Global Dealer Finance Market Size, Share and Analysis Report By Type (Retail Financing, Wholesale Financing, Leasing, Others), By Service Provider (Banks, NBFCs, OEM Captive Finance, Others), By Vehicle Type (Passenger Vehicles, Commercial Vehicles, Two-Wheelers, Others), By Channel (Direct, Indirect), By End-User (Dealers, Customers), By Regional Analysis, Global Trends and Opportunity, Future Outlook By 2025-2035

- Published date: Feb. 2026

- Report ID: 179634

- Number of Pages: 356

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Key Takeaway

- Financing Trends (Q1 2025)

- China Dealer Finance Market Size

- Type Analysis

- Service Provider Analysis

- Vehicle Type Analysis

- Channel Analysis

- End-User Analysis

- Investment and Business Benefits

- Emerging Trends

- Growth Factors

- Key Market Segments

- Drivers

- Restraint

- Opportunities

- Challenges

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

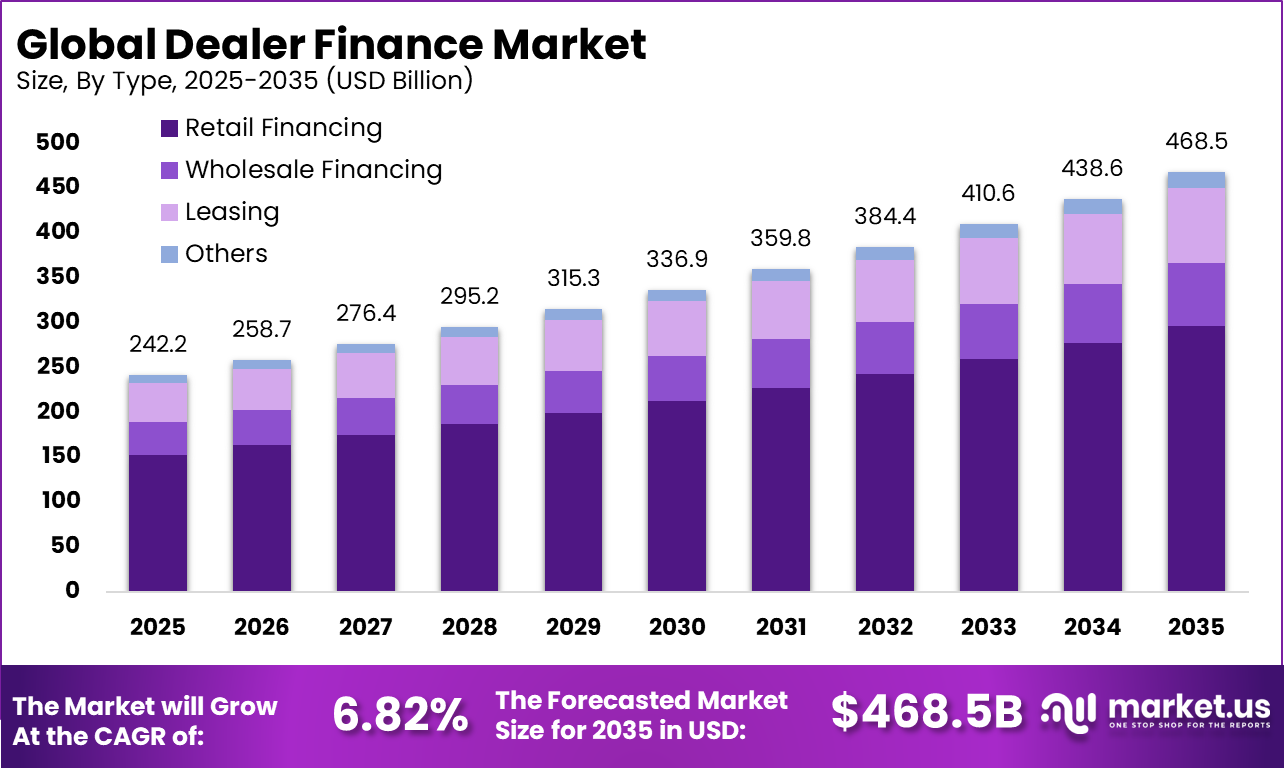

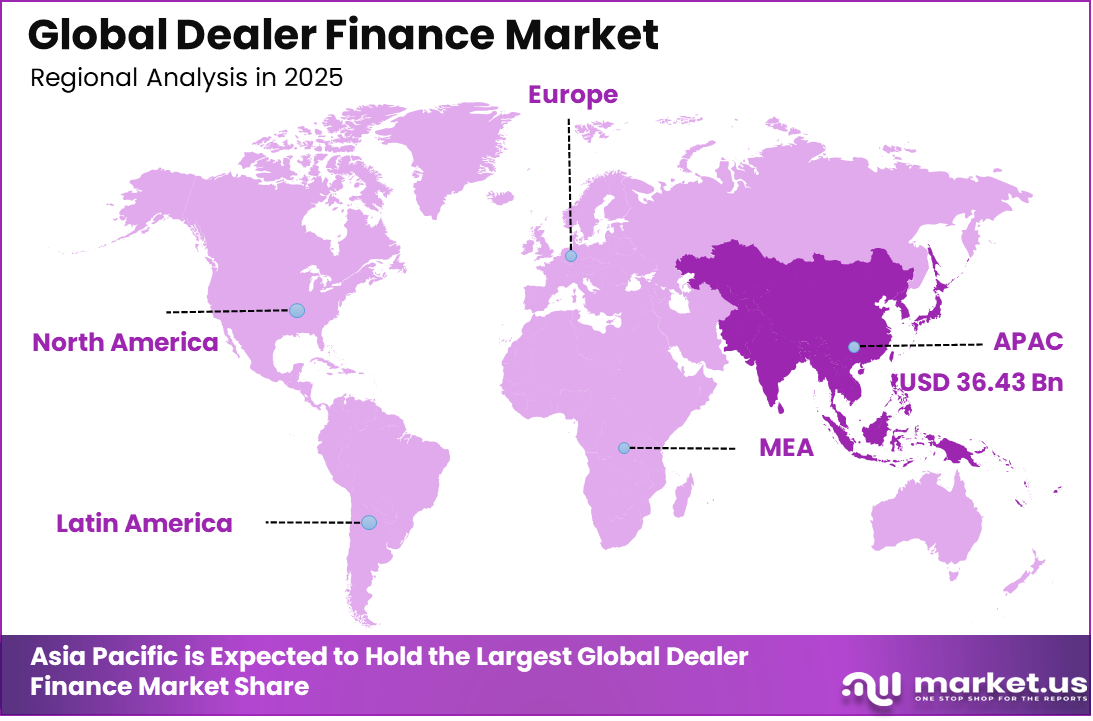

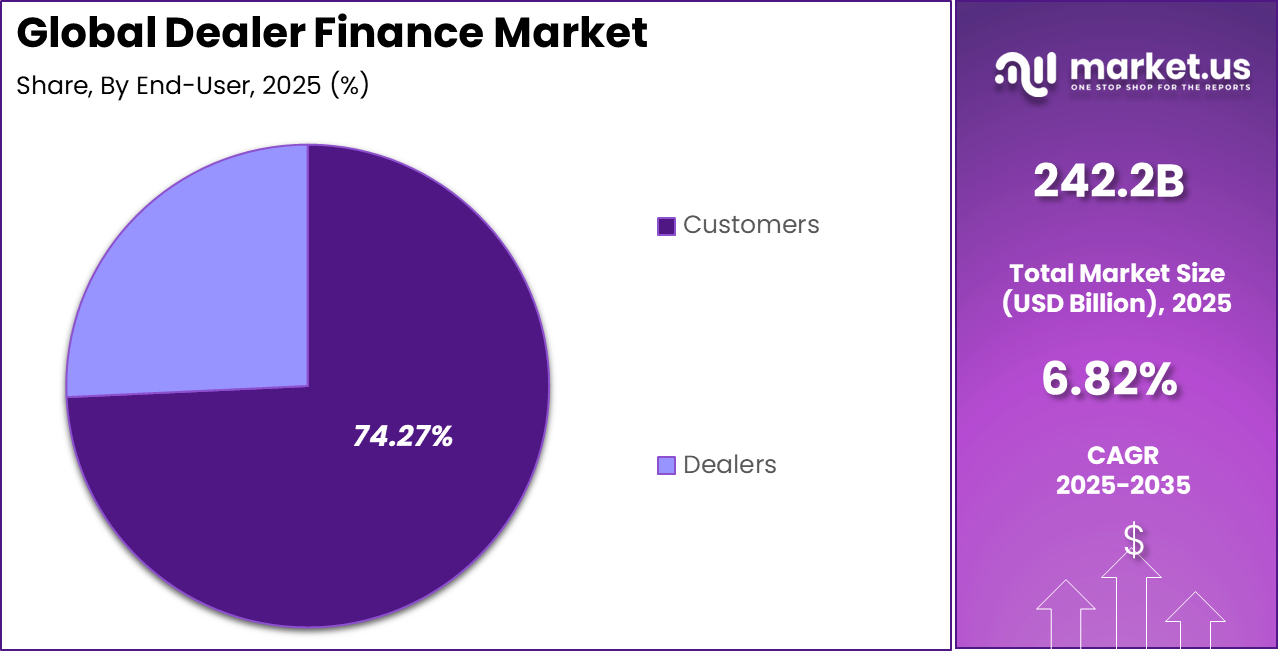

The Global Dealer Finance Market size is expected to be worth around USD 468.5 billion by 2035, from USD 242.2 billion in 2025, growing at a CAGR of 6.82% during the forecast period from 2025 to 2035. Asia Pacific held a dominant market position, capturing more than a 36.43% share, holding USD 88.2 billion in revenue.

