Global Coated Paper Packaging Box Market Size, Share, Growth Analysis By Box Type (Hinged lid Box, Telescopic Box, Shoulder Neck Box, Collapsible Box, Others), By Coating Type (Single-Sided Coating, Double-Sided Coating), By End Use (Fashion Accessories and Apparel, Food and Beverage, Cosmetic and Personal Care, Consumer Electronics, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2025-2034

- Published date: Aug 2025

- Report ID: 156349

- Number of Pages: 311

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

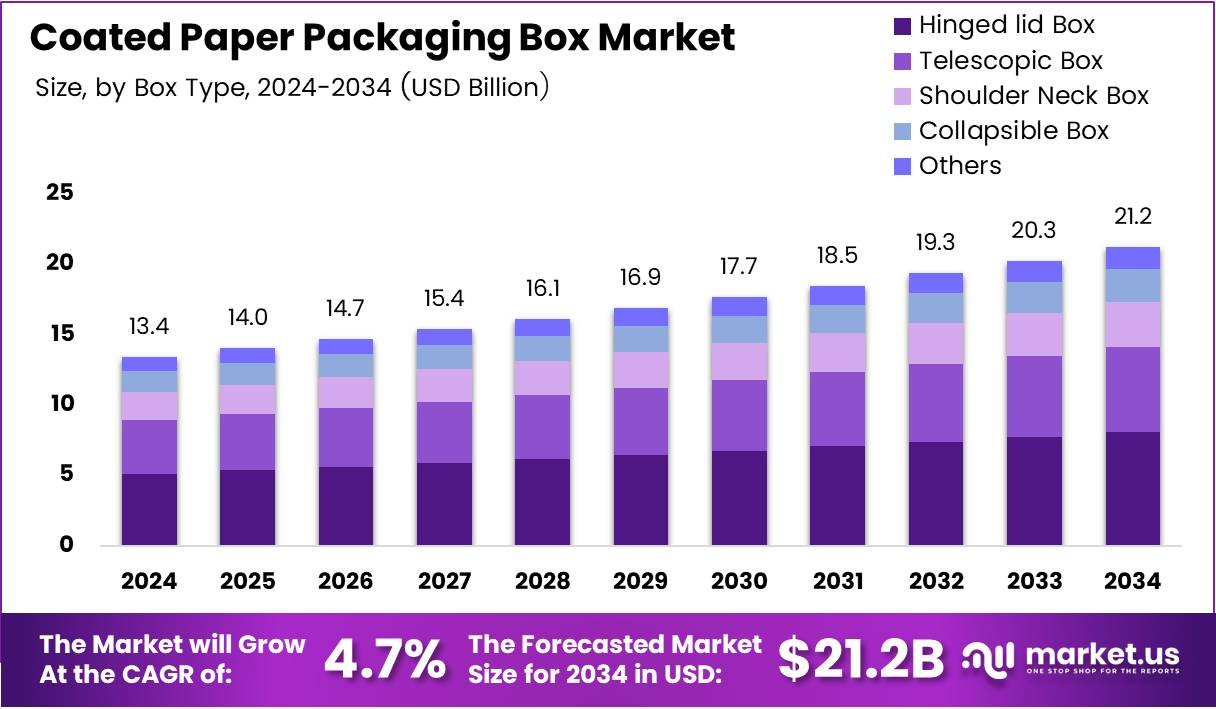

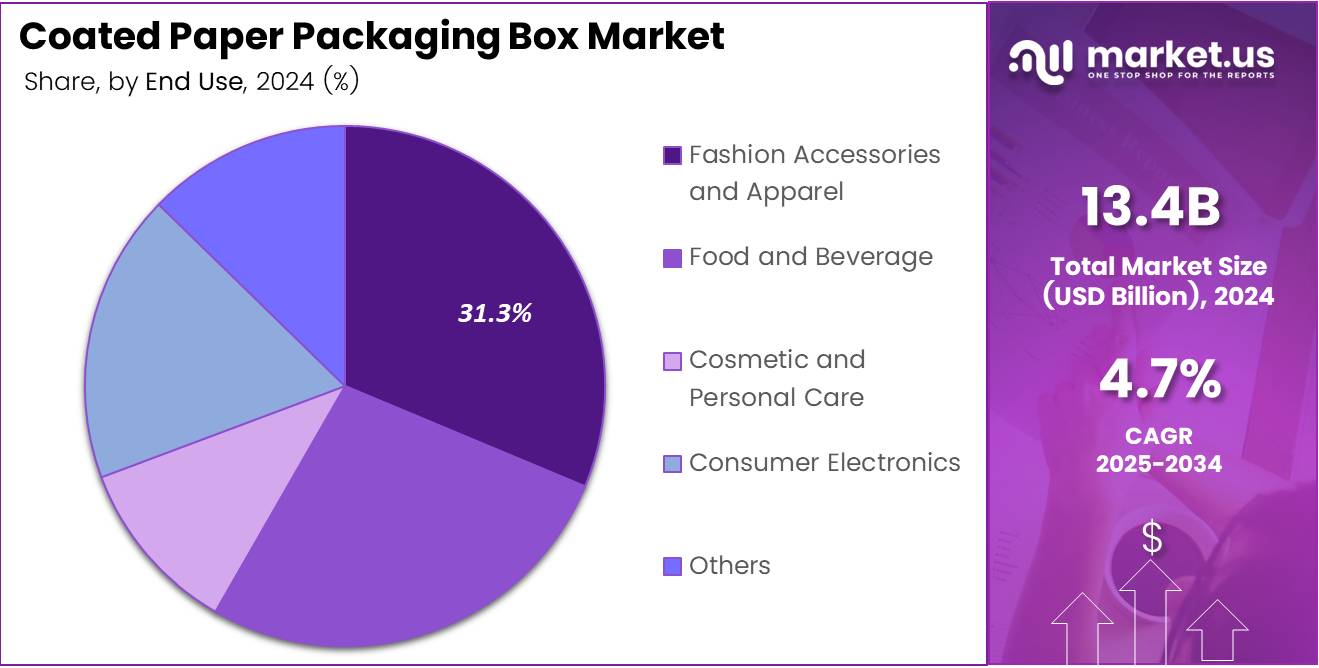

The Global Coated Paper Packaging Box Market size is expected to be worth around USD 21.2 Billion by 2034, from USD 13.4 Billion in 2024, growing at a CAGR of 4.7% during the forecast period from 2025 to 2034.

The Coated Paper Packaging Box Market refers to the segment of packaging that uses coated paper to enhance durability, printability, and overall product appeal. These boxes are widely adopted in industries such as food, beverages, cosmetics, and retail due to their eco-friendly profile and premium finish. Their versatility supports branding and consumer engagement.

Driven by rising demand for sustainable packaging, the market is gaining momentum across multiple sectors. Manufacturers are focusing on recyclable and biodegradable coated paper solutions to reduce environmental footprint. At the same time, innovations in coatings for moisture resistance and strength are making these boxes more reliable for diverse applications in logistics and retail.

