also influenced by the shift towards lifelong learning and upskilling. Professionals seeking to acquire new skills or certifications prefer flexible, online learning options that digital content provides. Moreover, educational institutions are increasingly incorporating digital materials into their curricula to supplement traditional teaching methods and cater to diverse learning styles.

Technological advancements play a crucial role in shaping the digital education content market. The integration of AI allows for the creation of intelligent tutoring systems that adapt to individual learner needs. VR and augmented reality (AR) technologies offer immersive learning experiences, particularly beneficial in fields requiring practical training. These innovations not only enhance the quality of education but also expand the possibilities for content creators and educators.

Key Takeaways

- The Global Digital Education Content Market is projected to grow from USD 24.51 Billion in 2024 to USD 249.17 Billion by 2034, marking a robust CAGR of 26.1%, driven by rising demand for online learning across all age groups.

- In 2024, North America led the global landscape with over 35% market share, translating to USD 8.5 Billion, showcasing strong institutional adoption and widespread EdTech integration.

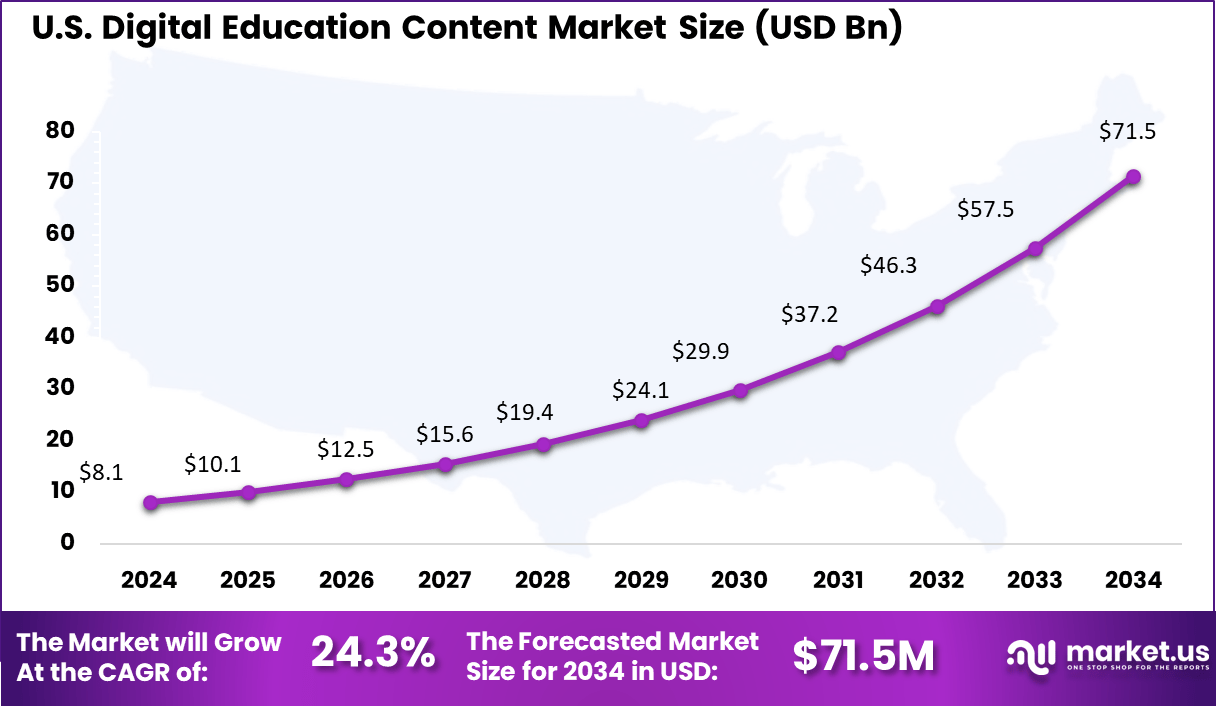

- The U.S. market alone was valued at USD 8.1 Billion in 2024, and is expected to surge to USD 71.5 Billion by 2034, growing steadily at a CAGR of 24.3%, reflecting increasing investments in K-12 and postsecondary digital content.

- Among content formats, the video-based learning segment held the lead in 2024 with more than 40% share, reflecting learner preference for visual and interactive formats that simplify complex topics.