Dealer finance is a structured lending model where dealerships arrange credit for customers directly at the point of sale. Nearly 75% of new vehicle purchases globally involve dealer arranged financing, showing its strong role in automotive retail. It allows buyers to complete vehicle purchases quickly while helping dealers secure immediate payment. This system improves transaction speed, simplifies paperwork, and supports smoother coordination between lenders and dealerships.

The main drivers of dealer finance include rising vehicle ownership, growing consumer preference for easy credit access, and digital loan processing systems. Over 60% of borrowers prefer financing arranged at dealerships due to faster approvals and convenience. Increasing smartphone penetration and online documentation tools have reduced loan processing time significantly. Flexible repayment options and competitive interest structures further encourage customers to choose dealer based financing solutions.

The market for Dealer Finance is growing due to increasing vehicle ownership and rising customer preference for manageable monthly payments instead of full upfront costs. Convenient financing at the dealership, faster approvals, and flexible loan options make vehicle purchases easier. Expanding digital tools and mobile applications also simplify loan processing, attracting more buyers and supporting steady growth in dealer arranged financing.

Demand for dealer finance remains strong from both buyers and dealerships. Around two thirds of vehicle buyers rely on financing rather than full cash payments. Dealers require steady cash flow to maintain inventory and meet supplier obligations. Financing solutions help bridge this gap by ensuring immediate fund transfers. Customers also seek predictable monthly payments, which makes structured dealer finance an attractive and practical purchase option.

For instance, in January 2026, GM Financial gained FDIC approval alongside Ford Credit to launch GM Financial Bank in Utah, focusing on retail installment contracts from dealers. This move enhances liquidity for nationwide auto financing, building on GM’s dealer network to streamline loans and deposits via digital channels. It’s a smart play to capture more middle-market volume amid rising EV demand.

Key Takeaway

- In 2025, the Retail Financing segment held a dominant market position, capturing a 63.24% share of the Global Dealer Finance Market.

- In 2025, the Banks segment held a dominant market position, capturing a 45.9% share of the Global Dealer Finance Market.

