Quick Navigation

Report Overview

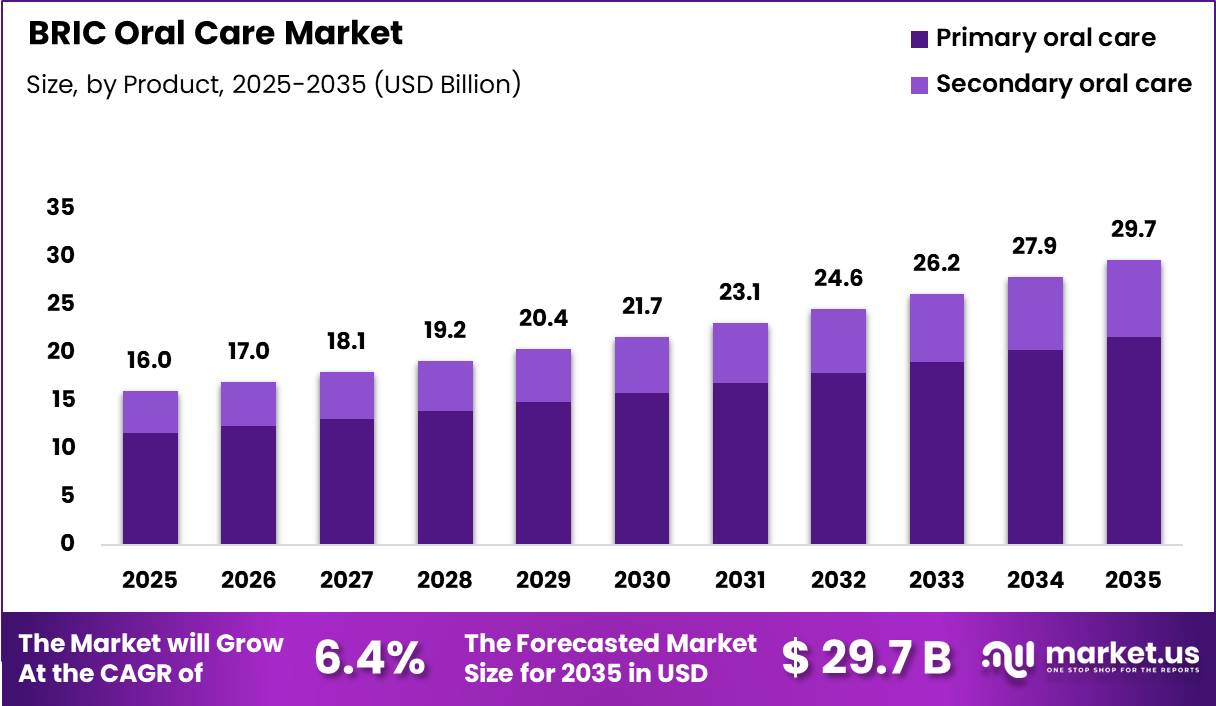

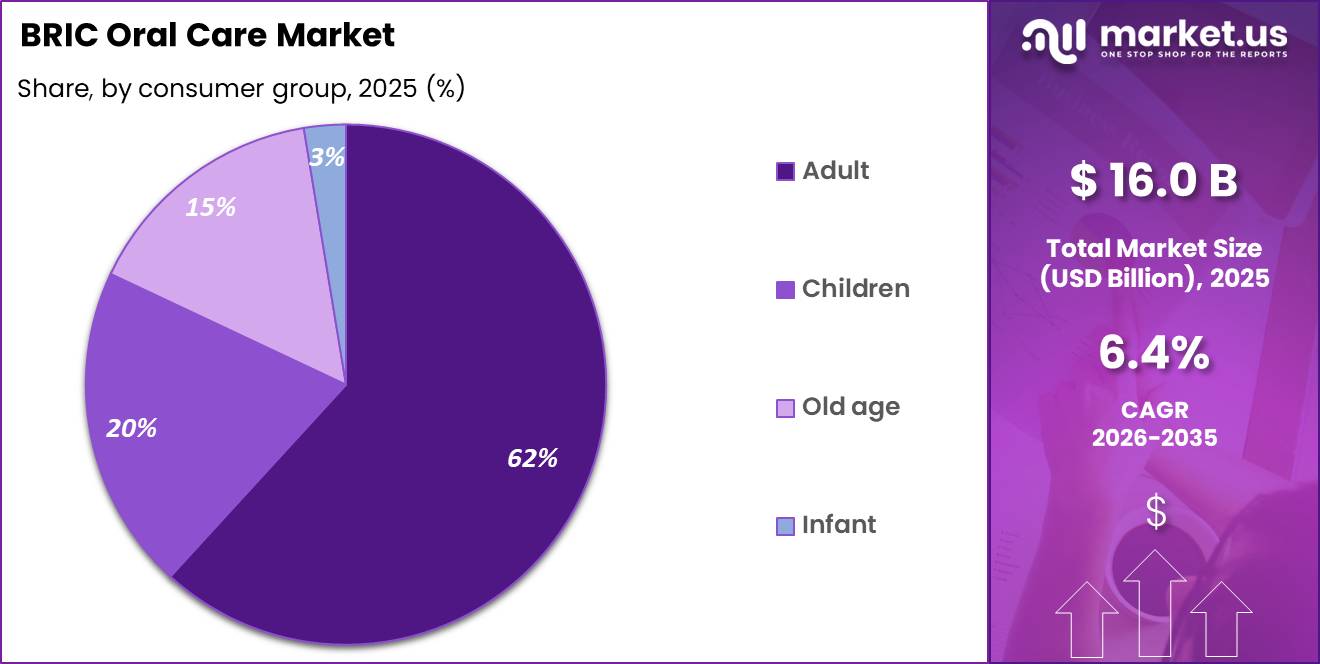

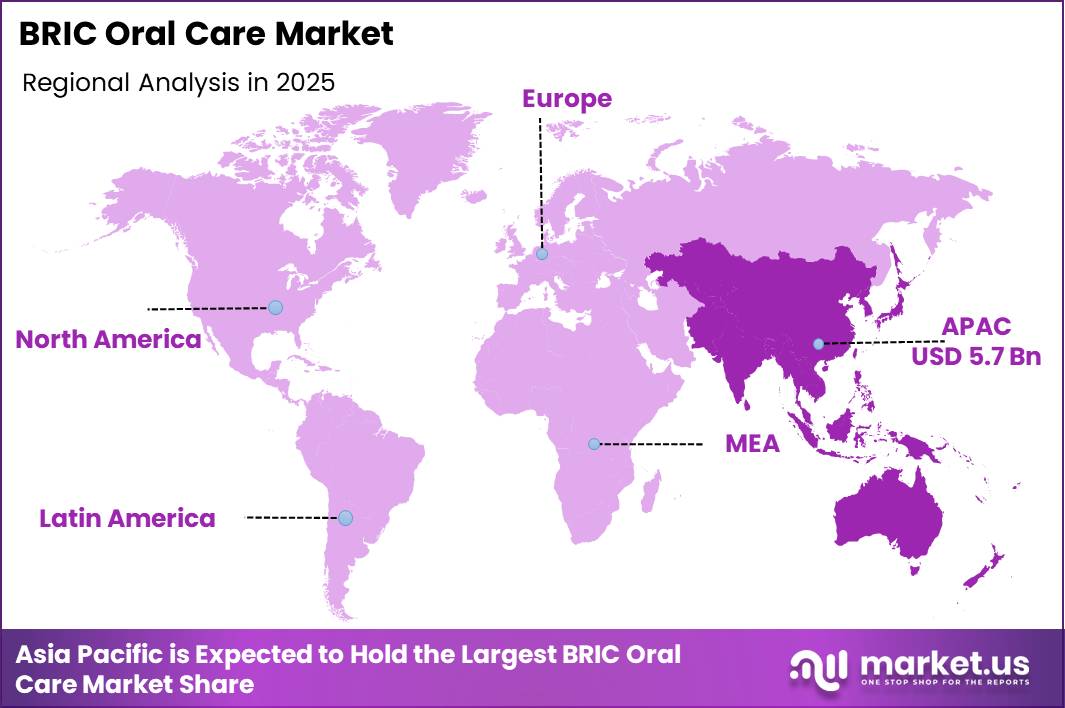

Global BRIC Oral Care Market size is expected to be worth around US$ 29.7 Billion by 2035 from US$ 16.0 Billion in 2025, growing at a CAGR of 6.4% during the forecast period from 2026 to 2035. In 2025, Asia Pacific led the market, achieving over 35.8% share with a revenue of US$ 5.7 Billion.