- The higher education sector emerged as the top contributor in 2024, accounting for over 32% of global revenue, fueled by growing enrollment in virtual universities and digital upskilling platforms.

Analysts’ Viewpoint

Investment opportunities in this market are huge. The growing demand for digital learning solutions has attracted significant funding from both public and private sectors. Investors are particularly interested in startups that offer innovative content delivery platforms, AI-driven learning analytics, and scalable educational technologies.

Businesses adopting digital education content benefit from increased efficiency and scalability in training programs. E-learning platforms enable organizations to deliver consistent training across geographically dispersed teams, track progress through analytics, and update materials swiftly in response to industry changes. This approach not only reduces training costs but also enhances employee performance and retention.

The regulatory environment surrounding digital education content is evolving to ensure quality and accessibility. Governments and educational bodies are establishing standards for content development, data privacy, and accessibility to protect learners and maintain educational integrity. Compliance with these regulations is essential for content providers to build trust and expand their reach in the market.

Strategic Importance of AI

Artificial Intelligence (AI) has become a pivotal force in shaping the digital education content landscape.The global AI in education market is rapidly expanding, driven by the demand for personalized learning and intelligent classroom tools. Valued at around USD 3.6 billion in 2023, the market is projected to reach nearly USD 73.7 billion by 2033, growing at a strong CAGR of 35.10%.

One of the primary advantages of integrating AI into digital education content is the facilitation of personalized learning. AI algorithms can analyze individual student performance and adapt content to meet specific learning needs, thereby improving engagement and outcomes.

In 2024, it was reported that 86% of students globally utilized AI tools in their studies, with 54% engaging with these tools on a weekly basis. This widespread adoption highlights the growing reliance on AI to support diverse learning styles and requirements.

Educators are also increasingly embracing AI to streamline administrative tasks and enhance instructional methods. According to our 2024 GenAI Report, 45% of higher education faculty and 51% of K-12 teachers incorporated AI tools into their teaching practices, utilizing them for lesson planning, grading, and providing real-time feedback.

Furthermore, AI’s role in developing intelligent tutoring systems and virtual learning environments has expanded access to quality education, particularly in remote or underserved regions. These technologies offer scalable solutions that can be tailored to various educational contexts, ensuring that learning is more inclusive and equitable.

US Economic Market Expansion

The US Digital Education Content Market is valued at approximately USD 8.1 Billion in 2024 and is predicted to increase from USD 10.1 Billion in 2025 to approximately USD 71.5 Billion by 2034, projected at a CAGR of 24.3% from 2025 to 2034.

North America Market Size

In 2024, North America held a dominant market position in the global digital education content market, capturing more than a 35% share and generating approximately USD 8.5 billion in revenue. This leadership was primarily driven by the region’s early adoption of advanced educational technologies, strong digital infrastructure, and a mature e-learning ecosystem supported by high internet penetration.

The presence of major content providers, tech giants, and numerous EdTech startups has further contributed to the consistent rollout of innovative and interactive learning modules across K-12, higher education, and corporate training sectors. The U.S. and Canada have prioritized digital transformation in education by integrating artificial intelligence, adaptive learning systems, and gamified content into formal learning environments.

Public and private investments have been strategically directed toward personalized learning platforms, cloud-based content delivery, and inclusive digital resources. The region’s education systems have also responded swiftly to policy support, curriculum modernization, and student-centric learning goals – factors that have strengthened North America’s competitive advantage in the market.

By Content Type Analysis

In 2024, the video-based segment held a dominant position in the digital education content market, capturing more than a 40% share. This leadership is attributed to the rising demand for engaging and accessible learning materials that cater to diverse learning styles.

Video content, encompassing lectures, tutorials, and demonstrations, offers a dynamic and interactive approach to education, making complex concepts more understandable and retaining learner attention effectively. The proliferation of high-speed internet and the widespread use of smartphones and tablets have further facilitated the consumption of video-based educational content, contributing to its significant market share.

The preference for video-based learning is also driven by its versatility and adaptability across various educational contexts, including K-12, higher education, and corporate training. Educators and trainers leverage video content to provide consistent instruction, accommodate different learning paces, and offer flexible access to learning materials.