- In 2025, the Passenger Vehicles segment held a dominant market position, capturing a 65.82% share of the Global Dealer Finance Market.

- In 2025, the Indirect segment held a dominant market position, capturing a 70.5% share of the Global Dealer Finance Market.

- In 2025, the Customers segment held a dominant market position, capturing a 74.27% share of the Global Dealer Finance Market.

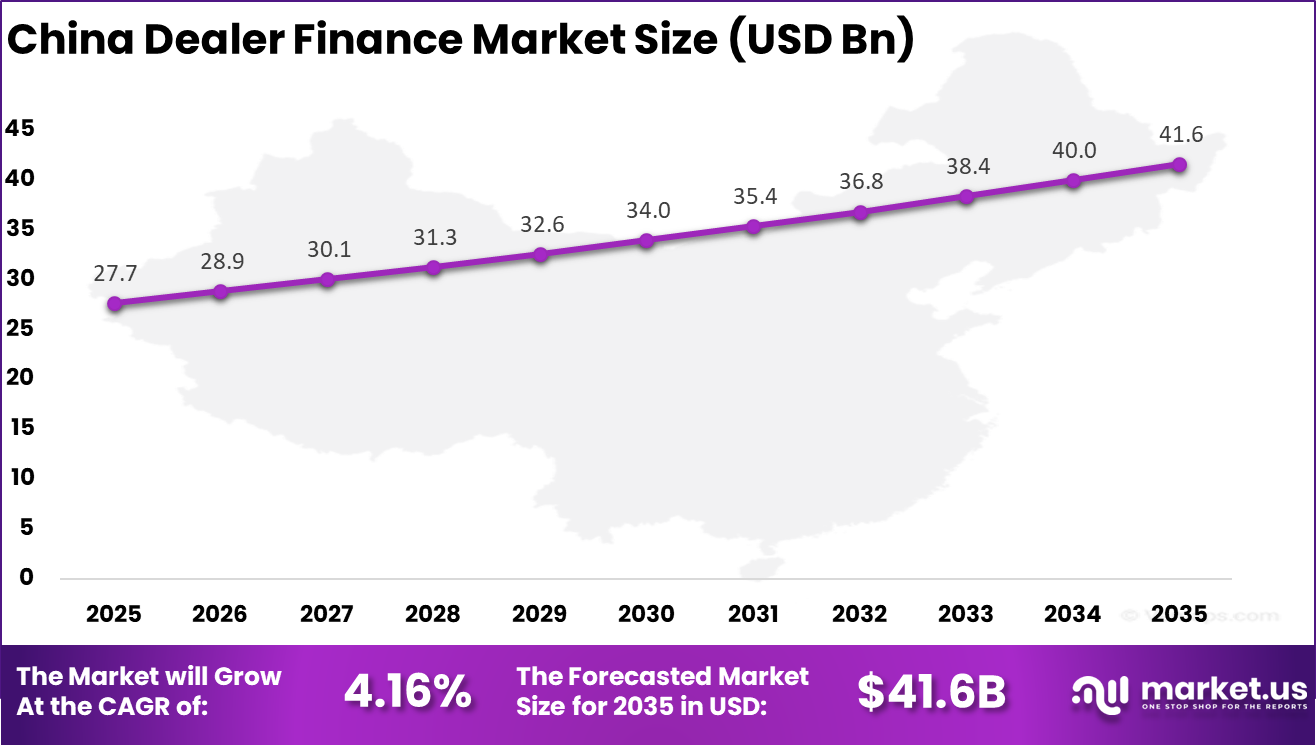

- TheChina Dealer Finance Market was valued at USD 27.7 billion in 2025, with a robust CAGR of 16%.

- In 2025, the Asia Pacific held a dominant market position in the Global Dealer Finance Market, capturing more than a 36.43% share.

Financing Trends (Q1 2025)

- In the first quarter of 2025, new vehicles accounted for 43.29% of total financing, while used vehicles represented 56.71%.

