Global Carbon Accounting Software Market Size, Share, Growth Analysis By Component (Software/Solutions, Services), By Deployment Mode (Cloud-based, On-premises), By Organization Size (Large Enterprises, Small and Medium-sized Enterprises), By Product Type (Enterprise Carbon Accounting Software, Carbon Footprint Management Software, Carbon Emission Tracking Tools, Climate Risk Assessment Software, Sustainability Reporting Tools, Carbon Offsetting Solutions, Others), By Technology Type (Cloud-based Platforms, AI-driven Solutions, IoT-integrated Systems, Machine Learning, Blockchain-based Systems, Others), By Application (ESG and Sustainability Reporting, Regulatory Compliance, Real-time Emission Monitoring, Investment and Risk Management, Energy Efficiency Optimization, Emissions Tracking and Compliance, Sustainability Strategy Development, Others), By End-User Industry (Energy and Utilities, IT and Telecom, Healthcare, Transportation and Logistics, Retail, Construction and Infrastructure, Food and Beverages, Chemicals, Oil and Gas, Manufacturing, Financial Institutions, Government Organizations, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2025-2035

- Published date: Feb 2026

- Report ID: 179566

- Number of Pages: 352

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Effective Takeaways

- Future Predictions

- Market Adoption

- By Component

- By Deployment Mode

- By Organization Size

- By Product Type

- By Technology Type

- By Application

- By End-User Industry

- Key Market Segments

- Regional Analysis

- US Market Size

- Driving Factors

- Restraint factors

- Growth Opportunities

- Trending factors

- Competitive Analysis

- Recent Developments

- Report Scope

Report Overview

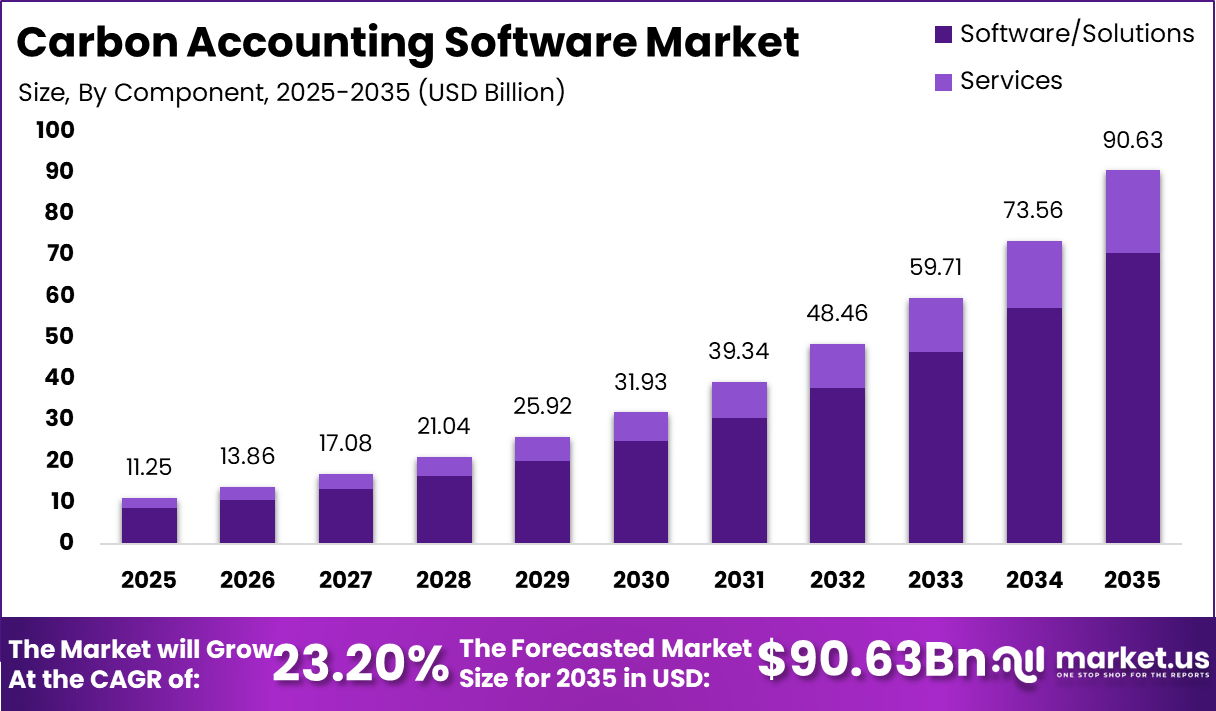

The Carbon Accounting Software market is poised for remarkable expansion, with a projected growth from USD 11.25 billion in 2025 to USD 90.63 billion by 2035, reflecting a CAGR of 23.2%. North America dominates the market with a 41.2% share, reaching USD 4.63 billion in 2025. The US alone contributes USD 4.19 billion and is expected to grow to USD 29.69 billion by 2035 at a CAGR of 21.63%. This rapid growth underscores the increasing corporate and regulatory emphasis on carbon footprint management and sustainability compliance.

