Global Computer Room Air Conditioning Market Size, Share, Growth Analysis By Type (Precision Air Conditioners, Comfort Air Conditioners), By Cooling System (Chilled Water, Direct Expansion), By Power Output (Up to 50 kW, 50 to 100 kW, Greater than 100 kW), By End-User (Data Centers, Server Rooms, Network Rooms, Others), By Organization Size (Large Enterprises, Small & Medium Enterprises), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 179389

- Number of Pages: 364

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

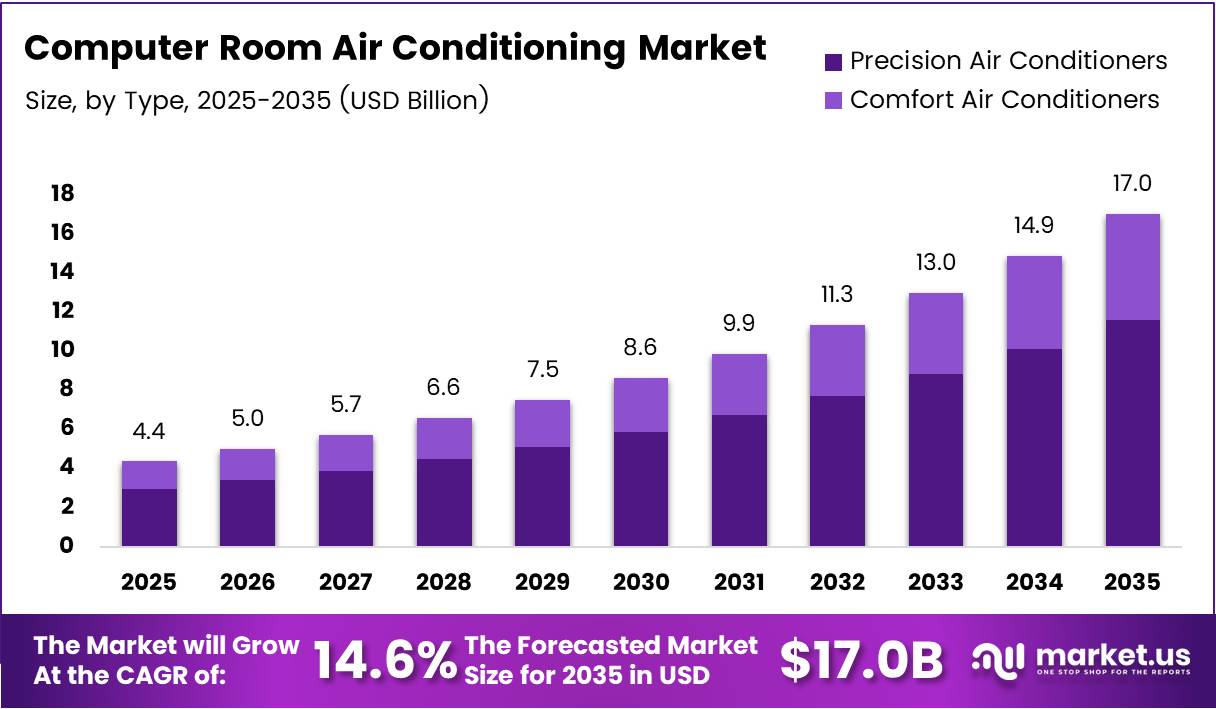

Global Computer Room Air Conditioning Market size is expected to be worth around USD 17.0 Billion by 2035 from USD 4.4 Billion in 2025, growing at a CAGR of 14.60% during the forecast period 2026 to 2035.

The computer room air conditioning (CRAC) market covers precision cooling systems designed to manage thermal loads in data centers, server rooms, and network facilities. Unlike comfort cooling, CRAC units deliver targeted temperature and humidity control to protect sensitive IT equipment. This distinction drives a separate procurement cycle with tighter performance specifications.

