Global Crop Micronutrients Market Size, Share, And Industry Analysis Report By Form (Chelated, Non-Chelated), By Type (Zinc, Boron, Iron, Manganese, Molybdenum, Copper), By Crop Type (Cereals and Grains, Fruits and Vegetables, Pulses and Oilseeds), By Application (Soil, Foliar, Fertigation), By End-Use (Conventional Farming, Organic Farming, Hydroponics), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 182216

- Number of Pages: 228

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

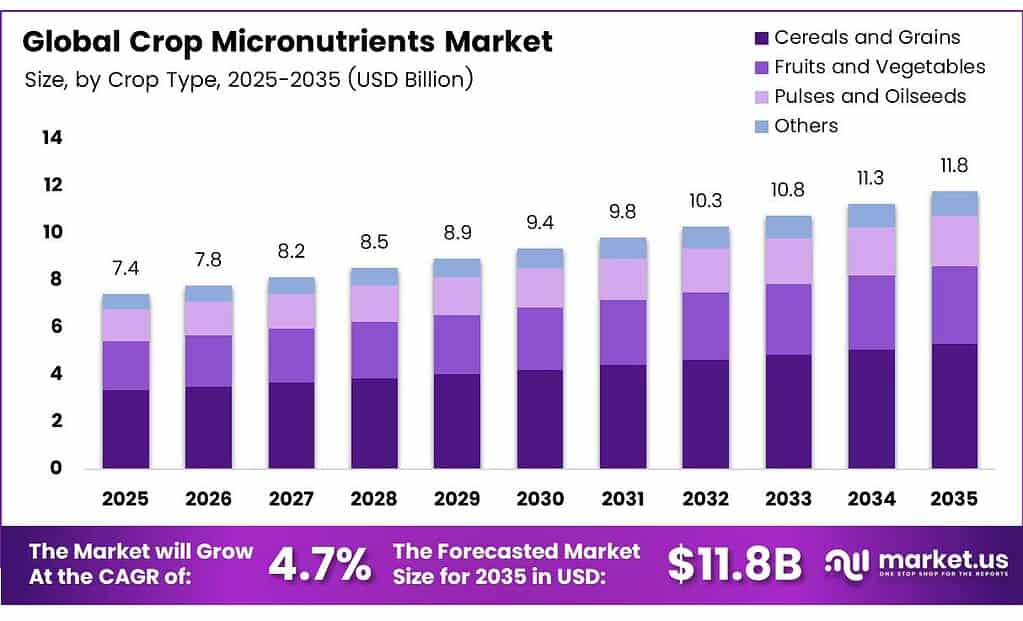

The Global Crop Micronutrients Market size is expected to be worth around USD 11.8 billion by 2035 from USD 7.4 billion in 2025, growing at a CAGR of 4.7% during the forecast period 2026 to 2035.

Crop micronutrients are essential mineral elements that plants require in small quantities for healthy growth. These include zinc, iron, boron, manganese, copper, and molybdenum. Farmers apply them through soil, foliar sprays, or fertigation systems to correct nutrient deficiencies and improve crop yields.

The market covers both chelated and non-chelated formulations used across cereals, fruits, vegetables, pulses, and oilseeds. Conventional farming drives the highest demand, though organic and hydroponic applications are growing steadily. Soil application remains the most widely adopted method across major agricultural regions worldwide.

India’s total fertiliser nutrient consumption increased to nearly 17 million tonnes annually, reflecting massive nutrient input demand, including micronutrient blends across irrigated farmland. This scale highlights how emerging economies drive the global crop micronutrients market through large-scale agricultural intensification programs.

India’s fertiliser distribution network includes approximately 283,000 sales points, indicating a deep domestic infrastructure that supports micronutrient fertiliser penetration across rural agricultural regions. Such extensive reach enables manufacturers and distributors to scale product delivery efficiently in high-volume markets.

Intensive cropping systems continue to deplete soil micronutrients faster than natural processes can replenish them. Farmers increasingly rely on targeted micronutrient fertilisers to restore soil health and maintain yield quality. This shift supports strong, consistent demand across both developing and developed agricultural markets globally.

Key Takeaways

- The Global Crop Micronutrients Market is valued at USD 7.4 billion in 2025 and is projected to reach USD 11.8 billion by 2035 at a CAGR of 4.7% during the forecast period 2026 to 2035.

- Chelated holds a dominant share of 65.9% in the crop micronutrients market.

