Global Carbon Capture, Utilization, and Storage (CCUS) Market Size, Share, Growth Analysis By Service (Capture, Transportation, Utilization, Storage), By Technology (Solvents and Sorbents, Chemical Looping, Membranes, Others), By End-User Industry (Oil and Gas, Power Generation, Chemical and Petrochemical, Cement, Iron and Steel, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 178778

- Number of Pages: 242

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

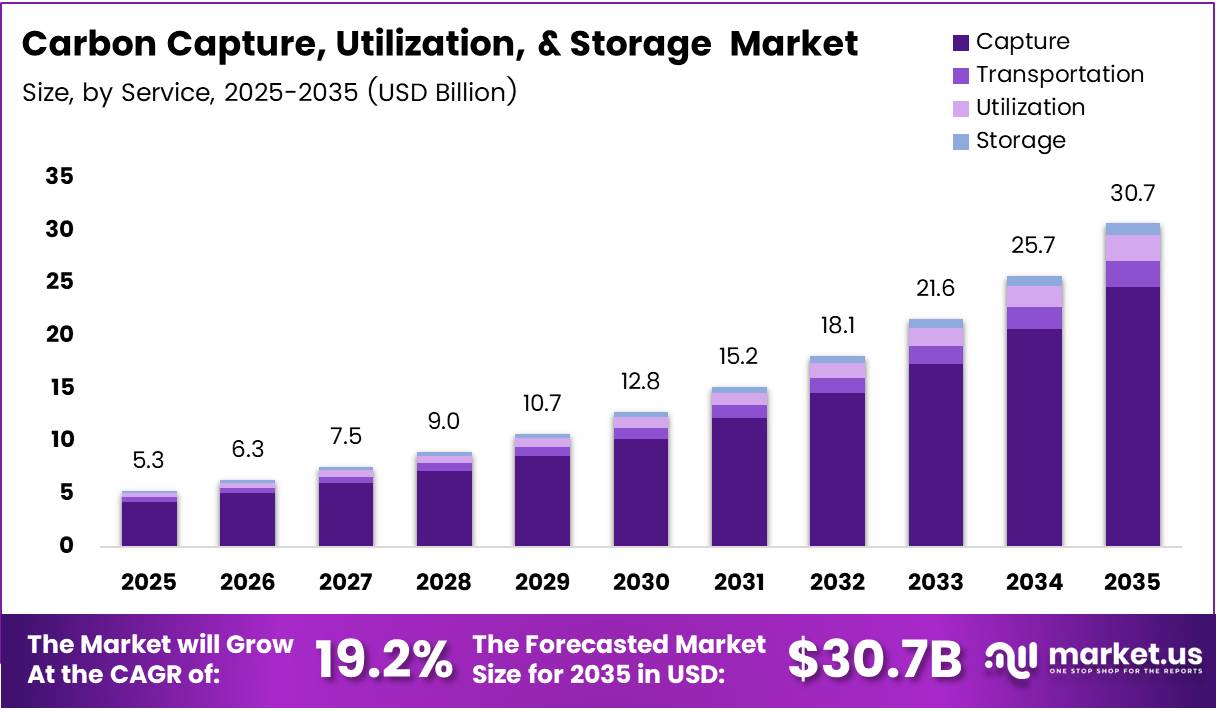

Global Carbon Capture, Utilization, and Storage (CCUS) Market size is expected to be worth around USD 30.7 Billion by 2035 from USD 5.30 Billion in 2025, growing at a CAGR of 19.20% during the forecast period 2026 to 2035.

The CCUS market covers technologies and services that capture CO₂ from industrial sources or the atmosphere, then transport, utilize, or permanently store it underground. This market spans the full carbon management chain — from solvent-based capture systems to geological storage infrastructure — serving hard-to-abate sectors such as oil and gas, power generation, and cement manufacturing.

Government policy sits at the center of this market’s commercial logic. Subsidy programs, carbon credit mechanisms, and net-zero mandates from major economies have turned CCUS from an experimental technology into a fundable infrastructure asset class. Without this policy layer, most projects would not clear investment hurdles — which means regulatory continuity is the single biggest variable investors must monitor.

Corporate ESG commitments have also shifted from voluntary branding to contractual obligations tied to financing conditions. Large industrial emitters now face direct pressure from lenders and shareholders to demonstrate measurable carbon reduction pathways. CCUS offers one of the few technically viable routes for industries where electrification cannot eliminate emissions — making it a strategic necessity, not just a sustainability preference.

