Global Competent Cells Market By Product Type (Chemically Competent Cells, Ultracompetent Cells and Electrocompetent Cells), By Application (Cloning, Mutagenesis, Protein Expression and Others), By End-User (Pharmaceutical & Biotechnology Companies, Academic & Research Institutes and Others), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2034

- Published date: Jan 2026

- Report ID: 174169

- Number of Pages: 198

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

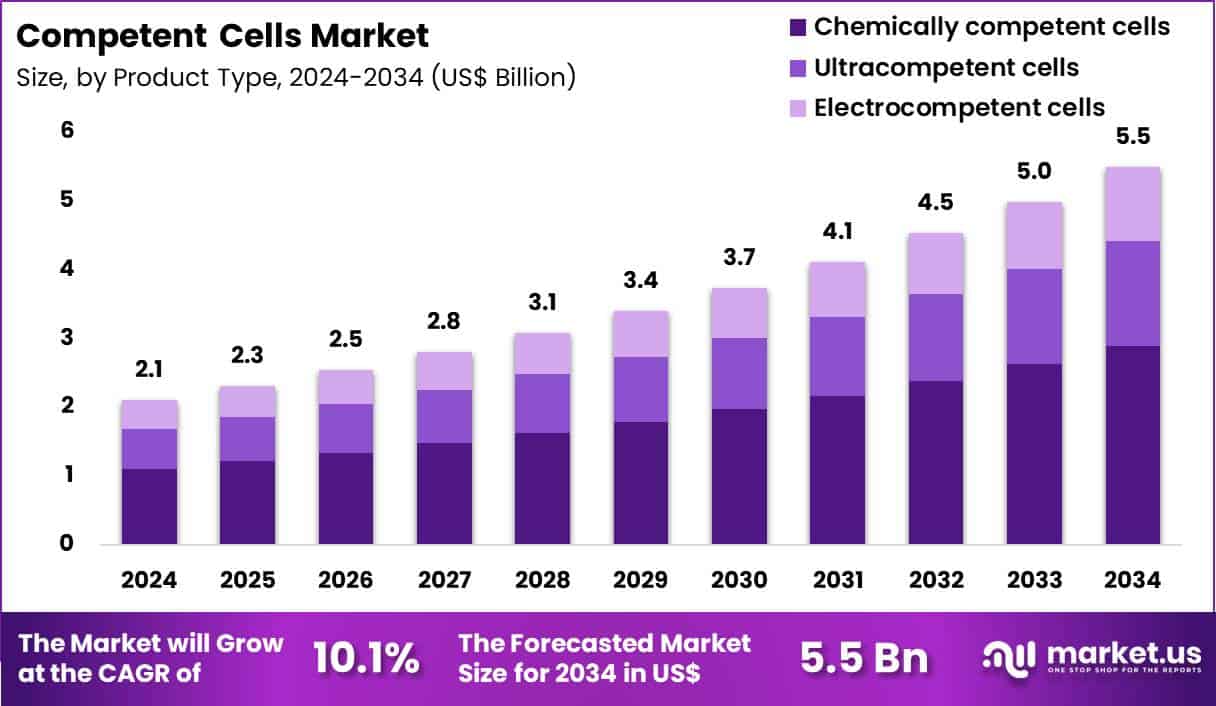

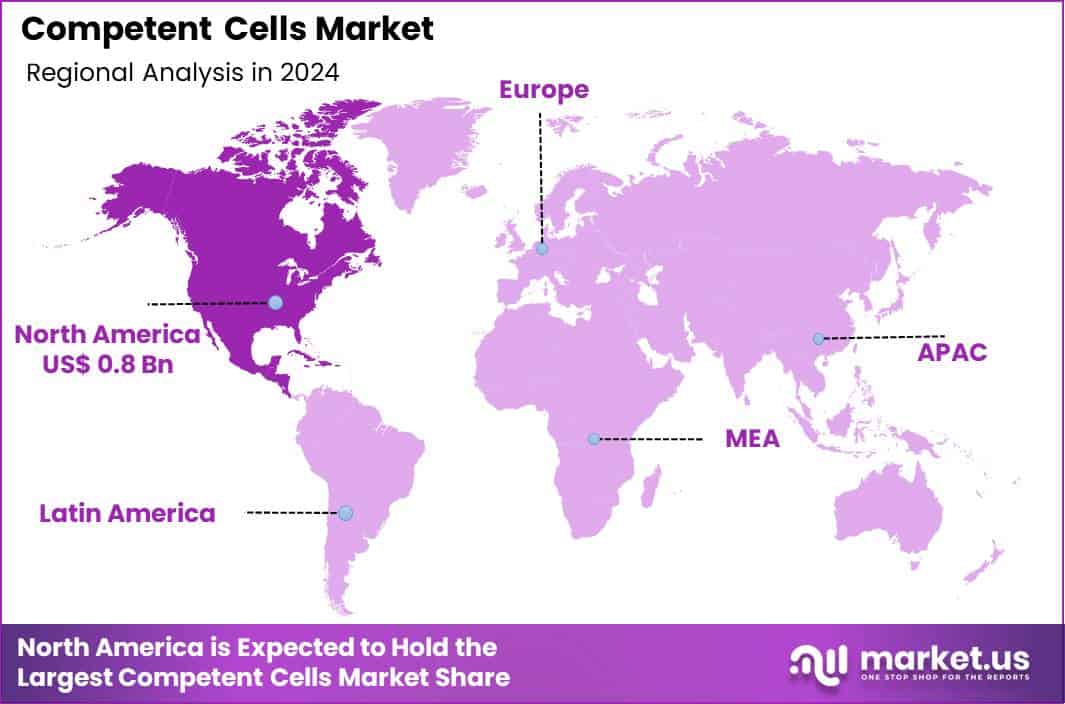

The Global Competent Cells Market size is expected to be worth around US$ 5.5 Billion by 2034 from US$ 2.1 Billion in 2024, growing at a CAGR of 10.1% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 38.8% share with a revenue of US$ 0.8 Billion.

The competent cells market is expanding as demand for recombinant DNA technologies rises across molecular biology, synthetic biology, and industrial biotechnology. Researchers widely use chemically competent and electrocompetent E. coli strains for gene cloning, protein expression, and high-throughput screening, enabling rapid construction of expression vectors and large genetic libraries.

These cells play a critical role in enzyme discovery, antibody development, site-directed mutagenesis, and metabolic engineering, supporting applications ranging from pharmaceutical research to industrial biocatalysis. In December 2023, CCM Biosciences launched its 5Prime Sciences division focused on advanced DNA tools and enzyme engineering, strengthening the development of cloning and synthetic biology technologies and reinforcing demand for high-performance competent cells.

Growth opportunities are emerging in specialized competent cells designed for difficult-to-clone sequences, large plasmids, and genome-editing workflows such as CRISPR-Cas9 and multiplex gene knockouts. Manufacturers are engineering strains with enhanced plasmid stability to support vaccine vector construction, viral particle production, and sustainable bio-based manufacturing.

Additional opportunities lie in competent cells optimized for non-model organisms, expanding genetic engineering capabilities in industrial bacteria and yeast. Recent trends focus on strain designs that reduce recombination, improve post-transformation recovery, and support large DNA constructs, including synthetic chromosomes. Companies are also prioritizing automation-ready formats and marker-free selection systems, aligning competent cell development with scalable, regulatory-compliant synthetic biology and advanced therapeutic production.

Key Takeaways

- In 2024, the market generated a revenue of US$ 2.1 Billion, with a CAGR of 10.1%, and is expected to reach US$ 5.5 Billion by the year 2034.

- The product type segment is divided into chemically competent cells, ultracompetent cells and electrocompetent cells, with chemically competent cells taking the lead in 2024 with a market share of 52.6%.

- Considering application, the market is divided into cloning, mutagenesis, protein expression and others. Among these, cloning held a significant share of 48.9%.