- Zinc leads with a 29.6% market share among all micronutrient types.

- Cereals and Grains account for 54.2% of the total market demand.

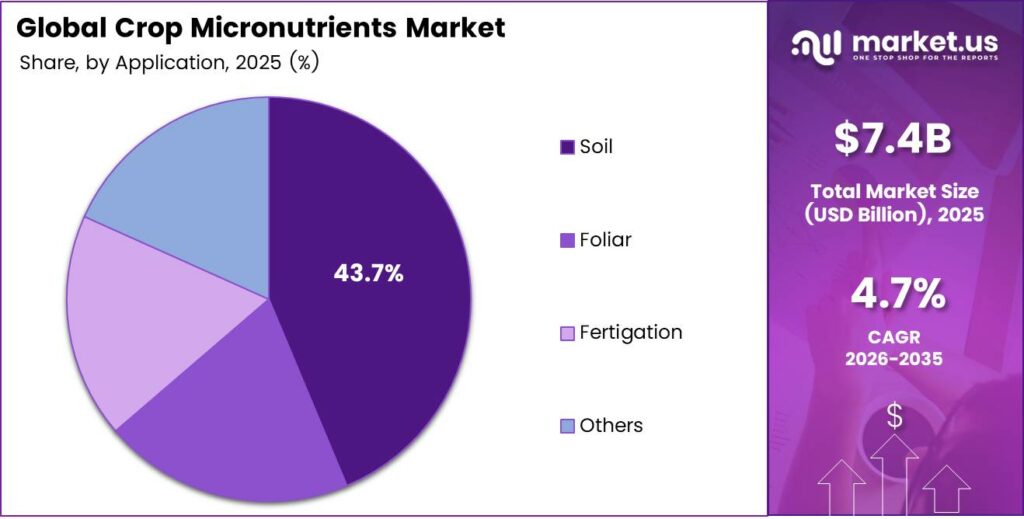

- Soil application dominates with a 43.7% share of the overall market.

- Conventional Farming leads with a 74.4% share of the end-use segment.

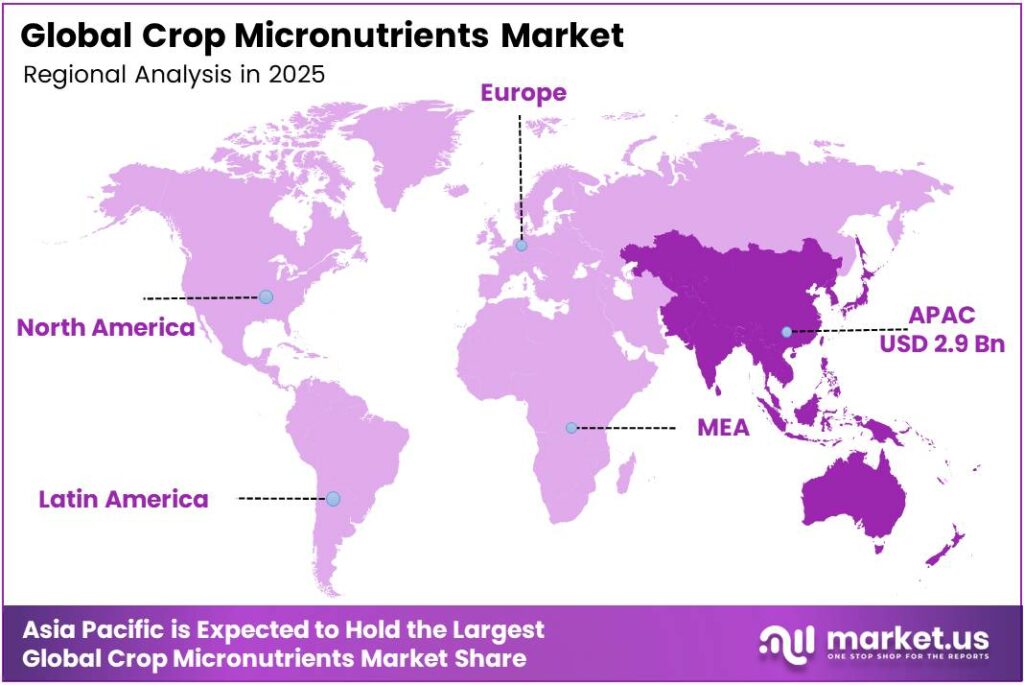

- Asia Pacific leads all regions with a 39.5% market share, valued at USD 2.9 billion.