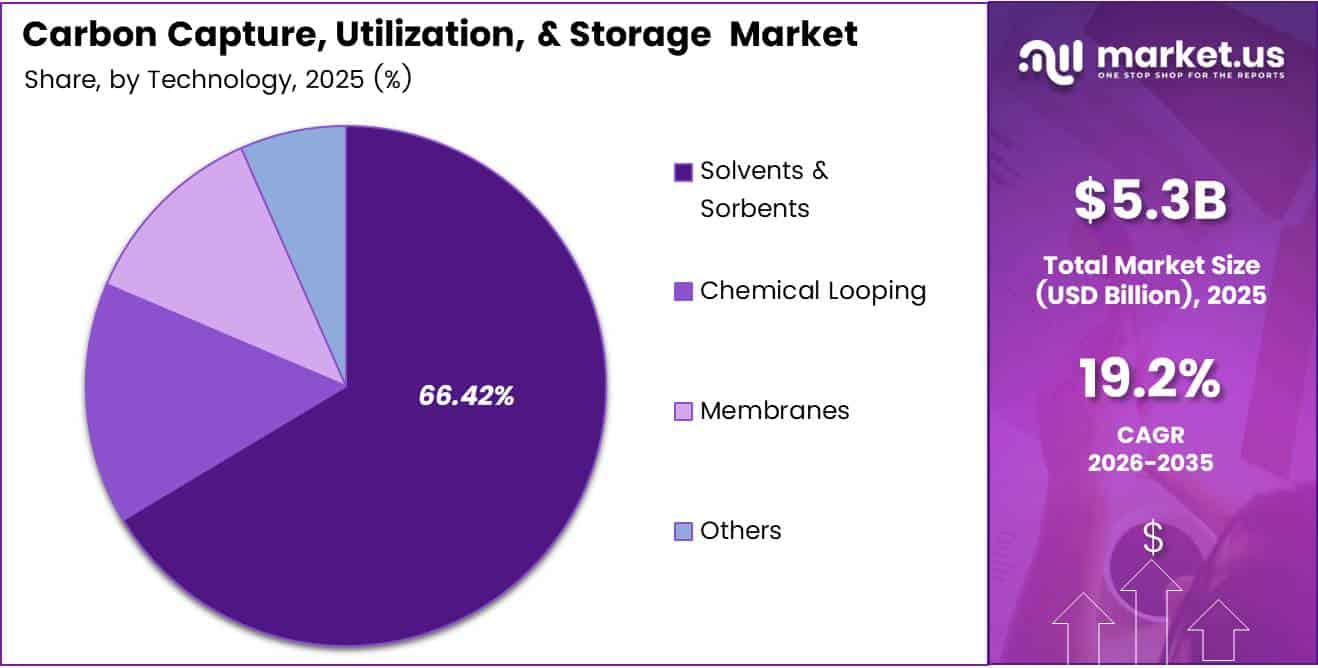

The Capture segment commands the largest share of the market, reflecting that front-end capture technology remains the most capital-intensive and technically complex part of the CCUS value chain. Solvents and sorbents account for 66.42% of the technology mix, indicating that the market still relies heavily on mature chemical absorption methods rather than emerging alternatives.

According to the International Energy Agency data reported by the Society of Chemical Industry, more than 50 million tonnes (Mt) of CO₂ capture and storage capacity is in operation globally as of early 2025. This figure confirms that commercial-scale deployment has moved beyond pilot projects — but at current rates, it remains a fraction of the volume needed to meet net-zero targets, signaling that the investment gap is still enormous.

According to the International Energy Agency project data via soci.org, approximately 45 commercial-scale CO₂ capture facilities operate worldwide. This concentration of capacity across a limited number of facilities means individual project economics carry outsized market risk — and that geographic diversification of infrastructure remains a structural priority for governments and developers alike.

Key Takeaways

- The global CCUS market was valued at USD 5.30 Billion in 2025 and is forecast to reach USD 30.7 Billion by 2035.

- The market advances at a CAGR of 19.20% during the forecast period 2026 to 2035.

- By Service, Capture leads with a dominant share of 80.30% of the market.

- By Technology, Solvents and Sorbents hold 66.42% share, making it the leading technology segment.

- By End-User Industry, Oil and Gas commands the largest share at 45.37%.

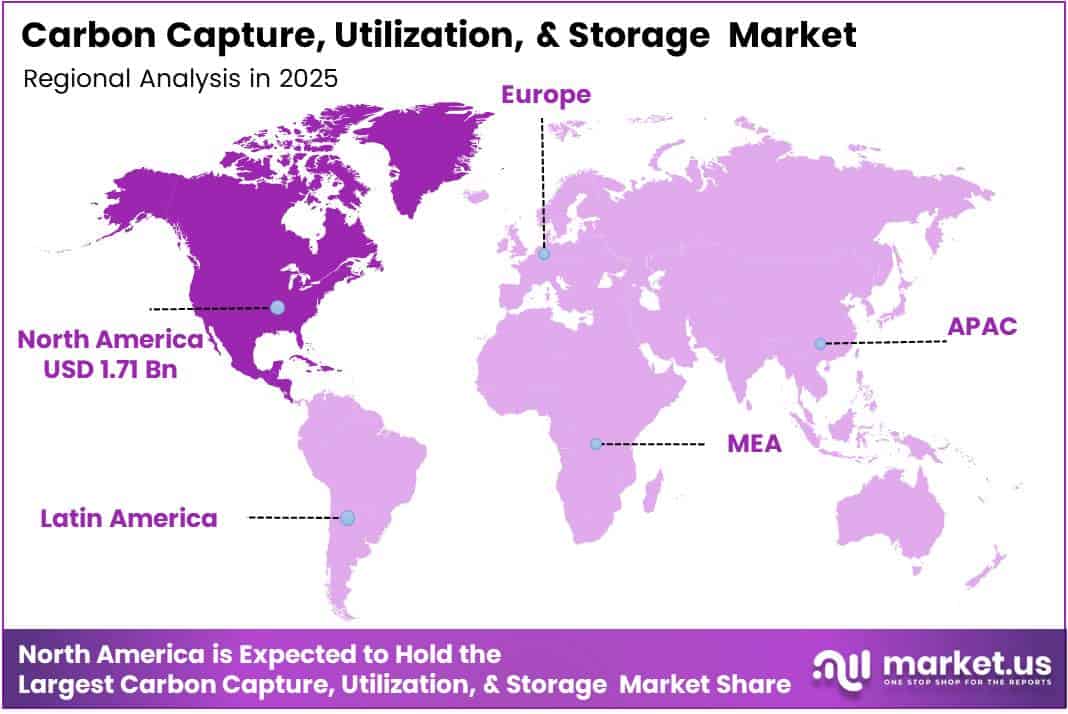

- North America dominates the regional landscape with 38.20% share, valued at USD 1.71 Billion.

Product Analysis

Capture dominates with 80.30% due to high capital intensity and technical complexity of front-end systems.

In 2025, Capture held a dominant market position in the By Service segment of the Carbon Capture, Utilization, and Storage (CCUS) Market, with an 80.30% share. This dominance reflects where the highest engineering effort and investment concentrate — upstream CO₂ separation remains the costliest and most technically demanding step, and vendors here command premium pricing and long-term service contracts.

Transportation serves as the connecting infrastructure between capture facilities and end-use or storage sites. Pipeline networks and shipping logistics for CO₂ require regulatory approvals, right-of-way negotiations, and specialized materials — creating a slower-moving but high-barrier segment that favors established energy infrastructure operators over new entrants.

Utilization differentiates through its ability to generate revenue from captured CO₂, converting it into fuels, chemicals, or building materials. This segment attracts investment precisely because it offers a commercial offset against capture costs — but current conversion economics remain constrained by energy input requirements and limited off-take markets at scale.

Storage carries the highest long-term liability within the CCUS chain, as permanent geological sequestration requires continuous monitoring, site certification, and regulatory compliance over decades. However, it also represents the most essential piece of the net-zero infrastructure puzzle — without viable storage, the entire upstream chain has nowhere to send captured CO₂.

Technology Analysis

Solvents and Sorbents dominate with 66.42% due to proven industrial-scale deployment and established supply chains.

In 2025, Solvents and Sorbents held a dominant market position in the By Technology segment of the CCUS Market, with a 66.42% share. Chemical absorption methods using amine-based solvents represent decades of engineering optimization — making them the default choice for large industrial emitters seeking reliable, bankable capture solutions rather than experimental alternatives.

Chemical Looping carries strong theoretical efficiency advantages over solvent systems, as it avoids energy-intensive solvent regeneration steps. However, it remains at an earlier commercialization stage, limiting its near-term competitive threat. Developers who reach commercial scale first in this segment will establish a durable cost advantage over later entrants.