The Global BRIC Oral Care market can be termed as a healthcare segment which involves the manufacture of consumer health care goods such as toothpaste, toothbrush, mouth wash, and other accessories for oral hygiene in the regions of Brazil, Russia, India, and China. There has been an increased involvement by the government in raising awareness about oral care through various programs conducted in BRIC nations.

The Global BRIC Oral Care market is growing due to the rising prevalence of oral diseases, increasing awareness of preventive healthcare, and stronger consumer interest in cosmetic dental health. As consumers become more conscious of maintaining oral hygiene, demand for premium and therapeutic oral care products continues to increase across Brazil, Russia, India, and China.

The expanding middle-class population and rising disposable incomes in these countries are further encouraging spending on high-quality oral care solutions. However, market growth is restrained by limited access to dental services in rural and low-income areas, reducing the adoption of preventive oral care products and regular dental care practices.

- In 2025, Oral diseases are estimated to affect approximately 3.5 billion people worldwide, with a global prevalence of 45%, and BRIC nations carrying a disproportionately high share of this burden, as highlighted in the WHO Global Oral Health Action Plan 2023–2030.

Personalized oral health devices that utilize artificial intelligence and toothbrush technology have started to be incorporated within the routine oral hygiene practices of consumers, making oral hygiene products more engaging and ensuring better compliance in treatment. According to World Health Organization in year 2024, The total annual global expenditures for public and private oral health have hit an estimated value of US$387 billion per year.

The rapid digital transformation of distribution channels, particularly the shift toward specialized e-commerce platforms and quick-commerce delivery services, is profoundly reshaping product accessibility across the BRIC nations. While brick-and-mortar retail remains dominant in suburban zones, online marketplaces have allowed premium oral care brands to bypass traditional supply chain bottlenecks and directly target urban consumers.

This digital expansion is further propelled by hyper-localized marketing campaigns on social media, where dental professionals and influencers educate the growing middle class on the benefits of advanced regimens like multi-step whitening and tartar-control rinsing. Consequently, manufacturers are heavily investing in region-specific product formulations such as herbal or charcoal-infused toothpastes tailored to cultural preferences in India and China to secure brand loyalty in an increasingly competitive and receptive consumer landscape.

Key Takeaways

- Market Size: Global BRIC Oral Care Market size is expected to be worth around US$ 29.7 Billion by 2035 from US$ 16.0 Billion in 2025

- Market Share: The market is growing at a CAGR of 6.4% during the forecast period from 2026 to 2035.

- Product Analysis: Primary oral care products are identified as the dominant product category, accounting for 72.8% of the market in 2025, driven by high toothpaste and toothbrush penetration across all four BRIC economies.

- Consumer Group Analysis: Adults represent the largest consumer group at 61.8%, anchored by high product usage frequency and expanding premium oral care adoption among working-age populations.

- Distribution Channel Analysis: Supermarkets and hypermarkets are confirmed as the dominant distribution channel at 49.9%, supported by wide product availability and competitive pricing across mass retail formats.

- Regional Anlaysis: Asia Pacific leads regional demand at 35.8%, driven by China’s and India’s large consumer bases and rising oral health awareness.

Product Analysis

Primary oral care represents dominant Segment in the Market.

Primary oral care represents the dominant segment in the BRIC Oral Care market, accounting for 72.8% share owing to the basic importance of toothpaste and toothbrushes within everyday oral care procedures among all four BRIC countries. Toothpaste is the leading sub-category by sales volumes thanks to mass and value brands available at supermarkets and pharmacies in affordable pricing options.