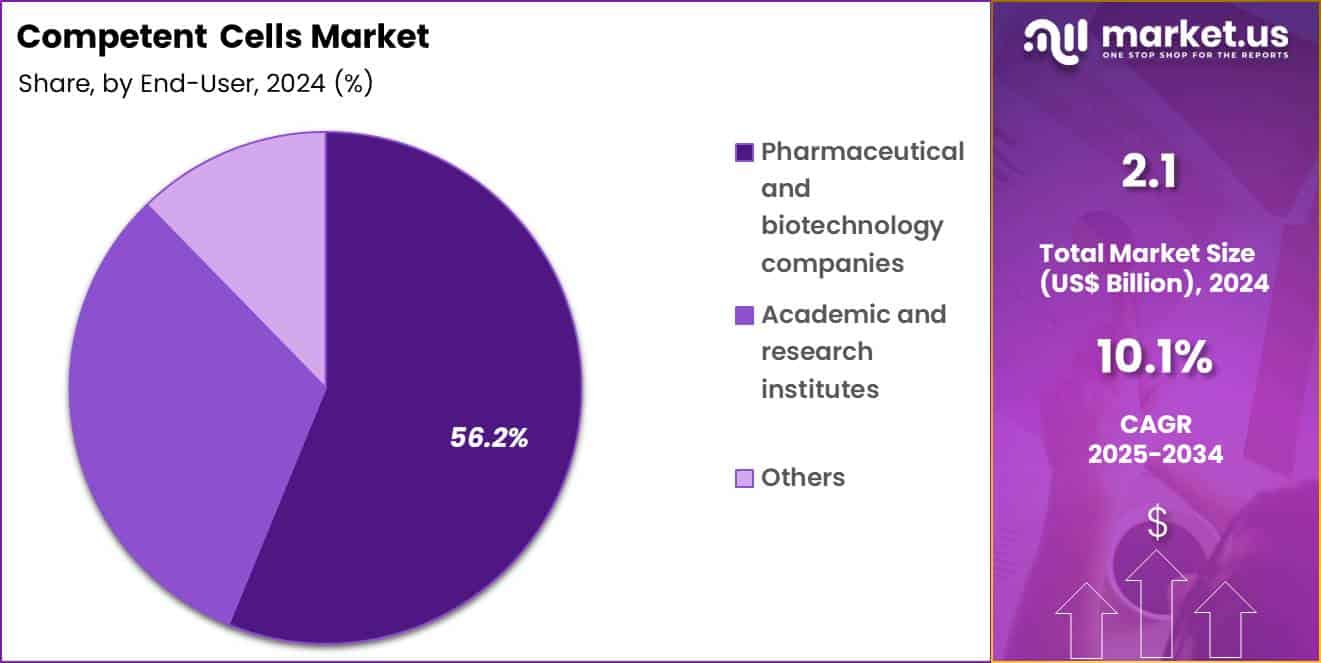

- Furthermore, concerning the end-user segment, the market is segregated into pharmaceutical & biotechnology companies, academic & research institutes and others. The pharmaceutical & biotechnology companies sector stands out as the dominant player, holding the largest revenue share of 56.2% in the market.

- North America led the market by securing a market share of 38.3% in 2024.

Product Type Analysis

Chemically competent cells accounted for 52.6% of growth within the product type category and represent the most widely adopted format in the Competent Cells market. Laboratories prefer chemically competent cells due to their ease of preparation and use. These cells support efficient plasmid uptake for routine molecular biology workflows. Cost-effectiveness strengthens adoption across high-throughput laboratories. Standard heat-shock protocols simplify training requirements for laboratory staff.

Consistent transformation efficiency supports reproducible experimental outcomes. Academic and industrial labs rely on chemically competent cells for daily cloning tasks. Compatibility with commonly used vectors increases usability. Shorter preparation time improves laboratory productivity. Suppliers offer a wide range of strains optimized for different applications. Shelf-stable formats support global distribution. Pharmaceutical laboratories prioritize reliability over ultra-high efficiency.

Reduced equipment dependency compared to electroporation improves accessibility. Chemically competent cells integrate seamlessly into standardized protocols. Routine research activities drive repeat purchasing behavior. Process scalability supports bulk procurement by large organizations.

Quality control improvements enhance transformation consistency. Entry-level researchers prefer chemically competent cells for simplicity. Expanding life science research activity sustains demand. The segment is projected to maintain dominance due to accessibility and operational efficiency.