Membranes differentiate through their potential for modular, lower-footprint deployment — particularly relevant for smaller industrial sites where traditional solvent plants are impractical. Moreover, membrane systems avoid liquid chemical handling, reducing operational complexity. Their commercial adoption will depend on achieving selectivity and throughput performance at competitive capital costs.

Others in the technology mix include cryogenic separation, mineralization, and direct air capture systems. These approaches target specific emission profiles or atmospheric CO₂, and while individually niche, they collectively represent the innovation frontier that will define next-generation CCUS economics as government R&D funding accelerates deployment timelines.

End-User Industry Analysis

Oil and Gas dominates with 45.37% due to regulatory exposure, existing infrastructure, and CO₂-enhanced recovery economics.

In 2025, Oil and Gas held a dominant market position in the By End-User Industry segment of the CCUS Market, with a 45.37% share. This sector combines the highest carbon liability exposure with the most direct economic incentive — enhanced oil recovery using CO₂ allows operators to monetize captured emissions while extending field production, creating a financial logic unavailable to other industries.

Power Generation represents the second major demand center, as coal and gas-fired plants face tightening emissions regulations across North America and Europe. Utilities operating baseload thermal assets under carbon pricing regimes must either retrofit with CCUS, pay increasing carbon costs, or shut down — making capture investment a forced economic decision rather than a voluntary one.

Chemical and Petrochemical producers face process emissions that cannot be eliminated through fuel switching alone, making CCUS one of the few decarbonization routes compatible with their existing operations. Additionally, some operators see captured CO₂ as a feedstock for low-carbon methanol or polymer production, adding a revenue dimension to what would otherwise be a pure compliance cost.

Cement manufacturing presents one of the structurally most challenging decarbonization problems, as roughly 60% of its CO₂ emissions come from limestone calcination — a chemical reaction independent of energy source. This makes CCUS not optional but technically necessary for cement producers targeting meaningful emissions reductions, driving long-term sector-specific demand.

Iron and Steel producers face similar process emission constraints, particularly in blast furnace operations where carbon plays a chemical role in iron reduction. Consequently, CCUS investment in this sector is increasingly tied to green steel transition roadmaps, with several major steelmakers piloting capture projects to secure future market access in carbon-regulated trade environments.

Others include sectors such as waste-to-energy, hydrogen production, and bioenergy facilities where CCUS can generate negative emissions credits. These applications remain early-stage commercially but represent high-value niches as carbon credit markets mature and bioenergy with carbon capture (BECCS) gains policy recognition in national net-zero strategies.

Key Market Segments

By Service

- Capture

- Transportation

- Utilization

- Storage

By Technology

- Solvents and Sorbents

- Chemical Looping

- Membranes

- Others

By End-User Industry

- Oil and Gas

- Power Generation

- Chemical and Petrochemical

- Cement

- Iron and Steel

- Others

Drivers

Government Incentive Programs and Corporate Net-Zero Commitments Drive Commercial CCUS Deployment

Expansion of government incentive programs — including carbon credit frameworks and direct subsidies — has fundamentally changed the investment calculus for CCUS projects. These mechanisms convert carbon reduction from a cost center into a revenue-generating asset. Without this policy layer, most large-scale projects would not achieve financial close under current technology economics.

According to International Energy Agency data via soci.org, CO₂ capture capacity rose from 47.4 Mt in Q1 2024 to over 50 Mt in Q1 2025. This year-on-year expansion confirms that incentive programs are translating into operational capacity — not just project announcements. Developers now see a clear line between policy commitment and bankable revenue streams from carbon credits.

Corporate net-zero commitments reinforce this dynamic from the demand side. In April 2025, Calpine and ExxonMobil signed a CO₂ transportation and storage agreement to permanently store up to 2 million metric tons of CO₂ per year from Calpine’s Baytown Energy Center in Texas. This deal illustrates how ESG obligations are forcing industrial operators to contract for CCUS capacity directly, creating durable long-term revenue visibility for infrastructure providers.

Restraints

High Capital Costs and Geological Storage Scarcity Constrain CCUS Project Economics

CCUS infrastructure demands substantial upfront capital before generating any return. Front-end capture equipment, pipeline networks, and storage site development each carry large individual cost burdens. For projects without long-term government subsidies or carbon credit offtake agreements, these economics remain prohibitive — particularly for industrial emitters outside the oil and gas sector with thinner margins.

