Quick Navigation

- Report Overview

- Key Takeaways

- Machine Analysis

- Bonding Analysis

- Application Analysis

- End-use Industry Analysis

- Key Market Segments

- Regional Analysis

- Key Regions and Countries

- Market Dynamics

- Drivers

- Restraints

- Challenges

- Opportunities

- Key Company Insights

- Recent Developments

- Geopolitical Impact Analysis

- Report Scope

Report Overview

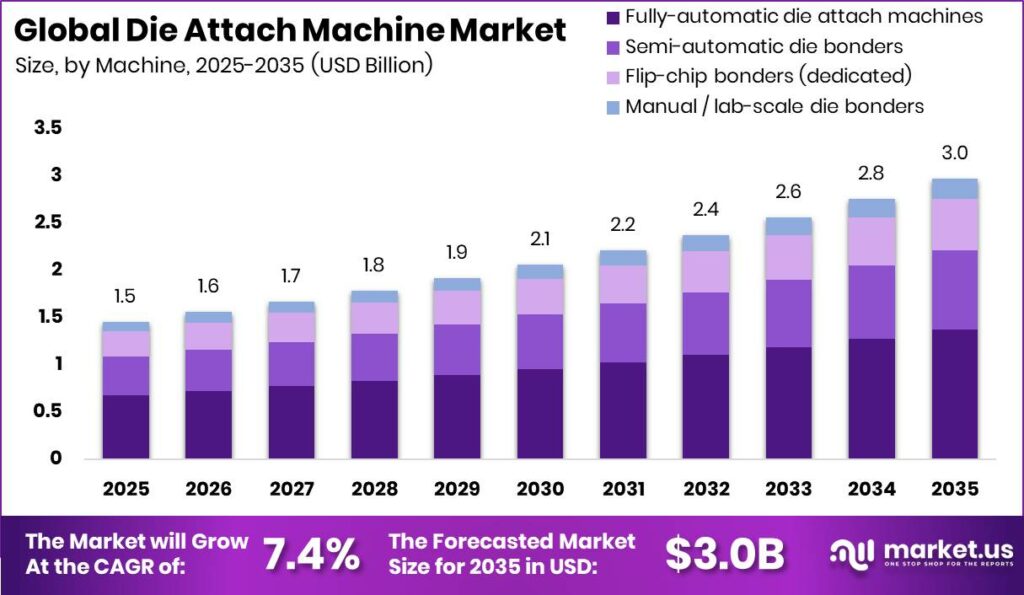

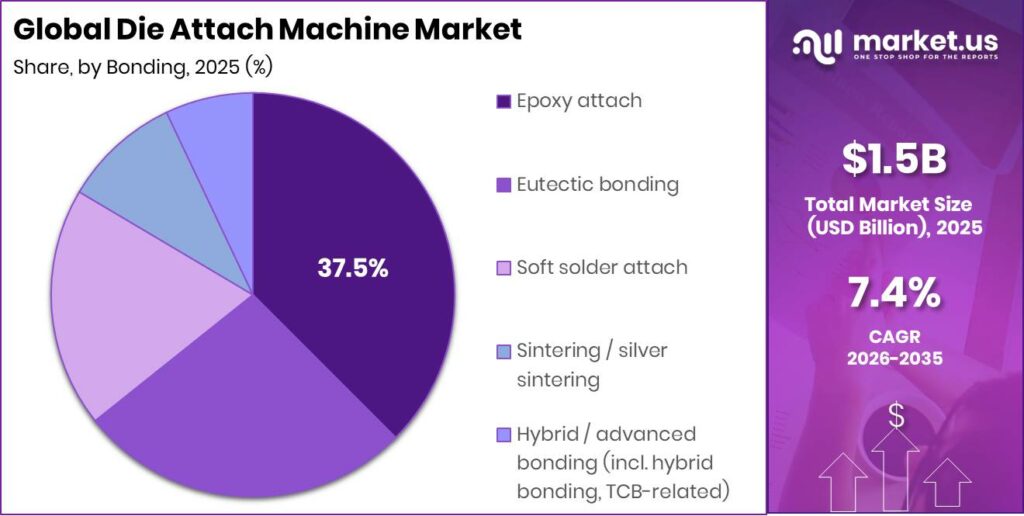

Global Die Attach Machine Market size is expected to be worth around USD 3.0 Billion by 2035 from USD 1.5 Billion in 2025, growing at a CAGR of 7.4% during the forecast period 2026 to 2035. This growth tracks directly with semiconductor back-end assembly capacity build-out. Buyers timing equipment procurement early will lock in supply before lead times extend during peak demand cycles.

The Die Attach Machine Market covers equipment that bonds semiconductor dies onto substrates or lead frames. This step opens every back-end assembly and packaging line. Machine tiers range from manual lab units to fully automatic high-precision platforms. Vendors compete across bonding method, placement accuracy, and throughput. This structure means suppliers must match platform capability to each customer’s product mix to win orders.

Key Takeaways

- Die Attach Machine Market size reaches USD 3.0 Billion by 2035 from USD 1.5 Billion in 2025 at a 7.4% CAGR.

- Fully automatic die attach machines lead the By Machine segment with a 46.3% share.

- Epoxy attach leads the By Bonding segment with a 37.5% share.

- Logic, processors and SoCs lead the By Application segment with a 24.0% share.

- Consumer electronics leads the By End-use Industry segment with a 33.0% share.

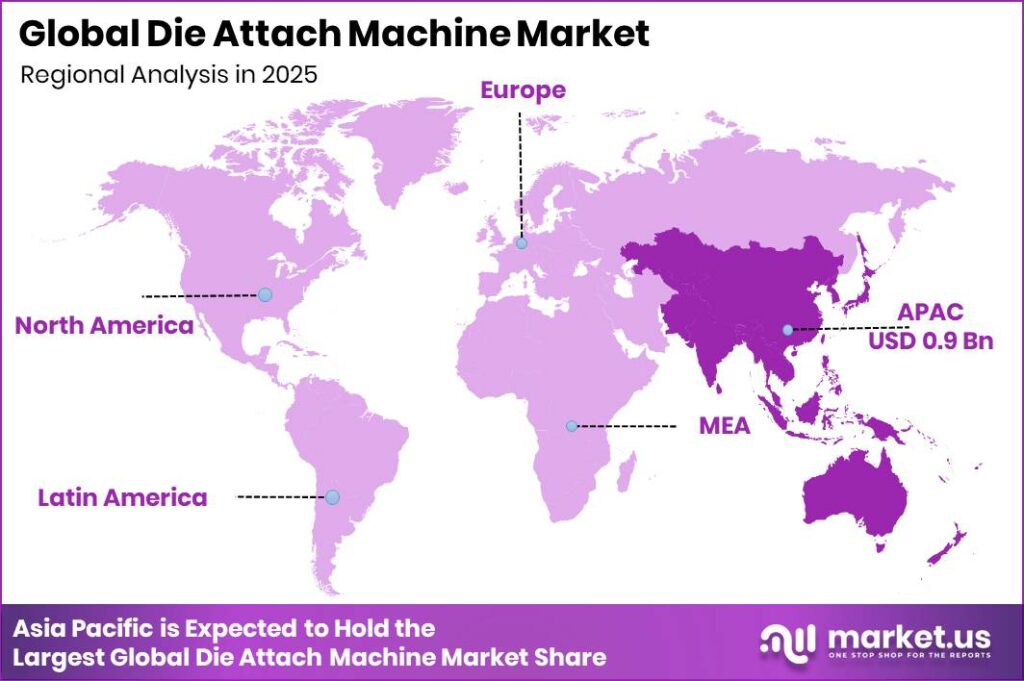

- Asia Pacific dominates with a 63.1% share, valued at USD 0.9 Billion.

Government funding now shapes where new die attach demand appears. National chip programs push assembly and test capacity into fresh geographies. This creates new procurement events that did not exist five years ago. As a result, equipment suppliers must build regional sales and service coverage to capture greenfield orders in India, the United States, and Europe.

End-use growth feeds directly into machine demand. Rising output in Embedded Die Packaging lifts orders for high-precision bonding platforms. Data from SEMI shows assembly and packaging equipment sales increased by 21% year over year in 2025 as advanced packaging adoption widened. This means suppliers with advanced platforms can capture disproportionate share as packaging complexity climbs.

Broad equipment spending confirms the demand base. According to SEMI, global semiconductor equipment billings reached US$32.05 billion in Q1 2025, an increase of 21% against Q1 2024. This billing strength funds customer capacity plans that convert into die attach orders. Therefore, vendors holding firm order backlogs gain pricing power and forward revenue visibility across multiple quarters.

Machine Analysis

Fully automatic die attach machines dominate with 46.3% due to high throughput volume production needs.

In 2025, Fully automatic die attach machines held a dominant market position in the By Machine segment of Die Attach Machine Market, with a 46.3% share. Corporate filings from ASMPT report its INFINITE bonder reaches up to 18,500 UPH in standard mode. This throughput lets high-volume fabs meet output targets without adding floor space. Buyers scaling production will favor these platforms to lower cost per die.

Semi-automatic die bonders serve mid-volume lines where operators still guide setup and changeover. Besi product data shows its Datacon 8800 FC QUANTUM handles high-volume flows at up to 10,000 UPH. This throughput band fits customers who need speed without full automation cost. This means suppliers can upsell semi-automatic buyers toward automation as volumes rise.

Flip-chip bonders serve advanced packaging lines that need precise placement on bumped dies. ASMPT filings show placement accuracy of ±20 μm at 3 sigma in standard mode, tightening to ±12.5 μm in high-precision mode. This accuracy supports chiplet and 2.5D assembly. As a result, vendors selling flip-chip tools access the fastest-growing packaging demand pool.

Manual and lab-scale die bonders anchor research, prototyping, and low-volume specialty work. These units hold the remaining share collectively alongside the other listed machine types. This means suppliers use lab units as an entry point to build customer relationships before production-scale orders follow.

Bonding Analysis

Epoxy attach dominates with 37.5% due to low cost broad process compatibility.

In 2025, Epoxy attach held a dominant market position in the By Bonding segment of Die Attach Machine Market, with a 37.5% share. According to SEMI, global semiconductor equipment billings reached US$33.66 billion in Q3 2025, up 11% year over year. This spending supports high-volume epoxy lines across consumer devices. Buyers favor epoxy for its low cost per bond and wide material choice.

Eutectic bonding serves applications needing strong metallurgical bonds and reliable heat paths. This method suits high-reliability parts where epoxy cannot meet thermal limits. This creates a premium niche for equipment tuned to eutectic profiles. Vendors serving this space defend margin through process expertise.

Soft solder attach supports power and discrete devices that carry high current loads. Sintering and silver sintering serve the most demanding thermal cases in power modules. Hybrid and advanced bonding, including thermocompression, covers leading-edge chiplet interconnect. These methods hold the remaining share collectively, so suppliers spanning several bonding types spread risk across cycles.

Application Analysis

Logic, processors and SoCs dominate with 24.0% due to high complementary metal oxide chip volumes.

In 2025, Logic, processors and SoCs held a dominant market position in the By Application segment of Die Attach Machine Market, with a 24.0% share. Corporate documentation from EV Group shows its GEMINI 300 mm platform delivers bond force up to 350 kN for high-volume production. This capability supports large logic dies. Buyers building compute capacity will prioritize platforms proven at 300 mm scale.

Memory and stacked memory rely on precise, repeatable placement across many stacked layers. This application needs tight accuracy to protect yield on dense parts. This means suppliers with fine placement control win memory-focused customers. Vendors lacking this precision cede the segment to specialists.

Power devices and discretes rank as the fastest-growing application as electrification spreads. RF, MEMS and sensors, optoelectronics, and LED round out the remaining applications and hold their share collectively. This range means equipment makers must cover diverse die sizes and bonding needs to serve the full application base.

End-use Industry Analysis

Consumer electronics dominates with 33.0% due to massive smartphone device unit volumes.

In 2025, Consumer electronics held a dominant market position in the By End-use Industry segment of Die Attach Machine Market, with a 33.0% share. As reported by SEMI, assembly and packaging equipment sales rose 21% year over year in 2025 on advanced packaging adoption. This demand flows from high device volumes. Suppliers serving consumer lines gain scale advantages that lower unit cost.

Automotive electronics ranks as the fastest-growing end-use industry as vehicles add more chips. Electrified powertrains and driver assistance systems raise die attach content per car. This creates a durable demand stream tied to vehicle production. As a result, vendors qualifying for automotive-grade processes secure multi-year supply positions.

Industrial and power electronics, telecommunications and data center, healthcare and medical devices, and aerospace and defense hold the remaining share collectively. Each vertical carries distinct reliability and qualification demands. This means suppliers with broad process portfolios capture cross-industry orders that single-focus rivals cannot.

Key Market Segments

By Machine

- Fully-automatic die attach machines

- Semi-automatic die bonders

- Flip-chip bonders (dedicated)

- Manual / lab-scale die bonders

By Bonding

- Epoxy attach

- Eutectic bonding

- Soft solder attach

- Sintering / silver sintering

- Hybrid / advanced bonding (incl. hybrid bonding, TCB-related)

By Application

- Logic, processors & SoCs

- Memory & stacked memory

- Power devices & discretes

- RF, MEMS & sensors

- Optoelectronics

- LED

By End-use Industry

- Consumer electronics

- Automotive electronics

- Industrial & power electronics

- Telecommunications & data center

- Healthcare / medical devices

- Aerospace & defense

Regional Analysis

Asia Pacific Dominates the Die Attach Machine Market with a Market Share of 63.1%, Valued at USD 0.9 Billion

Asia Pacific leads the Die Attach Machine Market with a 63.1% share, valued at USD 0.9 Billion. The region hosts most global assembly, test, and packaging capacity. This concentration keeps equipment demand anchored in the region. As a result, suppliers must maintain local service and spare parts networks to defend share against regional rivals.

North America ranks as a fast-expanding region as reshoring adds new capacity. Federal chip incentives pulled fresh fab and assembly investment into the United States. This shift moves a slice of procurement demand westward. Therefore, vendors building U.S. sales coverage can capture greenfield orders that did not exist before recent policy action.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Market Dynamics

Market Opportunity Analysis - Emerging OSAT geographies and underused bonding niches open entry points for new players

India and Southeast Asia stand out as underexploited supply territory. Federal incentives seeded fresh OSAT capacity where established suppliers hold little installed base. This gap lets new entrants win first-fit positions before incumbents lock in service contracts. This means vendors moving early into these regions gain durable account control that later rivals cannot easily displace.

Power devices and discretes remain underserved despite fastest-growing status. Most automotive-grade lines still lean on legacy bonding rather than advanced processes. This mismatch leaves room for suppliers with high-temperature capability. As a result, investors backing specialized power-device platforms tap a segment where demand outpaces qualified supply.

Automotive electronics offers open ground within end-use demand. Its fastest-growing status has yet to attract broad supplier commitment to qualification. This creates a window for makers willing to pass strict reliability programs. Therefore, early movers secure multi-year sole-source positions as vehicle chip content climbs.

Flip-chip bonding within the machine mix stays underpenetrated at many mid-tier customers. These operators run advanced packaging without dedicated flip-chip tools. This gap signals upgrade demand as their product complexity rises. Instead of chasing only top-tier accounts, vendors can convert this mid-tier base into a steady replacement pipeline.

Technology and Innovation Landscape - Throughput, placement precision, and wafer bonding force define the competitive edge

Throughput leadership now separates the top platforms. According to ASMPT, its INFINITE bonder reaches up to 18,500 UPH in standard production mode. This speed lets high-volume customers hit output targets with fewer machines. This means suppliers competing on throughput can lower a buyer’s cost per die and win volume accounts.

Placement precision anchors advanced packaging capability. ASMPT documentation shows accuracy of ±20 μm at 3 sigma in standard mode, tightening to ±12.5 μm in high-precision mode. This control protects yield on dense dies. As a result, vendors matching this precision access chiplet and 2.5D demand that lower-tier tools cannot serve.

Wafer bonding force enables large-format production. Figures from EV Group show its GEMINI 300 mm platform delivers adjustable bond force up to 350 kN for high-volume MEMS manufacturing. This force supports 300 mm wafer output. Therefore, suppliers offering high-force platforms capture MEMS and sensor customers scaling to larger wafers.

Reflow flip-chip systems widen high-volume packaging reach. Besi data shows its Datacon 8800 FC QUANTUM handles integrated circuit flows at up to 10,000 UPH. This capacity fits demanding advanced packaging lines. This means vendors with proven reflow platforms defend share in the fastest-moving packaging segments.

Drivers

Global semiconductor capacity expansion drives back-end equipment procurement. National programs funded a fresh wave of fab and assembly build-out through 2022 to 2025. The U.S. CHIPS and Science Act allocated about USD 52.7 billion and catalyzed announced investment above USD 200 billion through 2025. Each new facility requires a full die attach machine complement. This means suppliers face multi-year order cycles tied to every greenfield tool-in.

Regional programs widen the demand base further. The European Chips Act targets lifting Europe’s manufacturing share from about 9% to 20% by 2030, mobilizing an estimated EUR 43 billion. India approved three projects with incentive commitments near INR 1.26 trillion through 2024. Each medium-scale facility needs 40 to 120 die attach units. Therefore, vendors with regional reach capture direct procurement events worth USD 8 to 80 million each.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global Semiconductor Capacity Expansion & Fab Proliferation Driving Back-End Equipment Procurement | +2.60% | United States, Taiwan, South Korea, Japan, China, Europe, India | Short term (≤ 2 years) |

| Advanced Packaging Migration (Flip Chip, 2.5D/3D IC) Requiring High-Precision Die Attach Platforms | +1.80% | Taiwan, South Korea, United States, Japan, China | Short term (≤ 2 years) |

| Automotive Semiconductor Demand Growth for Power Modules & ADAS Die Attach Applications | +1.20% | Germany, Japan, United States, China, South Korea | Medium term (2–4 years) |

| AI Accelerator & HPC Chip Demand Accelerating Advanced Die Placement Volume at Leading OSATs | +1.05% | Taiwan, United States, South Korea, Malaysia, China | Short term (≤ 2 years) |

| SiC & GaN Power Device Volume Ramp Requiring Specialised High-Temperature Die Attach Processes | +0.65% | United States, Germany, Japan, China, South Korea | Medium term (2–4 years) |

| Government Semiconductor Self-Sufficiency Incentives Expanding OSAT & IDM Capacity in New Geographies | +0.52% | India, United States, European Union, Japan, Israel | Medium term (2–4 years) |

Restraints

Export controls restrict China market access for advanced equipment. The U.S. Bureau of Industry and Security issued sweeping controls in October 2022 and October 2023. Japan and the Netherlands harmonized parallel rules in 2023. China held an estimated 25% to 32% of global back-end equipment demand through 2020 to 2022. This means restricted access removes the single largest national end-market from reach.

The access drag forces suppliers to redirect sales. Restrictions suppress the addressable order pipeline by an estimated USD 300 to 600 million annually for non-Chinese makers. Compliance risk pushed several suppliers into voluntary sales pauses pending legal review. As a result, vendors accelerate diversification toward Southeast Asia, India, and U.S. reshoring customers to offset lost China revenue.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| US & Allied Export Controls on Advanced Semiconductor Equipment Restricting China Market Access | -1.60% | China — demand-side; United States, Japan, Netherlands — supply-side | Short term (≤ 2 years) |

| Semiconductor Capex Cyclicality & Inventory Correction-Driven Equipment Order Deferrals | -1.10% | Global — concentrated among memory and consumer IC-exposed OSATs | Short term (≤ 2 years) |

| High Unit Capital Cost Constraining Adoption by Smaller & Emerging Market OSAT Operators | -0.65% | India, Southeast Asia, Eastern Europe — nascent OSAT ecosystems | Medium term (2–4 years) |

| Geopolitical Supply Chain Fragmentation Increasing Dual-Sourcing & Qualification Cost for Buyers | -0.42% | Global — most acute for Taiwan-dependent and China-exposed OSAT operators | Medium term (2–4 years) |

Challenges

Sub-micron placement accuracy raises yield complexity. Advanced packaging migration pushes placement demand toward ±1 to 3 microns at 3 sigma, against ±10 to 25 microns for conventional wire bond attach. This specification sits at the edge of commercial precision technology. This means smaller vendors struggle to compete at the accuracy frontier.

Yield sensitivity ties machine performance to customer profit. Each 1% yield gain is worth roughly USD 1,500,000 to 8,000,000 per month at high volumes. Leading suppliers spend an estimated 12% to 18% of revenue on R&D to hold position. As a result, only the top 4 to 6 suppliers sustain this pace, pushing smaller makers into defensible niches.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Sub-Micron Placement Accuracy & Yield Optimisation Complexity | -1.10% | Global — most acute at leading advanced packaging OSATs in Taiwan, South Korea | Long term (≥ 4 years) |

| Sintering & Thermocompression Process Qualification Lead Time | -0.85% | Germany, Japan, United States — power device & automotive semiconductor segments | Medium term (2–4 years) |

| Precision Motion & Vision System Component Supply Concentration | -0.70% | Global — linear motor, camera module & granite base sourcing concentrated in Japan & Germany | Long term (≥ 4 years) |

| Skilled Process Engineering Talent Shortage at OSAT Customer Sites | -0.52% | United States, Europe, India, Southeast Asia — nascent capacity regions | Long term (≥ 4 years) |

| Heterogeneous Integration Roadmap Uncertainty Delaying Platform Investment Decisions | -0.38% | Global — advanced packaging customers in Taiwan, United States, South Korea | Medium term (2–4 years) |

Opportunities

Sintered silver and copper die attach open high-reliability power module white space. As of 2025 to 2026, sintering stayed a minority production technology despite superior performance. Silver sintering delivers thermal conductivity near 200 to 250 W/m·K against 30 to 55 W/m·K for solder. This enables 5 to 10 times longer power cycling life. This means early movers capture EV power module demand before rivals qualify.

Sintering machines command premium economics. These units carry ASPs of USD 800,000 to 2,500,000 against USD 150,000 to 600,000 for conventional platforms, at gross margins of 52% to 62%. Fewer than 5 to 8 suppliers had volume-proven platforms by 2025. As a result, qualified vendors win 3 to 5 year sole-source positions worth USD 200,000 to 600,000 in annual recurring revenue per line.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Sintered Silver & Copper Die Attach for EV Power Module High-Reliability Applications | +1.80% | Germany, Japan, United States, China, South Korea | Medium term (2–4 years) |

| Hybrid Bonding & Thermocompression Platform Development for Sub-1µm Chiplet Interconnect | +1.30% | Taiwan, United States, South Korea, Japan | Long term (≥ 4 years) |

| India & Southeast Asia Greenfield OSAT Equipment Supply Partnerships | +0.85% | India, Malaysia, Vietnam, Thailand, Indonesia | Short term (≤ 2 years) |

| Equipment-as-a-Service & Process Guarantee Contracting for Tier-2 OSAT Operators | +0.65% | Southeast Asia, India, Eastern Europe — emerging OSAT capacity regions | Long term (≥ 4 years) |

| Photonics & Silicon Photonics Die Attach for Optical Transceiver & Datacom Packaging | +0.48% | United States, Japan, Taiwan, Netherlands, South Korea | Medium term (2–4 years) |

Key Company Insights

BE Semiconductor Industries N.V. anchors its position in advanced flip-chip packaging. Its Datacon 8800 FC QUANTUM handles high-volume flows at up to 10,000 UPH. This throughput serves leading integrated circuit packaging lines. As reported by SEMI, equipment billings reached US$33.07 billion in Q2 2025, up 24% year over year. This demand strength supports the firm’s advanced platform investment and forward order visibility.

ASM Pacific Technology Ltd. competes through throughput leadership and advanced bonding. Its INFINITE bonder reaches up to 18,500 UPH in standard mode. In 2025, ASMPT secured orders for fifteen chip-to-substrate thermocompression bonding tools, expanding its packaging business. According to SIA, U.S.-headquartered firms generated US$318.2 billion in 2024 sales, up 20.0%. This demand base strengthens the case for its advanced capacity buildout.

Key Players

- BE Semiconductor Industries N.V. (Besi)

- ASM Pacific Technology Ltd. (ASMPT)

- Kulicke & Soffa Industries Inc.

- Palomar Technologies Inc.

- Shinkawa Ltd.

- MRSI Systems (Mycronic AB)

- Dr. Tresky AG

- Fasford Technology Co. Ltd.

- Finetech GmbH & Co. KG

- HYBOND Inc.

- West-Bond Inc.

- MicroAssembly Technologies Ltd. (MAT)

- Smart Equipment Technology

- SUSS MicroTec SE

- Shibaura Mechatronics

- Others

Recent Developments

- January 2025: Yamaha Robotics Holdings announced the merger of SHINKAWA LTD., APIC YAMADA CORPORATION, and PFA CORPORATION into Yamaha Robotics Co., Ltd. to strengthen its semiconductor back-end equipment business, including die attach and die bonding equipment.

- June 2025: Yamaha Robotics Co., Ltd. announced its medium to long-term management plan, stating it will increase investment in advanced semiconductor back-end equipment and develop new platform models for the semiconductor packaging business, which includes die bonders.

Geopolitical Impact Analysis

Trade tensions reshape semiconductor equipment flows and pricing. According to the WTO, world merchandise trade volume growth stayed near 2.7% in 2025 as tariff friction spread. Export controls tied to China cover a market once holding an estimated 25% of back-end equipment demand. This forces die attach suppliers to reroute sales and qualify new logistics paths. As a result, buyers face longer procurement timelines and higher qualification cost.

Supply chain rerouting lifts logistics cost for precision components. As reported by UNCTAD, container freight rate indices climbed sharply through 2025, with some routes up more than 60% against prior levels. Die attach platforms rely on linear motors and vision modules sourced from Japan and Germany. This concentration raises exposure to transit delay and freight volatility. Therefore, vendors build dual-sourcing buffers to protect delivery schedules.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1.5 Billion |

| Forecast Revenue (2035) | USD 3.0 Billion |

| CAGR (2026-2035) | 7.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Machine (Fully-automatic die attach machines, Semi-automatic die bonders, Flip-chip bonders, Manual / lab-scale die bonders), By Bonding (Epoxy attach, Eutectic bonding, Soft solder attach, Sintering / silver sintering, Hybrid / advanced bonding), By Application (Logic, processors & SoCs, Memory & stacked memory, Power devices & discretes, RF, MEMS & sensors, Optoelectronics, LED), By End-use Industry (Consumer electronics, Automotive electronics, Industrial & power electronics, Telecommunications & data center, Healthcare / medical devices, Aerospace & defense) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | BE Semiconductor Industries N.V. (Besi), ASM Pacific Technology Ltd. (ASMPT), Kulicke & Soffa Industries Inc., Palomar Technologies Inc., Shinkawa Ltd., MRSI Systems (Mycronic AB), Dr. Tresky AG, Fasford Technology Co. Ltd., Finetech GmbH & Co. KG, HYBOND Inc., West-Bond Inc., MicroAssembly Technologies Ltd. (MAT), Smart Equipment Technology, SUSS MicroTec SE, Shibaura Mechatronics, Others |

| Customization Scope | Customization for segments, region / country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License | Multi-User License (Up to 5 Users) | Corporate Use License (Unlimited User and Printable PDF) |