By End-User Analysis

In 2024, the higher education segment secured a leading position in the digital education content market, accounting for over 32% of the global share. This prominence is attributed to the widespread integration of digital learning platforms within universities and colleges, driven by the increasing demand for flexible and accessible educational resources.

The adoption of online courses, virtual classrooms, and AI-powered learning tools has enabled institutions to cater to diverse student needs, enhance learning outcomes, and expand their reach beyond traditional campus boundaries. The growth of this segment is further supported by the rising trend of lifelong learning and upskilling, as professionals seek to acquire new competencies in a rapidly evolving job market.

Higher education institutions have responded by offering a variety of digital programs, including micro-credentials and online degrees, to meet this demand. Additionally, the collaboration between educational institutions and technology providers has facilitated the development of innovative digital content, ensuring that higher education remains at the forefront of the digital transformation in the education sector.

Key Market Segments

By Content Type

- Text-Based (E-books, PDFs)

- Video-Based (Lectures, Tutorials)

- Interactive (Quizzes, Simulations)

- Adaptive Learning (AI-Powered)

By End-User

- K-12 Education

- Higher Education

- Corporate Training

- Others

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver

The proliferation of internet connectivity and mobile devices has been a pivotal driver for the digital education content market. As more regions gain reliable internet access, the potential user base for digital learning platforms expands correspondingly. This trend is particularly evident in emerging economies, where mobile devices often serve as the primary means of internet access.

The affordability and accessibility of smartphones and tablets have enabled a broader demographic to engage with digital educational resources, fostering inclusivity and continuous learning opportunities. The convenience offered by mobile learning platforms aligns with the needs of today’s learners, who seek flexible and on-the-go educational solutions.

This shift has prompted educational content providers to optimize their offerings for mobile compatibility, ensuring seamless user experiences. The synergy between increased internet penetration and mobile device usage is thus a significant catalyst propelling the growth of digital education content globally.

Restraint

Data Security and Privacy Concerns

Despite the advancements in digital education, data security and privacy remain pressing concerns that restrain market growth. The collection and storage of sensitive student information on digital platforms raise the risk of data breaches and unauthorized access. Such incidents can erode trust among users and deter the adoption of digital learning solutions.

Moreover, compliance with varying international data protection regulations adds complexity for educational content providers operating across borders. The challenge is compounded by the rapid integration of technologies like artificial intelligence and machine learning, which, while enhancing personalized learning experiences, also necessitate the handling of vast amounts of personal data.

Opportunity

Integration of Emerging Technologies

The integration of emerging technologies such as artificial intelligence (AI), virtual reality (VR), and augmented reality (AR) presents substantial opportunities for the digital education content market. These technologies enable the creation of immersive and interactive learning environments that can enhance student engagement and comprehension.

For instance, AI can facilitate personalized learning paths, adapting content to individual student needs and learning styles. Similarly, VR and AR can bring abstract concepts to life, providing experiential learning that is particularly beneficial in fields like science and engineering.

The adoption of these technologies can also aid in bridging educational gaps by offering scalable and cost-effective solutions. As technological advancements continue and become more accessible, their integration into digital education content is poised to revolutionize the learning experience and expand market opportunities.

Challenge

Digital Divide and Accessibility Issues

A significant challenge facing the digital education content market is the persistent digital divide, characterized by unequal access to technology and internet connectivity. In many regions, particularly in developing countries, limited infrastructure hampers the ability of students to participate in digital learning. This disparity not only affects individual learners but also exacerbates existing educational inequalities on a broader scale.

Addressing this challenge requires concerted efforts from governments, private sectors, and non-profit organizations to invest in infrastructure development and provide affordable access to digital tools. Initiatives such as subsidizing internet costs, distributing devices, and establishing community learning centers can play a pivotal role in bridging the gap.

Growth Factors

Technological Advancements and Increased Accessibility

The expansion of high-speed internet and the widespread adoption of smartphones and tablets have significantly enhanced access to digital education content. This technological proliferation enables learners worldwide to engage with educational materials anytime and anywhere, fostering a more inclusive learning environment.

Additionally, the integration of artificial intelligence (AI) and machine learning into educational platforms has facilitated personalized learning experiences, catering to individual learner needs and improving educational outcomes.

