Quick Navigation

Report Overview

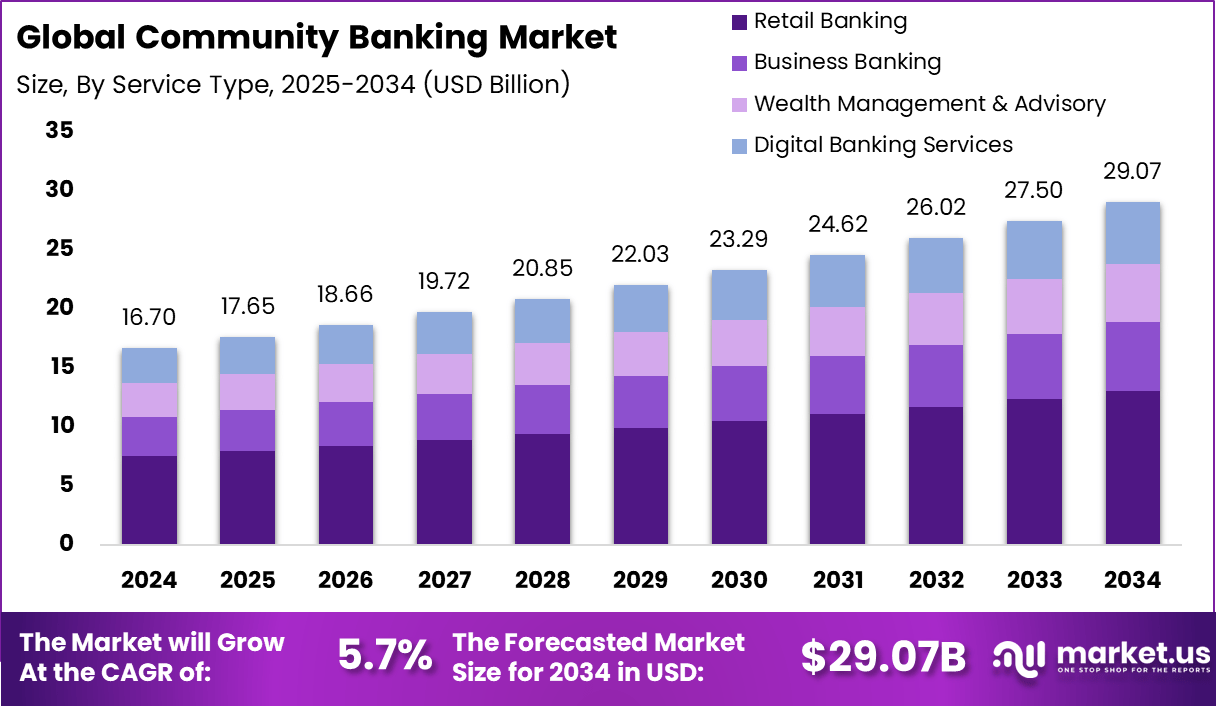

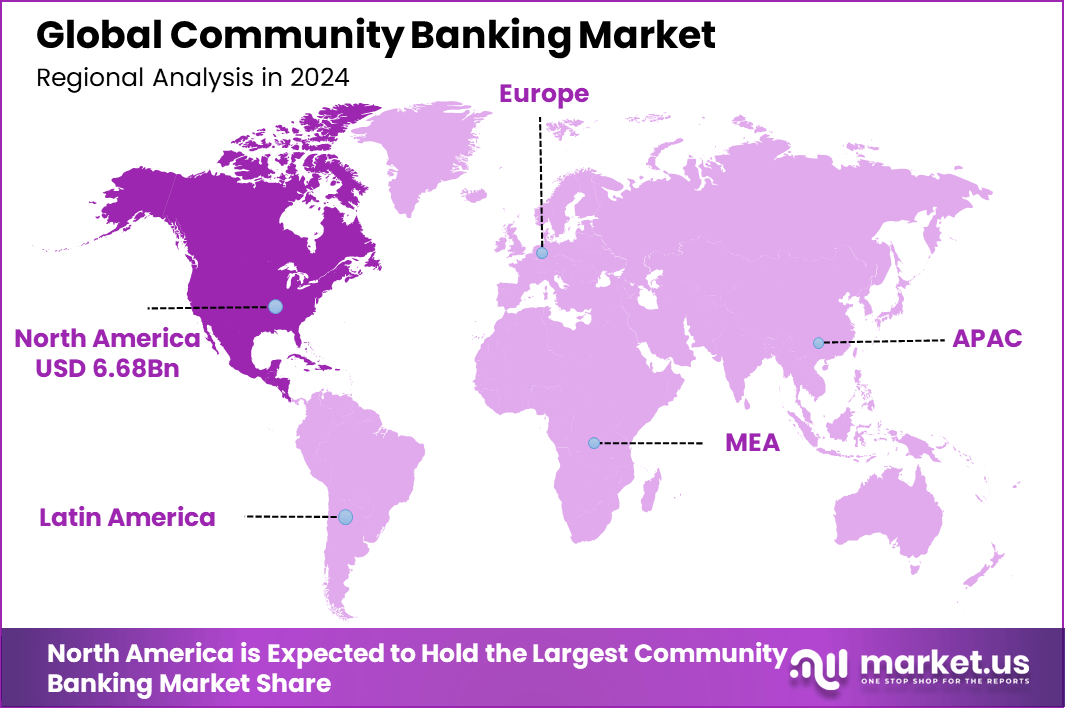

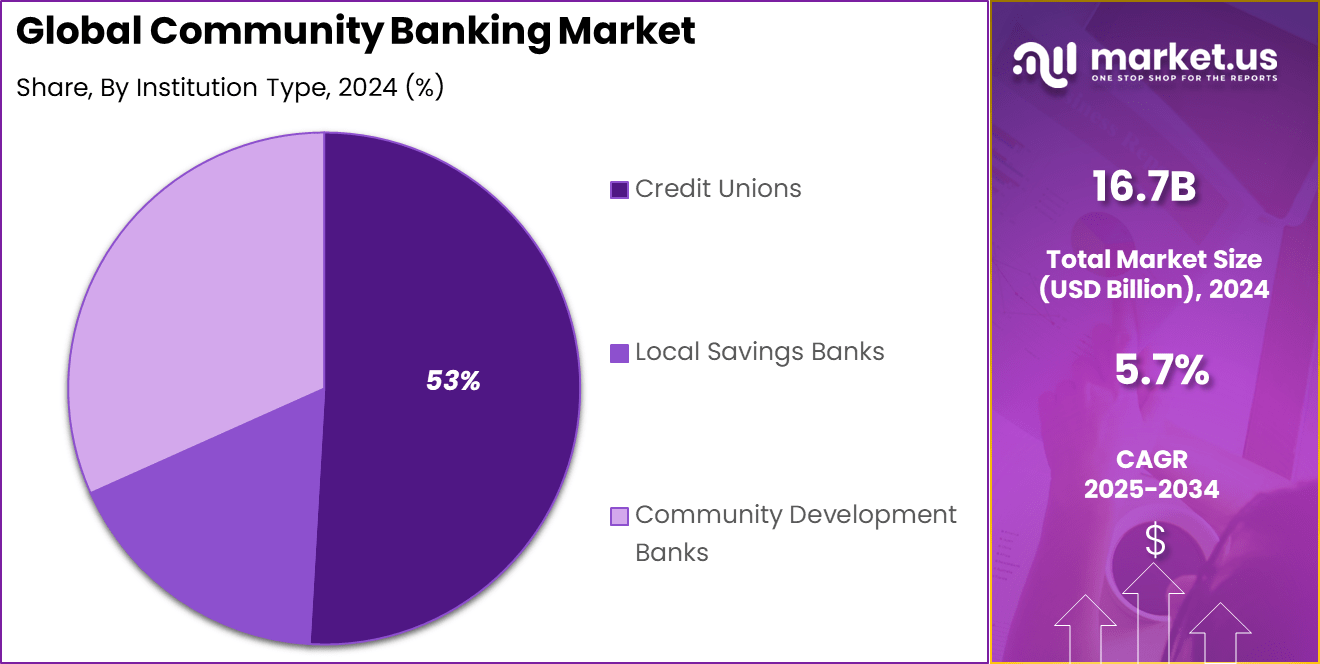

The Global Community Banking Market size is expected to be worth around USD 29.07 billion by 2034, from USD 16.7 billion in 2024, growing at a CAGR of 5.7% during the forecast period from 2025 to 2034. In 2024, North America held a dominant market position, capturing more than a 40% share, holding USD 6.68 Billion in revenue.