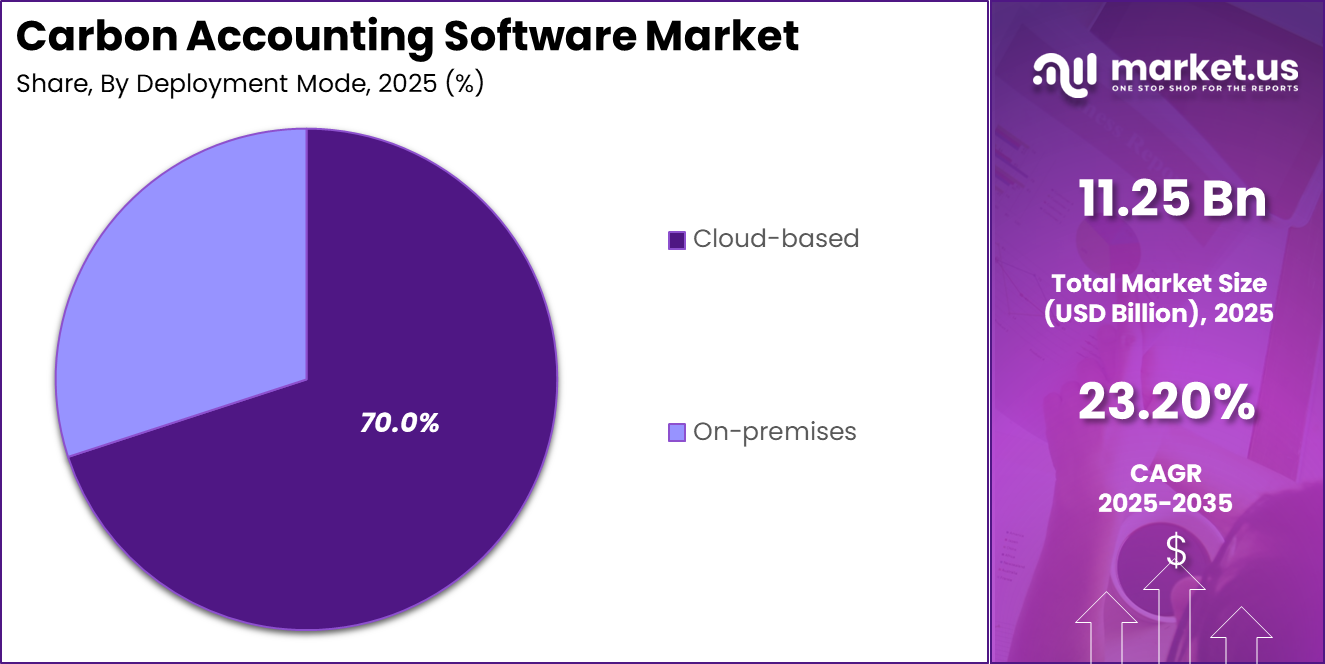

The market is primarily driven by software/solutions, accounting for 78% of the share, with cloud-based deployment capturing 70%, highlighting the shift toward scalable, real-time platforms. Large enterprises lead adoption at 65%, leveraging emission tracking platforms (28%) and cloud-based technologies (58%) to optimize ESG and sustainability reporting (32%). The energy and utilities sector represents the largest end-user segment at 35%, reflecting its critical role in global carbon management initiatives.

As organizations face rising pressure from investors, regulators, and consumers to reduce emissions and enhance transparency, this market offers high-value opportunities for strategic technology investments. This report provides comprehensive insights, detailed segmentation, and actionable intelligence, equipping stakeholders to make informed decisions and capitalize on the fast-growing carbon accounting software landscape.

The Carbon Accounting Software market is experiencing substantive expansion driven by global climate action, mandatory emissions reporting frameworks, and increasing corporate net‑zero commitments. According to estimates from international climate reporting bodies, over 90% of the world’s largest 2,000 companies now disclose greenhouse gas emissions annually.

Up from about 50% just a decade ago, creating substantial demand for reliable carbon accounting tools. At the same time, global CO₂ emissions surpassed 36.3 billion tonnes in 2023, highlighting the urgency for organizations to systematically measure and reduce their carbon footprints.

Regulatory momentum is strengthening: more than 130 countries now have some form of national climate law or emissions‑related regulation, up from around 60 countries in 2007, which directly increases corporate reporting obligations. In the United States, the number of companies voluntarily disclosing Scope 3 emissions has risen by over 150% in the past five years, reflecting a shift toward comprehensive emissions transparency that carbon accounting software uniquely supports.

