Global De-identified Health Data Market By Type (Clinical Data, Demographic Data, Administrative Data, Unstructured Data, Temporal Data and Others), By Application (Clinical and Medical Research, AI and Machine Learning Training, Electronic Health Records (EHR) Data Sharing, Healthcare Analytics and Marketing, Public Health and Disease Surveillance, and Others), By End User (Healthcare Providers, Pharmaceutical Companies, Biotechnology Firms, Medical Device Manufacturers, Insurance Companies/ Healthcare Payers, Research Institutions, Government Agencies and Others), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 181408

- Number of Pages: 203

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

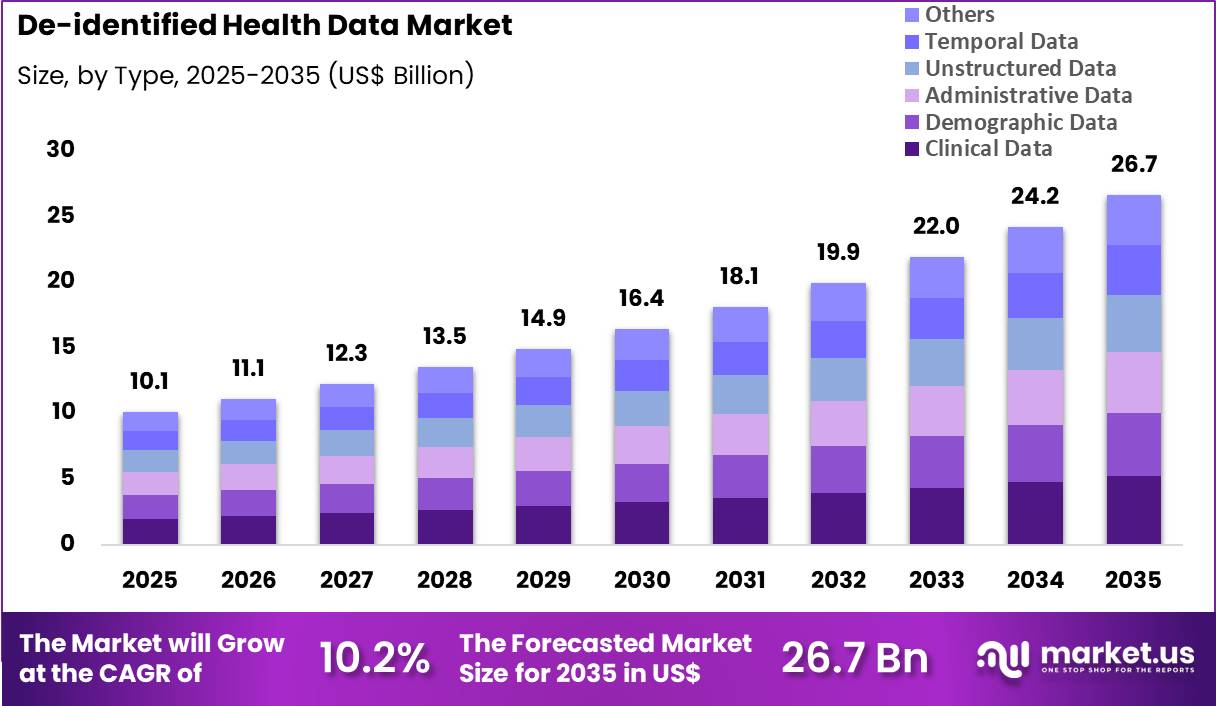

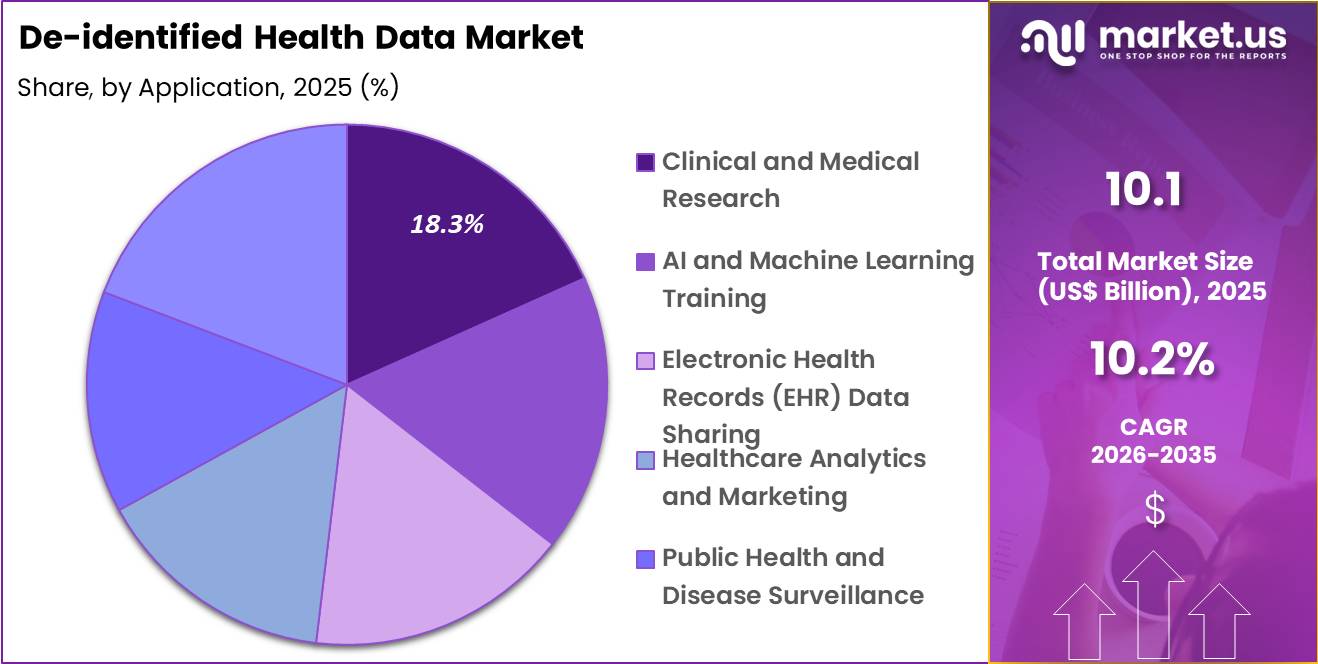

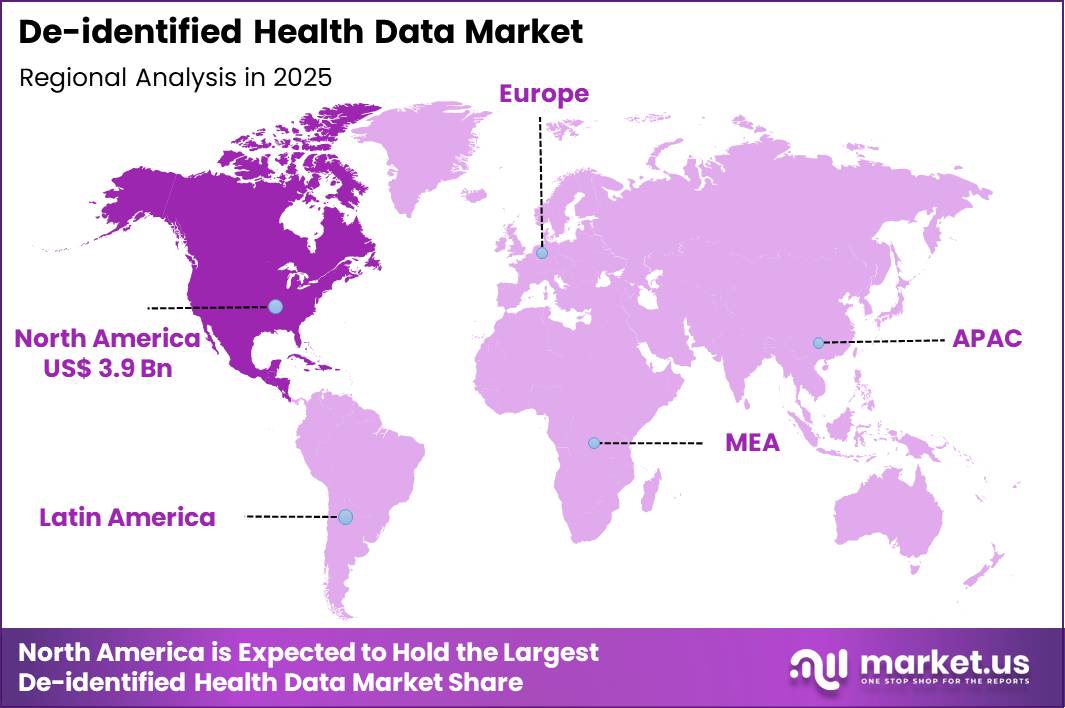

The Global De-identified Health Data Market size is expected to be worth around US$ 26.7 Billion by 2035 from US$ 10.1 Billion in 2025, growing at a CAGR of 10.2% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 38.5% share with a revenue of US$ 3.9 Billion.

