Quick Navigation

- Report Overview

- Top Market Takeaways

- Key Insights Summary

- Drivers Impact Analysis

- Restraint Impact Analysis

- Investor Type Impact Matrix

- Deployment Analysis

- Banking Type Analysis

- End-User Analysis

- Investment and Business Benefits

- Emerging Trends Analysis

- Growth Factors Analysis

- Key Market Segments

- Regional Analysis

- Driver Analysis

- Restraint Analysis

- Opportunity Analysis

- Challenge Analysis

- Competitive Analysis

- Future Outlook

- Recent Developments

- Report Scope

Report Overview

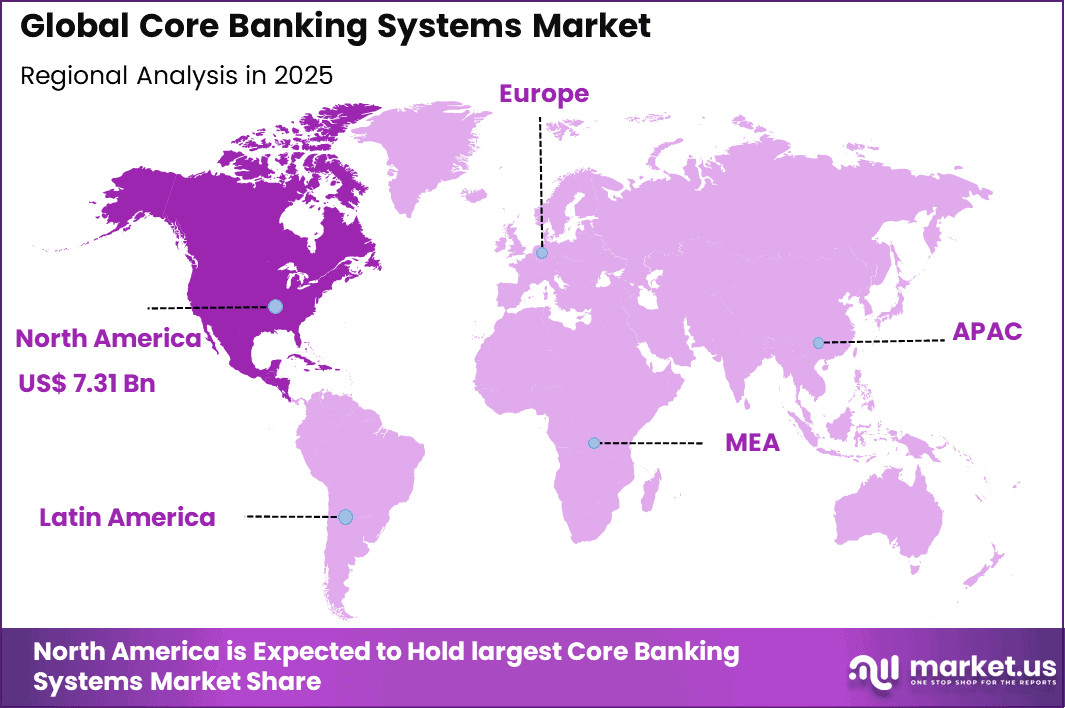

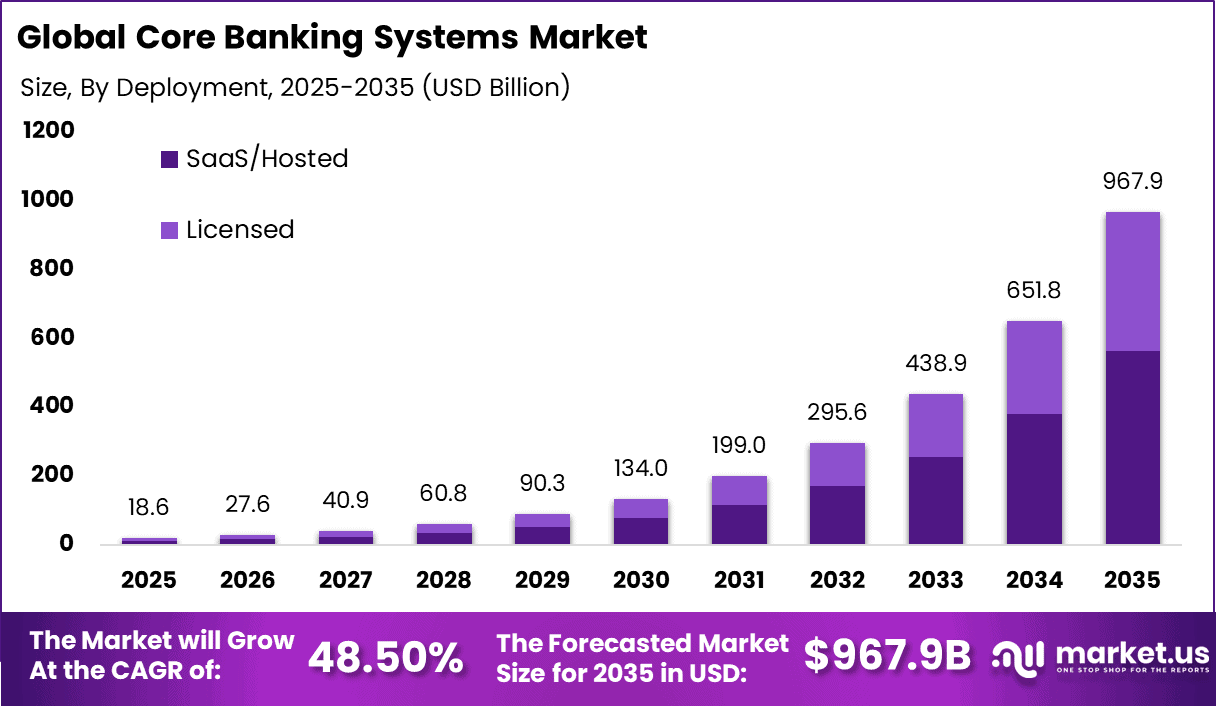

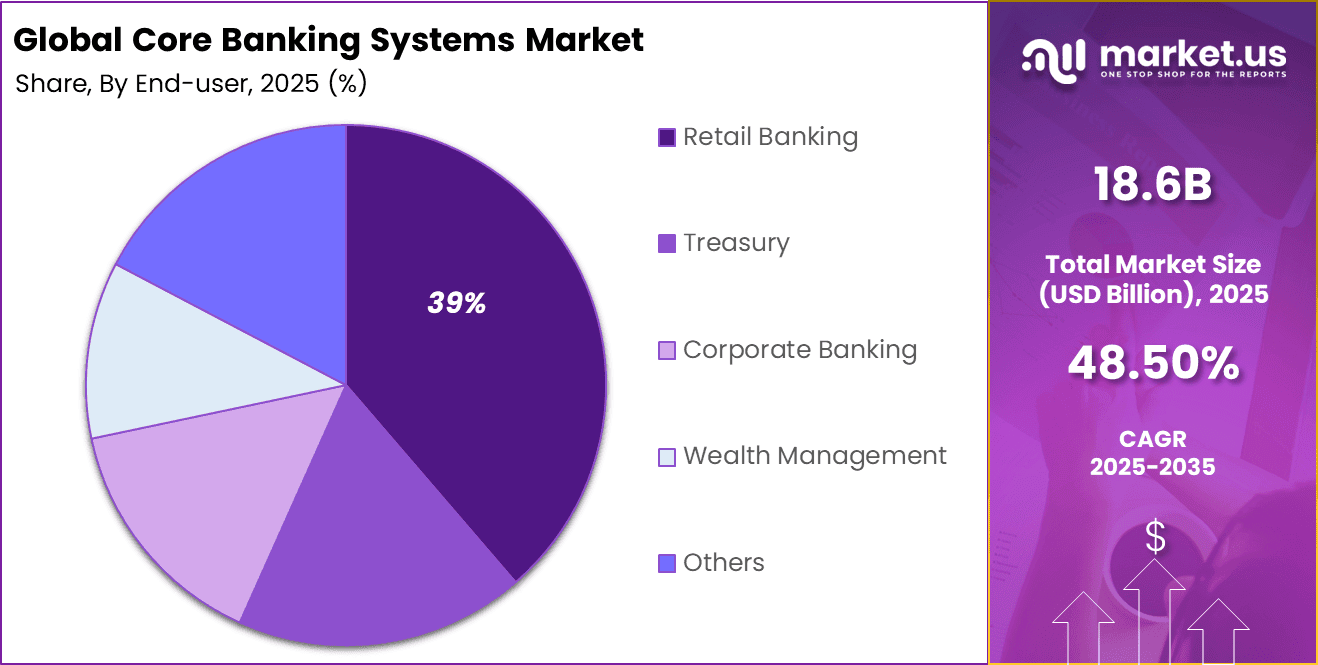

The Global Core Banking Systems Market generated USD 18.6 billion in 2025 and is predicted to register growth from USD 27.6 billion in 2026 to about USD 967.9 billion by 2035, recording a CAGR of 48.50% throughout the forecast span. In 2025, North America held a dominan market position, capturing more than a 39.4% share, holding USD 7.41 Billion revenue.