Cloud‑based solutions now represent the majority of deployments, providing real‑time data integration and automated analytics that significantly reduce manual reporting errors. Enterprises with structured sustainability strategies report up to 40% faster reporting cycles after adopting carbon accounting systems.

Illustrating measurable operational efficiency gains. With stakeholder demand for credible ESG disclosure intensifying, investment in carbon accounting software is no longer optional — it is a strategic imperative that delivers both compliance assurance and competitive advantage.

Effective Takeaways

- The global market is projected to grow from USD 11.25 billion in 2025 to USD 90.63 billion by 2035 at a CAGR of 23.2%.

- North America holds the largest share at 41.2%, valued at USD 4.63 billion in 2025.

- The US market is expected to reach USD 29.69 billion by 2035 with a CAGR of 21.63%.

- Software and solutions dominate the market with a 78% share.

- Cloud-based deployment leads adoption at 70% due to scalability and real-time analytics.

- Large enterprises account for 65% of total market adoption.

- Emission tracking platforms are the most popular product type at 28%.

- Cloud-based platforms form 58% of the technology type segment.

- ESG and sustainability reporting applications represent 32% of usage.

- Energy and utilities are the leading end-user industry with a 35% share.

Future Predictions

The Carbon Accounting Software market is set for substantial evolution over the next decade as regulatory frameworks, investor expectations, and corporate sustainability commitments deepen. With global climate policies becoming more stringent, mandatory reporting requirements for greenhouse gas emissions will expand beyond large public companies to include mid‑sized and privately held firms.

This shift will drive broader adoption of automated carbon accounting platforms that can manage Scope 1, Scope 2, and increasingly complex Scope 3 emissions data with accuracy and audit readiness. Cloud‑based solutions will continue to outpace on‑premises deployments due to their flexibility, real‑time analytics, and ease of integration with enterprise resource planning (ERP) and internet of things (IoT) systems.

AI and machine learning will increasingly be embedded into these platforms to enable predictive emissions modelling, anomaly detection, and automated recommendations for emissions reduction strategies. This technological advancement will improve data quality and reduce the manual burden on sustainability teams.

Large enterprises will maintain leadership in adoption, but mid‑sized companies will accelerate uptake as carbon pricing mechanisms and supply chain emissions scrutiny intensify. Sectors such as energy and utilities, manufacturing, and transportation will invest heavily in carbon accounting to support decarbonization roadmaps and meet investor expectations for transparency.

As investors, customers, and regulators demand more rigorous ESG disclosures, carbon accounting software will evolve from a compliance tool to a strategic enabler of decarbonization and competitive differentiation.

Market Adoption

The adoption of carbon accounting software across industries is accelerating as organizations recognize the strategic importance of managing carbon emissions and enhancing sustainability reporting. The energy and utilities sector leads adoption, representing 35% of the market, driven by regulatory pressure to reduce emissions and transition to cleaner energy sources.

Companies in this sector increasingly rely on cloud-based platforms for real-time monitoring of emissions, enabling them to meet stringent compliance requirements and optimize operational efficiency. Manufacturing and heavy industries are also investing in carbon accounting solutions to track Scope 1, 2, and 3 emissions across complex supply chains.

These industries face growing stakeholder scrutiny and are leveraging software to quantify carbon footprints, implement reduction strategies, and report transparently on sustainability goals. The adoption of financial services and retail is rising, primarily for ESG reporting and investor compliance, as more organizations integrate environmental performance into their decision-making processes.

Large enterprises dominate adoption at 65%, but mid-sized companies are expected to increase uptake as carbon pricing, voluntary reporting standards, and supply chain accountability expand. Cloud deployment, accounting for 70% of adoption, provides scalability and integration capabilities that appeal across sectors.

Overall, industry adoption is being fueled by regulatory mandates, investor expectations, and operational benefits, positioning carbon accounting software as a critical tool for achieving sustainability and ESG objectives across diverse industries.

By Component

78% of the component market is attributed to software and solutions, with services representing the remaining share (approximately 22%). Software and solutions dominate because they provide end-to-end capabilities for data ingestion, automated emissions calculations across Scope 1, 2, and 3, and audit-ready reporting that is expected to meet tightening regulatory and investor requirements.

These platforms are projected to deliver faster reporting cycles, higher data fidelity, and advanced analytics through embedded AI and machine learning, enabling proactive decarbonization planning. Services remain strategically important by delivering implementation, data integration, validation, training, and verification support that accelerate software adoption and ensure compliance readiness.