By Form Analysis

Chelated dominates with 65.9% due to superior nutrient bioavailability and plant uptake efficiency.

In 2025, Chelated micronutrients held a dominant market position in the By Form segment of the Crop Micronutrients Market, with a 65.9% share. Chelated formulations bond micronutrients with organic molecules, preventing soil fixation and improving absorption. Moreover, their effectiveness in diverse soil conditions makes them the preferred choice for high-value crop applications globally.

Non-Chelated micronutrients represent a cost-effective alternative widely used in conventional farming systems. These formulations suit high-pH soils where basic inorganic salts remain adequately soluble. However, their lower bioavailability compared to chelated products limits their adoption in precision farming operations. Consequently, non-chelated products serve price-sensitive markets in developing agricultural economies.

By Type Analysis

Zinc dominates with 29.6% due to widespread soil zinc deficiency across major crop-growing regions.

In 2025, Zinc held a dominant market position in the By Type segment of the Crop Micronutrients Market, with a 29.6% share. Zinc deficiency affects nearly half of the world’s agricultural soils, driving strong demand. Additionally, zinc plays a critical role in enzyme activity, protein synthesis, and overall plant immunity, making it the most widely applied micronutrient globally.

Boron supports cell wall development and reproductive growth in crops such as sunflower, canola, and legumes. Its deficiency reduces fruit set and grain filling significantly. Therefore, boron applications are essential in fruit and vegetable cultivation, where yield quality directly impacts market value and farmer income.

By Crop Type Analysis

Cereals and Grains dominate with 54.2% due to their large cultivation area and high micronutrient demand globally.

In 2025, Cereals and Grains held a dominant market position in the By Crop Type segment of the Crop Micronutrients Market, with a 54.2% share. Staple crops like wheat, rice, and maize cover billions of hectares globally. Moreover, their large-scale cultivation under intensive systems depletes soil micronutrients rapidly, creating consistent and high-volume demand for correction inputs.

Fruits and Vegetables represent a high-value crop segment with above-average micronutrient requirements per hectare. Growers apply multiple micronutrient products to maintain produce quality, colour, and shelf life. Consequently, this segment commands premium product formulations, including chelated sprays and drip fertigation solutions that deliver nutrients precisely to root zones.

By Application Analysis

Soil application dominates with 43.7% due to its widespread compatibility with conventional farming practices.

In 2025, Soil application held a dominant market position in the By Application segment of the Crop Micronutrients Market, with a 43.7% share. Soil-applied micronutrients are incorporated during land preparation or early crop stages. Moreover, this method supports long-term nutrient availability in the root zone, making it the most established and farmer-preferred delivery approach globally.

Foliar application delivers micronutrients directly onto leaf surfaces for rapid absorption during crop stress periods. It allows targeted correction of acute deficiencies without disturbing soil chemistry. However, foliar applications require precise timing and dilution to avoid phytotoxicity, limiting their independent use to technically skilled growers or advisory-supported farming operations.

Fertigation integrates micronutrient delivery through irrigation systems, enabling precise and uniform nutrient distribution. This method is highly efficient in drip-irrigated orchards, greenhouses, and high-value cropping systems. Consequently, fertigation is gaining strong momentum in water-scarce regions where maximising input efficiency drives both agronomic and economic returns.

By End-Use Analysis

Conventional Farming dominates with 74.4% due to its large-scale adoption and high input intensity globally.

In 2025, Conventional Farming held a dominant market position in the By End-Use segment of the Crop Micronutrients Market, with a 74.4% share. Large commercial farms rely on intensive nutrient management to sustain high yields across monoculture systems. Moreover, fertiliser recommendation programs by extension services drive regular micronutrient applications in conventional production environments globally.

Organic Farming uses naturally derived micronutrient sources such as rock minerals, composts, and bio-chelates. This segment is growing as consumer demand for organic produce accelerates globally. However, strict input regulations under organic certification standards limit the range of permitted micronutrient products, creating a niche but rapidly expanding sub-market for compliant formulations.