Growth opportunities remain significant as global trade and e-commerce expand. Companies in the sector are adopting lightweight, durable, and cost-efficient coated paper packaging boxes to reduce shipping costs while maintaining product safety. The growing preference for renewable materials further accelerates demand, with retailers increasingly shifting from plastic-based options toward paper-based alternatives.

Governments are also supporting sustainable packaging through strict regulations against single-use plastics and policies promoting recycling. Such interventions are pushing manufacturers to scale coated paper packaging production. Additionally, investments in recycling infrastructure and incentives for paper-based packaging materials are boosting market competitiveness and innovation across developed and emerging economies.

According to the U.S. Environmental Protection Agency (EPA), in 2024, around 46 million tons of paper were recycled, with recycling rates of 60–64% for paper and 69–74% for cardboard. This highlights strong regulatory and consumer support for paper-based packaging. Moreover, a consumer survey revealed that 67% of buyers find paper packaging boxes more attractive than alternatives, reflecting a clear shift in purchasing behavior.

Key Takeaways

- The Global Coated Paper Packaging Box Market is projected to reach USD 21.2 Billion by 2034 from USD 13.4 Billion in 2024, expanding at a CAGR of 4.7%.

- In 2024, Hinged lid Box dominated the Box Type segment with a 38.2% share, supported by luxury and premium product packaging demand.