Managed services and advisory offerings are anticipated to grow as organizations seek turnkey arrangements to operationalize carbon accounting. Together, software and services form a complementary ecosystem where scalable platforms provide the core capability and professional services enable tailored deployment, governance, and continuous improvement in corporate sustainability programs.

By Deployment Mode

Cloud-based deployment dominates the carbon accounting software market with a 70% share, while on-premises solutions account for the remaining 30%. The preference for cloud-based systems is driven by their scalability, real-time data access, and ability to integrate seamlessly with existing enterprise systems such as ERP, IoT, and business intelligence platforms.

Organizations can leverage these platforms to automate emissions tracking, generate audit-ready reports, and analyze sustainability performance efficiently across multiple locations. On-premises solutions continue to be adopted by companies with strict data security policies or regulatory restrictions, but their growth is slower due to higher upfront costs, maintenance requirements, and limited flexibility compared to cloud-based platforms.

Cloud deployments also support advanced technologies like AI and machine learning, enabling predictive emissions modelling, anomaly detection, and actionable insights for carbon reduction strategies. Large enterprises are the primary adopters, using cloud systems to manage complex operations.

Ensure compliance with evolving ESG and sustainability regulations, and enhance transparency for investors and stakeholders. Overall, cloud-based deployment is expected to remain the preferred choice, offering agility, cost efficiency, and scalability, while on-premises solutions retain a niche role for organizations with specific compliance or security needs.

By Organization Size

Large enterprises dominate the carbon accounting software market with a 65% share, while small and medium-sized enterprises (SMEs) account for the remaining 35%. Large organizations adopt these solutions to manage complex operations, comply with stringent regulatory requirements, and provide transparent ESG and sustainability reporting to investors and stakeholders.

Their scale and resource availability allow them to implement comprehensive software platforms, often leveraging cloud-based systems for real-time emissions tracking, analytics, and reporting across multiple locations. SMEs are increasingly adopting carbon accounting software as regulatory pressure and stakeholder expectations extend beyond large corporations.

Cloud-based solutions make these tools more accessible and cost-effective for smaller organizations, allowing them to automate data collection, monitor emissions, and generate sustainability reports without significant IT investment. While SMEs currently represent a smaller share, their adoption is expected to grow steadily as environmental compliance, corporate social responsibility initiatives, and supply chain accountability become critical for maintaining market competitiveness.

Overall, large enterprises lead adoption due to their operational complexity and reporting needs, while SMEs are gradually integrating these solutions, highlighting a broader industry shift toward universal carbon management and sustainability practices.

By Product Type

Emission tracking platforms lead the product type segment with a 28% share, reflecting strong demand for tools that monitor and quantify organizational carbon emissions in real time. Enterprise carbon accounting software is widely adopted by large organizations to centralize emissions data, streamline reporting, and support strategic decarbonization initiatives.

Carbon footprint management software allows businesses to evaluate and reduce their environmental impact across operations and supply chains, while carbon emission tracking tools focus on real-time measurement and operational monitoring.

Climate risk assessment software helps organizations identify and mitigate environmental and regulatory risks that may affect business continuity. Sustainability reporting tools enable standardized ESG disclosures, meeting both global and regional compliance requirements. Carbon offsetting solutions provide a mechanism for organizations to compensate for unavoidable emissions through verified environmental projects.

Other niche solutions complement the ecosystem by offering specialized analytics, scenario planning, or sector-specific reporting capabilities. Collectively, these products provide organizations with comprehensive solutions to manage carbon emissions, improve transparency, and achieve sustainability objectives.

By Technology Type

Cloud-based platforms dominate the technology type segment with a 58% share, reflecting their flexibility, scalability, and real-time data processing capabilities. These platforms enable organizations to integrate emissions data across multiple sites, automate reporting, and generate actionable insights for sustainability and ESG compliance.

AI-driven solutions are increasingly incorporated to provide predictive analytics, identify emissions reduction opportunities, and optimize operational efficiency. Machine learning enhances data accuracy and supports scenario modeling for strategic decarbonization planning. IoT-integrated systems allow real-time collection of energy and emissions data from connected devices, improving monitoring and operational control.

Blockchain-based systems are emerging to ensure transparency, traceability, and security of carbon transactions and sustainability reporting. Other specialized technologies offer sector-specific analytics, reporting templates, and decision-support tools to complement core platforms. The combined use of these technologies enables organizations to manage complex carbon accounting requirements, enhance compliance with regulatory frameworks, and improve stakeholder confidence.

Cloud-based platforms remain the backbone due to their ease of deployment and integration, while AI, ML, IoT, and blockchain provide advanced capabilities that strengthen emissions management and sustainability performance. Overall, technology adoption in carbon accounting software is focused on delivering real-time insights, predictive intelligence, and secure, transparent reporting.

By Application

ESG and sustainability reporting lead the application segment with a 32% share, highlighting the increasing importance of transparent environmental, social, and governance disclosures. Organizations use these applications to generate standardized, audit-ready reports that meet investor expectations, regulatory requirements, and global sustainability frameworks.

Real-time emission monitoring enables continuous data collection from operations, providing actionable insights for immediate corrective measures. Investment and risk management applications assess environmental risks and inform strategic decisions related to capital allocation and portfolio management. Energy efficiency optimization tools support organizations in reducing consumption, lowering emissions, and achieving sustainability targets.

Emissions tracking and compliance platforms streamline data aggregation and reporting, improving accuracy and operational efficiency. Sustainability strategy development applications assist in setting long-term decarbonization goals, monitoring progress, and aligning corporate initiatives with global climate commitments. Other specialized applications provide industry-specific analytics, benchmarking, and scenario modeling.

Overall, the diverse application portfolio allows organizations to integrate sustainability into core operations, enhance transparency, and drive performance improvement. ESG and sustainability reporting remain central as companies face rising pressure from investors, regulators, and stakeholders to demonstrate measurable environmental impact and accountability.

By End-User Industry

The energy and utilities sector leads the end-user industry segment with a 35% share, reflecting high demand for carbon accounting software to manage emissions, meet regulatory requirements, and support sustainability initiatives. Companies in this sector leverage these tools for real-time monitoring, emission reduction planning, and ESG reporting, ensuring compliance with evolving environmental standards and enhancing operational efficiency.

IT and telecom industries are increasingly adopting carbon accounting solutions to manage energy-intensive operations, data centers, and network infrastructure emissions. Healthcare organizations use these platforms to monitor facility emissions and improve sustainability reporting, while transportation and logistics companies implement tracking systems to optimize fuel usage and reduce carbon footprints.

Retail and manufacturing sectors adopt carbon accounting software to manage supply chain emissions and improve transparency for consumers and investors. Construction and infrastructure firms utilize these tools for project-level emissions monitoring and regulatory compliance.

Food and beverage, chemicals, and oil and gas industries are integrating carbon management systems to meet environmental regulations and reduce operational emissions. Financial institutions and government organizations are leveraging software for ESG assessments, risk management, and policy compliance. Other industries are adopting specialized solutions tailored to sector-specific sustainability requirements.

Overall, diverse industry adoption reflects the growing emphasis on measurable carbon management, regulatory compliance, and stakeholder accountability, positioning carbon accounting software as an essential tool across multiple sectors.