Increasing demand for real-world evidence and precision medicine propels the De-identified Health Data market as pharmaceutical companies, researchers, and healthcare organizations require large-scale, privacy-protected datasets to drive clinical insights and therapeutic innovation.

Life sciences companies increasingly leverage de-identified electronic health records to analyze treatment patterns and outcomes in oncology, identifying real-world effectiveness of targeted therapies and informing label expansions or post-marketing studies. These datasets support pharmacoepidemiology research by enabling longitudinal tracking of drug safety and adverse events across diverse patient populations without compromising individual privacy.

Payers and health systems utilize de-identified claims data to evaluate cost-effectiveness of interventions, optimizing formulary decisions and value-based contracting for chronic conditions like diabetes and cardiovascular disease.

Academic researchers apply de-identified genomic and clinical data to discover novel biomarkers and disease subtypes, accelerating translational research in rare diseases and complex multifactorial disorders. Public health entities use aggregated, anonymized data to monitor disease trends, assess vaccination impact, and evaluate healthcare disparities in population-level studies.

Data providers and technology partners pursue opportunities to enhance data linkage and interoperability through advanced tokenization and privacy-preserving technologies, expanding applications in multi-source real-world evidence generation that connects disparate datasets across care settings.

These advancements support federated learning models that enable collaborative analysis without centralizing sensitive information, broadening utility in cross-industry consortia for drug development and health economics research. Opportunities emerge in synthetic data generation that replicates de-identified datasets for training AI models while eliminating re-identification risks.

Companies invest in secure data marketplaces and governance frameworks that facilitate compliant data sharing for precision oncology and rare disease research. In February 2026, Thermo Fisher Scientific expanded its real-world data capabilities through a strategic collaboration with Datavant. This partnership focuses on enhancing data interoperability and linkage, allowing researchers to connect fragmented clinical datasets while maintaining strict patient privacy.

By utilizing Datavant’s tokenization technology, the initiative aims to accelerate the development of precision medicines by providing a more comprehensive view of the patient journey across diverse care settings.

Recent trends emphasize privacy-enhancing technologies, federated analytics, and real-world evidence integration, positioning de-identified health data as a foundational asset for innovation in evidence-based medicine and personalized therapeutics.

Key Takeaways

- In 2025, the market generated a revenue of US$ 10.1 Billion, with a CAGR of 10.2%, and is expected to reach US$ 26.7 Billion by the year 2035.

- The type segment is divided into clinical data, demographic data, administrative data, unstructured data, temporal data and others, with clinical data taking the lead with a market share of 19.6%.

- Considering application, the market is divided into clinical and medical research, AI and machine learning training, electronic health records (EHR) data sharing, healthcare analytics and marketing, public health and disease surveillance, and others. Among these, clinical and medical research held a significant share of 18.3%.

- Furthermore, concerning the end user segment, the market is segregated into healthcare providers, pharmaceutical companies, biotechnology firms, medical device manufacturers, insurance companies/ healthcare payers, research institutions, government agencies and others. The healthcare providers sector stands out as the dominant player, holding the largest revenue share of 36.4% in the market.

- North America led the market by securing a market share of 38.5%.

Type Analysis

Clinical data accounted for 19.6% of growth within type and dominate the de-identified health data market due to its critical role in clinical research, healthcare analytics, and treatment outcome evaluation. Healthcare systems generate large volumes of clinical data through electronic health records, laboratory results, imaging reports, and treatment histories.

Hospitals and health networks increasingly anonymize these datasets to support medical research while complying with privacy regulations such as HIPAA. The Office of the National Coordinator for Health Information Technology reported that more than 96% of U.S. hospitals adopted electronic health record systems, which significantly expanded the volume of digital clinical data available for analysis.

Researchers and technology developers rely on anonymized clinical datasets to develop predictive models, evaluate treatment effectiveness, and improve patient care strategies. The segment is expected to grow as healthcare institutions expand digital infrastructure and participate in large-scale data sharing initiatives that support precision medicine and population health research.

Application Analysis

Clinical and medical research accounted for 18.3% of growth within application and dominate the de-identified health data market because researchers require extensive real-world datasets to evaluate disease patterns, treatment responses, and healthcare outcomes. De-identified data enables researchers to analyze patient populations without compromising personal privacy, which supports ethical research practices and regulatory compliance.

Pharmaceutical companies and academic institutions increasingly collaborate with healthcare providers to access anonymized datasets that support drug discovery and clinical studies. The National Institutes of Health continues to promote data-sharing initiatives that encourage the use of anonymized health records for biomedical research.

Researchers analyze these datasets to understand disease progression, identify treatment trends, and evaluate healthcare interventions across large populations. The segment is anticipated to expand as precision medicine programs and data-driven healthcare research initiatives increase globally.

End-User Analysis

Healthcare providers accounted for 36.4% of growth within end users and dominate the de-identified health data market because hospitals and healthcare systems generate the majority of patient health records used in anonymized data programs. Healthcare providers collect extensive clinical, demographic, and treatment information through electronic health record platforms and diagnostic systems.

These organizations increasingly share anonymized datasets with research institutions, technology developers, and pharmaceutical companies to advance healthcare innovation. Hospitals also participate in national health data networks that promote secure data exchange and collaborative research.

According to healthcare IT adoption reports, the rapid expansion of digital health records significantly increased the availability of structured clinical data across healthcare systems. Healthcare providers are projected to remain the primary contributors of de-identified health data as digital health infrastructure continues to expand and healthcare organizations increasingly rely on data-driven decision making to improve patient outcomes.

Key Market Segments

By Type

- Clinical Data

- Demographic Data

- Administrative Data

- Unstructured Data

- Temporal Data

- Others

By Application

- Clinical and Medical Research

- AI and Machine Learning Training

- Electronic Health Records (EHR) Data Sharing

- Healthcare Analytics and Marketing

- Public Health and Disease Surveillance

- Others

By End User

- Healthcare Providers

- Pharmaceutical Companies

- Biotechnology Firms

- Medical Device Manufacturers

- Insurance Companies/ Healthcare Payers

- Research Institutions

- Government Agencies

- Other

Drivers

Increasing regulatory support for secondary use of de-identified health data is driving the market.

Federal agencies have advanced policies encouraging the responsible sharing and analysis of de-identified health information to support public health research and innovation. The U.S. Department of Health and Human Services maintains guidance under the HIPAA Privacy Rule that permits de-identification through safe harbor or expert determination methods. These frameworks enable healthcare organizations to release datasets for purposes beyond direct treatment without requiring individual authorization.

The driver aligns with national initiatives to accelerate medical discovery through large-scale data aggregation. Entities increasingly contribute de-identified records to research networks and registries. The trend corresponds with expanded acceptance of real-world evidence in regulatory decision-making.

Data custodians implement robust de-identification protocols to maintain compliance while maximizing utility. The momentum facilitates growth in platforms that aggregate and curate anonymized clinical information. Enhanced trust in de-identification methodologies sustains broader participation from providers. This factor reinforces steady market progression through policy-enabled data mobility.

Restraints

Persistent re-identification risks in large datasets are restraining the market.

Despite established de-identification standards, studies have demonstrated successful linkage attacks that compromise anonymity in certain high-dimensional health datasets. The presence of auxiliary information from public sources increases vulnerability when datasets contain rare combinations of attributes.

The restraint limits willingness of some organizations to release granular records even after application of safe harbor criteria. Data stewards must allocate substantial resources to risk assessment and mitigation measures. The factor contributes to cautious approaches in sharing datasets with external researchers or commercial entities.

The dynamic moderates the volume and diversity of available de-identified data in the marketplace. Providers encounter challenges balancing data utility with privacy protection obligations. The concern influences contractual terms and restricts certain high-value use cases. This limitation persists in constraining unrestricted market expansion. The issue requires ongoing methodological improvements to restore confidence in de-identification practices.

Opportunities

Expansion of federated learning platforms for privacy-preserving analysis is creating growth opportunities.

Federated learning architectures enable collaborative model training across distributed health datasets without centralized data pooling or transfer. These systems maintain raw patient-level information within institutional firewalls while sharing only model updates. Opportunities arise for multi-institutional research initiatives that preserve regulatory compliance and institutional control.

The framework supports development of robust AI models across diverse populations and care settings. Developers gain capacity to access larger effective sample sizes without direct data exchange. The approach facilitates participation from organizations previously restricted by privacy concerns.

Such platforms promote equitable access to advanced analytics capabilities. The opportunity fosters innovation in privacy-enhancing technologies tailored to healthcare. Stakeholders anticipate improved model generalizability through broader representation. This advancement positions the sector for scalable, privacy-conscious data utilization.

Impact of Macroeconomic / Geopolitical Factors

Implementation of enhanced de-identification standards under updated HIPAA guidance is driving the market.

The U.S. Department of Health and Human Services issued revised guidance in 2024 clarifying expectations for expert determination of de-identification under the HIPAA Privacy Rule. This update emphasizes risk-based assessments incorporating current re-identification techniques and available public data sources. The guidance addresses evolving threats from advanced linkage methods and machine learning capabilities.

Covered entities benefit from more transparent criteria for achieving de-identification status. The 2024-2025 development aligns with increased scrutiny of secondary data uses in commercial and research contexts. Organizations report improved consistency in applying de-identification processes across enterprise datasets.

The framework supports standardized documentation of risk mitigation steps. The policy evolution stimulates investment in advanced anonymization tools and validation services. Early adopters demonstrate enhanced defensibility during regulatory reviews. Overall, this regulatory clarification strengthens the foundation for secure and compliant data sharing activities.

Latest Trends

Macroeconomic conditions shape the de-identified health data market through trends in healthcare analytics investment, pharmaceutical research spending, and expansion of digital health infrastructure. Rising inflation increases the cost of cloud computing, data processing, cybersecurity systems, and regulatory compliance, which raises operating expenses for companies that manage large healthcare datasets.

In addition, higher interest rates reduce venture capital activity, slowing funding for emerging health data platforms and delaying expansion of advanced analytics capabilities. Geopolitical uncertainty also affects the market by complicating cross-border data sharing, tightening privacy regulations, and creating barriers for international research collaborations that rely on large patient datasets.

Tariffs in the US on imported servers, storage equipment, and networking components further increase the infrastructure costs required to operate large-scale data repositories. Despite these pressures, many organizations are strengthening domestic data center capacity and investing in secure governance frameworks to protect sensitive information.

At the same time, increasing demand for real-world evidence, artificial intelligence training datasets, and population health insights continues to support stable long-term growth in the market.

Regional Analysis

North America is leading the De-identified Health Data Market

North America accounted for 39.6% of the de-identified health data market in 2025 as healthcare organizations increasingly leveraged anonymized patient datasets for clinical research, artificial intelligence development, and population health analysis.

Hospitals, pharmaceutical companies, and research institutions across the United States and Canada are generating vast volumes of electronic health records and medical imaging data that can be anonymized and used for scientific innovation without exposing patient identities.

According to the Office of the National Coordinator for Health Information Technology, about 96% of non-federal acute care hospitals in the United States had adopted certified electronic health record systems by 2023, creating a large digital data environment suitable for de-identification and secondary research use.

Growing adoption of digital health systems has therefore accelerated the availability of structured clinical datasets that support drug discovery, predictive analytics, and public health research. Pharmaceutical companies and biotechnology firms are collaborating with healthcare institutions to access anonymized clinical information that improves understanding of disease patterns and treatment outcomes.

Government initiatives supporting health data interoperability have further strengthened the ecosystem for secure data exchange and research collaboration. Technology companies are developing advanced privacy-preserving algorithms that remove personal identifiers while maintaining data utility for research.

Academic medical centers are also expanding data science programs focused on healthcare analytics and precision medicine. These developments collectively supported steady expansion of anonymized healthcare data utilization across North America in 2025.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to witness strong growth during the forecast period as governments and healthcare organizations accelerate digital health transformation and expand data-driven medical research initiatives. Countries such as China, Japan, South Korea, and Singapore are investing heavily in national health information systems that collect large volumes of electronic clinical data.

The World Health Organization reported that the Western Pacific region accounts for nearly one quarter of the global population, highlighting the vast healthcare datasets generated through regional health systems. Governments across the region are therefore promoting data governance frameworks that allow anonymized patient information to be used safely for research and healthcare innovation.

Hospitals and research institutions are collaborating with technology companies to analyze anonymized datasets for disease surveillance, drug discovery, and predictive healthcare analytics. Pharmaceutical companies operating in the region are also seeking access to privacy-protected clinical datasets that support regional clinical trials and treatment development.

Academic institutions are expanding biomedical informatics programs that train specialists in secure health data analytics. National digital health initiatives are encouraging interoperability between hospitals, laboratories, and research centers. These developments are expected to accelerate the use of anonymized healthcare data for medical research and innovation across Asia Pacific in the coming years.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

Key participants in the De-identified Health Data Market expand growth by developing advanced data anonymization platforms, strengthening collaborations with healthcare providers, and creating secure data exchange ecosystems that enable research without compromising patient privacy.

Companies invest in artificial intelligence tools that process large clinical datasets and remove personally identifiable information while maintaining analytical value. They also establish partnerships with pharmaceutical firms, academic institutions, and healthcare systems to support drug discovery, epidemiological research, and population health analytics.

IQVIA represents a notable participant in the De-identified Health Data Market and operates as a global healthcare analytics company headquartered in the United States that provides data science, real-world evidence, and clinical research solutions to the life sciences industry.

The company leverages extensive healthcare datasets and advanced analytics to support medical research and healthcare decision making. Industry competitors continue to strengthen privacy technologies, expand health data networks, and develop regulatory-compliant data platforms to increase the availability of secure research-ready health information.

Top Key Players

- IQVIA

- Oracle (Cerner Corporation)

- Optum, Inc. (UnitedHealth Group)

- ICON plc

- Veradigm LLC

- IBM

- Premier, Inc.

- Shaip

- Komodo Health, Inc.

- Evidation Health, Inc.

- Medidata

- Clarify Health Solutions

Recent Developments

- In February 2026, Datavant was named the top-ranked provider in the Best in KLAS awards for its risk adjustment and outsourced coding solutions. The company’s Clinical Insights Platform utilizes purpose-built AI trained on millions of medical records to identify gaps in patient documentation. As per clinical evaluations, this platform has achieved a 98% coding accuracy rate, helping large health systems manage the rising complexity of diagnostic data without compromising compliance or data security.

- In April 2025, Truveta announced a major expansion of its de-identified health data platform, which now incorporates clinical records from over 30 large US health systems. This dataset covers more than 100 million patients and includes granular, longitudinal data such as lab results, physician notes, and imaging. The expansion is designed to support pharmaceutical companies in conducting large-scale real-world evidence (RWE) studies, particularly for rare diseases and oncology, where high-fidelity, de-identified data is critical for regulatory submissions.

Report Scope

Report Features Description Market Value (2025) US$ 10.1 Billion Forecast Revenue (2035) US$ 26.7 Billion CAGR (2026-2035) 10.2% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Type (Clinical Data, Demographic Data, Administrative Data, Unstructured Data, Temporal Data and Others), By Application (Clinical and Medical Research, AI and Machine Learning Training, Electronic Health Records (EHR) Data Sharing, Healthcare Analytics and Marketing, Public Health and Disease Surveillance, and Others), By End User (Healthcare Providers, Pharmaceutical Companies, Biotechnology Firms, Medical Device Manufacturers, Insurance Companies/ Healthcare Payers, Research Institutions, Government Agencies and Others) Regional Analysis North America – The US, Canada; Europe – Germany, France, The U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America Competitive Landscape IQVIA, Oracle (Cerner Corporation), Optum, Inc. (UnitedHealth Group), ICON plc, Veradigm LLC, IBM, Premier, Inc., Shaip, Komodo Health, Inc., Evidation Health, Inc., Medidata, Clarify Health Solutions. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  De-identified Health Data MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

De-identified Health Data MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- IQVIA

- Oracle (Cerner Corporation)

- Optum, Inc. (UnitedHealth Group)

- ICON plc

- Veradigm LLC

- IBM

- Premier, Inc.

- Shaip

- Komodo Health, Inc.

- Evidation Health, Inc.

- Medidata

- Clarify Health Solutions

Our Clients

- 181408

- March 2026