The Core Banking Systems Market covers software platforms that manage essential banking operations such as deposits, loans, payments, customer accounts, and transaction processing. These systems form the operational backbone of retail, corporate, and digital banks. Core banking platforms enable real-time processing across branches, digital channels, and third-party integrations. Their reliability and scalability are critical to daily banking operations.

Modern core banking systems are evolving from legacy, branch-centric architectures to centralized and modular platforms. This transition supports real-time access, faster product launches, and improved customer service. As banking services become increasingly digital, core systems are no longer back-office tools but strategic enablers. This shift elevates their importance across the financial services ecosystem.

One major driving factor is the rapid shift toward digital banking and omni-channel service delivery. Customers expect seamless access to banking services through mobile, web, and branch channels. Legacy systems often struggle to support these expectations due to rigid architectures. This gap drives banks to modernize or replace core banking platforms.

Cloud computing is a key technology influencing core banking system adoption. Cloud-based platforms offer scalability, cost efficiency, and faster deployment compared to traditional on-premise systems. They also support continuous updates and improved resilience. These advantages drive growing interest in cloud-native core systems.

Demand for core banking systems is driven by both system replacement and expansion needs. Many financial institutions operate on aging platforms that are costly to maintain and difficult to upgrade. These institutions seek modern systems to reduce operational risk and technical debt. Replacement demand is therefore a major contributor.

Top Market Takeaways

- By deployment, SaaS/hosted solutions captured 58.2% of the core banking systems market, offering scalable, cost-effective platforms with rapid updates and cloud flexibility.

- By banking type, large banks with over USD 30 billion in assets held 40.6%, modernizing legacy systems for complex operations and regulatory compliance.

- By end-user, retail banking led at 38.7%, focusing on digital channels, customer personalization, and transaction processing efficiency.