Key Market Segments

By Component

- Software/Solutions

- Services

By Deployment Mode

- Cloud-based

- On-premises

By Organization Size

- Large Enterprises

- Small and Medium-sized Enterprises

By Product Type

- Enterprise Carbon Accounting Software

- Carbon Footprint Management Software

- Carbon Emission Tracking Tools

- Climate Risk Assessment Software

- Sustainability Reporting Tools

- Carbon Offsetting Solutions

- Others

By Technology Type

- Cloud-based Platforms

- AI-driven Solutions

- IoT-integrated Systems

- Machine Learning

- Blockchain-based Systems

- Others

By Application

- ESG and Sustainability Reporting

- Regulatory Compliance

- Real-time Emission Monitoring

- Investment and Risk Management

- Energy Efficiency Optimization

- Emissions Tracking and Compliance

- Sustainability Strategy Development

- Others

By End-User Industry

- Energy and Utilities

- IT and Telecom

- Healthcare

- Transportation and Logistics

- Retail

- Construction and Infrastructure

- Food and Beverages

- Chemicals

- Oil and Gas

- Manufacturing

- Financial Institutions

- Government Organizations

- Others

Regional Analysis

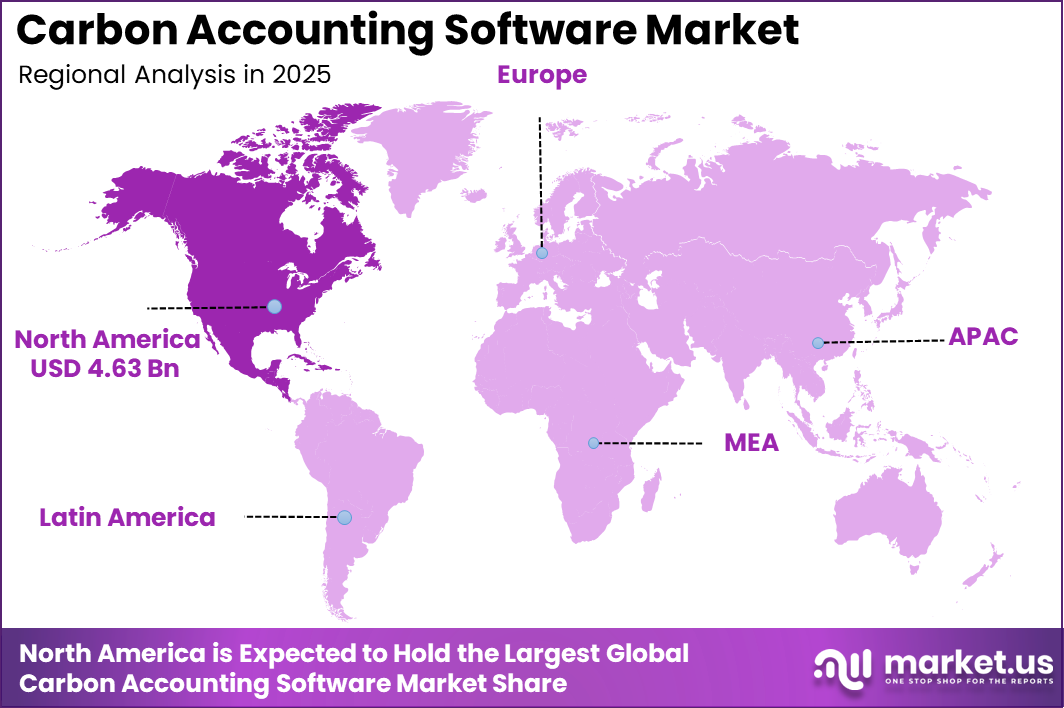

North America dominates the carbon accounting software market with a 41.2% share, valued at USD 4.63 billion in 2025. The region’s leadership is driven by stringent environmental regulations, growing investor pressure for ESG disclosures, and widespread corporate adoption of sustainability initiatives. Canada and Mexico are also showing steady growth as businesses expand carbon management practices to meet local regulatory requirements and international climate commitments.

Cloud-based deployment is preferred across the region due to its scalability, real-time analytics, and ability to integrate with enterprise systems such as ERP, IoT, and business intelligence platforms. Large enterprises lead adoption, leveraging advanced software and AI-driven analytics to optimize energy usage, reduce emissions, and develop decarbonization strategies.

The energy and utilities sector, along with manufacturing, IT, and financial services, represents the most significant end users, reflecting operational complexity and high emissions accountability. Overall, North America’s regulatory environment, technological adoption, and corporate sustainability focus position it as a key growth driver in the global carbon accounting software market.