For example, Colgate-Palmolive was holding an overall toothpaste market share equal to 41.1% year-to-date in Q1 2026 and an even higher share of manual toothbrushes equal to 32.6% an advantage stemming from the fact that the Colgate brand is known to virtually all BRIC consumers.

The use of power toothbrushes and artificial intelligence (AI) enabled smart oral care devices is one of the minor secondary oral care products and trending segment. The use of AI and real-time plaque removal smart toothbrushing systems will be commercially available at moderate pricing levels targeting Chinese and Brazilian urban consumers.

The availability of consumer electronic infrastructure, smartphone connectivity, affordability of products, and willingness of consumers to spend on preventive oral health care are some of the key factors driving adoption of smart oral care devices.

Consumer Group Analysis

BRIC Oral Care Are the Most Widely Used by Adults.

Adults accounting for 61.8% market share of the BRIC oral care market, represents the dominant material segment. This dominance is because of their high rate of usage of products, wide-ranging category involvement, and large proportion of total population in the BRIC countries.

The working age adult population of China and India, the two biggest BRIC markets, form the driving force behind the consumption of premium toothpaste, mouthwashes, and whitening products. Oral diseases have a heavy incidence among adults’ severe periodontal disease is common.

The high usage rates, premiumization trends amongst urban adult populations, and growing awareness of its health implications are some of the main factors influencing this dominance by adult consumer groups.

The fastest growing consumer segment is that of the children’s oral care market. Growing parental awareness about the importance of oral hygiene among children, the introduction of school oral health programs in BRIC countries, as well as the increased availability of children’s specific products, including fluoride toothpaste and soft bristled tooth brushes, is fueling growth in the market.

The WHO’s Global Oral Health Action Plan 2023-2030 emphasizes the reduction in childhood dental caries making this a supportive policy environment for children’s oral care products in BRIC countries.

Distribution Channel Analysis

BRIC Oral Care Are Mostly Utilized in the Supermarkets & hypermarkets Sector.

The Supermarkets & hypermarkets, accounting for 49.9% of the BRIC Oral Care market, remains the dominant distribution channel category as a result of the superior standing that they hold within the consumer products supermarkets and hypermarkets within all the BRIC countries, together with the extensive range of oral care products available within the economy at competitive prices.

Large-format retailing includes the operations of Walmart stores in Brazil, X5 Group stores in Russia, as well as hypermarket chains located in major Chinese urban centers that have the ability to sell substantial amounts of oral care products.

Online retail is emerging as the fastest-growing distribution channel in the BRIC oral care market, supported by the strong expansion of e-commerce ecosystems across key countries. In China, platforms such as Alibaba’s Tmall and JD.com continue to drive large-scale digital sales, while India is witnessing rapid growth in quick commerce and mobile-based retail. Brazil is also steadily increasing its online FMCG adoption, with rising smartphone usage in Tier 2 and Tier 3 cities expected to further accelerate digital penetration in oral care distribution.

Key Market Segments

By Product

- Primary oral care

- Secondary oral care

By Consumer group

- Adult

- Children

- Old age

- Infant

By Distribution Channel

- Supermarkets & hypermarkets

- Pharmacies & drug stores

- Convenience / department stores

- Online retail

- Other channels

Driver

Preventive Oral Health Push Expanding Daily-Use Categories

Oral health is increasingly being positioned as a preventive, habit-based care area rather than episodic treatment, supporting steady growth in daily-use products like toothpaste, mouthwash, floss, and children’s oral-care lines. The World Health Organization estimates that oral diseases affect nearly 3.7 billion people globally and emphasizes that most are preventable through routine hygiene, including twice-daily brushing with fluoride toothpaste.

Recent WHO guidance (2026) reinforces prevention and primary-care integration, strengthening policy support for routine oral hygiene adoption. Public health campaigns such as World Oral Health Day further sustain awareness and encourage regular behavior change, particularly in high-population emerging markets.

Country-level programs, including India’s National Oral Health Programme, are also expanding access and awareness through public facilities and education initiatives, helping convert first-time users and increase brushing frequency. Overall, this shift supports stronger, more stable demand growth in preventive oral-care categories, especially in India, Brazil, and urban China.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Preventive oral-health push expands daily-use categories | +1.4% | India core, Brazil core, China urban, Russia metro spill-over | Short term |

| Fluoride, safety, and toothpaste-rule tightening upgrades value mix | +1.1% | China core, Brazil regulated base, India formal sector | Medium term |

| Sugar-linked caries burden lifts therapeutic and specialist demand | +1.3% | India core, Brazil core, China mass market, Russia selective | Medium term |

| Primary-care integration improves entry-level product penetration | +0.9% | Brazil core, India core, Russia public-channel selective | Medium term |

| Premiumization through herbal, sensitivity, and adjunct formats | +1.6% | China core, India core, Brazil urban, Russia affluent urban | Short term |

| E-commerce and digital discovery accelerate portfolio trading-up | +1.2% | China core, India urban-rural bridge, Brazil urban, Russia large cities | Short term |

Challenge

Uneven Oral Health Infrastructure Constraining BRIC Market Growth

Uneven distribution of oral health infrastructure across BRIC economies limits the conversion of high disease prevalence into consistent product usage, despite an estimated 3.7 billion people affected globally. In countries such as India and Brazil, dentist to population ratios of roughly 1 to 9,000 to 1 to 15,000 are significantly below developed market levels, constraining routine care delivery and extending wait times that disrupt continuity of treatment.

In rural China and inland regions of Brazil, clinic density gaps of 40 to 60 % versus urban centers mean a large share of the population relies on irregular outreach or self medication, reducing uptake of preventive and higher value oral care products. This leads to lower penetration of premium toothpaste, mouthwash, and interdental care products even as income levels gradually rise.

For manufacturers, this infrastructure gap shifts strategy toward low margin sachets, mobile dental campaigns, and school based programs, diverting marketing spend away from brand building toward access expansion. Retail penetration also remains uneven, with underserved areas carrying 20 to 30 % smaller oral care assortments.

Overall, closing these gaps requires sustained public investment and integration of oral health into primary care systems. Without it, infrastructure constraints are estimated to reduce potential oral care market CAGR by approximately 1.4 % points over the medium term in BRIC markets.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Uneven oral health infrastructure | -1.4% | Brazil, India, rural China | Long term (≥ 4 years) |

| Low preventive behaviour adherence | -1.1% | All BRIC urban–rural mix | Medium term (2–4 years) |

| Fragmented regulatory & quality regimes | -0.8% | Brazil, India, Russia | Medium term (2–4 years) |

| Supply chain cost & cold-chain gaps | -0.9% | Brazil inland, India tier-2/3, Russia regions | Long term (≥ 4 years) |

| Skilled dental workforce & channel capacity | -0.7% | India, Brazil, Russia public systems | Long term (≥ 4 years) |

| Digital engagement and data scarcity | -0.6% | BRIC mass-market segments | Short term (≤ 2 years) |

Restraints

Underfunded Public Oral Care Limiting BRIC Market Value Expansion

Underfunded public oral health systems across BRIC economies limit the conversion of high disease prevalence into structured, high value oral care consumption. Despite oral diseases affecting roughly 3.5 to 3.7 billion people globally, according to the World Health Organization, many low and middle income countries lack adequate preventive and treatment coverage, with particularly weak access in parts of India, Brazil, and rural China.

In these settings, limited dentist availability and inconsistent public dental programs reduce early diagnosis and professional recommendation of higher margin products such as sensitivity treatments, therapeutic mouthrinses, and prescription strength toothpaste.

As a result, a large share of consumers remain in low engagement, self care pathways, relying primarily on basic toothpaste and sporadic treatment.This weak clinical linkage suppresses conversion rates into premium oral care categories and slows adoption of innovative SKUs, keeping per capita spending lower despite high underlying disease burden.

The market therefore remains skewed toward low cost, high volume products, constraining margin expansion and delaying category premiumization.Overall, underfunded public oral care systems act as a structural brake on growth and mix shift, limiting value capture in BRIC markets and reinforcing reliance on mass market oral care formats rather than clinically driven, high value segments.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Underfunded public oral care & low clinical access | -2.0% | Brazil, India, rural China, Russia tier-2/3 | Long term (≥ 4 years) |

| High sugar consumption & weak SSB taxation | -1.8% | Brazil, Russia, India, urban China | Medium term (2–4 years) |

| Regulatory fragmentation on fluoride & claims | -1.4% | All BRIC, stronger in Brazil & Russia | Medium term (2–4 years) |

| Supply chain volatility in key ingredients & packaging | -1.6% | All BRIC, import-reliant nodes | Short–Medium term (≤ 4 years) |

| Price sensitivity & informal competition | -1.5% | India, Brazil, low-income China & Russia | Long term (≥ 4 years) |

| Low consumer adherence to preventive routines | -1.2% | All BRIC, strongest in rural belts | Long term (≥ 4 years) |

Opportunity

Rural Essential Oral Care Inclusion Driving BRIC Demand Expansion

Rural and low income households across BRIC markets remain underpenetrated in basic oral care despite rising national consumption trends. In countries such as India and Brazil, a significant share of rural populations still report inconsistent brushing habits and limited awareness of fluoride benefits, leaving a large addressable base for essential oral care expansion.While urban demand is increasingly driven by premiumization, rural segments represent an untapped volume opportunity.

Current per capita oral care spending in these areas remains significantly below urban levels, but even partial convergence through low cost formats such as sachet toothpaste, low priced brushes, and micro distribution channels could materially expand category penetration.Inclusive product strategies focused on affordability and accessibility, combined with rural distribution networks and public health campaigns, could add meaningful incremental volume growth.

By bridging part of the rural urban spending gap, manufacturers could unlock a multi billion dollar incremental market across BRIC economies.Overall, rural inclusion strategies shift growth from premium mix expansion toward penetration led volume gains, supporting a potential approximately 2.0 % point uplift in long term CAGR while strengthening baseline category resilience.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Rural essential oral care inclusion | +2.0% | India, Brazil, inland China | Medium term (2-4 years) |

| Integrated oral health & NCD prevention platforms | +1.8% | BRIC urban & peri-urban | Medium term (2-4 years) |

| Premium whitening & cosmeticization wave 2.0 | +1.5% | Brazil, China, urban India | Short term (≤ 2 years) |

| Senior-focused oral wellness & prosthetic care | +1.3% | Russia, China, Brazil | Long term (≥ 4 years) |

| Digital oral care ecosystems & smart devices | +1.2% | Tier-1/2 BRIC cities | Medium term (2-4 years) |

| Baby, kids & maternal oral care platforms | +1.0% | India, Brazil, China | Long term (≥ 4 years) |

Geopolitical Impact Analysis

Trade Disputes between U.S. and China and Pressure on Regional Supply Chains Have Generated Cost and Market Entry Issues for the BRIC Oral Care Industry

Escalating U.S.-China trade tensions and broader global tariff pressures are introducing cost headwinds across the BRIC oral care supply chain. Raw material inputs including specialty surfactants, fluoride compounds, packaging materials, and active whitening agents are sourced across international supply chains exposed to tariff escalation. For multinational oral care manufacturers with manufacturing bases across BRIC nations, tariff-related input cost inflation is compressing gross margins and complicating multi-country pricing strategies.

The continued geopolitical isolation faced by Russia post-Ukraine invasion has created unique access issues for the BRIC countries’ markets. Several western brands of oral care products have either scaled down their presence in the Russian market or undergone some strategic restructuring, presenting a good opportunity for both domestic and Asian brands, yet causing some disruptions in their supply chains.

In March 2026, Colgate-Palmolive announced that it would align itself with the new regionally reportable segment by placing Russia and Belarus in its Asia Pacific region from its Africa/Eurasia region. These factors notwithstanding, structural issues related to oral diseases coupled with increased consumer health consciousness should sustain demand for oral care products in BRIC nations.

Regional Analysis

Asia Pacific Held the Largest Share of the BRIC Oral Care Market.

In 2025, Asia Pacific dominated the BRIC Oral Care market, holding about 35.8% of total global consumption with revenue of US$ 5.7 billion. This dominance is primarily driven by China and India, which together form the largest consumer base in the region. China’s market is witnessing rapid premiumisation, strong growth in e-commerce channels, and rising competition between domestic premium brands and multinational companies.

India’s market is shaped by a mix of fluoride-based mass products and Ayurvedic oral care solutions, with companies such as Patanjali Ayurved and Dabur India competing alongside Colgate and Hindustan Unilever. WHO oral health data also highlights significant untreated dental disease burdens in both countries, supporting long-term demand for preventive oral care products.

Brazil is the most developed oral care market within the BRIC economies, supported by a large urban population, strong modern retail infrastructure, and increasing adoption of premium oral hygiene products among middle-class consumers. In Russia, geopolitical disruptions and reduced presence of Western brands have reshaped the market, creating opportunities for domestic and Asian manufacturers across pharmacy and retail channels.

North America, Europe, and the Middle East and Africa remain outside the core BRIC geographic scope but represent export and manufacturing reference markets for BRIC-based oral care producers. Across all BRIC regions, urban middle-class expansion, rising health literacy, and e-commerce development are expected to sustain oral care market growth through 2035.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

BRIC Oral Care Market is characterized by an oligopoly market that is consolidated at the head level but shows fragmentation at the tail end. There are three multinational corporations that dominate the market: Colgate-Palmolive, Procter & Gamble, and Unilever.

The multinationals capture the largest shelf space and volume share in the market through extensive distribution and large-scale advertising expenditure. Nevertheless, this consolidation has been facing stiff competition from emerging regional companies and direct-to-consumer brands in the market. The competitive edge is based on monopolistic competition due to product differentiation.

These competitive dynamics vary from one country to another. In Brazil, the country is still the most traditional and consolidated, although the local brands are catching up based on their focus on high-end whitening. The situation in Russia involves a transition from an oligopoly that favors western brands to a mixed oligopoly that sees a rapid rise of local brands such as Dental-S due to import substitution.

Finally, India and China represent the most fragmented markets, with India featuring its mass market divided by an Ayurvedic and herbal revolution, spearheaded by brands like Dabur and Patanjali, and China being highly competitive because of its online commerce market, which gives local brands such as Guangzhou Weimeizi an advantage over other players.

Top Key Players

- Colgate‑Palmolive Company

- The Procter & Gamble Company

- Unilever PLC

- Haleon plc

- Johnson & Johnson / Kenvue

- GlaxoSmithKline

- Church & Dwight Co., Inc.

- Koninklijke Philips N.V. (Sonicare and power brushes)

- LG Household & Health Care Ltd.

- Lion Corporation

- Sunstar Suisse SA (GUM)

- Dabur India Ltd.

- Hindustan Unilever Limited

- Patanjali Ayurved Limited

- Guangzhou Weimeizi Industrial Co. Ltd.

- Other Players

Key Development

- April, 2025 – Haleon announced the construction of a £130 million Global Oral Health Innovation Centre in Weybridge, United Kingdom. The new facility will strengthen research, product development, consumer testing, and clinical capabilities for flagship oral care brands including Sensodyne, Corsodyl, and Polident, supporting long-term innovation across international markets, including BRIC countries.

- April, 2025 – The company highlighted continued investment in oral care innovation, with its global toothpaste market share reaching 40.9% during the first quarter of 2025. The performance was supported by premium product launches and ongoing expansion of its preventive oral care portfolio.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 16.0 Billion |

| Forecast Revenue (2035) | US$ 29.7 Billion |

| CAGR (2026-2035) | 6.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Primary oral care, Secondary oral care), By Consumer group (Adult, Children, Old age, Infant), By Distribution Channel (Supermarkets & hypermarkets, Pharmacies & drug stores, Convenience / department stores, Online retail, Other channels) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Colgate‑Palmolive Company, The Procter & Gamble Company, Unilever PLC, Haleon plc, Johnson & Johnson / Kenvue, GlaxoSmithKline, Church & Dwight Co. Inc., Koninklijke Philips N.V. (Sonicare and power brushes), LG Household & Health Care Ltd., Lion Corporation, Sunstar Suisse SA (GUM), Dabur India Ltd., Hindustan Unilever Limited, Patanjali Ayurved Limited, Guangzhou Weimeizi Industrial Co. Ltd., Other Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |