Global Dermaplaning Tools Market Size, Share, Growth Analysis By Product (Facial Razors, Dermaplaning Scrapers, Dermaplaning Refills, Others), By Application (Individuals, Professionals), By End Use (Women, Men), By Distribution Channel (Specialty Beauty Stores, Supermarkets & Hypermarkets, Pharmacies & Drugstores, Online, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 180021

- Number of Pages: 313

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

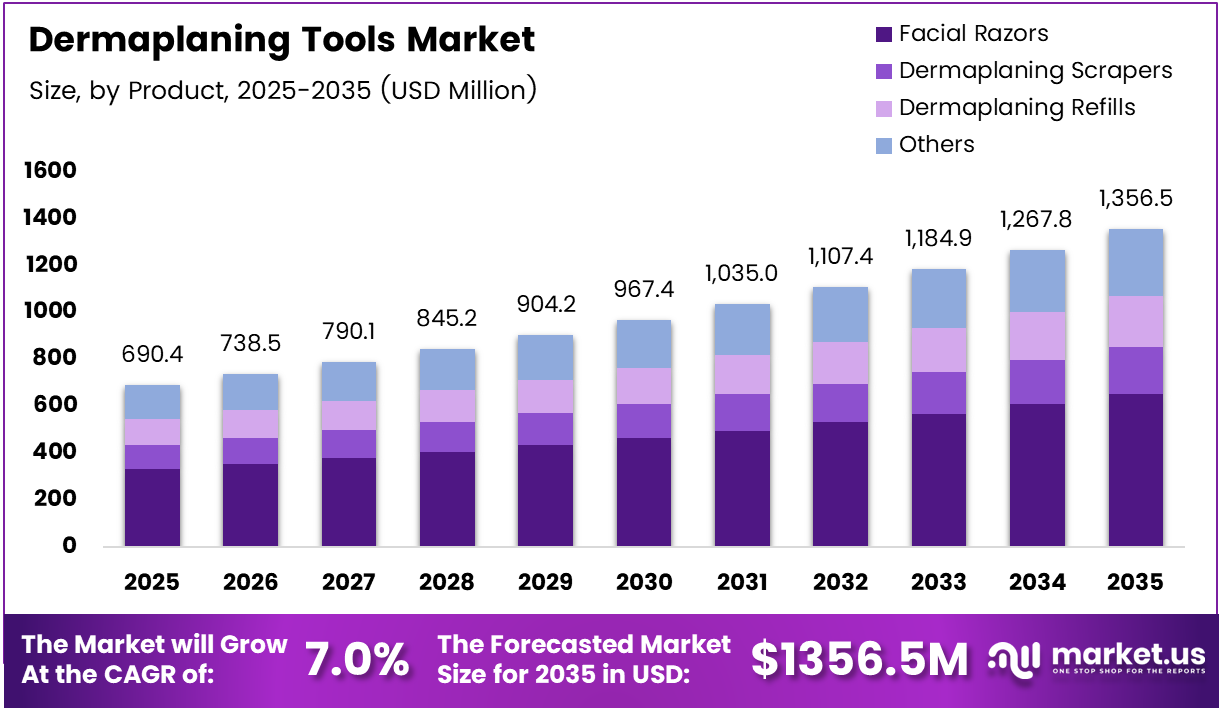

Global Dermaplaning Tools Market size is expected to be worth around USD 1,356.5 Million by 2035 from USD 690.4 Million in 2025, growing at a CAGR of 7.0% during the forecast period 2026 to 2035.

The dermaplaning tools market covers manual and sonic-powered devices used for facial exfoliation and vellus hair removal. These tools serve both at-home consumers and licensed professionals. The segment spans facial razors, dermaplaning scrapers, and refill accessories sold across specialty beauty retailers, pharmacies, and e-commerce platforms.

Consumer interest in non-invasive skincare treatments has redirected spending from clinic visits toward at-home precision tools. This behavioral shift creates a durable demand floor for device manufacturers and refill suppliers. The economics favor recurring revenue models, as blades and replacement heads generate repeat purchases beyond the initial device sale.

Social media continues to reshape purchase decisions in this category. Beauty content featuring dermaplaning routines on platforms like TikTok and Instagram has shortened consumer education timelines significantly. Brands that align with influencer distribution channels now reach engaged buyers who arrive with purchase intent rather than awareness alone.

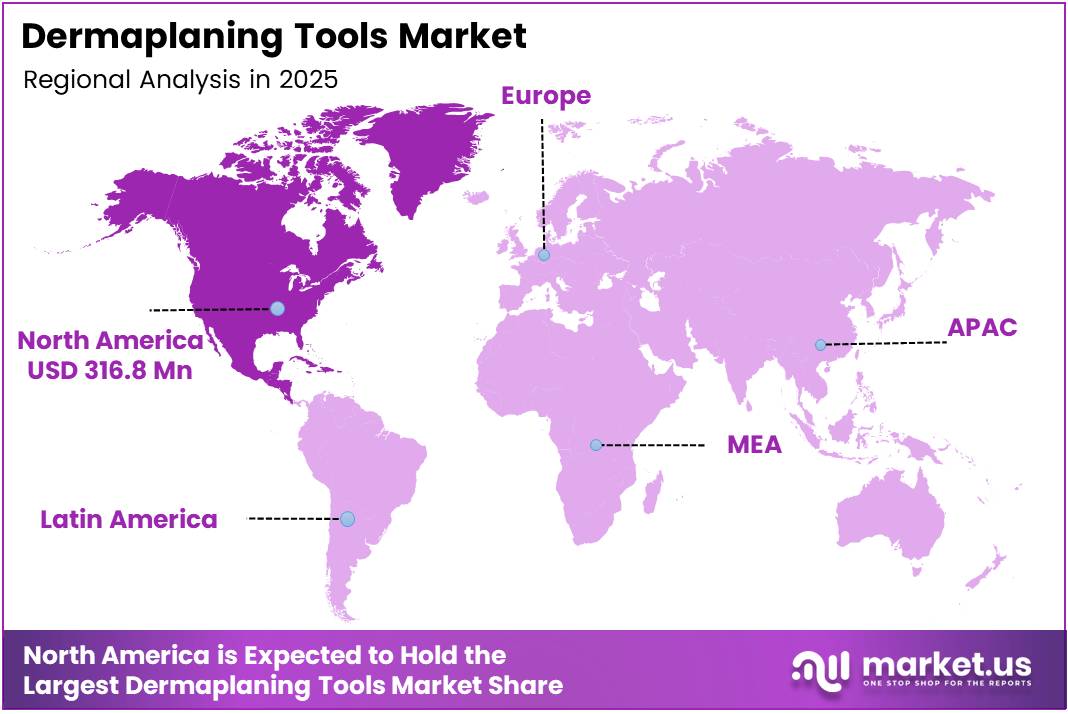

North America leads all regions with a 45.90% share, valued at approximately USD 316.8 Million in 2025. This position reflects early market development, high per-capita beauty spending, and established retail infrastructure. As similar conditions develop in Western Europe, North America’s lead signals where other geographies are heading rather than where the market’s next growth will come from.