According to multiple reports on the Norwegian CCS initiative, Norway’s Longship project involves roughly USD 3.4 billion in long-term subsidies and investment. The fact that one of the world’s most advanced CCUS projects requires this scale of government backing underscores how dependent the market remains on public funding — and signals the financial risk that private developers face without sovereign support.

Limited availability of suitable geological storage sites compounds the capital challenge. Not every industrial cluster sits near viable aquifers or depleted reservoirs. This mismatch between emission sources and storage locations forces costly CO₂ transportation — adding pipeline infrastructure investment and regulatory complexity that further stretches project timelines and strains returns for developers operating in geologically constrained regions.

Growth Factors

CCUS Integration with Hydrogen Production and Carbon-to-Value Technologies Opens New Revenue Pathways

The integration of CCUS with blue hydrogen production creates a commercially compelling bundled offering. Industrial facilities can capture CO₂ from natural gas reforming while simultaneously producing low-carbon hydrogen — generating both a carbon credit revenue stream and a clean fuel product. This dual-output model improves overall project economics compared with standalone capture infrastructure.

The Northern Lights facility in Norway marked the start of operations with the first volumes of CO₂ injected and stored — a milestone that demonstrates offshore geological storage at commercial scale for the first time in Europe. This operational proof point reduces perceived technical risk for developers considering similar offshore storage projects, potentially unlocking project pipelines in the North Sea and other offshore basins.

Development of carbon-to-value technologies — converting captured CO₂ into chemicals, fuels, or construction materials — represents a structural shift in CCUS economics. Rather than treating CO₂ as a waste stream, these technologies create sellable outputs that offset capture costs. Strategic partnerships between energy majors and technology providers are actively accelerating this commercialization pathway across multiple end-use applications.

Emerging Trends

Modular CCUS Solutions and AI-Driven Optimization Reshape Project Design and Operational Efficiency

Modular and small-scale CCUS systems are emerging as a practical solution for industrial facilities too small to justify conventional large-scale plant investment. These decentralized units lower the entry threshold for sectors like food processing, smaller cement plants, and distributed power assets. Consequently, they expand the addressable market well beyond the heavy industrial clusters that traditional CCUS projects target.

According to multiple reports by project owner announcements and industry press, the Northern Lights Phase 2 expansion targets an increase in storage capacity from 1.5 Mt to at least 5 Mt CO₂ per year. This planned scale-up signals that first-mover infrastructure is moving from demonstration to full commercial throughput — and that the pipeline of industrial emitters seeking verified storage capacity is outpacing initial facility sizing assumptions.

AI-driven monitoring and optimization tools are entering CCUS operations, enabling real-time performance management of capture units, compressors, and injection wells. Additionally, digital twins of storage reservoirs improve injection strategy and reduce monitoring costs over the project lifecycle. Early adopters of these operational technologies will achieve lower cost-per-tonne metrics — a decisive advantage as carbon credit markets mature and price pressure on capture efficiency intensifies.

Regional Analysis

North America Dominates the CCUS Market with a Market Share of 38.20%, Valued at USD 1.71 Billion

North America holds 38.20% of the global CCUS market, valued at USD 1.71 Billion, driven by a combination of mature carbon policy frameworks, substantial geological storage capacity, and deep energy industry infrastructure. The U.S. Section 45Q tax credit has been the single most effective commercial lever, enabling projects to achieve bankable returns without relying solely on voluntary carbon markets.

Europe CCUS Market Trends

Europe represents the second-largest regional market, anchored by Norway’s Longship and Northern Lights projects, which provide the continent’s first commercial-scale CO₂ shipping and offshore storage infrastructure. The EU Emissions Trading System imposes a direct carbon price on industrial emitters, creating structural financial pressure that accelerates CCUS adoption among power generators, steelmakers, and cement producers across member states.

Asia Pacific CCUS Market Trends

Asia Pacific holds significant long-term potential, with Japan, South Korea, and Australia leading regulatory development for carbon storage. Japan’s carbon recycling roadmap and Australia’s offshore CCS legislation provide frameworks that industrial operators need before committing capital. However, the region’s project pipeline remains thinner than North America or Europe, reflecting earlier-stage policy maturity and infrastructure readiness across most economies.

Middle East and Africa CCUS Market Trends

Middle East national oil companies are integrating CCUS into their long-term production strategies, recognizing that oil and gas export revenue depends on demonstrating emissions reduction credibility to carbon-regulated importing economies. The region’s abundant geological storage potential in depleted hydrocarbon reservoirs provides a natural asset base for large-scale sequestration, though project commercialization remains dependent on establishing viable carbon pricing frameworks domestically.

Latin America CCUS Market Trends

Latin America’s CCUS activity concentrates around Brazil’s pre-salt offshore oil production, where Petrobras reinjected CO₂ operations provide a proven model for associated gas capture. Regional industrial growth in cement, steel, and petrochemicals creates a long-term emissions base that will require carbon management solutions — but near-term project development depends on establishing clearer regulatory pathways and carbon credit monetization mechanisms at the national level.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Fluor Corporation positions itself as a full-scope EPC contractor across the CCUS value chain, combining engineering, procurement, and construction capabilities that few pure-play technology vendors can match. This integrated delivery model gives Fluor a structural advantage on large, complex projects where owner-operators prefer single-contract accountability over managing multiple specialist subcontractors simultaneously.

Exxon Mobil Corporation leverages decades of subsurface expertise and existing pipeline infrastructure to compete not just as an energy producer but as a third-party CO₂ storage and transportation provider. Its April 2025 agreement with Calpine — to permanently store up to 2 million metric tons of CO₂ annually — signals a deliberate strategy to build a carbon infrastructure business that generates long-term fee-based revenue independent of commodity prices.

Shell Plc has made a direct commercial bet on integrated CCS hub development, with its June 2024 Final Investment Decision for the Polaris CCS project in Canada targeting approximately 650,000 tonnes of CO₂ captured annually at Scotford. By combining a capture facility with the Atlas Carbon Storage Hub, Shell builds a vertically integrated asset that captures value across both the service and storage segments of the value chain.

Equinor ASA anchors its CCUS strategy in the Northern Lights project — the first commercial cross-border CO₂ shipping and offshore storage operation in Europe. This positions Equinor not as a technology vendor but as a carbon infrastructure operator, owning the storage asset that competing industrial emitters depend on. As Phase 2 expansion targets a fivefold capacity increase, Equinor’s first-mover storage position becomes a durable competitive moat.

Key Players

- Fluor Corporation

- Exxon Mobil Corporation

- Shell Plc

- Equinor ASA

- TotalEnergies

- Linde PLC

- Mitsubishi Heavy Industries Ltd

- JGC Holdings Corporation

- SLB

- Aker Solutions

- Honeywell International Inc.

- Hitachi

- Siemens Energy

- GE Vernova

- Halliburton

- Others

Recent Developments

- August 2025 — Norway’s Northern Lights CCS facility started operations, with the first volumes of CO₂ successfully injected and stored offshore, marking the first commercial cross-border carbon storage project to reach operational status in Europe.

- 2025 — Northern Lights received approval for Phase 2 storage expansion, with plans to increase annual CO₂ storage capacity from 1.5 Mt to at least 5 Mt, representing a more than threefold scale-up of the facility’s throughput capability.

- June 2024 — Shell announced its Final Investment Decision for the Polaris CCS project in Canada, targeting capture of approximately 650,000 tonnes of CO₂ per year at the Shell Energy and Chemicals Park in Scotford, Alberta, paired with the Atlas Carbon Storage Hub for permanent underground sequestration.

Report Scope

Report Features Description Market Value (2025) USD 5.30 Billion Forecast Revenue (2035) USD 30.7 Billion CAGR (2026-2035) 19.20% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Service (Capture, Transportation, Utilization, Storage), By Technology (Solvents and Sorbents, Chemical Looping, Membranes, Others), By End-User Industry (Oil and Gas, Power Generation, Chemical and Petrochemical, Cement, Iron and Steel, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Fluor Corporation, Exxon Mobil Corporation, Shell Plc, Equinor ASA, TotalEnergies, Linde PLC, Mitsubishi Heavy Industries Ltd, JGC Holdings Corporation, SLB, Aker Solutions, Honeywell International Inc., Hitachi, Siemens Energy, GE Vernova, Halliburton, Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Market") Carbon Capture, Utilization, and Storage (CCUS) MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample

Carbon Capture, Utilization, and Storage (CCUS) MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Fluor Corporation

- Exxon Mobil Corporation

- Shell Plc

- Equinor ASA

- TotalEnergies

- Linde PLC

- Mitsubishi Heavy Industries Ltd

- JGC Holdings Corporation

- SLB

- Aker Solutions

- Honeywell International Inc.

- Hitachi

- Siemens Energy

- GE Vernova

- Halliburton

- Others

Our Clients

- 178778

- Feb 2026