Application Analysis

Cloning captured 48.9% of growth within the application category and stands as the primary driver of the Competent Cells market. Gene cloning remains fundamental to molecular biology research. Rising demand for recombinant DNA technologies supports sustained cloning activity. Pharmaceutical discovery pipelines rely heavily on gene cloning for target validation. Synthetic biology applications increase cloning frequency. Cloning workflows require reliable transformation performance.

High success rates reduce experimental repetition. Drug development programs depend on cloned constructs for screening assays. Academic research continuously generates new cloning requirements. Plasmid library construction increases transformation volumes. Biologics development drives complex cloning strategies.

Rapid cloning turnaround improves research timelines. Cloning supports downstream protein expression and mutagenesis workflows. Expanding genomics research increases cloning demand. Regulatory-driven research documentation strengthens cloning rigor. Automation adoption increases throughput of cloning experiments.

Cloning kits integrate efficiently with competent cell products. Funding growth in life sciences supports sustained research activity. Intellectual property generation increases cloning projects. The segment is anticipated to remain dominant due to foundational importance in molecular research.

End-User Analysis

Pharmaceutical and biotechnology companies accounted for 56.2% of growth within the end-user category and dominate the Competent Cells market. Drug discovery and development require extensive genetic manipulation. Biologics manufacturing depends on cloned and expressed genetic material. High R&D spending supports continuous procurement of competent cells. Pharmaceutical pipelines emphasize recombinant protein and gene-based therapies.

Biotechnology firms operate high-throughput molecular laboratories. Standardized workflows increase demand for reliable competent cell products. Internal quality standards favor commercially validated cell preparations. Scale of operations drives bulk purchasing agreements. Cell-based assay development relies on cloning efficiency. Vaccine research increases genetic engineering activity. Biosimilar development supports sustained molecular cloning needs.

Industrial timelines prioritize reproducibility and speed. Outsourcing trends still maintain in-house cloning capabilities. Advanced therapeutic research expands transformation requirements. Regulatory compliance encourages use of consistent cell systems.

Skilled workforce adoption supports high utilization rates. Innovation cycles increase experimental iterations. Strategic collaborations expand research volume. Capital investment in biotech infrastructure sustains demand. The segment is expected to retain dominance due to R&D intensity and commercial-scale research activity.

Key Market Segments

By Product Type

- Chemically competent cells

- Ultracompetent cells

- Electrocompetent cells

By Application

- Cloning

- Mutagenesis

- Protein expression

- Others

By End-User

- Pharmaceutical & biotechnology companies

- Academic & research institutes

- Others

Drivers

Rising R&D funding in biotechnology is driving the market

The competent cells market is propelled by the rising R&D funding in biotechnology, which supports the development of advanced cell lines for gene editing and cloning applications. Healthcare and biotech companies are increasing investments to enhance transformation efficiency in competent cells, driving innovation in molecular biology.

Regulatory agencies like the NIH are allocating substantial funds to projects involving cell biology, sustaining market momentum. Pharmaceutical firms are leveraging these funds to accelerate research in therapeutics, where competent cells play a key role in vector construction. Clinical protocols integrate competent cells for high-throughput screening, improving drug discovery processes. Global health initiatives promote biotech funding to address diseases through genetic research.

Academic institutions utilize grants to explore new competent cell strains for improved stability. Patient care benefits from advancements enabled by funded research in cell-based therapies. Economic returns from biotech investments further justify market expansion. The National Institutes of Health awarded approximately $37 billion in research funding in 2024.

Restraints

Market slump in life science research is restraining the market

The competent cells market is restrained by the market slump in life science research, which reduces demand for reagents and cell products due to economic slowdowns and inflation. Manufacturers face decreased sales as biotech firms cut R&D budgets, impacting production volumes. Regulatory compliance costs rise during slumps, deterring investment in new cell lines.

Pharmaceutical companies delay projects, limiting market penetration for competent cells. Clinical research slows, affecting the adoption of cell biology tools. Global economic uncertainties exacerbate the slump in research funding. Academic institutions reduce purchases of competent cells for experiments.

Patient therapies are indirectly affected by delayed innovations in gene research. Economic models project continued restraint without recovery in research spending. Takara Bio Group reported net sales of ¥43,505 million in FY2024, down from ¥78,142 million in FY2023.

Opportunities

Growth in gene therapy CDMO services is creating growth opportunities

The competent cells market offers growth opportunities through the growth in gene therapy CDMO services, where competent cells are essential for vector production and cell transfection. Developers can expand services to support clinical-grade cell lines for regenerative medicine. Regulatory frameworks encourage CDMO expansion for gene therapy, facilitating market entry.

Healthcare systems benefit from outsourced cell biology solutions for faster therapy development. Pharmaceutical partnerships focus on competent cells in robotic manufacturing for efficiency. Clinical research explores cell applications in targeted delivery for genetic disorders. Global adoption in emerging markets aligns with infrastructure development for biotech services.

Academic collaborations refine cell protocols to ensure quality in CDMO. Patient therapies gain from scalable production enabling affordable treatments. Takara Bio’s CDMO segment achieved net sales exceeding ¥10 billion for the first time in FY2022.

Impact of Macroeconomic / Geopolitical Factors

Global economic surges infuse vitality into biotechnology research, elevating the competent cells market through amplified funding for genetic engineering projects in leading laboratories. Executives harness robust consumer confidence to deploy advanced cloning kits, which captures escalating demand from pharmaceutical R&D expansions worldwide.

However, unrelenting worldwide inflation propels utility and reagent prices upward, obliging suppliers to confront eroded earnings in fiercely contested arenas. Surging diplomatic clashes between the US and China fracture biotech supply lines, postponing deliveries of essential bacterial strains from Asian exporters. Visionary firms neutralize these frictions by restructuring alliances in geopolitically calm areas, which refines procurement reliability and ignites novel efficiency protocols.

Current US tariffs, frequently imposing 10-25% surcharges on imported biological reagents under Section 301 from key sources, augment overheads for international vendors navigating American distribution. Native biotech enterprises exploit this climate to fortify in-country labs, which propels skill-building initiatives and cements market dominance locally. Forward-looking evolutions in electrocompetent cell technologies invariably fortify the industry’s core, heralding amplified productivity and enduring prosperity on an international stage.

Latest Trends

Launch of new competent cell products for CRISPR is a recent trend

In 2024, the competent cells market has exhibited a prominent trend toward the launch of new competent cell products optimized for CRISPR applications, enhancing editing efficiency in cell biology research. Manufacturers are focusing on high-competency strains to support advanced gene editing techniques. Healthcare research integrates these cells for therapeutic development in genetic diseases.

Regulatory evaluations accommodate innovations that demonstrate improved transformation rates. Clinical trials are evaluating new cells in vector delivery for gene therapy. Academic studies are exploring cell adaptations for diverse host systems.

Global distribution expands access to specialized cells in biotech labs. Patient therapies benefit from precise editing enabled by these products. Ethical protocols ensure safety in CRISPR applications. Thermo Fisher Scientific highlighted advancements in cell biology tools in their 2024 annual report, with life sciences solutions contributing 21% of total revenue of $42.88 billion.

Regional Analysis

North America is leading the Competent Cells Market

In 2024, North America held a 38.3% share of the global competent cells market, driven by surging demands in genetic engineering and synthetic biology applications, where chemically and electroporation-competent strains enable efficient plasmid uptake for CRISPR-based gene editing in pharmaceutical R&D. Biotechnology firms expanded procurement of high-efficiency E. coli variants to accelerate protein production pipelines, supported by federal initiatives promoting cell therapy advancements amid talent shortages in traditional cloning methods.

Innovations in freeze-dried formats improved storage stability, aligning with regulatory focus on reproducibility in preclinical vaccine development. Rising investments in personalized medicine amplified usage for library construction in oncology research, prompting integrated workflows with automated transformation systems.

Academic labs refined host strains with reduced recombination for stable expression, facilitating broader integrations in microbiome studies. Collaborative consortia validated competency kits through proficiency testing, bridging gaps in emerging biotech hubs.

Supply adaptations ensured GMP-compliant cells for clinical-grade manufacturing, optimizing scalability in high-throughput facilities. In 2024 alone, NIH awarded approximately $37 billion in research funding, supporting over 408,000 researchers engaged in biotechnology projects that rely on competent cells for molecular manipulations.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Stakeholders forecast vigorous proliferation of competent cell technologies across Asia Pacific during the forecast period, as nations amplify indigenous R&D to tackle infectious disease modeling and agricultural biotech amid population pressures. Researchers harness electroporation strains for rapid vector insertion in antiviral drug screening, adapting protocols to humid lab conditions in tropical zones.

Governments channel funds into competency enhancement programs, equipping universities to support biosimilar cloning for affordable therapeutics. Biotech startups customize chemically treated hosts with improved transformation rates, tailoring them to regional plasmid diversities in plant genome editing.

Cross-national alliances evaluate strain performance through comparative studies, fostering efficiency for microbial fuel cell developments. Pharmaceutical entities localize production of freeze-thaw resistant variants, ensuring cost-effectiveness for rural innovation centers.

Policy incentives promote technician training on uptake optimization, extending capabilities to peripheral institutes facing equipment limitations. Since 2022, Chinese biotechs have developed 639 first-in-class drug candidates, up 360% from 137 candidates between 2018 and 2021.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the Competent Cells market drive growth by supplying high-efficiency transformation products that support faster cloning, protein expression, and synthetic biology workflows in research and biomanufacturing. Companies expand demand by continuously improving transformation efficiency, strain stability, and consistency to meet the needs of advanced genetic engineering applications.

Commercial strategies focus on bundling competent cells with plasmids, reagents, and technical support to simplify purchasing and lock in repeat laboratory usage. Innovation priorities include chemically and electrocompetent variants optimized for large constructs and difficult-to-clone sequences.

Market expansion targets rapidly growing biotech hubs and academic research centers with rising molecular biology activity. Thermo Fisher Scientific represents a leading participant through its broad molecular biology portfolio, global distribution scale, and strong technical expertise that enables reliable supply of high-performance competent cell solutions worldwide.

Top Key Players

- New England Biolabs

- Thermo Fisher Scientific

- Merck KGaA

- Promega Corporation

- Agilent Technologies

- Takara Bio Inc.

- Bio-Rad Laboratories

- Lonza Group

- Sigma-Aldrich

- Invitrogen (part of Thermo Fisher Scientific)

Recent Developments

- In February 2024, researchers in the US reported the development of a naturally competent Vibrio natriegens system that allows plasmids to be taken up efficiently without complex preparation steps. This breakthrough reduces transformation time and cost, speeding up synthetic biology workflows and increasing dependence on reliable, high performance competent cells for rapid cloning, strain optimization, and scalable gene expression.

- In February 2024, Bio-Rad introduced Vericheck ddPCR assay kits in the US for detecting replication competent lentivirus and AAV, strengthening quality control processes in viral vector manufacturing. As cell and gene therapy programs continue to scale, upstream activities such as plasmid assembly and vector construction intensify, directly boosting the need for highly efficient competent cells to support increased cloning and packaging workloads.

Report Scope

Report Features Description Market Value (2024) US$ 2.1 Billion Forecast Revenue (2034) US$ 5.5 Billion CAGR (2025-2034) 10.1% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product Type (Chemically Competent Cells, Ultracompetent Cells and Electrocompetent Cells), By Application (Cloning, Mutagenesis, Protein Expression and Others), By End-User (Pharmaceutical & Biotechnology Companies, Academic & Research Institutes and Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape New England Biolabs, Thermo Fisher Scientific, Merck KGaA, Promega Corporation, Agilent Technologies, Takara Bio Inc., Bio-Rad Laboratories, Lonza Group, Sigma-Aldrich, Invitrogen (Thermo Fisher Scientific) Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- New England Biolabs

- Thermo Fisher Scientific

- Merck KGaA

- Promega Corporation

- Agilent Technologies

- Takara Bio Inc.

- Bio-Rad Laboratories

- Lonza Group

- Sigma-Aldrich

- Invitrogen (part of Thermo Fisher Scientific)

Our Clients

- 174169

- Jan 2026