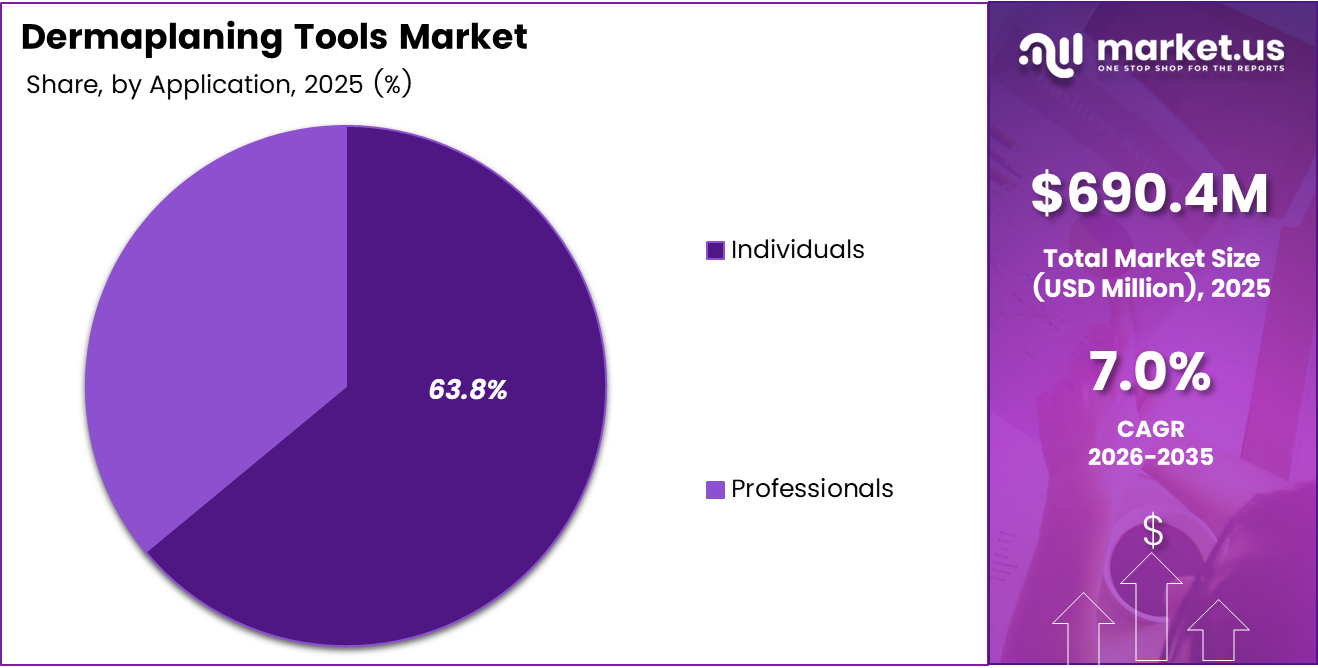

Women represent 77.3% of end-users, and the individual consumer segment holds 63.8% of application share. These figures confirm that at-home use drives volume. Brands targeting professional channels face a structurally smaller addressable market, though that segment commands higher average unit values and generates brand credibility that cascades into retail demand.

According to Nimbi, 97% of users strongly agreed the facial dermaplaner made their skin feel smoother after use. This near-universal satisfaction rate tells a clear story: product efficacy is not a barrier in this market. The challenge for brands is now distribution, discovery, and price positioning rather than convincing consumers the category delivers results.

According to Nimbi, 93% of users strongly agreed the tool performed well in removing peach fuzz and exfoliating. High performance scores across independent brands signal category maturity. In 2025, Nimbi’s eco-friendly dermaplaners sold out in the United Kingdom within 24 hours of launch, confirming that product-market fit in new geographies can convert rapidly when pricing and positioning align with consumer expectations.

Key Takeaways

- The Global Dermaplaning Tools Market was valued at USD 690.4 Million in 2025 and is forecast to reach USD 1,356.5 Million by 2035.

- The market advances at a CAGR of 7.0% during the forecast period 2026 to 2035.

- By Product, Facial Razors dominate with a 47.9% share in 2025.

- By Application, Individuals lead with a 63.8% share, reflecting strong at-home usage behavior.

- By End Use, Women account for 77.3% of the market in 2025.

- By Distribution Channel, Specialty Beauty Stores hold the highest share at 34.6%.

- North America dominates regionally with a 45.90% share, valued at USD 316.8 Million.

Product Analysis

Facial Razors dominate with 47.9% due to broad retail availability and low entry price.

In 2025, Facial Razors held a dominant market position in the By Product segment of the Dermaplaning Tools Market, with a 47.9% share. Their accessibility across mass retail and pharmacy channels, combined with a sub-USD-10 price point for entry-level options, makes them the default first purchase for new consumers entering the category. This volume leadership also drives the highest refill attachment rates.

Dermaplaning Scrapers carry a higher average selling price and serve consumers seeking a more structured exfoliation experience. These devices typically feature ergonomic handles and replaceable blades, appealing to buyers who have moved past single-use razors. According to DERMAFLASH, 100% of users of the LUXE+ sonic device reported instant improvement in skin texture after just one treatment — a data point that justifies premium pricing for performance-driven scraper formats.

Dermaplaning Refills represent the most structurally valuable sub-segment for manufacturers pursuing recurring revenue. Refill sales create predictable cash flow tied to active device users. As device penetration rises, refill volumes scale proportionally — making this segment increasingly important to long-term margin profiles. Brands that lock users into proprietary blade systems gain a durable competitive advantage over commodity razor formats.

Others within the product category include multi-functional tools and accessory kits that bundle dermaplaning blades with complementary skincare items. In October 2024, Estrid launched its first dermaplaning face razor featuring diamond-coated blades and a weighted ergonomic handle, signaling that accessory-adjacent innovations are raising consumer expectations for tactile quality across the broader category.

Application Analysis

Individuals dominate with 63.8% due to high at-home skincare routine adoption.

In 2025, Individuals held a dominant market position in the By Application segment of the Dermaplaning Tools Market, with a 63.8% share. This reflects a decisive shift of consumers performing professional-grade exfoliation treatments at home. The implication for brands is clear: product design, packaging, and communication must prioritize ease of use and safety for non-professional hands, not clinic-grade technical performance.

Professionals — including estheticians, dermatologists, and spa therapists — represent a smaller share but disproportionate influence on product credibility. Professional endorsements and clinic-sourced recommendations shape consumer product choices in retail channels. Brands that build clinical validation and maintain professional relationships create trust signals that accelerate retail uptake among individual buyers.

End Use Analysis

Women dominate with 77.3% due to established facial grooming and skincare routine behavior.

In 2025, Women held a dominant market position in the By End Use segment of the Dermaplaning Tools Market, with a 77.3% share. Women’s skincare routines create natural entry points for dermaplaning tools as a complement to existing cleansing and moisturizing steps. This deep behavioral integration means product switching costs are low, but brand loyalty — when earned — proves durable across product categories.

Men represent an underpenetrated but structurally expanding segment. Social media normalization of male skincare routines, combined with the rise of gender-neutral grooming brands, has lowered adoption barriers. Leaf Shave’s September 2024 “Beyond the Razor” campaign, which tied dermaplaner sales to PCOS awareness, demonstrated how cause-based marketing can expand category conversation beyond a traditionally female audience.

Distribution Channel Analysis

Specialty Beauty Stores dominate with 34.6% due to expert staff and curated brand environments.

In 2025, Specialty Beauty Stores held a dominant market position in the By Distribution Channel segment of the Dermaplaning Tools Market, with a 34.6% share. These stores provide a high-consideration environment where trained staff guide first-time buyers. For dermaplaning brands, specialty retail placement functions as both a revenue channel and a credibility signal that reinforces premium positioning across all other touchpoints.

Supermarkets and Hypermarkets serve volume-sensitive consumers seeking convenience and accessible price points. This channel drives facial razor sales in particular, where purchase decisions are low-involvement and brand familiarity matters more than expert guidance. Supermarket placement expands reach into consumers who would never visit a specialty retailer, widening the total addressable buyer pool at the cost of margin compression.

Pharmacies and Drugstores benefit from consumer trust in health and personal care contexts. Shoppers visiting these outlets for skincare often respond to adjacent dermaplaning products positioned alongside facial cleansers and exfoliants. This channel is especially effective for brands that emphasize dermatologist-approved messaging or clinical safety credentials.

Online retail has restructured how new dermaplaning brands enter markets without traditional retail infrastructure. Direct-to-consumer e-commerce enables precise targeting of skincare-interested consumers through digital content and influencer channels. Nimbi’s UK sell-out within 24 hours of launch occurred via online distribution — demonstrating that digital-first entry strategies can generate rapid volume when consumer awareness is already established through social media.

Others in distribution include professional salon supply wholesalers and subscription beauty box services. These channels serve niche but high-engagement audiences. Subscription models in particular create recurring revenue structures and reduce customer acquisition cost over multi-cycle relationships.

Key Market Segments

By Product

- Facial Razors

- Dermaplaning Scrapers

- Dermaplaning Refills

- Others

By Application

- Individuals

- Professionals

By End Use

- Women

- Men

By Distribution Channel

- Specialty Beauty Stores

- Supermarkets & Hypermarkets

- Pharmacies & Drugstores

- Online

- Others

Drivers

Social Media-Fueled At-Home Skincare Behavior Expands the Consumer Base for Dermaplaning Devices

Consumer preference for at-home facial exfoliation has shifted from a niche behavior to a mainstream skincare practice. Beauty tutorials on TikTok and Instagram have reduced the knowledge gap that previously limited dermaplaning to professional settings. This democratization of technique directly expands the addressable market beyond salon clients to everyday skincare consumers.

Influencer-led content creates purchase intent rather than just awareness. According to DERMAFLASH, 100% of users observed effective peach fuzz removal after a single use of the LUXE+ device. User results this immediate and visible generate shareable content that multiplies organic brand reach — a compounding marketing mechanism that paid advertising alone cannot replicate. In September 2024, Leaf Shave’s campaign tied product sales to PCOS awareness, demonstrating how mission-aligned marketing drives both discovery and conversion simultaneously.

The global skincare and personal grooming industry provides structural tailwinds for precision beauty tools. Rising disposable income in emerging markets and growing awareness of non-invasive cosmetic options expand the universe of potential buyers. Brands that entered this market early now hold significant advantages in brand recognition and retail shelf space as new consumer cohorts begin their dermaplaning journey.

Restraints

Safety Risks and Alternative Treatment Competition Limit Mass-Market Adoption of Dermaplaning Tools

Improper use of dermaplaning tools creates tangible risks including cuts, skin irritation, and infection. These outcomes generate negative reviews and consumer hesitation, particularly among first-time buyers who lack professional guidance. For brands, this means that inadequate safety design or insufficient user education directly translates into returns, reputational damage, and category abandonment.

According to Nimbi, 97% of dermaplaning tool users strongly agreed they experienced no discomfort within 48 hours after use. While this figure validates well-designed tools, it also highlights that discomfort perception remains a key purchase barrier across the category. Brands that fail to invest in safety-guard design or post-purchase education face avoidable conversion losses at the point of repurchase.

Alternative treatments — including laser hair removal, waxing, and chemical peels — compete directly for the same consumer spending. Many of these alternatives offer longer-lasting results with professional oversight, which appeals to consumers willing to pay for convenience and permanence. Dermaplaning’s value proposition depends on its low cost and at-home convenience, factors that become less compelling as competing treatments grow more accessible.

Growth Factors

Product Innovation, E-Commerce Expansion, and Sustainability Preferences Open New Revenue Channels

Ergonomic, reusable, and safety-guarded dermaplaning devices address the primary barriers that deter cautious first-time buyers. Manufacturers investing in handle design, blade geometry, and skin-contact safety features can command premium pricing while reducing negative use experiences. This segment of product innovation directly converts a restraint — safety concern — into a competitive differentiator.

E-commerce platforms remove the geographic and shelf-space constraints that limit traditional retail distribution. Direct-to-consumer channels enable brands to build proprietary customer data, execute personalized replenishment campaigns, and manage margin without retailer intermediaries. According to DERMAFLASH, 97% of users saw brighter, more radiant skin after treatment — a result type that photographs well, drives user-generated content, and converts social media engagement into measurable online sales.

Dermatology clinics and medical spas adopting professional dermaplaning services create downstream demand for consumer-grade products. Patients who experience professional treatments frequently seek at-home maintenance tools between appointments. This clinical-to-consumer pipeline represents a high-intent acquisition channel. Simultaneously, demand for sustainable personal care tools opens a product line opportunity for brands willing to invest in biodegradable materials and refillable formats.

Emerging Trends

Multi-Functional Tools and Gender-Neutral Positioning Reshape Consumer Expectations Across the Category

Dermatologist-recommended skincare tools are integrating into daily beauty routines rather than remaining in the category of occasional treatments. This behavioral shift means consumers now expect dermaplaning devices to complement — not compete with — their existing cleanser, serum, and moisturizer steps. Brands positioned within a broader skincare routine rather than as standalone tools earn higher purchase frequency and basket attachment.

The development of multi-functional skincare devices combining dermaplaning with micro-exfoliation features raises the category’s perceived value and justifies higher price thresholds. In August 2025, Michael Todd Beauty launched the Sonicsmooth Pro+ dermaplaning device, delivering professional-style sonic exfoliation at home. This product direction signals that device convergence — rather than single-function tools — defines where consumer expectations are heading.

According to DERMAFLASH, 94% of users experienced a reduced appearance of dark spots after four weeks of consistent use. Results of this type — measurable skin improvements tied to continued use — create the behavioral foundation for subscription refill models and multi-SKU product journeys. Gender-neutral grooming positioning further expands the addressable audience, with male consumer participation beginning to add incremental volume to a category previously defined by a single demographic.

Regional Analysis

North America Dominates the Dermaplaning Tools Market with a Market Share of 45.90%, Valued at USD 316.8 Million

North America holds a 45.90% share valued at USD 316.8 Million, driven by early consumer adoption, mature specialty beauty retail infrastructure, and high per-capita spending on personal grooming. The United States leads category innovation, with most major product launches and brand campaigns originating domestically before extending internationally. This structural advantage positions North America as both the largest and most competitive regional market.

Europe Dermaplaning Tools Market Trends

Europe shows consistent category development, supported by a strong wellness culture and growing consumer familiarity with at-home facial care tools. The United Kingdom demonstrates accelerating uptake — illustrated by Nimbi’s sell-out within 24 hours of its UK launch in 2025. Germany and France contribute steady professional channel volume through established dermatology clinic networks and specialty beauty retail chains.

Asia Pacific Dermaplaning Tools Market Trends

Asia Pacific represents the most significant long-term volume opportunity as skincare culture deepens across China, South Korea, India, and Southeast Asia. South Korea’s established beauty technology influence and China’s massive e-commerce infrastructure create natural entry points for dermaplaning brands expanding beyond Western markets. Rising middle-class spending on premium personal care accelerates product consideration across the region.

Latin America Dermaplaning Tools Market Trends

Latin America shows early-stage category development, with Brazil and Mexico representing the primary consumer markets. Growing e-commerce penetration and rising urban consumer interest in professional-grade at-home skincare tools are building the foundation for future volume. Distribution constraints in traditional retail channels make digital-first market entry the most viable strategy for international brands entering this region.

Middle East and Africa Dermaplaning Tools Market Trends

The Middle East and Africa region demonstrates selective but high-value demand, particularly across GCC countries where premium beauty spending per capita is among the highest globally. Urbanization and expanding modern retail formats in South Africa are gradually broadening consumer access to facial grooming tools. Cultural preferences for facial hair removal create a structurally receptive consumer environment for dermaplaning category growth.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Dermaflash has built its market position around clinically validated sonic exfoliation technology. The LUXE+ device operates at 14,000 sonic vibrations per minute, a proprietary specification that anchors premium pricing and differentiates the brand from commodity razor formats. In 2025, Dermaflash extended this technology with improved safety edge blades and enhanced vibration performance, reinforcing its technical authority as competitors enter the professional-grade home device segment.

StackedSkincare positions itself at the intersection of professional skincare tools and consumer accessibility. Its strategy focuses on offering clinic-adjacent product lines that appeal to consumers who follow dermatologist-recommended routines. This positioning creates brand credibility in a category where safety perception directly influences purchase decisions, giving StackedSkincare a defensible advantage over mass-market facial razor brands competing on price alone.

Tinkle USA occupies the high-volume, low-price end of the dermaplaning tools spectrum, where facial razors dominate and purchase frequency drives revenue. Its broad retail availability across pharmacies and supermarkets makes it a default choice for first-time buyers. While margin per unit is modest, Tinkle’s volume leadership in accessible price tiers gives it unmatched consumer reach and strong shelf positioning in mass retail environments.

Edgewell Personal Care brings established personal care manufacturing infrastructure and global retail relationships to the dermaplaning category. Its ability to scale production, manage multi-region distribution, and invest in consumer safety R&D gives it structural advantages that smaller specialty brands cannot match. Edgewell’s presence signals category maturation — when large personal care conglomerates enter a niche beauty segment, it confirms that consumer demand has reached commercially meaningful scale.

Key Players

- Dermaflash

- StackedSkincare

- Tinkle USA

- Edgewell Personal Care

- KITSCH

- Leaf Shave

- Offspring Beauty Co.

- Tweezerman International, LLC

- ennva

Recent Developments

- January 2024 – Billie launched the Dermaplane Starter Kit, expanding its skincare portfolio with an at-home dermaplaning tool featuring a reusable handle and replaceable blades designed for facial exfoliation and peach-fuzz removal.

- January 2024 – Harry’s Inc. brand Flamingo introduced the Flamingo Dermaplane Razor, a precision facial razor with Japanese stainless-steel blades and safety guards to improve at-home dermaplaning safety for everyday consumers.

- August 2025 – Michael Todd Beauty launched the Sonicsmooth Pro+ dermaplaning device, an upgraded sonic exfoliation tool designed to deliver professional-style dermaplaning treatments at home with enhanced performance features.

- 2025 – DERMAFLASH expanded its dermaplaning device lineup with updated sonic exfoliation technology, introducing improved safety edge blades and enhanced vibration technology for professional-grade home treatments across its product range.

Report Scope

Report Features Description Market Value (2025) USD 690.4 Million Forecast Revenue (2035) USD 1,356.5 Million CAGR (2026-2035) 7.0% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product (Facial Razors, Dermaplaning Scrapers, Dermaplaning Refills, Others), By Application (Individuals, Professionals), By End Use (Women, Men), By Distribution Channel (Specialty Beauty Stores, Supermarkets & Hypermarkets, Pharmacies & Drugstores, Online, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Dermaflash, StackedSkincare, Tinkle USA, Edgewell Personal Care, KITSCH, Leaf Shave, Offspring Beauty Co., Tweezerman International LLC, ennva Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Dermaflash

- StackedSkincare

- Tinkle USA

- Edgewell Personal Care

- KITSCH

- Leaf Shave

- Offspring Beauty Co.

- Tweezerman International, LLC

- ennva

Our Clients

- 180021

- Feb 2026