US Market Size

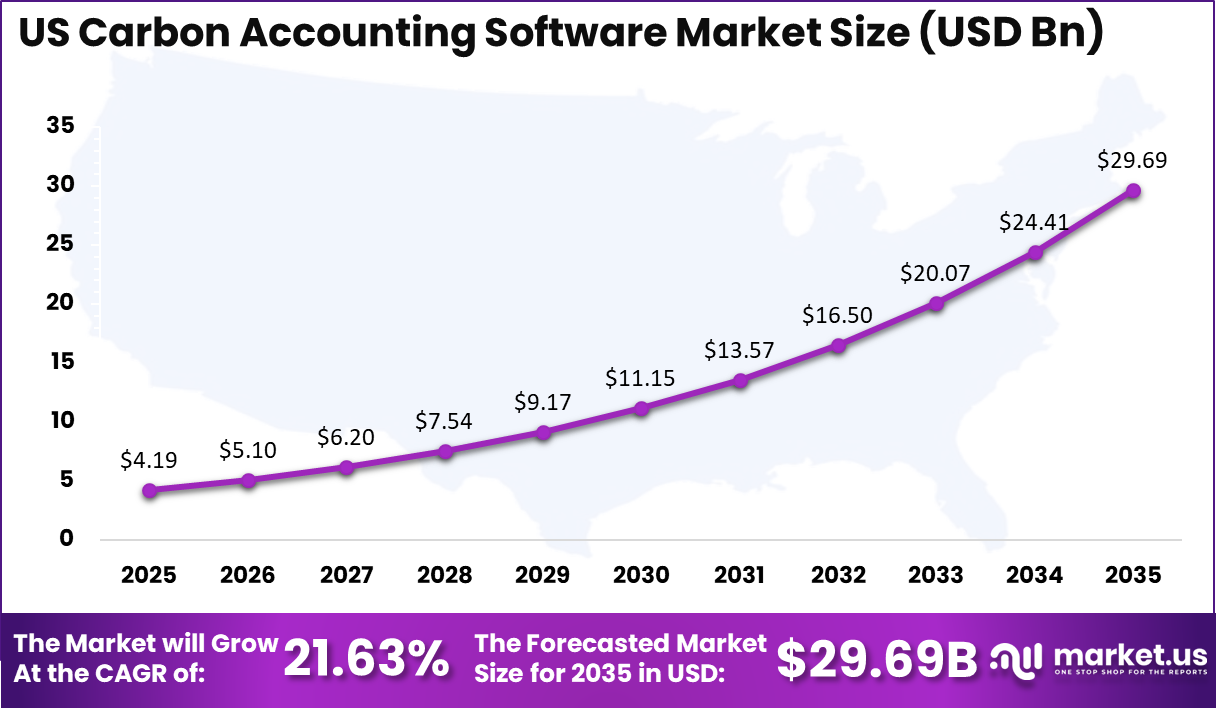

The US carbon accounting software market is projected to grow from USD 4.19 billion in 2025 to USD 29.69 billion by 2035, reflecting a robust CAGR of 21.63%. This growth is driven by increasing regulatory requirements, rising investor expectations for ESG disclosures, and widespread corporate adoption of sustainability strategies.

Large enterprises are leading adoption due to their operational complexity and the need for centralized, real-time carbon management solutions. Cloud-based deployment dominates, offering scalability, integration with enterprise systems, and advanced analytics powered by AI and machine learning. The energy and utilities sector, followed by manufacturing, IT, and financial services, represents the largest end-user industries, reflecting high emissions intensity and regulatory accountability.

The US market is also benefiting from increasing stakeholder pressure for credible ESG reporting and corporate decarbonization initiatives. Companies are leveraging carbon accounting software not only for compliance but also for strategic decision-making, operational efficiency, and long-term sustainability planning. Overall, the US is expected to remain the leading regional market, setting a benchmark for adoption and innovation in carbon management solutions.

Regional Analysis and Coverage

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of Latin America

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driving Factors

The carbon accounting software market is experiencing strong momentum due to growing corporate responsibility toward environmental sustainability. Organizations are increasingly under pressure from regulators, investors, and consumers to monitor, report, and reduce carbon emissions across operations.

Cloud-based platforms and AI-driven tools allow real-time data collection and analysis, enabling companies to track Scope 1, 2, and 3 emissions efficiently. Energy-intensive sectors such as utilities, manufacturing, and transportation are adopting these solutions to optimize energy consumption and achieve decarbonization goals.

Additionally, rising awareness of climate risks and the financial impact of carbon management is motivating enterprises to implement comprehensive reporting frameworks. The integration of sustainability objectives into corporate strategy further reinforces the adoption of software that supports ESG compliance and operational efficiency. These factors collectively drive the increasing deployment of carbon accounting tools across diverse industries.

Restraint factors

Adoption of carbon accounting software faces several challenges that may slow growth. High costs associated with purchasing, implementing, and maintaining advanced platforms can deter smaller businesses. Complex integration with existing enterprise systems and supply chains often requires specialized technical expertise, creating barriers for organizations with limited resources.

Variations in global regulatory standards and inconsistent emission measurement methodologies can complicate compliance efforts. Data security and privacy concerns, particularly for cloud-based deployments, add further caution among potential adopters.

Additionally, the lack of trained personnel to interpret emissions data and develop actionable sustainability strategies can limit the effectiveness of software solutions. These challenges highlight the need for simplified, user-friendly, and secure platforms that address both technical and operational hurdles.

Growth Opportunities

The market for carbon accounting software is set to expand as organizations intensify efforts to meet sustainability targets. Growing regulatory frameworks worldwide create opportunities for software adoption, especially in regions introducing stricter climate reporting mandates.

Small and medium-sized enterprises are emerging as a key segment, benefiting from cloud-based solutions that offer cost-effective deployment and scalability. Technological advancements, including AI, machine learning, IoT, and blockchain, present opportunities to enhance predictive analytics, real-time monitoring, and secure data management.

Increased focus on Scope 3 emissions and supply chain transparency further drives demand for sophisticated tracking platforms. Partnerships between software providers and consulting firms, as well as expansion into untapped geographic markets, are additional avenues for growth. Collectively, these factors position the market for accelerated adoption and long-term expansion.

Trending factors

Current trends indicate a move toward automation, cloud adoption, and AI-enabled carbon management systems. Organizations are leveraging real-time dashboards and predictive analytics to monitor emissions and identify reduction opportunities. ESG and sustainability reporting have become a core requirement, driving software development to support compliance with international standards.

Industries such as energy, manufacturing, and transportation are at the forefront, while SMEs are increasingly adopting scalable platforms. Emerging technologies like blockchain for traceability and IoT sensors for continuous emissions tracking are influencing product innovation.

Companies are also integrating carbon accounting software into broader sustainability strategies, including emissions reduction planning and energy efficiency optimization. These trends demonstrate the market’s evolution toward comprehensive, intelligent, and actionable carbon management solutions.