- The average interest rate for new vehicle loans declined to 6.73%, while used vehicle loan rates fell to 11.87%.

- The average monthly payment for new vehicles increased to USD 745, while the average loan amount for used vehicles recorded a slight rise.

- Nearly 10% of new vehicle transactions involved electric vehicles, and approximately 60% of these EV transactions were structured as leases.

- In early 2025, banks increased their auto finance market share to 26.55%, up from 24.79% in 2024, while manufacturer owned captives declined slightly to 29.81%.

- The average new vehicle loan amount reached USD 41,720 in the first quarter of 2025.

- Nearly 1 in 5 new car buyers selected 84 month loan terms to improve affordability.

- Serious auto loan delinquencies of 90+ days stood at 5.0% in the third quarter of 2025, close to historical highs seen in 2010.

- Net floor plan financing costs increased by 35% in early 2025, reaching USD 487 per unit, reflecting higher inventory carrying expenses for dealers.

- Finance and insurance income grew by 9%, partially offsetting weaker front end vehicle margins.

China Dealer Finance Market Size

The market for Dealer Finance within China is growing tremendously and is currently valued at USD 27.7 billion, the market has a projected CAGR of 4.16%. The growth is supported by rising vehicle ownership across urban and semi urban areas, along with strong demand for electric vehicles.

Expanding digital payment systems and widespread use of mobile banking make loan processing faster and more accessible. Supportive government policies promoting automotive consumption and structured lending practices are also strengthening dealership based financing across the country.

For instance, in January 2026, FAW Group’s finance arm launched zero-down-payment loans for passenger vehicles, boosting sales amid EV incentives and urbanization. This innovation expanded penetration to 71% projected by year-end, outpacing global averages via digital fintech integration and policy support.

In 2025, the Asia Pacific held a dominant market position in the Global Dealer Finance Market, capturing more than a 36.43% share, holding USD 88.2 billion in revenue. This dominance is driven by high vehicle sales volumes, expanding middle class populations, and strong demand for affordable financing options.

Rapid digital lending adoption, growth of automotive dealerships, and increasing consumer preference for installment based purchases are strengthening dealer finance usage across major economies like China, India, and Southeast Asian countries.

Type Analysis

In 2025, Retail financing leadership at 63.24% indicates that dealer finance remains most dependent on converting individual customer purchases. This segment performs strongly because financing is often required to match vehicle price points with monthly affordability expectations. Retail financing also benefits from dealership influence at the point of sale, where lender offers can be presented alongside vehicle choices. In many dealer models, this creates a direct link between credit availability and vehicle delivery volumes.

Retail financing demand is also strengthened by the operational advantages of dealership arranged processing. The indirect flow allows dealers to submit applications to multiple lenders and select the best approval for the customer and the deal structure. This process has been widely described as a standard pattern in auto lending and explains why retail finance remains highly integrated with dealer sales operations. Over time, the segment has required investment in faster approvals and better risk controls to remain efficient.

For Instance, in February 2026, Ally Financial Inc. reported stable retail auto trends with net charge-offs at 1.97% in 2025, guiding 1.8-2.0% for 2026. As an OEM-neutral lender, Ally hit record consumer applications and insurance premiums in dealer services. This boosts retail financing by offering full-spectrum loans that help dealers close more individual buyer deals reliably.

Service Provider Analysis

In 2025, Banks at 45.9% indicate that traditional lenders remain central to auto credit supply, particularly in prime and near prime lending. Banks typically bring stable funding and scale, which supports high volume indirect lending programs with large dealer groups. This position also reflects the long established role of banks in purchasing retail installment contracts originated through dealerships. In most markets, banks remain a key pricing reference for auto credit offers at the point of sale.

The bank position is increasingly shaped by portfolio performance and risk appetite. US bank auto loan delinquency ratios were reported to have reached a decade high in 2023, which has increased focus on tighter underwriting and more active monitoring. When performance pressure rises, banks tend to rebalance exposures by credit tier, geography, and vehicle segment, which then affects dealership approval rates. This makes bank participation a critical sensitivity factor for dealer finance growth.