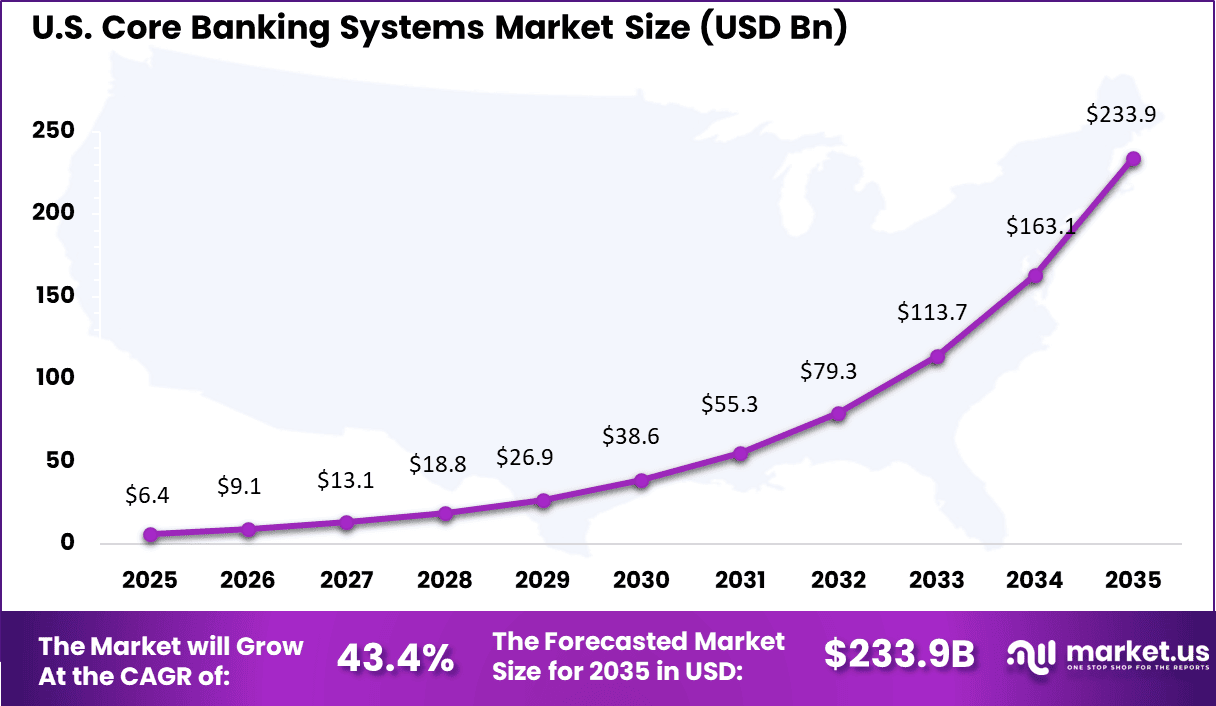

- North America accounted for 39.4% of the global market, with the U.S. valued at USD 6.36 billion and growing at a CAGR of 43.4%.

Key Insights Summary

Core Banking Adoption Rates (2026)

- About 68% of banks globally have adopted cloud native platforms for core banking operations as of early 2026.

- Around 78% of banks have deployed SaaS based core banking platforms to support AI adoption and real time data processing, resulting in up to 30% reduction in operational costs.

- More than 50% of banking institutions have either adopted modern core systems or have active plans to do so within the next two years.

- Nearly 89% of digital only banks and neobanks launch with fully cloud based core infrastructure.

Usage and Workload Statistics

- Around 60% of banks have migrated at least 30% of critical workloads to the cloud by 2026.

- Legacy infrastructure maintenance continues to consume about 70% of bank technology budgets, limiting modernization speed.

- SaaS and hosted deployment models are projected to hold 67.54% market share by late 2026.

- On premises systems remain in use among some large banks due to regulatory and data residency requirements.

- About 82% of financial institutions operate using hybrid or multi cloud strategies.

Modernization Impact and Efficiency Gains

- Core banking modernization delivers 35% to 38% improvement in operational efficiency.

- Loan processing times decline by 42% following modernization.

- Transaction processing times reduce by 53% with modern core platforms.

- Migration to SaaS based systems can generate long term cost savings of up to 40%.

Drivers Impact Analysis

| Key Driver | Impact on CAGR Forecast (~)% | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated migration from legacy core systems to cloud-native platforms | +12.4% | North America, Europe | Short to medium term |

| Rapid expansion of digital banks and fintech-led banking models | +10.6% | Europe, Asia Pacific | Medium term |

| Demand for real-time payments and instant account processing | +9.1% | Global | Short to medium term |

| Regulatory push for transparency, reporting, and compliance automation | +8.3% | Europe, North America | Medium term |

| Growing adoption of Banking-as-a-Service and open banking models | +6.8% | North America, Asia Pacific | Medium to long term |

Restraint Impact Analysis

| Key Restraint | Impact on CAGR Forecast (~)% | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High migration cost and operational risk during core replacement | -8.6% | Global | Short to medium term |

| Complexity of integrating legacy data and workflows | -7.2% | Global | Medium term |

| Shortage of skilled core banking and cloud specialists | -6.1% | Asia Pacific, Latin America | Medium term |

| Long decision cycles in large traditional banks | -5.0% | Europe, North America | Medium term |

| Data security and system resilience concerns | -4.2% | Global | Medium to long term |

Investor Type Impact Matrix

| Investor Type | Growth Sensitivity | Risk Exposure | Geographic Focus | Investment Outlook |

|---|---|---|---|---|

| Core banking software providers | Very High | Medium | Global | Strong recurring SaaS and license growth |

| Cloud infrastructure and platform providers | Very High | Medium | North America, Europe | Strategic backbone of banking modernization |

| Fintech and digital bank operators | High | Medium | Europe, Asia Pacific | Competitive differentiation and scale |

| Private equity firms | Medium | Medium | North America, Europe | Modernization-led consolidation plays |

| Venture capital investors | High | High | North America | Focus on cloud-native and API-first cores |

Deployment Analysis

SaaS and hosted deployment accounts for 58.2% of the Core Banking Systems market, showing a clear shift away from traditional on-premises systems. Banks adopt hosted core banking platforms to reduce infrastructure burden and improve system flexibility. These platforms allow banks to access core functions such as account management, transaction processing, and reporting through secure cloud environments.

SaaS deployment also supports faster upgrades and easier compliance with changing regulatory requirements. From an operational standpoint, SaaS and hosted models help banks lower capital expenditure and move toward predictable operating costs.

System updates, security patches, and performance improvements are handled centrally, reducing IT workload. The strong share of this segment reflects banks’ focus on agility, scalability, and faster time to market for new banking products and services.

Banking Type Analysis

Large banks with assets above USD 30 billion account for 40.6% of the market, highlighting strong adoption among institutions with complex operations. These banks manage high transaction volumes, diverse product portfolios, and large customer bases. Modern core banking systems help them centralize operations and standardize processes across branches and regions. This improves efficiency and operational visibility.

Large banks also face high regulatory scrutiny and require robust reporting and risk management capabilities. Advanced core banking platforms support compliance, data accuracy, and audit readiness. The strong presence of this segment reflects the need for reliable and scalable core systems to support enterprise-level banking operations.

End-User Analysis

Retail banking represents 39% of end-user demand, making it the largest application area for core banking systems. Retail banks rely on core platforms to manage savings accounts, loans, payments, and customer transactions. A modern core system ensures real-time processing and consistent customer experience across digital and branch channels.

Retail banking operations also require frequent product updates and customer-centric features. Core banking systems enable faster launch of new offerings and support digital banking services. The strong share of this segment reflects ongoing digital transformation in retail banking and growing demand for efficient and responsive banking platforms.

Investment and Business Benefits

Investment opportunities exist in modular core banking platforms that support phased modernization. Banks prefer solutions that allow gradual migration rather than full system replacement. Modular systems reduce disruption and implementation risk. This creates sustained demand for adaptable solutions.

There is also opportunity in managed services and system integration offerings. Core banking transformation requires planning, customization, and long-term support. Service providers that assist throughout the lifecycle add significant value. This service-driven approach supports recurring revenue models.

For banks, modern core banking systems improve service reliability and customer experience. Real-time processing enables faster transactions and account updates. Improved system performance reduces downtime and operational errors. These benefits strengthen customer trust and satisfaction.

From an internal perspective, modern systems enhance transparency and control. Centralized data improves reporting and decision-making. Automation reduces manual processing and error rates. These efficiencies support sustainable operational performance.

Emerging Trends Analysis

An emerging trend in the core banking systems market is the shift toward real time processing capabilities. Real time payments and instant account updates are becoming standard expectations. Core platforms are evolving to support continuous transaction processing rather than batch based operations. This trend improves customer experience and operational responsiveness.

Another trend is increased focus on interoperability through open interfaces. Open banking frameworks encourage secure data sharing with third party services. Core systems are being designed to support standardized interfaces that allow controlled data access. This trend supports innovation and ecosystem expansion.

Growth Factors Analysis

One key growth factor for the core banking systems market is the expansion of digital financial services across emerging economies. Increased access to banking services creates demand for scalable and reliable core platforms. As more users enter the formal banking system, transaction volumes grow. Core systems are essential to support this expansion.

Another growth factor is the need for operational efficiency and cost control. Automated processing reduces manual intervention and error rates. Core banking platforms help banks streamline operations and improve service consistency. This efficiency driven demand supports long term market growth.