Competitive Analysis

The competitive landscape of the Carbon Accounting Software market is marked by strong innovation, strategic partnerships, and rapid product enhancement as vendors vie to support increasingly sophisticated sustainability and ESG requirements. Established enterprise software providers are expanding their carbon management capabilities by embedding advanced analytics, real‑time monitoring, and regulatory reporting modules into broader environmental performance suites.

These incumbents leverage existing customer bases and integration ecosystems (ERP, BI, and IoT platforms) to strengthen market penetration and drive cross‑sell opportunities. At the same time, specialized carbon accounting vendors focus on modular, cloud‑native solutions tailored for real‑time emissions tracking, Scope 3 data management, and audit‑ready ESG reporting, differentiating through usability, automation, and predictive insights powered by AI and machine learning.

Strategic partnerships and ecosystem collaborations are also shaping competition. Software providers are increasingly teaming with consulting firms and sustainability advisory networks to offer implementation support, data governance frameworks, and benchmarking services that enhance customer outcomes. Open APIs and integrations with IoT sensors, blockchain traceability solutions, and data verification services further distinguish competitive offerings by enabling seamless data flows and trusted audit trails.

Mid‑sized and emerging vendors compete on agility and niche innovation, often focusing on industry‑specific capabilities for sectors such as energy, manufacturing, and logistics. These players emphasize rapid deployment, cost efficiency, and flexible reporting templates to attract organizations seeking scalable carbon management tools without heavy customization. Overall, competition centers on depth of functionality, integration strength, deployment flexibility, and the ability to deliver actionable insights that accelerate decarbonization and ESG performance.

Top Key Players in the Market

- Microsoft Corporation

- Salesforce, Inc.

- IBM Corporation

- SAP SE

- Persefoni AI Inc.

- Sphera Solutions GmbH

- Watershed Technology, Inc.

- Sweep

- Greenly

- Diligent Corporation

- Sinai Technologies

- Emitwise

- Plan A

- Cority Software Inc.

- Gravity

- Others

Recent Developments

- In Q1 2025, Salesforce unveiled Net Zero Cloud 2.0, enhancing its carbon accounting platform with advanced emissions tracking, automated regulatory reporting, and deeper integration for enterprise ESG compliance workflows.

- Envizi secured a major contract with the Australian government in Q1 2025 to provide its carbon accounting platform for national greenhouse gas emissions reporting, marking one of the largest public sector deployments in the region.

- Plan A raised USD 50 million in Series B funding in Q2 2025 to scale its carbon accounting software across Europe and accelerate product development focused on decarbonization analytics and automation.

Report Scope

Report Features Description Market Value (2025) USD 11.25 Billion Forecast Revenue (2035) USD 90.63 Billion CAGR(2025-2035) 23.20% Base Year for Estimation 2024 Historic Period 2020-2024 Forecast Period 2025-2035 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics, and Emerging Trends Segments Covered By Component (Software/Solutions, Services), By Deployment Mode (Cloud-based, On-premises), By Organization Size (Large Enterprises, Small and Medium-sized Enterprises), By Product Type (Enterprise Carbon Accounting Software, Carbon Footprint Management Software, Carbon Emission Tracking Tools, Climate Risk Assessment Software, Sustainability Reporting Tools, Carbon Offsetting Solutions, Others), By Technology Type (Cloud-based Platforms, AI-driven Solutions, IoT-integrated Systems, Machine Learning, Blockchain-based Systems, Others), By Application (ESG and Sustainability Reporting, Regulatory Compliance, Real-time Emission Monitoring, Investment and Risk Management, Energy Efficiency Optimization, Emissions Tracking and Compliance, Sustainability Strategy Development, Others), By End-User Industry (Energy and Utilities, IT and Telecom, Healthcare, Transportation and Logistics, Retail, Construction and Infrastructure, Food and Beverages, Chemicals, Oil and Gas, Manufacturing, Financial Institutions, Government Organizations, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Microsoft Corporation, Salesforce, Inc., IBM Corporation, SAP SE, Persefoni AI Inc., Sphera Solutions GmbH, Watershed Technology, Inc., Sweep, Greenly, Diligent Corporation, Sinai Technologies, Emitwise, Plan A, Cority Software Inc., Gravity, Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Carbon Accounting Software MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample

Carbon Accounting Software MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Microsoft Corporation

- Salesforce, Inc.

- IBM Corporation

- SAP SE

- Persefoni AI Inc.

- Sphera Solutions GmbH

- Watershed Technology, Inc.

- Sweep

- Greenly

- Diligent Corporation

- Sinai Technologies

- Emitwise

- Plan A

- Cority Software Inc.

- Gravity

- Others

Our Clients

- 179566

- Feb 2026