Key Market Segments

By Form

- Chelated

- Non-Chelated

By Type

- Zinc

- Boron

- Iron

- Manganese

- Molybdenum

- Copper

- Others

By Crop Type

- Cereals and Grains

- Fruits and Vegetables

- Pulses and Oilseeds

- Others

By Application

- Soil

- Foliar

- Fertigation

- Others

By End-Use

- Conventional Farming

- Organic Farming

- Hydroponics

Emerging Trends

Chelated and Nano-Based Micronutrient Products Gain Rapid Adoption

Manufacturers are developing nano-based and advanced chelated micronutrient formulations that improve plant uptake while reducing application rates. These next-generation products enhance nutrient efficiency under variable soil conditions. Fertiliser and micronutrient-related indicators now cover over 245 countries, reflecting global momentum toward smarter, data-driven nutrient management strategies in modern agriculture.

Climate-Smart Agriculture Integrates Organic and Inorganic Micronutrient Sources

Agronomists increasingly combine organic and inorganic micronutrient sources in climate-smart farming protocols to address climate-induced declines in crop nutrient bioavailability. Global policy frameworks aligned with Sustainable Development Goals now actively support precision nutrient management tools. Consequently, research institutions and agri-input companies are collaborating to design solutions that maintain crop nutrition under increasingly unpredictable weather patterns.

Drivers

Soil Micronutrient Depletion Accelerates Demand for Corrective Inputs

Intensive cropping systems continuously deplete soil micronutrient reserves faster than natural replenishment cycles allow. Exclusive reliance on macronutrient fertilisers worsens this depletion over time. Zimbabwe’s large-scale farms applied fertiliser nutrients at 290 kg per hectare compared to only 15 kg per hectare in communal lands, illustrating how uneven input intensity drives targeted micronutrient deficiency and correction demand.

High-Yielding Cultivars and Precision Farming Boost Micronutrient Requirement

Modern high-yielding crop varieties demand supplemental micronutrients to achieve their full genetic yield potential under intensive cultivation conditions. Precision farming practices enable farmers to deliver micronutrients at exactly the right time and location. Additionally, international initiatives promoting balanced fertilisation elevate crop nutritional quality while simultaneously addressing food security goals across major agricultural regions globally.

Restraints

High Product Costs and Testing Requirements Create Adoption Barriers

Micronutrient fertilisers carry significantly higher per-unit costs than standard macronutrient inputs, limiting their accessibility for smallholder farmers. Mandatory soil or tissue testing adds further time and expense to the application process. Sudan’s fertiliser consumption averaged approximately 4kg of total nutrients per hectare, indicating how extremely low input intensity in cost-constrained regions directly reflects affordability and access challenges for micronutrient adoption.

Regulatory Approval Challenges Slow New Formulation Market Entry

Innovative micronutrient formulations face persistent regulatory hurdles related to environmental risk assessment and approval processes. Companies must invest heavily in toxicology studies and compliance documentation before launching new products. Consequently, these extended development timelines increase costs and reduce speed-to-market, discouraging smaller manufacturers from entering the premium micronutrient formulation space in highly regulated markets.

Growth Factors

Foliar Integration and Soil Mapping Unlock Efficiency Gains

Integrated foliar micronutrient programs combined with optimised macronutrient regimes deliver measurably higher nutrient-use efficiency on commercial farms. Comprehensive soil micronutrient mapping helps identify high-risk zones needing targeted intervention. South Africa’s fertiliser consumption reached approximately 1,400 thousand tonnes of nutrients in peak periods, demonstrating how large nutrient markets create infrastructure for scaling advanced micronutrient delivery programs.

Biofortification and Public-Private Partnerships Expand Market Reach

Agronomic biofortification techniques are gaining strong traction globally, elevating micronutrient levels in staple crops to address dietary deficiencies. Collaborative public-private programs are developing next-generation sustainable fertiliser technologies that reduce environmental impact. Global fertiliser use datasets now cover major countries based on surveys conducted every 2 to 4 years since 1990, supporting evidence-based micronutrient intervention programs worldwide.

Regional Analysis

Asia Pacific Dominates the Crop Micronutrients Market with a Market Share of 39.5%, Valued at USD 2.9 Billion

Asia Pacific leads the global crop micronutrients market with a 39.5% share, valued at USD 2.9 billion in 2025. The region benefits from massive agricultural output in countries like China, India, and Southeast Asia. Moreover, government-backed soil health programs and subsidised fertiliser distribution networks actively support micronutrient adoption across millions of smallholder farms.

North America maintains a mature and technology-driven crop micronutrients market supported by advanced soil testing infrastructure. Precision agriculture adoption is high across the US and Canada, enabling targeted micronutrient applications. Additionally, robust agronomic advisory networks and strong distribution channels ensure consistent product availability across diverse farming systems in the region.

Europe’s crop micronutrients market benefits from stringent environmental regulations that encourage efficient and sustainable fertiliser use. Farmers in Germany, France, and the UK actively adopt balanced nutrient programs under EU agricultural policy frameworks. Consequently, demand for chelated and slow-release micronutrient formulations is particularly strong across high-value horticultural and speciality crop sectors.

Latin America is emerging as a high-growth region for crop micronutrients, driven by expanding soybean, sugarcane, and coffee cultivation in Brazil and Mexico. Large-scale commercial farming operations increasingly adopt micronutrient programs to sustain soil productivity. Furthermore, regional agribusinesses are partnering with international input companies to introduce advanced formulations that support export-oriented high-yield crop production.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

BASF SE is a global leader in crop nutrition, offering an extensive portfolio of chelated micronutrient products tailored for diverse soil types and crop systems. The company combines deep agronomic research with a broad distribution reach across major agricultural markets. Moreover, BASF’s investment in sustainable formulation science positions it strongly in the premium micronutrient segment worldwide.

DowDuPont Inc. leverages integrated crop science capabilities to deliver micronutrient solutions that align with broader plant protection and yield improvement strategies. Its research-backed product development approach enables the creation of high-performance formulations for intensive farming systems. Additionally, the company’s global footprint ensures effective supply chain management and agronomic support across key regional markets.

Nutrien Ltd operates one of the world’s largest agricultural retail and distribution networks, making micronutrient products accessible to millions of farmers globally. The company’s vertically integrated model spans production, blending, and direct farm advisory services. Consequently, Nutrien effectively translates soil science research into practical, field-ready micronutrient programs that support both conventional and speciality crop producers.

Corteva Agriscience applies advanced seed and crop protection science to develop complementary micronutrient technologies that enhance overall crop performance. The company focuses on data-driven agronomic solutions that integrate micronutrient management with seed genetics and pest control programs. Therefore, Corteva’s holistic approach to crop productivity places it among the most influential players in the global micronutrients market.

Top Key Players in the Market

- BASF SE

- DowDuPont Inc.

- Nutrien Ltd

- Corteva Agriscience

- Yara International ASA

- The Mosaic Company

- Nouryon

- Nufarm Ltd

- Compass Minerals International

- Western Nutrients Corporation

Recent Developments

- In April 2025, BASF launched Ampliqan, a new nitrification inhibitor (active ingredient DMPSA-K2) for urea- and ammonium-based fertilisers. It improves nitrogen use efficiency by reducing losses from leaching and nitrous oxide emissions, supporting climate-smart agriculture. The ammonium-based nutrition provides a secondary benefit by making more micronutrients available in the soil, which is particularly important for crop quality.

- In April 2024, Nutrien opened a new state-of-the-art retail facility in Balgonie, Saskatchewan (replacing an older Regina site). The 29,000-square-foot dry fertiliser warehouse and automated plant can blend and load over 40 tonnes of product quickly while incorporating both liquid and dry micronutrients plus stabiliser additives directly into fertiliser blends.

Report Scope

Report Features Description Market Value (2025) USD 7.4 Billion Forecast Revenue (2035) USD 11.8 Billion CAGR (2026-2035) 4.7% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Form (Chelated, Non-Chelated), By Type (Zinc, Boron, Iron, Manganese, Molybdenum, Copper, Others), By Crop Type (Cereals and Grains, Fruits and Vegetables, Pulses and Oilseeds, Others), By Application (Soil, Foliar, Fertigation, Others), By End-Use (Conventional Farming, Organic Farming, Hydroponics) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape BASF SE, DowDuPont Inc., Nutrien Ltd, Corteva Agriscience, Yara International ASA, The Mosaic Company, Nouryon, Nufarm Ltd, Compass Minerals International, Western Nutrients Corporation Customization Scope Customisation for segments, region/country-level will be provided. Moreover, additional customisation can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Crop Micronutrients MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Crop Micronutrients MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- BASF SE

- DowDuPont Inc.

- Nutrien Ltd

- Corteva Agriscience

- Yara International ASA

- The Mosaic Company

- Nouryon

- Nufarm Ltd

- Compass Minerals International

- Western Nutrients Corporation

Our Clients

- 182216

- March 2026