Community banking refers to the operations of locally owned and operated financial institutions that primarily serve the needs of individuals, small businesses, and farmers within a specific geographic area. These banks are characterized by their relationship-based approach, emphasizing personalized customer service and a deep understanding of the local community’s economic dynamics.

The community banking market has been experiencing steady growth, driven by increasing demand for personalized financial services and the need for accessible banking solutions in underserved areas. Several factors are propelling the growth of community banks. The demand for personalized and convenient banking services is on the rise, prompting community banks to leverage their local knowledge and customer relationships.

According to CSI’s Banking Priorities Executive Report, 28% of community financial professionals identified cybersecurity and data privacy as their top concern, ranking it higher than any other issue. This reflects growing anxiety over rising cyber threats, regulatory pressures, and the need to protect sensitive customer data in an increasingly digital financial landscape.

For instance, In April 2025, the Independent Community Bankers of America (ICBA) celebrated Community Banking Month by highlighting the vital role community banks play in strengthening local economies. Rebeca Romero Rainey, the incoming president and CEO of ICBA, stated that community banks are essential for small businesses and help build trust and long-term growth in local communities across the country.

Nationally, these banks are responsible for providing over 60% of small-business loans and over 80% of the banking industry’s agricultural loans. In addition, community banks serve as active civic leaders and contribute to local causes through programs like ICBA’s National Community Bank Service Awards, making them the sole physical banking institution in one-third of U.S. counties.

The demand for community banking services is increasing, particularly among small businesses and individuals seeking tailored financial solutions. Community banks are well-positioned to meet this demand due to their flexibility and deep understanding of local markets. Their ability to offer customized products and services fosters strong customer loyalty and trust.

Community banks are increasingly adopting advanced technologies to streamline operations and enhance customer experiences. The integration of digital platforms, mobile banking apps, and online services allows these banks to offer convenient and efficient services. Moreover, partnerships with fintech companies are enabling community banks to access innovative solutions and stay competitive in the digital age.

Key Takeaways

- In 2024, the retail banking segment held a commanding 45% share of the global community banking market, driven by increased customer preference for personalized, relationship-based financial services.

- The credit unions segment led the market with a 53% share in 2024, supported by their cooperative structure, local trust, and competitive lending rates for small businesses and individual customers.

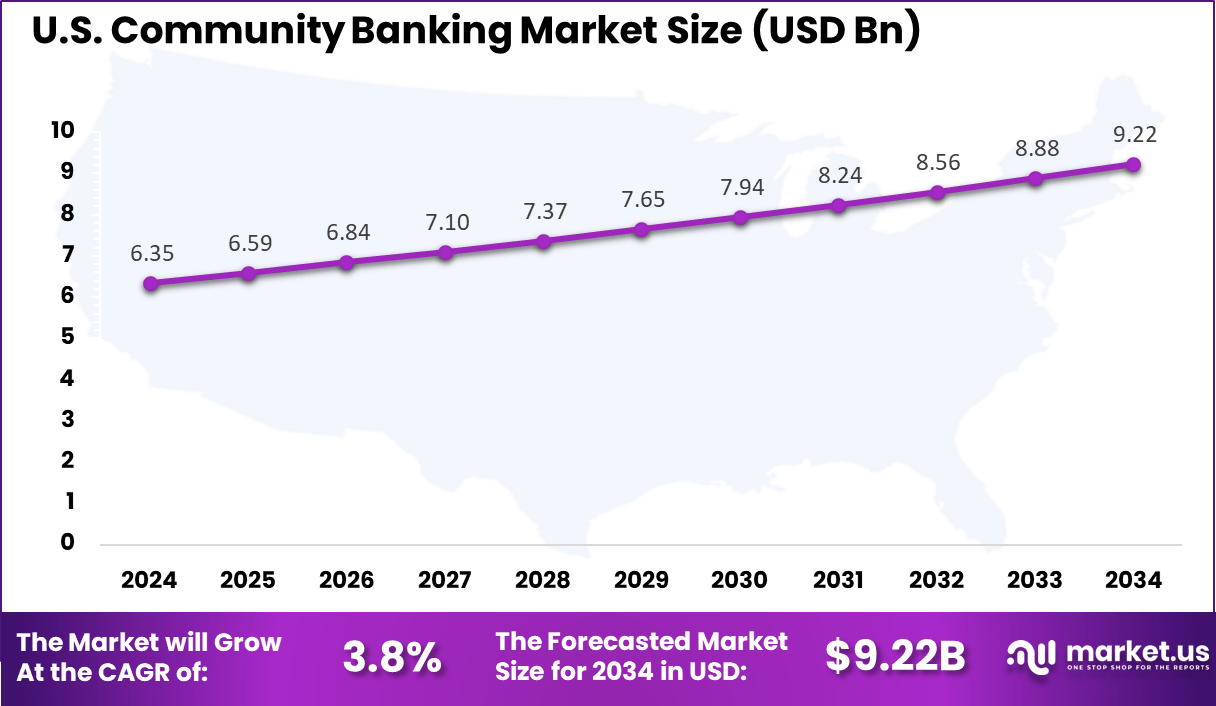

- The U.S. community banking market reached a valuation of USD 6.35 billion in 2024, showing stable growth with a projected CAGR of 3.8%, reflecting sustained demand for localized banking models and regulatory support.

- North America remained the market leader in 2024, securing over 40% of the global share, supported by a mature banking infrastructure, strong community bank presence, and emphasis on financial inclusion in regional economies.

Role of AI

Artificial Intelligence (AI) is increasingly becoming a cornerstone in the evolution of community banking, offering tools that enhance efficiency, customer service, and risk management. While larger financial institutions have been at the forefront of AI adoption, community banks are now recognizing its potential to level the playing field.

A significant number of community banks are exploring AI applications. According to a recent survey, approximately 43% of community bankers have identified AI and automation as key areas for technological investment in 2025. This shift is driven by the need to improve operational efficiency and meet evolving customer expectations.

AI’s role in community banking extends to various functions. For instance, AI-powered chatbots can provide 24/7 customer support, addressing routine inquiries and freeing up human staff for more complex tasks . Additionally, AI algorithms can analyze transaction data to detect fraudulent activities, enhancing security measures.

Risk management is another area where AI proves beneficial. By analyzing historical data and market trends, AI can assist community banks in making informed lending decisions and managing overall risk exposure . This capability is particularly valuable for smaller banks that may lack extensive analytical resources.

US Market Expansion

The market for Community Banking Market within the U.S. is growing tremendously and is currently valued at USD 6.35 billion and growing at a CAGR of 3.8%. The U.S. community banking sector is experiencing significant growth, driven by several key factors.

Firstly, community banks are increasingly leveraging digital platforms to enhance customer engagement and streamline operations, aligning with the broader trend of digital transformation in the financial industry. Additionally, these institutions are concentrating on customized financial products and services that address the specific needs of local communities.

Moreover, supportive regulatory changes and a favorable interest rate environment have also helped the financial health of community banks as they can expand their lending activities and invest in technological developments. The sector is being consolidated through strategic mergers and acquisitions, leading to economies of scale and better service delivery.

For instance, In March 2025, the Independent Community Bankers of America (ICBA) and Mastercard announced a strategic partnership aimed at enhancing the card and payment services of 1,400 community banks. This partnership aims to bring about transformation in card programs by introducing new features like contactless cards, digital wallet tokenization, and eight-digit Bank Identification Numbers (BINs).

North America Growth

In 2024, North America held a dominant market position in the global Community Banking Market, capturing more than a 40% share. The region’s robust financial infrastructure, coupled with a strong emphasis on digital transformation, has enabled community banks to offer personalized services that cater to local needs.

Technological advancements have facilitated enhanced customer experiences, streamlined operations, and improved financial inclusion. Favorable economic conditions and supportive regulatory systems have encouraged the growth of community banks, which in turn enabled them to compete with larger financial institutions. Together, these elements make North America a leader in community banking.

For instance, In June 2023, New York Community Bank (NYCB) partnered with fintech startup MoCaFi to enhance financial inclusion for underserved communities. This collaboration enables NYCB to offer digital banking services, including mobile banking and financial literacy tools, to individuals without access to traditional banking. By leveraging MoCaFi’s technology, NYCB aims to bridge the gap in financial services and provide equitable access to banking for all.

Service Type Analysis

In 2024, the Retail Banking segment held a dominant market position, capturing more than 45% of the community banking market share. This leadership is attributed to its foundational role in providing essential financial services such as savings and checking accounts, personal loans, and mortgages to individuals and households.

The segment’s strength is further bolstered by the widespread adoption of digital banking platforms, which have made banking services more accessible and convenient for customers. The prominence of retail banking is also supported by its adaptability to changing consumer behaviors and technological advancements.

The integration of mobile and online banking services has not only enhanced customer experience but also expanded the reach of community banks to serve a broader demographic. Furthermore, the emphasis on personalized financial solutions and community engagement has strengthened customer loyalty and trust, reinforcing the segment’s leading position in the market.

For instance, In July 2024, First Abu Dhabi Bank (FAB) and Al Maryah Community Bank (Mbank) formed a strategic partnership to enhance banking accessibility across the UAE. The collaboration links Mbank’s digital services with FAB 396, FAB’s extensive e-commerce network, and enables customers to use FAB’s ATMs and Cash Deposit Machines (CDMs) via the FABePay portal.

Institution Type Analysis

In 2024, the Credit Unions segment held a dominant market position within the community banking sector, capturing more than 53% of the market share. This leadership is attributed to their member-owned, not-for-profit structure, which allows them to offer competitive rates and personalized services.

Credit unions have increasingly become the preferred choice for consumers seeking community-focused financial institutions that prioritize member benefits over shareholder profits. Their ability to provide lower loan rates and higher savings yields has resonated with a broad demographic, leading to substantial growth in membership and assets.

The expansion of credit unions is further evidenced by their strategic acquisitions of community banks. In 2024, credit unions acquired more banks than in any previous year, surpassing the 11 deals announced in 2023. This trend underscores their commitment to extending services and reaching underserved communities.

For instance, In April 2025, credit unions are increasingly focusing on digital innovation to enhance member engagement and meet the evolving expectations of their members. According to a recent report, 55% of credit unions plan to innovate and enhance self-service solutions such as mobile banking and digital onboarding within the next three years.

Key Market Segments

By Service Type

- Retail Banking

- Business Banking

- Wealth Management & Advisory

- Digital Banking Services

By Institution Type

- Credit Unions

- Local Savings Banks

- Community Development Banks

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver

Digital Transformation Enhancing Customer Engagement

Community banks are increasingly embracing digital transformation to meet evolving customer expectations and remain competitive. The integration of digital technologies has enabled these banks to offer seamless online and mobile banking experiences, personalized financial services, and efficient customer support.

This shift not only enhances customer satisfaction but also expands the banks’ reach to tech-savvy consumers who prefer digital interactions over traditional banking methods. The adoption of digital tools has become a strategic imperative for community banks aiming to attract and retain customers in a rapidly digitizing financial landscape.

Restraint

Regulatory Compliance Burden

Community banks face significant challenges in navigating complex regulatory requirements, which can strain their limited resources. Compliance with regulations such as the Bank Secrecy Act (BSA), Anti-Money Laundering (AML) laws, and Know Your Customer (KYC) protocols demands substantial investments in compliance infrastructure, staff training, and ongoing monitoring systems.

These obligations can divert attention and resources away from core banking activities, hindering the banks’ ability to innovate and compete effectively. The financial burden of regulatory compliance is particularly pronounced for smaller community banks, which may lack the economies of scale to absorb these costs efficiently.

Opportunity

Serving Underserved and Rural Communities

Community banks have a unique opportunity to expand their services to underserved and rural communities that are often overlooked by larger financial institutions. By leveraging their local knowledge and personalized approach, community banks can address the specific financial needs of these populations, such as providing accessible credit, tailored financial products, and financial education.

This focus not only fulfills a critical social need but also opens new markets for growth and customer acquisition. The withdrawal of larger banks from less profitable regions has created a service gap that community banks are well-positioned to fill.

Initiatives like the establishment of micro-branches and the deployment of digital banking solutions can enhance accessibility and convenience for customers in remote areas. By capitalizing on this opportunity, community banks can strengthen their community ties, foster economic development, and secure a loyal customer base in these underserved markets.

Challenge

Cybersecurity Threats Amid Digital Adoption

As community banks adopt digital technologies to enhance their services, they face increasing cybersecurity threats that pose significant risks to their operations and customer trust. Cyberattacks, data breaches, and fraud attempts have become more sophisticated, targeting vulnerabilities in digital banking platforms and third-party service providers.

Community banks, often with limited cybersecurity budgets and expertise, may struggle to implement robust security measures to protect sensitive customer information and maintain regulatory compliance. The financial and reputational damage resulting from cybersecurity incidents can be substantial.

Collaborating with cybersecurity experts and leveraging shared resources can also enhance their resilience against cyber threats. Proactively managing cybersecurity risks is essential for community banks to safeguard their operations and uphold customer confidence in the digital age.

Emerging Trends

Community banks are actively embracing digital transformation to enhance customer experience and operational efficiency. The adoption of technologies such as mobile banking, artificial intelligence, and open banking platforms is becoming increasingly prevalent. These innovations enable community banks to offer personalized services and streamline processes, ensuring they remain competitive in a rapidly evolving financial landscape.

Additionally, partnerships with fintech companies are facilitating the integration of advanced solutions, allowing community banks to expand their service offerings and reach a broader customer base. This strategic shift towards digitalization is essential for meeting the changing expectations of consumers and maintaining relevance in the industry .

Another significant trend is the focus on financial inclusion and community engagement. Community banks are leveraging their local knowledge and relationships to support underserved populations and small businesses. By providing accessible financial services and fostering economic development, these institutions play a crucial role in strengthening local economies.

Business Benefits

Community banks offer several advantages to businesses, particularly small and medium-sized enterprises (SMEs). One of the primary benefits is the personalized service and relationship-based approach. Community banks often have a deep understanding of the local market and can provide tailored financial solutions that align with the specific needs of businesses.

Additionally, community banks contribute significantly to local economic development. By investing in local businesses and supporting community initiatives, they help stimulate economic growth and job creation. Their commitment to reinvesting in the community fosters a sustainable economic environment, benefiting both businesses and residents.

Moreover, community banks’ emphasis on customer service and community involvement enhances their reputation and trust within the community, making them a preferred choice for businesses seeking a banking partner that understands and supports their goals.

Key Player Analysis

Community banking refers to financial institutions that primarily serve local communities by offering traditional banking services, including loans, deposits, and savings. These banks typically operate on a smaller scale than large national banks and focus on relationship-based banking, especially supporting small businesses, individuals, and local development projects.

U.S. Bancorp has remained a leading force in the community banking domain through its proactive acquisition strategy. Its $8 billion acquisition of MUFG Union Bank significantly expanded its customer base on the U.S. West Coast. In 2024, it further diversified into healthcare payments with the purchase of Salucro Healthcare Solutions

First Republic Bank, known for its high-touch customer service, underwent a pivotal change following financial instability. In May 2023, JPMorgan Chase acquired First Republic’s assets, including $173 billion in loans. While the acquisition marked the end of First Republic’s independent operations, it was a critical move to stabilize client services and retain trust in the broader banking system.

Top Key Players Covered

- S. Bancorp

- First Republic Bank

- New York Community Bancorp

- SVB Financial Group

- Comerica Bank

- Crédit Mutuel

- Rabobank

- Nationwide Building Society

- HDFC Bank

- Others

Recent Developments

- In May 2025, Comerica Bank announced a $250,000 initiative to assist in the development of small businesses by awarding grants to five nonprofit organizations during National Small Business Week. A sum of $50,000 was allotted to each group for the purpose of supporting entrepreneurial education and empowerment.

- In September 2024, HDFC Bank unveiled a bold target under its CSR initiative Parivartan, aiming to improve the income of 500,000 marginal farmers earning below ₹60,000 annually by 2025. To achieve this, the bank plans to deliver skill development support to nearly 200,000 individuals, assist 20,000 community-based organizations, and promote 25,000 community-led enterprises.

- In February 2024, Fidelity National Information Services (FIS) introduced its new digital banking platform, FIS Modern Banking, tailored for community banks. This solution is designed to equip smaller financial institutions with advanced digital tools, enabling them to better compete with larger banks.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 6.8 Bn |

| Forecast Revenue (2034) | USD 179 Bn |

| CAGR (2025-2034) | 23.6% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Component (Sensors and Detectors, Command and Control (C2) Systems, Communication Infrastructure, Trigger Mechanisms, Weapon Platforms, Others), By Platform (Land-Based, Naval-Based, Air-Based), By End-User (National Strategic Forces, Defense Ministries & Intelligence Agencies, Defense Contractors & System Integrators) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | IBM Corporation, Microsoft Corporation, Google LLC, Amazon Web Services, Intel Corporation, Nvidia Corporation, AT&T, China Mobile, Deutsche Telekom, Telefónica, SK Telecom, Verizon, Vodafone, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |