Global Calcium Acetate Market Size, Share, And Business Benefits By Grade (Pharmaceutical Grade, Industrial Grade), By Function (Firming Agent, Texturizer, Stabilizer, Thickener, Others), By Application (Food Additive, Pharmaceutical Ingredient, Resins, Coatings, Detergents, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2025-2034

- Published date: October 2025

- Report ID: 162066

- Number of Pages: 252

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

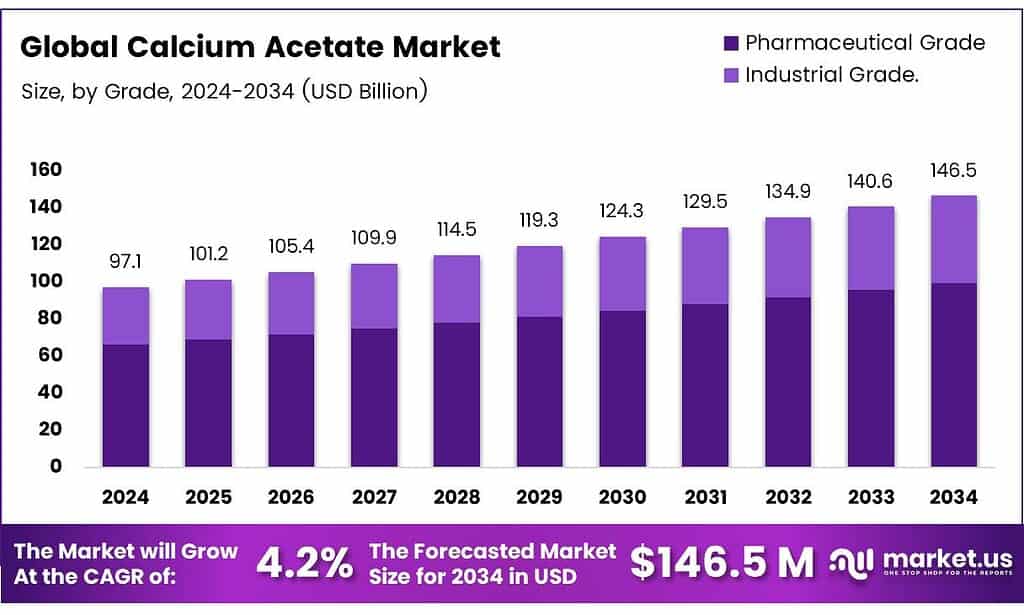

The Global Calcium Acetate Market size is expected to be worth around USD 146.5 Million by 2034, from USD 97.1 Million in 2024, growing at a CAGR of 4.2% during the forecast period from 2025 to 2034.

Calcium acetate, the calcium salt of acetic acid, is commonly used as a hydrate to treat hyperphosphatemia (elevated blood phosphate levels) in patients with kidney disease. The calcium ions bind dietary phosphate to form insoluble calcium phosphate, which is excreted in feces. It functions as a chelator and contains an acetate group.

Calcium carbonate and calcium acetate are widely used phosphate-binding agents with comparable efficacy. However, calcium acetate contains less elemental calcium (325 mg vs. 500 mg per dose) compared to calcium carbonate. Exclusive use of calcium-containing phosphate binders in dialysis patients may lead to hypercalcemia, particularly when combined with vitamin D sterols.

- High doses of calcium have been linked to soft tissue and vascular calcification in long-term dialysis patients and may increase the risk of calciphylaxis. The K/DOQI guidelines recommend limiting elemental calcium intake to 1500 mg/day, with an additional 500 mg from dietary sources, capping total intake at 2000 mg/day. This restriction often limits the use of calcium-based binders for adequate phosphate control.

Calcium acetate, with 25% elemental calcium, is effective across a broad intestinal pH range, while calcium carbonate, with 40% elemental calcium, is less effective at alkaline pH (e.g., in patients using H2 blockers or PPIs). Although guidelines suggest a 1500 mg/day calcium intake limit (plus 500 mg from diet), supporting data are limited.

- Compared to calcium-containing binders, calcium-free phosphate binders are associated with a 22% reduction in all-cause mortality (risk ratio 0.78, 95% CI 0.61–0.98). The calcium content varies significantly among compounds: calcium gluconate (9%), calcium carbonate (40%), and calcium oxide (71%) by weight. Solubility also varies, with calcium carbonate being relatively insoluble at neutral pH, while calcium acetate and calcium chloride are highly soluble.

Key Takeaways

- The Global Calcium Acetate Market is projected to grow from USD 97.1 million in 2024 to USD 146.5 million by 2034, at a CAGR of 4.2%.

- Pharmaceutical Grade captured 83.9% of the market in 2024, driven by its use as a phosphate binder and excipient in drug formulations.

- Firming Agent held a 36.3% market share in 2024, fueled by its role in maintaining texture in processed foods.

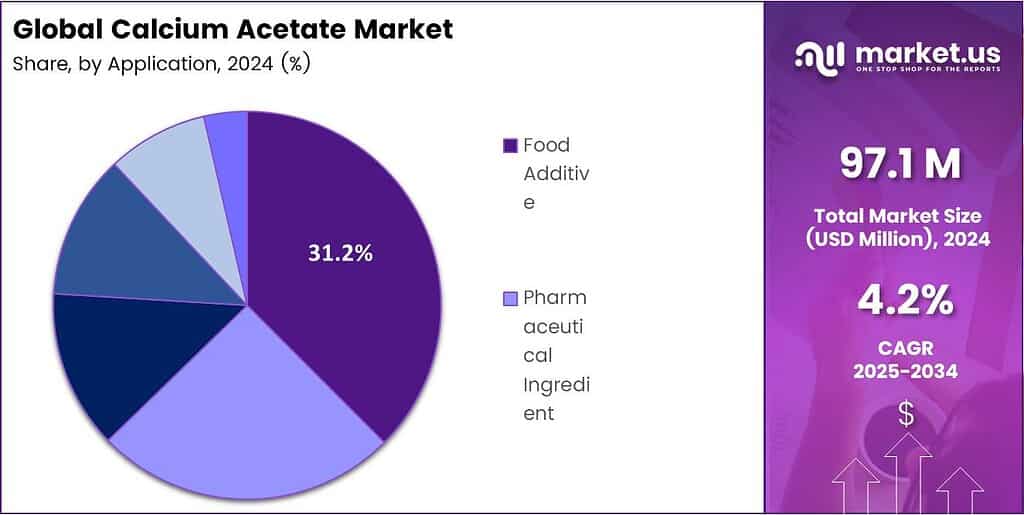

- Food additives accounted for 31.2% of the market in 2024, valued for stabilizing and preserving food quality.

- North America led with a 37.5% share in 2024 (USD 36.4 million), driven by its robust pharmaceutical sector and CKD treatment demand.

By Grade

Pharmaceutical Grade Leads with 83.9% Market Share

In 2024, Pharmaceutical Grade held a dominant market position in the global Calcium Acetate Market, capturing more than 83.9% share. This segment’s leadership is driven by its widespread use as a phosphate binder in patients with chronic kidney disease and as a key excipient in tablet formulations. High purity, consistent performance.

The growing demand for effective calcium supplements and phosphate management therapies has further strengthened its consumption. The demand for pharmaceutical-grade calcium acetate is expected to rise steadily as global healthcare systems expand their focus on renal health and mineral metabolism management.

Rising approvals of calcium-based formulations by regulatory authorities and the expansion of pharmaceutical manufacturing capacities in Asia-Pacific and North America are reinforcing this growth trajectory. The increasing adoption of pharmaceutical-grade calcium acetate in nutraceutical applications is broadening its end-use potential, ensuring that this segment continues to dominate the overall market landscape in the coming years.

By Function

Firming Agent Dominates with 36.3% Market Share

In 2024, Firming Agent held a dominant market position in the global Calcium Acetate Market, capturing more than a 36.3% share. Its growing usage in the food and beverage industry has been a key factor driving this dominance. Calcium acetate is widely used to maintain the firmness and texture of processed fruits, vegetables, and baked goods, ensuring product stability and extended shelf life.

The rising demand for packaged and ready-to-eat food products, particularly in urban regions, has significantly boosted their consumption as a firming additive. The segment is expected to maintain its strong position due to increasing food processing activities and consumer preference for high-quality, stable food textures.

Food manufacturers are increasingly relying on calcium acetate as a multifunctional ingredient that not only enhances firmness but also supports pH regulation and preservation. With stricter food safety standards and growing applications in dairy and confectionery products, the Firming Agent segment is set to remain a leading contributor to the overall market expansion.

By Application

Food Additive Leads with 31.2% Market Share

In 2024, Food Additive held a dominant market position in the global Calcium Acetate Market, capturing more than a 31.2% share. Its strong presence is driven by increasing use in the food and beverage industry as a stabilizer, buffer, and preservative. Calcium acetate plays a vital role in maintaining food quality by regulating acidity, preventing spoilage, and enhancing texture.

It is commonly used in baked goods, dairy items, and confectionery to improve product consistency and extend shelf life, making it a preferred additive for large-scale food producers. The Food Additive segment is expected to witness steady growth as consumer demand for processed and convenience foods continues to expand globally.

The rising shift toward clean-label and safer food ingredients is also encouraging manufacturers to use calcium-based additives due to their natural origin and recognized safety profile. The growing regulatory approvals for calcium acetate in food applications across North America, Europe, and the Asia-Pacific are anticipated to sustain its market dominance.

Key Market Segments

By Grade

- Pharmaceutical Grade

- Industrial Grade

By Function

- Firming Agent

- Texturizer

- Stabilizer

- Thickener

- Others

By Application

- Food Additive

- Pharmaceutical Ingredient

- Resins

- Coatings

- Detergents

- Others

Emerging Trends

Rising Demand for Clean-Label and Functional Food Applications of Calcium Acetate

An important emerging trend in the use of Calcium Acetate is growing adoption in the food and beverage industry as a clean-label ingredient and calcium-fortifier. Consumers are increasingly looking for simpler ingredient lists, higher nutrient content, and minimal synthetic additives—this is opening up space for calcium acetate to be used not just as a preservative or texture regulator but as a value-adding source of dietary calcium.

- Calcium acetate can be added to high-calcium milk, certain fruit juices, or bakery products to enhance their nutritional appeal. From a regulatory standpoint, this is bolstered by the fact that the United States Food and Drug Administration (FDA) allows calcium acetate to be used at specified levels in baked goods (at up to 0.2% in baked goods and up to 0.15% in sweet sauces/toppings) under its GRAS (Generally Recognized as Safe) framework.

In terms of volumes, one industry analysis estimated that the global calcium acetate market was approximately 110 thousand tonnes in 2023, with the food & beverage sector growing as one of the largest end-use segments. As manufacturers launch more fortified, clean-label, and texture-improved food innovations, the demand for calcium acetate as a functional food ingredient is set to accelerate.

Drivers

Growth in Chronic Kidney Disease Increasing Demand for Calcium Acetate

- One of the strongest drivers behind the rising demand for Calcium Acetate is the growing global incidence of Chronic Kidney Disease (CKD), which increases the need for phosphate-binders and allied therapies. In the United States alone, about 14% of adults — roughly 35.5 million people — are estimated to have CKD. Globally, reports suggest that more than 700 million people are living with CKD.

When kidneys fail to properly filter phosphate, elevated blood phosphate becomes a serious risk, particularly in dialysis patients. Calcium acetate is used as a phosphate binder in such cases, binding dietary phosphate in the gut and preventing its absorption. The increasing number of people with kidney disease, plus higher survival rates of patients on dialysis, directly boosts demand for formulations containing calcium acetate.

In addition to the pure prevalence numbers, government health programmes and clinical guidelines are emphasising early diagnosis and management of kidney disease. For example, the global focus on kidney health as a non-communicable disease means that therapies which control complications — such as phosphate binding — are seeing broader uptake. This regulatory and healthcare framework strengthens the position of calcium acetate as a go-to compound for treatment.

Restraints

Hypercalcemia risk limits the widespread use of calcium acetate

Calcium acetate’s clinical use is limited by the risk of hypercalcemia, with 16% of patients in a three-month study experiencing serum calcium levels above 11 mg/dL, as per U.S. FDA labeling. This often necessitates dose reductions or discontinuation, requiring regular monitoring of serum calcium and calcium-phosphorus product. Such monitoring increases costs and care burden for patients with chronic kidney disease (CKD).

Global kidney-care guidelines, such as the KDIGO update, recommend restricting calcium-based phosphate binders in CKD patients due to risks of calcium loading, vascular calcification, and hypercalcemia. These guidelines urge clinicians to individualize therapy and avoid elevating serum calcium in at-risk patients. This narrows the eligible patient population for calcium acetate.

Comparative data further challenge calcium acetate’s safety profile, with a meta-analysis showing sevelamer has significantly lower hypercalcemia rates risk ratios of 0.44 and 0.24 for different thresholds. This leads to fewer dose interruptions and lab abnormalities compared to calcium-based binders. As payers and providers prioritize outcomes and safety, these findings reduce calcium acetate’s uptake.

Opportunity

Rising Incidence of Hyperphosphatemia in Chronic Kidney Disease Patients

One of the strongest growth drivers for the use of calcium acetate is the increasing prevalence of hyperphosphatemia among patients with chronic kidney disease (CKD). Studies indicate that between 50% and 74% of CKD patients develop elevated serum phosphorus levels as their renal function declines. It contributes to complications like bone mineral disorders, vascular calcification, and cardiovascular disease — so managing phosphate safely becomes critical.

Because Calcium Acetate acts as an effective oral phosphate-binder, its demand is being pulled upward by the growing need to control phosphate in this patient group. For example, as more health systems acknowledge the dangers of hyperphosphatemia in CKD and payers support early intervention, this creates more opportunities for calcium acetate-based therapies.

In parallel, many governments and public health agencies are pushing for improved kidney health screening and early treatment. As awareness grows and more patients are diagnosed with CKD and related disorders, the pool of individuals who may require phosphate-binding therapy grows too, thus favouring growth in calcium acetate consumption. Although alternative binders exist, calcium acetate remains widely used due to its relative cost-effectiveness and experience in the field.

Regional Analysis

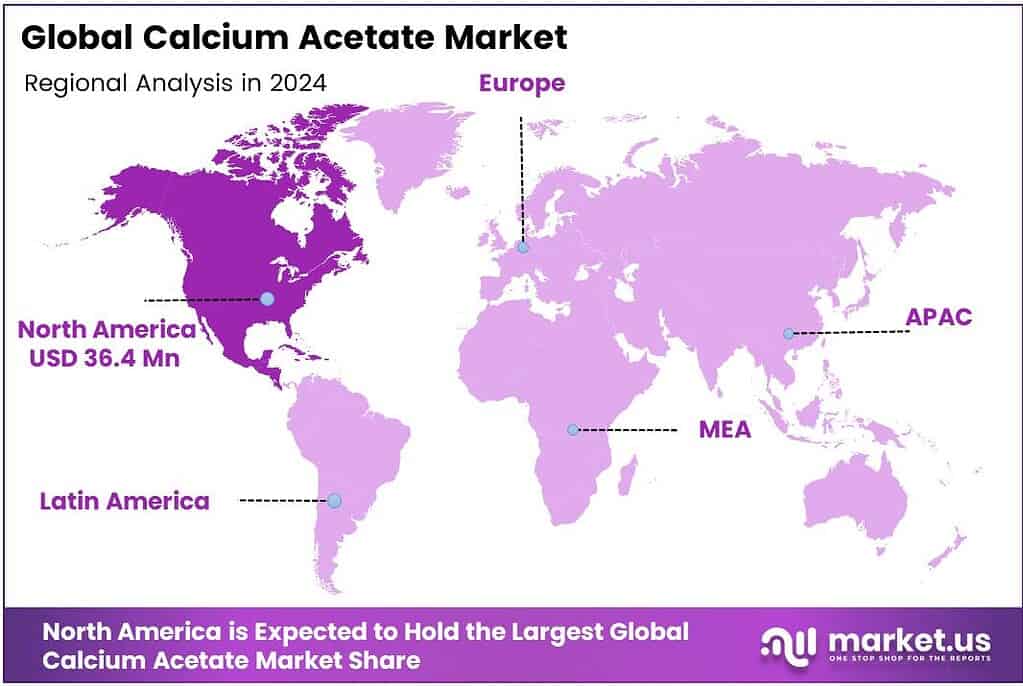

North America leads with a 37.5% share and a USD 36.4 Million market value.

In 2024, North America held a dominant position in the global Calcium Acetate Market, accounting for more than 37.5% of the market share, equivalent to approximately USD 36.4 million. This leadership is largely attributed to the region’s well-established pharmaceutical sector and strong demand for calcium acetate as a phosphate binder in the treatment of chronic kidney disease (CKD).

The United States, with its high prevalence of CKD and supportive healthcare policies, remains the primary consumer. According to the Centers for Disease Control and Prevention (CDC), nearly 35 million Americans are affected by CKD, directly influencing the consumption of calcium-based phosphate binders across the country.

The region’s advanced food processing industry has further strengthened the adoption of calcium acetate as a firming agent and food additive in bakery, dairy, and confectionery products. Regulatory approvals from agencies such as the U.S. Food and Drug Administration (FDA) for its use in both pharmaceutical and food formulations have provided a strong foundation for growth.

The market is projected to expand steadily as healthcare expenditure rises and manufacturers focus on producing high-purity, pharmaceutical-grade calcium acetate domestically. The growing awareness of dietary calcium supplementation and the shift toward fortified and clean-label food products also contribute to sustained regional demand. North America is expected to maintain its dominance throughout the forecast period.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Niacet is a globally recognized leader, renowned for its high-purity specialty salts. As a subsidiary of Niacet Corporation, it leverages strong technical expertise and significant production capacity to serve diverse industries, including pharmaceuticals and food. Its strategic focus on innovation and stringent quality control solidifies its position as a key supplier in the global calcium acetate market, often setting industry standards for product consistency and reliability for industrial and specialty applications.

Macco Organiques Inc. is a prominent North American producer with a long-standing reputation. The company specializes in the manufacturing of high-purity acetate esters and salts, with calcium acetate being a core product. Its strategic focus on the food, pharmaceutical, and industrial sectors, combined with a commitment to consistent quality and customer-centric supply chains, establishes it as a reliable and essential partner for clients across the continent and in select international markets.

The Akshay Group is a significant and rapidly growing player in the chemical sector, based in India. It capitalizes on cost-effective manufacturing and a strong distribution network, particularly within the Asia-Pacific region. The company supplies calcium acetate primarily for industrial applications, including water treatment and chemical synthesis. Its competitive pricing and agility in serving emerging markets make it a formidable and increasingly influential contender in the global calcium acetate supply chain.

Top Key Players in the Market

- Niacet

- Macco Organiques

- Akshay Group

- Amsyn

- Daito Chemical

- Plater Group

- Jiangsu Kolod Food

- Wuxi Yangshan Biochemical

- Tengzhou Zhongzheng Chemical

- Alemark

Recent Developments

- In 2024, Niacet divested its sodium diacetate business to Jungbunzlauer Ladenburg, a Swiss-Austrian firm specializing in fermentation-based ingredients. This move allows Niacet to streamline operations and potentially redirect resources toward core products like calcium acetate, which remains a key offering for phosphate binding in dialysis solutions.

- In 2024, Macco Organiques participated in Food Ingredients Europe (FiE) in Frankfurt, Germany, showcasing its mineral ingredients portfolio, including calcium acetate innovations for the food and pharma sectors. The event highlighted sustainable sourcing and high-purity formulations to meet EU regulatory standards for food additives.

Report Scope

Report Features Description Market Value (2024) USD 97.1 Million Forecast Revenue (2034) USD 146.5 Million CAGR (2025-2034) 4.2% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Grade (Pharmaceutical Grade, Industrial Grade), By Function (Firming Agent, Texturizer, Stabilizer, Thickener, Others), By Application (Food Additive, Pharmaceutical Ingredient, Resins, Coatings, Detergents, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape Niacet, Macco Organiques, Akshay Group, Amsyn, Daito Chemical, Plater Group, Jiangsu Kolod Food, Wuxi Yangshan Biochemical, Tengzhou Zhongzheng Chemical, Alemark Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- Niacet

- Macco Organiques

- Akshay Group

- Amsyn

- Daito Chemical

- Plater Group

- Jiangsu Kolod Food

- Wuxi Yangshan Biochemical

- Tengzhou Zhongzheng Chemical

- Alemark

Our Clients

- 162066

- October 2025