- In 2024, Single-Sided Coating led the Coating Type segment with a 69.4% share, balancing cost efficiency with protection and printability.

- In 2024, Fashion Accessories and Apparel held the top position in End Use with a 31.3% share, highlighting strong adoption by luxury brands.

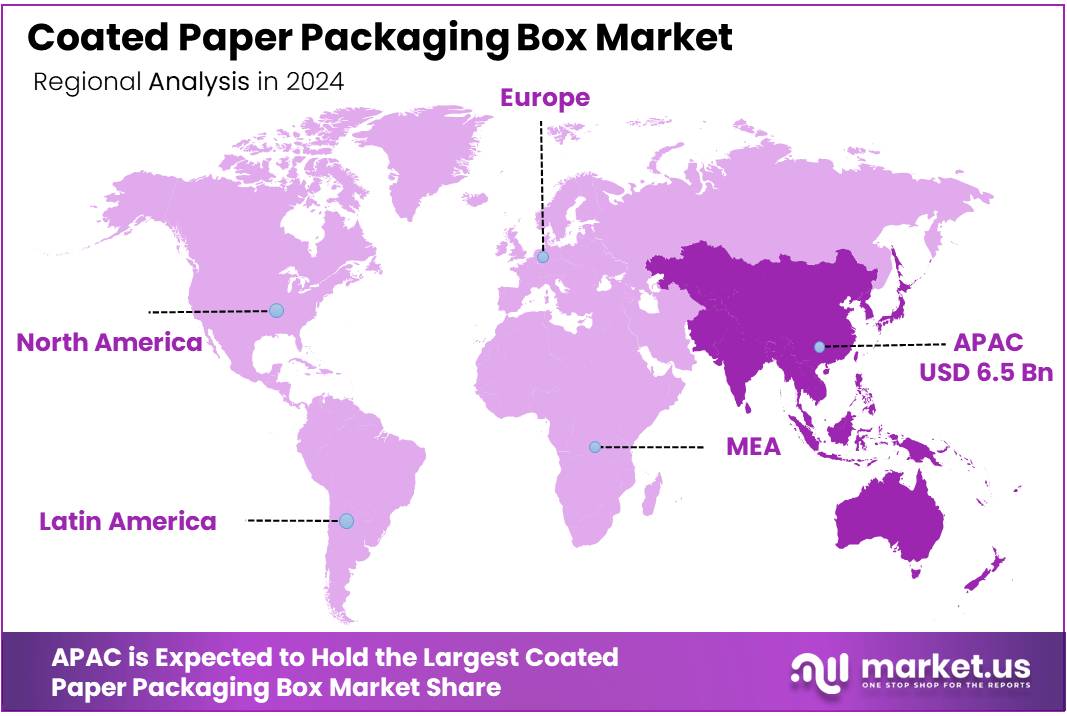

- Asia Pacific emerged as the leading region with a 48.9% share, generating USD 6.5 Billion in 2024, driven by e-commerce growth and sustainability trends.

Box Type Analysis

Hinged lid Box dominates with 38.2% owing to its durability and premium appeal in packaging solutions.

In 2024, Hinged lid Box held a dominant market position in By Box Type Analysis segment of Coated Paper Packaging Box Market, with a 38.2% share. Its popularity is largely driven by luxury and premium product packaging, where rigid structure and convenience play a critical role in consumer appeal.

Telescopic Box followed as a preferred option for items requiring protective strength and stacking efficiency. These boxes are particularly adopted by e-commerce and industrial suppliers that focus on cost efficiency without compromising quality.

Shoulder Neck Box continued to gain traction as a luxury packaging choice in cosmetic and personal care applications. The rigid design combined with elegant finishing makes it highly suitable for premium branding in retail stores.

Collapsible Box is increasingly being used in the fashion and apparel industry due to its space-saving benefits. Lightweight yet durable, collapsible formats support sustainable packaging trends by optimizing storage and reducing transportation costs.

Others in the segment include specialized designs tailored for niche industries such as jewelry, electronics, and personalized gifting. These custom variations, though smaller in market size, contribute to diversification in coated paper packaging applications.

Coating Type Analysis

Single-Sided Coating dominates with 69.4% due to its cost-effectiveness and efficiency in mass packaging production.

In 2024, Single-Sided Coating held a dominant market position in By Coating Type Analysis segment of Coated Paper Packaging Box Market, with a 69.4% share. It remains the most widely used option, offering protection and printability while keeping costs manageable for manufacturers and retailers.

Double-Sided Coating, though comparatively less dominant, is expanding in demand across food and beverage and high-end consumer goods packaging. This type provides added resistance to moisture, grease, and external damage, making it ideal for sectors where product safety and aesthetics are crucial.

While Single-Sided Coating continues to lead due to affordability and ease of mass adoption, Double-Sided Coating represents an evolving niche where sustainability, durability, and premium visual appeal align with consumer expectations. This dual presence ensures that coated paper packaging maintains relevance across both price-sensitive and premium markets.

End Use Analysis

Fashion Accessories and Apparel dominate with 31.3% as premium brands prioritize aesthetics and brand-enhancing packaging.

In 2024, Fashion Accessories and Apparel held a dominant market position in By End Use Analysis segment of Coated Paper Packaging Box Market, with a 31.3% share. High adoption by luxury apparel and footwear brands underlines the demand for premium presentation in retail environments.

Food and Beverage is another key segment, where coated boxes serve as an effective medium for branding and product safety. The segment leverages moisture-resistant coated paper packaging to maintain freshness and enhance shelf presence.

Cosmetic and Personal Care relies heavily on coated packaging for its ability to deliver superior printing, texture, and premium look. The rising demand for high-end skincare and beauty products continues to drive growth in this category.

Consumer Electronics utilize coated paper boxes for protective and aesthetic purposes. With increasing sales of gadgets and accessories, packaging has become integral for both safety and consumer experience.

Others in the category include gifting, stationery, and niche retail products. Though smaller in size, these segments collectively add diversity to coated paper packaging applications, particularly in seasonal and promotional markets.

Key Market Segments

By Box Type

- Hinged lid Box

- Telescopic Box

- Shoulder Neck Box

- Collapsible Box

- Others

By Coating Type

- Single-Sided Coating

- Double-Sided Coating

By End Use

- Fashion Accessories and Apparel

- Food and Beverage

- Cosmetic and Personal Care

- Consumer Electronics

- Others

Drivers

Rising Demand for Premium Aesthetic Appeal in Consumer Goods Packaging Drives Market Growth

The rising demand for premium and visually appealing packaging in consumer goods is a major driver for the coated paper packaging box market. Brands are increasingly investing in coated paper boxes to create an elegant appearance that enhances shelf visibility and strengthens customer perception. This shift is pushing consistent adoption across multiple industries.

The rapid growth of e-commerce has intensified the need for packaging that is not only durable but also attractive to consumers. Coated paper boxes are gaining traction as they combine strength with high-quality finishes, meeting both functional and visual requirements in online deliveries. This trend is fueling significant market momentum.

Food safety concerns have also created opportunities for coated paper packaging. With rising adoption of food-grade coatings, manufacturers are addressing consumer demand for hygienic and eco-friendly packaging solutions. This approach is particularly important in fresh food, bakery, and ready-to-eat product segments, strengthening trust and compliance with safety regulations.

Luxury retail and personal care sectors are also boosting the demand for coated paper packaging boxes. Customized designs, embossing, and premium finishes are increasingly used to deliver an exclusive unboxing experience. The expansion of these industries continues to provide a strong growth path for coated paper packaging, as companies align packaging with brand identity.

Restraints

Volatility in Raw Material Prices Impacting Coated Paper Production Costs

One of the key restraints for the coated paper packaging box market is the volatility in raw material prices. Fluctuations in the cost of paper pulp and coatings make it difficult for manufacturers to maintain stable pricing, creating pressure on margins and profitability.

Another challenge is the limited recycling infrastructure available for coated paper packaging. While coated paper is recyclable in theory, many regions lack proper facilities to separate coatings from paper fibers, leading to waste management issues. This limitation affects sustainability goals and slows down large-scale adoption.

Competition from alternative packaging formats also adds to the restraints. Plastic and flexible packaging solutions often come at lower costs and offer longer shelf life, making them attractive to price-sensitive industries. This substitution risk limits the expansion potential of coated paper packaging in certain markets.

Collectively, these restraints highlight the importance of innovation and policy support to ensure long-term market stability. Overcoming raw material fluctuations, improving recycling systems, and competing with cost-effective alternatives remain crucial challenges for the coated paper packaging box market.

Growth Factors

Advancements in Bio-based Coatings for Sustainable Packaging Solutions Drive Growth Opportunities

One of the biggest opportunities for the coated paper packaging market lies in bio-based coatings. Advancements in plant-derived and biodegradable coatings are reducing reliance on synthetic chemicals, allowing manufacturers to meet eco-friendly standards and appeal to sustainability-conscious consumers.

Smart packaging integration is another opportunity. Coated paper boxes with QR codes, NFC tags, and augmented reality features are gaining attention as brands look to enhance consumer engagement. This technological edge allows companies to merge traditional packaging with digital interaction, adding more value to end-users.

Emerging markets present significant potential due to the rapid expansion of organized retail. Countries in Asia, Africa, and Latin America are witnessing strong growth in retail infrastructure, boosting demand for premium and customized packaging. Coated paper boxes are positioned well to serve this growing consumer base.

Additionally, the development of lightweight yet high-strength coated papers offers cost efficiency for manufacturers. By reducing material usage without compromising durability, companies can improve margins while supporting sustainability goals. This innovation is expected to play a vital role in expanding market opportunities.

Emerging Trends

Shift Toward Water-Based Coatings for Eco-friendly Packaging Solutions Drives Market Trends

The coated paper packaging market is witnessing a clear shift toward water-based coatings as businesses prioritize sustainability. These coatings reduce harmful chemical emissions and align with global regulations, making them a preferred choice for both manufacturers and end-users.

Minimalist and customizable packaging designs are trending strongly. Consumers are increasingly attracted to simple yet elegant designs that focus on brand identity without excess material use. Coated paper boxes offer flexibility in finishes, embossing, and printing, supporting this growing preference.

Digital printing technologies are transforming coated paper packaging with high-resolution graphics and faster turnaround times. The ability to print short-run, personalized packaging is becoming a key advantage, especially for e-commerce brands and promotional campaigns.

Collaboration between packaging manufacturers and brand owners is also shaping trends. Joint efforts are being made to design innovative, eco-friendly, and cost-effective solutions that balance functionality with aesthetics. These partnerships are accelerating the adoption of coated paper boxes in global markets.

Regional Analysis

Asia Pacific Dominates the Coated Paper Packaging Box Market with a Market Share of 48.9%, Valued at USD 6.5 Billion

Asia Pacific held the dominant position in the coated paper packaging box market with 48.9% share, generating USD 6.5 Billion in 2024. Strong manufacturing hubs, rapid e-commerce expansion, and increasing preference for recyclable packaging in China, India, and Southeast Asia are fueling demand. Rising consumer awareness toward sustainable solutions further strengthens its leadership position.

North America Coated Paper Packaging Box Market Trends

North America represents a mature yet steadily growing market, driven by high consumer awareness of eco-friendly packaging and strict sustainability regulations. The United States leads in adopting coated paper packaging for food, beverages, and premium consumer goods, reflecting a strong shift toward recyclable materials in packaging strategies.

Europe Coated Paper Packaging Box Market Trends

Europe continues to show consistent growth, supported by government-led recycling initiatives and a circular economy approach. Demand is particularly strong in countries such as Germany, France, and the UK, where luxury retail and personal care industries rely heavily on aesthetically appealing coated paper packaging for product differentiation.

Middle East and Africa Coated Paper Packaging Box Market Trends

The Middle East and Africa are emerging markets where demand is rising in urban centers due to growth in retail chains, food service, and cosmetics. Although the market is smaller compared to developed regions, investments in sustainable packaging solutions are gradually increasing, driven by regulatory pressures and consumer awareness.

Latin America Coated Paper Packaging Box Market Trends

Latin America is witnessing gradual adoption of coated paper packaging, led by Brazil and Mexico. The growth is supported by rising disposable incomes and the expansion of e-commerce platforms. However, the market is still developing, with opportunities largely tied to the replacement of plastic-based packaging solutions in consumer goods.

U.S. Coated Paper Packaging Box Market Trends

The U.S. stands out as a significant contributor within North America, driven by high retail consumption and strong e-commerce logistics networks. Increasing demand from food packaging and luxury retail industries has reinforced the adoption of coated paper boxes, supported by recycling infrastructure and consumer preference for sustainable materials.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Coated Paper Packaging Box Company Insights

In 2024, the global Coated Paper Packaging Box Market was shaped significantly by the strategic initiatives and operational strengths of leading players. WestRock Company maintained a strong presence with its emphasis on sustainable coated paper packaging solutions that align with rising consumer demand for eco-friendly alternatives. Its ability to integrate innovation with large-scale production capacity allowed it to capture substantial market opportunities across retail and food packaging segments.

Huhtamaki Oyj demonstrated steady growth through its diversified coated paper packaging portfolio, especially in food service applications. The company leveraged its expertise in sustainable packaging materials, aligning with regulatory pressures and consumer preferences for recyclable and biodegradable options. This positioning enhanced its global footprint in both developed and emerging markets.

Smurfit Kappa Group Plc further strengthened its market leadership by focusing on high-quality, customizable coated paper packaging solutions. With strong investments in digital printing and innovative designs, the company catered to premium consumer goods and e-commerce sectors. Its robust distribution network supported its dominance across Europe and growing expansion in North America and Latin America.

GWP Packaging contributed significantly by offering tailored coated paper packaging boxes suited for specialized industries such as electronics and medical devices. Its focus on customization and protective solutions ensured competitive differentiation. The company’s agility in meeting client-specific requirements positioned it as a reliable partner for businesses demanding precision and flexibility in packaging solutions.

Together, these key players reinforced the market’s growth trajectory, reflecting how sustainability, innovation, and customization are driving competition in the coated paper packaging box industry.

Top Key Players in the Market

- WestRock Company

- Huhtamaki Oyj

- Smurfit Kappa Group Plc

- GWP Packaging

- DS Smith plc

- Robinson plc

- Stora Enso Oyj

- Pakfactory

- Burt Rigid Box

- Bigso Box of Swede

Recent Developments

- In Jan 2025, Sveza Group acquired new assets in the paper-making segment, strengthening its production capabilities and expanding its influence in the global paper industry. This move is expected to enhance operational efficiency and secure raw material supply for its diverse portfolio.

- In Jul 2025, JK Paper approved the acquisition of Borkar Packaging, marking a strategic entry into premium packaging solutions. This acquisition broadens JK Paper’s product offering and reinforces its position in the high-value packaging market.

- In Aug 2025, Siegwerk strengthened its coatings business with the acquisition of Allinova, a move aimed at boosting innovation and expanding sustainable product solutions. The deal supports Siegwerk’s long-term growth strategy in advanced coatings and specialty chemicals.

- In Jun 2024, Green Bay Packaging Inc. expanded operations with the acquisition of SMC Packaging Group, significantly increasing its footprint in corrugated packaging. This acquisition enhances its distribution network and meets rising demand in the U.S. packaging market.

Report Scope

Report Features Description Market Value (2024) USD 13.4 Billion Forecast Revenue (2034) USD 21.2 Billion CAGR (2025-2034) 4.7% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Box Type (Hinged lid Box, Telescopic Box, Shoulder Neck Box, Collapsible Box, Others), By Coating Type (Single-Sided Coating, Double-Sided Coating), By End Use (Fashion Accessories and Apparel, Food and Beverage, Cosmetic and Personal Care, Consumer Electronics, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape WestRock Company, Huhtamaki Oyj, Smurfit Kappa Group Plc, GWP Packaging, DS Smith plc, Robinson plc, Stora Enso Oyj, Pakfactory, Burt Rigid Box, Bigso Box of Swede Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Coated Paper Packaging Box MarketPublished date: Aug 2025add_shopping_cartBuy Now get_appDownload Sample

Coated Paper Packaging Box MarketPublished date: Aug 2025add_shopping_cartBuy Now get_appDownload Sample -

-

- WestRock Company

- Huhtamaki Oyj

- Smurfit Kappa Group Plc

- GWP Packaging

- DS Smith plc

- Robinson plc

- Stora Enso Oyj

- Pakfactory

- Burt Rigid Box

- Bigso Box of Swede

Our Clients

- 156349

- Aug 2025