Hyperscale data center expansion by operators such as Amazon Web Services and Microsoft Azure directly pushes demand for precision cooling infrastructure. These facilities require consistent thermal management at scale, where a single degree of variation can trigger equipment failure. This creates a capital-intensive, specification-driven procurement environment that favors established precision cooling vendors over general HVAC suppliers.

In May 2025, Samsung Electronics announced it would acquire Germany-based FläktGroup for €1.5 billion, signaling that large electronics manufacturers view precision data center cooling as a strategic growth vertical. This level of M&A activity confirms that the CRAC market has moved beyond niche infrastructure into a boardroom-level priority.

Energy efficiency regulations, including ASHRAE thermal guidelines, now directly shape purchasing decisions. Operators cannot simply add cooling capacity — they must demonstrate PUE compliance and carbon footprint reduction. This compliance pressure shortens equipment replacement cycles and accelerates the upgrade of older CRAC installations with energy-efficient alternatives.

According to Google Data Centers, Google’s global data center fleet achieved an average annual Power Usage Effectiveness (PUE) of 1.09 as of Q3 2025. This benchmark illustrates how aggressively hyperscale operators optimize cooling performance. For CRAC vendors, this sets a de facto performance floor — buyers now expect systems that can support sub-1.2 PUE outcomes at scale.

According to academic modeling research, cooling systems account for approximately 40% of total data center electrical energy use. This single figure explains why data center operators treat cooling as a cost center requiring active engineering — not just a utility. Vendors that offer measurable energy savings gain direct access to capex budgets tied to operational cost reduction programs.

Key Takeaways

- The global Computer Room Air Conditioning Market was valued at USD 4.4 Billion in 2025 and is forecast to reach USD 17.0 Billion by 2035.

- The market grows at a CAGR of 14.60% during the forecast period 2026 to 2035.

- By Type, Precision Air Conditioners dominate with a 96.30% share in 2025.

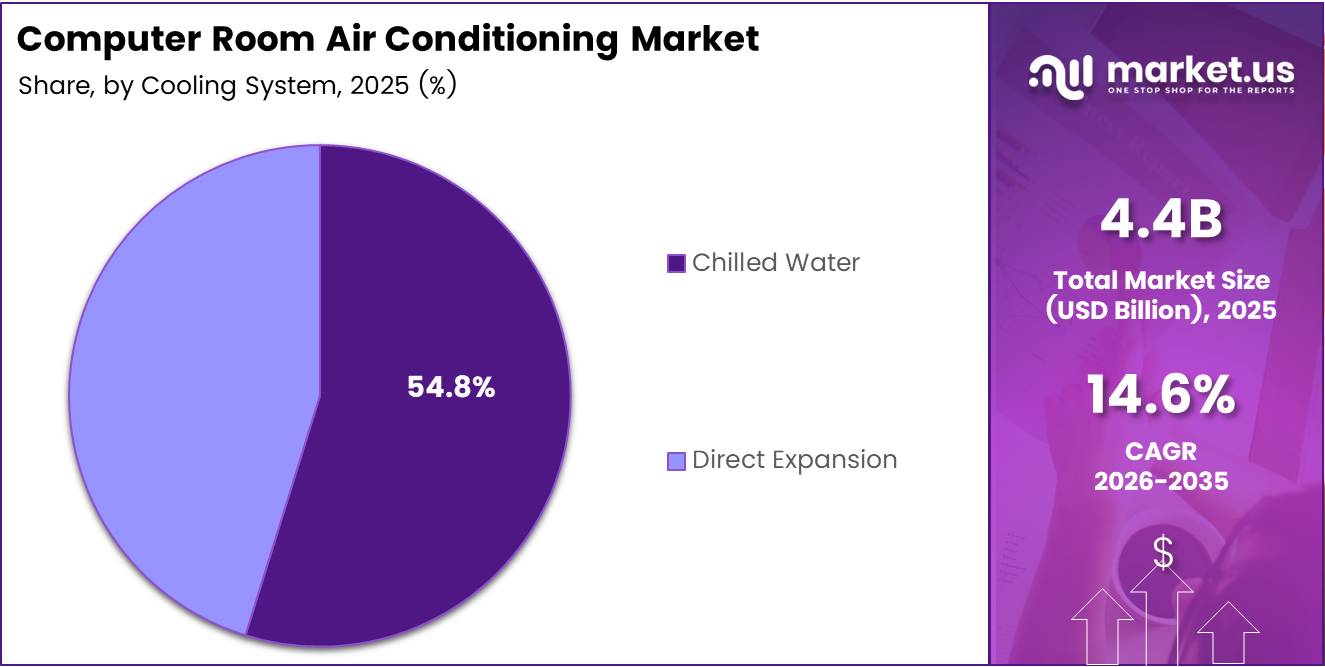

- By Cooling System, Chilled Water leads with a 54.80% share in 2025.

- By Power Output, Greater than 100 kW holds the largest share at 44.71% in 2025.

- By End-User, Data Centers account for 62.50% of total market share in 2025.

- By Organization Size, Large Enterprises dominate with a 73.29% share in 2025.

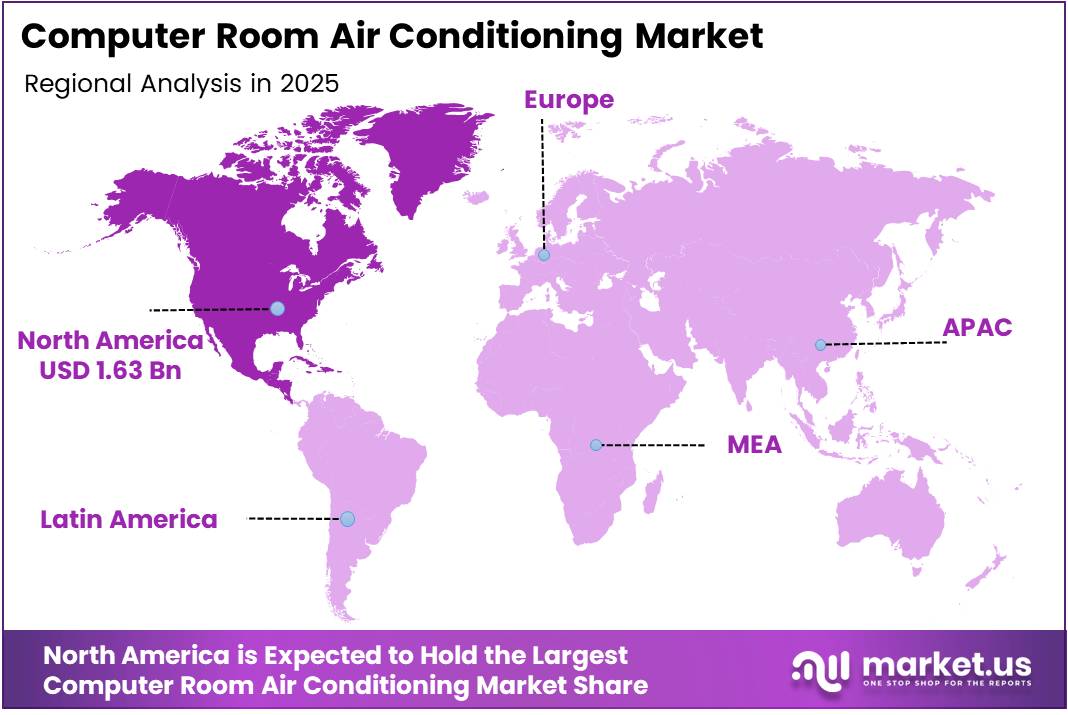

- North America leads regional markets with a 37.46% share, valued at USD 1.63 Billion in 2025.

Type Analysis

Precision Air Conditioners dominate with 96.30% due to mission-critical thermal control requirements.

In 2025, Precision Air Conditioners held a dominant market position in the By Type segment of the Computer Room Air Conditioning Market, with a 96.30% share. These units deliver temperature accuracy within ±1°C and humidity control that comfort systems cannot match. This precision directly protects IT uptime, making substitution economically irrational for data center operators.

Comfort Air Conditioners serve as supplementary cooling in small server closets and low-density network rooms where precision tolerances are not required. Their lower cost makes them accessible for budget-constrained SME deployments. However, as rack power densities rise with AI workloads, comfort units face displacement by precision alternatives even in these lower-tier environments.

Cooling System Analysis

Chilled Water dominates with 54.80% due to scalability in large-facility deployments.

In 2025, Chilled Water systems held a dominant market position in the By Cooling System segment of the Computer Room Air Conditioning Market, with a 54.80% share. Chilled water infrastructure suits large-scale data centers where centralized plant efficiency outweighs installation complexity. Operators building at hyperscale consistently specify chilled water to achieve the PUE targets that energy regulations now mandate.

Direct Expansion (DX) cooling offers faster deployment and lower upfront plant costs, making it the preferred choice for edge deployments, smaller colocation facilities, and retrofit scenarios. DX systems do not require complex chiller plant infrastructure, which reduces commissioning time. Consequently, edge computing expansion across Tier II and Tier III cities creates a structural demand channel for DX-based CRAC installations.

Power Output Analysis

Greater than 100 kW dominates with 44.71% due to high-density hyperscale facility requirements.

In 2025, the Greater than 100 kW segment held a dominant market position in the By Power Output segment of the Computer Room Air Conditioning Market, with a 44.71% share. Hyperscale and large colocation facilities require high-capacity cooling units to handle concentrated heat loads from AI-optimized server racks. NVIDIA GPU-dense configurations generate thermal loads that only high-output CRAC systems can reliably manage.

50 to 100 kW systems serve mid-tier data centers and enterprise server rooms where power density is moderate but growing. These buyers face upgrade pressure as they refresh aging server hardware with higher-TDP processors. This creates a recurring replacement cycle that sustains revenue for mid-range CRAC vendors throughout the forecast period.

Up to 50 kW units address small server rooms, network closets, and edge micro-data centers where floor space and power budgets are constrained. The rise of distributed edge computing infrastructure expands the addressable site count for this segment. However, average unit values remain low, limiting revenue concentration in this tier.

End-User Analysis

Data Centers dominate with 62.50% due to high-density, continuous cooling requirements.

In 2025, Data Centers held a dominant market position in the By End-User segment of the Computer Room Air Conditioning Market, with a 62.50% share. Hyperscale and colocation operators drive bulk procurement of precision CRAC systems with strict performance SLAs. Their continuous 24/7 operational requirement means cooling failures translate directly to revenue loss, justifying premium system investment.

Server Rooms within enterprises and financial institutions represent a stable but slower-growth end-user category. These facilities typically operate smaller footprints with moderate cooling loads. However, the adoption of AI inference workloads within enterprise IT environments gradually pushes server room thermal loads upward, triggering CRAC upgrades in this segment.

Network Rooms house telecommunications and routing equipment with more predictable and lower heat outputs than compute-dense environments. Cooling requirements here favor reliability and redundancy over raw capacity. Vendors targeting this segment compete more on service contracts and uptime guarantees than on unit performance specifications.

Others includes healthcare IT infrastructure, government facilities, and defense computing installations where compliance requirements often mandate dedicated precision cooling. These buyers prioritize regulatory conformance and long system lifespans. This creates a defensible niche for vendors with documented compliance certifications and extended warranty programs.

Organization Size Analysis

Large Enterprises dominate with 73.29% due to complex, multi-site cooling infrastructure needs.

In 2025, Large Enterprises held a dominant market position in the By Organization Size segment of the Computer Room Air Conditioning Market, with a 73.29% share. These organizations operate dedicated data centers with significant rack counts, requiring centralized precision cooling infrastructure at scale. Their procurement processes favor established vendors with proven enterprise service networks and long-term maintenance contracts.

Small and Medium Enterprises (SMEs) represent an underserved but structurally expanding buyer segment as edge computing and cloud-hybrid architectures push localized server infrastructure into smaller organizations. SMEs typically opt for DX-based CRAC solutions with lower upfront costs. As modular and containerized data center formats become more accessible, SME adoption of precision cooling will accelerate during the forecast period.

Key Market Segments

By Type

- Precision Air Conditioners

- Comfort Air Conditioners

By Cooling System

- Chilled Water

- Direct Expansion

By Power Output

- Up to 50 kW

- 50 to 100 kW

- Greater than 100 kW

By End-User

- Data Centers

- Server Rooms

- Network Rooms

- Others

By Organization Size

- Large Enterprises

- Small & Medium Enterprises (SMEs)

Drivers

Hyperscale Expansion and Rising Rack Power Density Force Precision Cooling Upgrades Across Data Center Infrastructure

Hyperscale data center buildouts by operators like Amazon Web Services and Microsoft Azure require precision cooling infrastructure at a scale that general HVAC systems cannot serve. These facilities demand temperature accuracy and redundancy that only CRAC systems deliver. This creates a direct, high-value procurement pipeline for precision cooling vendors tied to hyperscale capital programs.

According to Tom’s Hardware, nearly 7,000 out of 8,808 operational data centers worldwide sit outside the ASHRAE-recommended optimal temperature range of 18°C–27°C. This structural mismatch increases cooling load and raises operational energy costs. For CRAC vendors, it represents a documented upgrade and remediation opportunity across a majority of the global installed base.

NVIDIA’s AI-optimized server configurations push rack power densities to levels where legacy CRAC installations fail to maintain safe operating temperatures. In September 2025, Johnson Controls launched its Silent-Aire Coolant Distribution Unit platform, offering scalable liquid cooling solutions up to 10 MW — a direct response to this thermal escalation. Vendors that align product roadmaps with GPU-driven heat loads capture the highest-value replacement cycles.

Restraints

High Capital Costs and the Shift Toward Liquid Cooling Limit Traditional CRAC System Adoption

Precision cooling infrastructure carries significant upfront capital costs, including equipment, installation, and commissioning expenses that strain budgets for smaller operators and emerging market data center developers. Lifecycle maintenance adds further cost pressure, including refrigerant management, component replacement, and compliance-driven system audits. These combined costs create a financing barrier that slows adoption among non-hyperscale buyers.

The shift toward liquid cooling and immersion cooling technologies directly challenges the long-term role of traditional air-based CRAC systems. According to All About AI, approximately 73% of new AI facilities deploy direct-to-chip or immersion liquid cooling to manage high heat loads. This adoption rate signals that traditional CRAC vendors must reposition their portfolios or risk structural revenue decline in the highest-growth data center segment.

These two restraints compound each other. Operators facing high CRAC capital costs now have a technically credible alternative in liquid cooling, reducing the economic pressure to upgrade existing air systems. Vendors relying on traditional CRAC replacement cycles must accelerate their entry into hybrid and liquid-assisted cooling formats to retain relevance with the buyer segment building next-generation AI infrastructure.

Growth Factors

AI-Driven Predictive Maintenance, Modular Data Centers, and Renewable-Powered Cooling Open New Revenue Channels

AI-based predictive maintenance integration transforms CRAC units from passive infrastructure into active cost management tools. According to arXiv research, an offline reinforcement learning model demonstrated 14–21% cooling energy savings in a large production data center. Vendors embedding this capability into CRAC systems can directly quantify operational savings, shifting the sales conversation from capital cost to ROI-driven justification.

In October 2025, Johnson Controls made a multi-million-dollar strategic investment in Accelsius, a liquid cooling company focused on two-phase, direct-to-chip solutions. This investment pattern illustrates how established CRAC vendors are funding adjacent technologies to retain data center operator relationships. Companies that build hybrid air-and-liquid portfolios position themselves as single-source thermal management partners rather than point-solution suppliers.

Expansion of modular and containerized data centers in emerging economies creates new deployment sites that require purpose-built precision cooling from day one. Retrofitting legacy server rooms with variable speed CRAC solutions offers a near-term revenue channel in mature markets where full replacement is not yet justified. Renewable energy-powered cooling systems address carbon neutrality mandates, opening budget access in organizations with active ESG commitments.

Emerging Trends

Close-Coupled Architectures, Free Cooling Integration, and Low-GWP Refrigerants Redefine CRAC System Design Standards

In-row and close-coupled cooling architectures concentrate thermal management directly at the heat source, reducing the energy losses inherent in room-level air distribution. This design shift reflects the reality that AI server racks generate heat at densities that perimeter CRAC units cannot efficiently capture. Vendors that offer close-coupled product lines gain specification preference in new high-density data center builds.

Free cooling and economizer modes allow colocation facilities to use ambient air conditions to offset mechanical cooling loads, directly reducing energy costs during favorable weather periods. In March 2025, CoolIT Systems showcased AI-ready liquid cooling technologies at NVIDIA GTC 2025, highlighting how the industry connects thermal innovation directly to AI workload requirements. This event-driven visibility accelerates enterprise awareness and procurement consideration cycles.

Low global warming potential (GWP) refrigerant mandates from environmental regulators force CRAC manufacturers to reformulate system designs ahead of compliance deadlines. Digital twin integration for real-time thermal optimization gives operators continuous visibility into cooling performance without manual audits. Together, these developments move CRAC systems from static hardware assets toward software-managed, continuously optimized infrastructure components.

Regional Analysis

North America Dominates the Computer Room Air Conditioning Market with a Market Share of 37.46%, Valued at USD 1.63 Billion

North America holds 37.46% of the global market, valued at USD 1.63 Billion in 2025. The region’s position reflects early hyperscale data center concentration, mature colocation infrastructure, and ASHRAE compliance mandates that accelerate CRAC upgrade cycles. US-based cloud operators run among the largest precision cooling procurement programs globally, sustaining a structurally elevated demand baseline.

Europe Computer Room Air Conditioning Market Trends

Europe enforces stringent energy efficiency and refrigerant regulations that push data center operators to upgrade aging CRAC infrastructure faster than in less regulated markets. Germany, the UK, and the Netherlands house major colocation hubs that drive regional procurement. The EU’s F-Gas regulation timeline on high-GWP refrigerants creates a mandatory replacement cycle that benefits low-GWP CRAC system vendors.

Asia Pacific Computer Room Air Conditioning Market Trends

Asia Pacific represents the fastest-expanding regional market, driven by hyperscale data center investments across China, India, Japan, and Southeast Asia. In October 2025, Johnson Controls introduced its Silent-Aire CDU liquid cooling solution specifically for high-density data centers in the Asia Pacific region, signaling vendor recognition of this geography as a priority growth market.

Middle East and Africa Computer Room Air Conditioning Market Trends

The Middle East and Africa region faces a structural cooling challenge: approximately 600 facilities globally operate in regions with average annual temperatures above 27°C, and a significant portion of these sit in the MEA geography. This climate mismatch increases cooling energy requirements and drives adoption of high-capacity, energy-efficient CRAC systems in Gulf state data center developments.

Latin America Computer Room Air Conditioning Market Trends

Latin America’s CRAC market centers on Brazil and Mexico, where digital infrastructure investment and colocation expansion create new data center sites requiring precision cooling. Cost sensitivity and infrastructure maturity gaps mean buyers in this region favor modular and DX-based CRAC solutions over complex chilled water installations. Government-backed digital economy programs in Brazil create a policy tailwind for data center infrastructure investment.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Vertiv Holdings Co. positions itself as a full-spectrum data center infrastructure provider, with thermal management as a core revenue pillar. In November 2025, Vertiv completed its acquisition of PurgeRite Intermediate for approximately $1 billion, expanding its liquid cooling and thermal services portfolio. This acquisition signals Vertiv’s intent to capture the liquid cooling transition rather than defend its legacy CRAC installed base.

Johnson Controls International plc pursues a hybrid strategy that combines traditional precision air cooling with aggressive investment in liquid cooling adjacencies. The company launched the Silent-Aire CDU platform for deployments up to 10 MW and invested in Accelsius for two-phase liquid cooling. This dual-track approach lets Johnson Controls serve both the existing CRAC replacement market and the new high-density AI data center segment simultaneously.

Eaton entered the data center thermal solutions space at scale with its $9.5 billion agreement to acquire the Boyd Thermal business in November 2025. This transaction repositions Eaton from a power management company into a comprehensive data center infrastructure provider. The acquisition scale signals that Eaton views thermal management as a structurally important and margin-rich addition to its existing data center power portfolio.

CoolIT Systems occupies a specialized position in high-performance liquid cooling, targeting the AI and HPC workload segments that generate the most aggressive thermal loads. The company unveiled a direct liquid cooling coldplate capable of managing chips up to 4,000 W in March 2025. This technical capability addresses a specific gap in the market — thermal management for next-generation GPU and accelerator hardware — where established CRAC vendors have limited credibility.

Key players

- Vertiv Holdings Co.

- Johnson Controls International plc

- Eaton Corporation

- CoolIT Systems

- Schneider Electric

- Emerson Electric Co.

- Stulz GmbH

- Rittal GmbH & Co. KG

- Airedale International Air Conditioning

- Samsung Electronics

Recent Developments

- November 2025 – Vertiv Holdings Co. completed its acquisition of PurgeRite Intermediate for approximately $1 billion, expanding its liquid cooling and thermal services portfolio for data centers. This transaction reinforces Vertiv’s strategic pivot toward liquid-based thermal management to serve AI-driven data center buildouts.

- November 2025 – Eaton signed an agreement to acquire the Boyd Thermal business for $9.5 billion, gaining advanced liquid cooling technologies to strengthen its data center and thermal solutions offerings. The acquisition scale positions Eaton as a major competitor in the precision cooling market across air and liquid cooling formats.

- March 2025 – CoolIT Systems unveiled a single-phase direct liquid cooling coldplate prototype capable of cooling chips up to 4,000 W, directly addressing the thermal management demands of AI and HPC workloads. This development advances the performance ceiling for chip-level liquid cooling beyond what traditional CRAC air systems can address.

- September 2025 – Swiss startup Corintis raised $24 million in Series A funding and added Intel CEO Lip-Bu Tan to its board, scaling production of liquid cooling cold plates for semiconductors. The board appointment signals strategic alignment with leading chip manufacturers and validates microfluidic cooling as a viable next-generation thermal solution.

- September 2025 – Microsoft and Corintis collaborated on a microfluidic cooling technique that reduces peak chip temperatures by up to 65%, introducing a new thermal management approach beyond conventional cold plates. This partnership demonstrates that hyperscale operators are actively co-developing cooling technologies rather than waiting for vendor-led solutions.

Report Scope

Report Features Description Market Value (2025) USD 4.4 Billion Forecast Revenue (2035) USD 17.0 Billion CAGR (2026-2035) 14.60% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Precision Air Conditioners, Comfort Air Conditioners), By Cooling System (Chilled Water, Direct Expansion), By Power Output (Up to 50 kW, 50 to 100 kW, Greater than 100 kW), By End-User (Data Centers, Server Rooms, Network Rooms, Others), By Organization Size (Large Enterprises, Small & Medium Enterprises) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Vertiv Holdings Co., Johnson Controls International plc, Eaton Corporation, CoolIT Systems, Schneider Electric, Emerson Electric Co., Stulz GmbH, Rittal GmbH & Co. KG, Airedale International Air Conditioning, Samsung Electronics Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Computer Room Air Conditioning MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample

Computer Room Air Conditioning MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Vertiv Holdings Co.

- Johnson Controls International plc

- Eaton Corporation

- CoolIT Systems

- Schneider Electric

- Emerson Electric Co.

- Stulz GmbH

- Rittal GmbH & Co. KG

- Airedale International Air Conditioning

- Samsung Electronics

Our Clients

- 179389

- Feb 2026