For instance, in January 2025, JPMorgan Chase Bank expanded its Chase Auto division, financing luxury brands like McLaren and Aston Martin with $85 billion in loans. They focus on white-label services for dealers, holding steady amid tariffs. Banks like Chase provide reliable funding, drawing more dealer partnerships.

Vehicle Type Analysis

In 2025, Passenger vehicle dominance at 65.82% is consistent with the large base of consumer purchases that require financing to complete transactions. These loans tend to be high in volume and operationally standardised, which suits indirect dealership workflows. Passenger vehicles also attract promotional financing and brand linked programs in many markets, which further supports credit penetration. This structure sustains dealer finance demand even when sales cycles fluctuate.

Passenger vehicle financing has also been affected by changing affordability conditions and inventory dynamics. When vehicle prices and interest rates rise, consumers become more payment sensitive and depend more on financing structure to reach a workable monthly payment. This increases the importance of fast, competitive offers at the dealership. It also increases the need for accurate risk pricing so that lenders can remain active without absorbing unstable losses.

For Instance, in October 2025, Ford Motor Credit Company LLC enhanced passenger vehicle programs with promotional rates and loyalty perks. Their specialized financing reflects Ford’s vehicle values, making sedans and SUVs more accessible. Dealers use these to push family cars, driving segment growth.

Channel Analysis

In 2025, The Indirect channel leadership at 70.5% shows that dealership arranged financing remains the main origination route for retail auto credit. In this model, the dealer submits the customer’s application to one or more financing sources, and the approved contract is then assigned to the lender. This structure has been described as widely used because it supports conversion at the point of sale and reduces customer effort.

The indirect model also increases the importance of governance, because dealer incentives and pricing behaviour can affect customer outcomes. In China, banks were reported to have moved to rein in commissions paid to dealers for arranging auto loans amid regulatory scrutiny, and limits on practices such as forcing loans were referenced. These developments highlight why transparency, audit trails, and controlled compensation structures are becoming more important.

For Instance, in July 2025, Capital One Auto Finance’s Navigator platform handled 30% of U.S. subprime buys indirectly. Dealers tap it for end-to-end support, from inventory to approvals. This backend tech grows indirect channels by simplifying complex transactions.

End-User Analysis

In 2025, Customer dominance at 74.27% indicates that dealer finance is primarily driven by retail borrowers rather than fleet and commercial borrowers. Retail borrowers typically prioritise ease, speed, and predictable monthly payments, which suits dealership arranged financing. This segment also relies heavily on credit access at the point of sale because many buyers do not pre arrange financing before visiting a dealership. As a result, customer lending remains the largest consumption base for dealer finance products.

Retail customer outcomes are strongly influenced by underwriting and delinquency conditions in the broader credit cycle. When delinquency pressure rises, pricing tends to become more sensitive and approvals may tighten for higher risk tiers. US credit reporting has signalled elevated auto delinquency conditions in recent periods, reinforcing the need for careful affordability checks and fraud reduction. These realities keep customer lending at the centre of dealer finance risk management priorities.

For Instance, in November 2025, TD Auto Finance LLC upgraded customer portals for faster pre-approvals, targeting individual buyers. These tools cut credit impacts, easing purchases for everyday users. End-user focus with personalized rates sustains high engagement in dealer deals.

Investment and Business Benefits

Investment opportunities in dealer finance are expanding with the growth of electric vehicles, used vehicle financing, and small business fleet funding. Digital lending adoption continues to rise, creating demand for secure fintech platforms. Investors are also focusing on credit risk analytics and fraud detection tools, as financial fraud cases have increased in recent years. Platforms that serve first time buyers and underserved borrowers present additional long term potential.

Dealer finance improves dealership profitability by accelerating sales cycles and strengthening customer relationships. Financing availability can increase vehicle sales conversion rates by more than 20% in some markets. Dealers benefit from quicker inventory turnover and better cash flow management. Lenders gain access to a steady customer pipeline through dealership partnerships. Together, these advantages create a more stable and predictable revenue structure.

Emerging Trends

Digital first financing is becoming a major trend in dealer finance. Customers increasingly expect online loan applications, instant credit decisions, and paperless documentation. Dealerships are integrating finance platforms with mobile apps and websites to provide faster approvals and a smoother buying experience.

Another emerging trend is flexible financing models such as subscription plans and usage based payments. Growing interest in electric vehicles is also shaping customized loan products. Data driven credit assessment tools are improving risk evaluation and helping lenders serve a broader customer base efficiently.

Growth Factors

Rising vehicle ownership and increasing reliance on credit are key growth factors in dealer finance. Many buyers prefer manageable monthly payments instead of full upfront costs. Expanding middle income populations and easier access to banking services are supporting steady demand for dealership based financing solutions.

Technological improvements are also accelerating growth in dealer finance. Digital verification, automated credit scoring, and faster approval systems reduce processing time significantly. Strong partnerships between dealerships and financial institutions help widen customer reach, improve loan accessibility, and strengthen overall sales performance.

Key Market Segments

By Type

- Retail Financing

- Wholesale Financing

- Leasing

- Others

By Service Provider

- Banks

- NBFCs

- OEM Captive Finance

- Others

By Vehicle Type

- Passenger Vehicles

- Commercial Vehicles

- Two-Wheelers

- Others

By Channel

- Direct

- Indirect

By End-User

- Customers

- Dealers

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Drivers

Rising Vehicle Financing Demand

The growing desire for vehicle ownership is pushing more customers toward dealer financing. Many buyers cannot pay the full cost upfront, so they prefer installment based loans. This helps dealers close sales faster and makes vehicles more affordable to a wider audience. Personalized financing options also allow buyers to select plans that match their income and repayment capacity, improving customer satisfaction.

Completing vehicle purchase and financing at the same location adds convenience for customers. Faster approvals and simplified documentation encourage buyers to use dealer arranged finance rather than seeking external loans. This seamless experience strengthens customer confidence and supports consistent demand for dealership financing services.

For instance, in June 2025, Nissan Motor Acceptance filed to start Nissan Bank U.S. to ramp up dealer commercial financing, meeting demand from over 1,200 dealerships for better rates and support. The plan targets efficient loans for inventory and operations, helping dealers serve more customers amid strong vehicle needs without draining cash. It aims to support local businesses key to communities.

Restraint

Cost Barriers and Credit Requirements

High interest rates and strict credit checks can prevent some buyers from accessing dealer finance. Customers with limited credit history or lower income may find qualifying for loans challenging. Even approved buyers sometimes hesitate due to higher repayment obligations. These factors limit potential loan adoption and can reduce dealership sales in certain markets.

Dealers and lenders must balance offering flexible credit with managing risk. Conservative approval criteria protect against defaults but exclude some willing buyers. As a result, many customers delay purchases or seek alternative financing, which slows the growth of dealer finance in certain segments.

For instance, in August 2025, Capital One stuck to a 500+ credit score minimum for loans but highlighted geographic and dealer limits that block some buyers, like no service in Alaska or Hawaii. Their pre-approval tools help compare rates without score hits, yet strict income and debt checks remain hurdles for many. This setup balances access with risk control in a picky market.

Opportunities

Digital Tools Integrated in Dealer Platforms

Integrating digital solutions into dealer finance offers an opportunity to improve efficiency and customer experience. Online applications, automated credit checks, and e-documentation simplify the process. Customers can complete approvals faster, while dealers reduce errors and paperwork. These tools make financing more accessible and attractive.

Digital platforms also enable dealers to analyze customer needs and offer tailored loan products. Faster communication with lenders and smooth transaction processing increases conversion rates. Overall, digital integration strengthens dealership operations and supports a more competitive and customer friendly financing environment.

For instance, in May 2025, Toyota Financial Services kicked off an Instagram channel to share auto finance stories digitally, making info fun and easy for dealers and buyers. It flips traditional updates into engaging content, helping platforms connect better with users seeking quick tool access. This builds on their retail tools for smoother experiences.

Challenges

Keeping Up with Regulations

Dealer finance is highly regulated, requiring strict adherence to consumer protection, disclosure, and data privacy rules. Dealers must constantly update processes to remain compliant and avoid penalties. Regulatory changes can influence how loans are structured and presented to customers, adding complexity to operations.

Compliance demands also affect smaller dealerships more heavily due to resource constraints. Dealers need to work with legal and compliance teams to align products with current regulations. Meeting these requirements can slow down operational efficiency and innovation, presenting ongoing challenges in the dealer finance market.

For instance, in February 2025, Ford Motor Credit detailed its cybersecurity governance in a 10-K filing, with the CTO updating committees on risks and incidents per rules. They notify the Audit Committee ahead of reports on big issues, showing tight compliance in a shifting landscape. This keeps operations steady amid growing oversight demands.

Key Players Analysis

The Dealer Finance Market is led by captive finance arms such as Ford Motor Credit Company LLC, GM Financial Company, Inc., Toyota Motor Credit Corporation, American Honda Finance Corporation, and Nissan Motor Acceptance Corporation. These firms provide wholesale floorplan financing and retail auto loans through aligned dealer networks. Strong brand affiliation supports customer retention. Competitive rates and promotional financing programs improve dealer liquidity. Digital loan processing tools enhance speed and transparency.

Large banking institutions such as JPMorgan Chase Bank, National Association, Wells Fargo Bank, National Association, Capital One Auto Finance, and TD Auto Finance LLC compete through diversified funding bases and risk management capabilities. These lenders offer inventory financing, commercial lines of credit, and consumer auto loans. Strong balance sheets support competitive pricing. Advanced credit analytics improve underwriting accuracy.

Independent and hybrid finance providers, including Ally Financial Inc. and other regional lenders, focus on flexible funding structures and dealer centric services. These firms emphasize relationship management and tailored credit solutions. Technology driven platforms support real time inventory monitoring and performance tracking. Risk sharing arrangements and securitization strategies enhance capital efficiency.

Top Key Players in the Market

- Ally Financial Inc.

- American Honda Finance Corporation

- Capital One Auto Finance

- Ford Motor Credit Company LLC

- GM Financial Company, Inc.

- JPMorgan Chase Bank, National Association

- Nissan Motor Acceptance Corporation

- TD Auto Finance LLC

- Toyota Motor Credit Corporation

- Wells Fargo Bank, National Association

- Others

Recent Developments

- In February 2026, TD Auto Finance saw originations rise 5% in 2025, fueled by buy box expansions and upcoming tech upgrades for better loan structures. The lender is prioritizing dealer tools amid competition, signaling steady growth in prime auto financing.

- In September 2025, GM Financial and Ford Credit innovated to extend $7,500 federal EV tax credits via dealer inventory down payments, maintaining lease incentives through year-end despite IRS deadline changes. This dealer workaround highlights captive finance arms’ agility in navigating policy shifts for EV adoption.

Report Scope

Report Features Description Market Value (2025) USD 242.2 Bn Forecast Revenue (2035) USD 468.5 Bn CAGR (2026-2035) 6.8% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends Segments Covered By Type (Retail Financing, Wholesale Financing, Leasing, Others), By Service Provider (Banks, NBFCs, OEM Captive Finance, Others), By Vehicle Type (Passenger Vehicles, Commercial Vehicles, Two-Wheelers, Others), By Channel (Direct, Indirect), By End-User (Dealers, Customers) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Ally Financial Inc., American Honda Finance Corporation, Capital One Auto Finance, Ford Motor Credit Company LLC, GM Financial Company, Inc., JPMorgan Chase Bank, National Association, Nissan Motor Acceptance Corporation, TD Auto Finance LLC, Toyota Motor Credit Corporation, Wells Fargo Bank, National Association, Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

Our Clients

- 179634

- Feb. 2026