Government initiatives promoting digital literacy and online education have further accelerated market growth. For instance, various countries have implemented policies to integrate digital tools into their education systems, aiming to bridge educational gaps and enhance learning efficiency. These combined factors contribute to the robust growth trajectory of the digital education content market.

Emerging Trends

Personalized Learning and Micro-Credentials

Personalized learning, powered by AI, is emerging as a significant trend in digital education. AI-driven platforms assess individual learning styles and progress, enabling the customization of content to suit each learner’s needs. This approach enhances engagement and retention, leading to improved academic performance.

Another notable trend is the rise of micro-credentials and digital badges. These certifications allow learners to acquire and showcase specific skills, offering flexibility and relevance in a rapidly changing job market. Educational institutions and employers increasingly recognize these credentials, integrating them into formal education and professional development pathways.

Business Benefits

Cost-Effective Training Solutions

Digital education content offers businesses a cost-effective alternative to traditional training methods. Online training programs reduce expenses related to travel, accommodation, and printed materials. Moreover, digital platforms enable scalable training solutions, allowing organizations to train large numbers of employees simultaneously, regardless of geographical locations.

The flexibility of digital learning also contributes to increased productivity. Employees can access training materials at their convenience, minimizing disruptions to work schedules. This self-paced learning approach not only enhances knowledge retention but also aligns with the diverse learning preferences of a modern workforce.

Key Player Analysis

Digital Education Content Market Key Players Analysis refers to a detailed examination of the most influential companies that shape the digital learning landscape through their innovations, market strategies, partnerships, and technological advancements. These players are evaluated based on their roles in driving market growth, launching new products, entering strategic collaborations, and adapting to shifts in learner behavior and institutional needs.

Pearson has actively pursued strategic collaborations to enhance its digital learning offerings. In early 2025, the company announced a multiyear partnership with Microsoft aimed at transforming the future of learning and work through artificial intelligence (AI) integration. This collaboration focuses on developing AI-powered tools to support personalized learning experiences and improve educational outcomes.

McGraw Hill has continued to innovate in the digital education space by launching updated editions of its educational materials. In 2025, the company released the “Taxation of Individuals and Business Entities” evergreen edition, providing up-to-date content for students and professionals . This release underscores McGraw Hill’s dedication to delivering current and relevant educational resources.

Coursera has solidified its position as a leading online learning platform by expanding its course offerings and forging new partnerships. In 2025, the company was recognized among Fast Company’s Most Innovative Companies in education, highlighting its impact on transforming how students learn. Coursera’s emphasis on providing accessible, high-quality education has contributed to its growing user base.

Top Key Players

- 2U Inc.

- Adobe Inc.

- Ambow Education Holding Ltd.

- Apollo Global Management Inc.

- Articulate Global Inc.

- Cambridge University Press

- Cengage Learning Holdings II Inc.

- Chegg, Inc.

- Coursera Inc.

- D2L Corp.

- Echo360 Inc.

- edX Inc.

- IXL Learning

- LinkedIn Corporation

- MPS Limited

- NIIT Ltd.

- Oxford University Press

- Pearson Plc

- Pluralsight LLC

- Others

Recent Developments

- In July 2024, D2L acquired H5P Group, a provider of interactive content creation tools, for $25.6 million. This acquisition aimed to enhance D2L’s Brightspace platform with advanced content creation capabilities.

- In July 2024, private equity firm KKR agreed to acquire Instructure Holdings, known for its Canvas learning platform, for $4.8 billion. This move followed a trend of significant investments in the edtech sector.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 24.51Bn |

| Forecast Revenue (2034) | USD 249.17 Bn |

| CAGR (2025-2034) | 26.1% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Content Type (Text-Based (E-books, PDFs), Video-Based (Lectures, Tutorials), Interactive (Quizzes, Simulations), Adaptive Learning (AI-Powered)), By End-User (K-12 Education, Higher Education, Corporate Training, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | 2U Inc., Adobe Inc., Ambow Education Holding Ltd., Apollo Global Management Inc., Articulate Global Inc., Cambridge University Press, Cengage Learning Holdings II Inc., Chegg, Inc., Coursera Inc., D2L Corp., Echo360 Inc., edX Inc., IXL Learning, LinkedIn Corporation, MPS Limited, NIIT Ltd., Oxford University Press, Pearson Plc, Pluralsight LLC, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |