Global Breathalyzers Market By Technology (Fuel cell, Semiconductor sensor, Infrared spectroscopy and Others), By Application (Drug abuse detection, Alcohol detection, Medical application and Others), By End-use (Law enforcement agencies, Enterprises, Individuals and Others), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: April 2026

- Report ID: 183534

- Number of Pages: 230

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

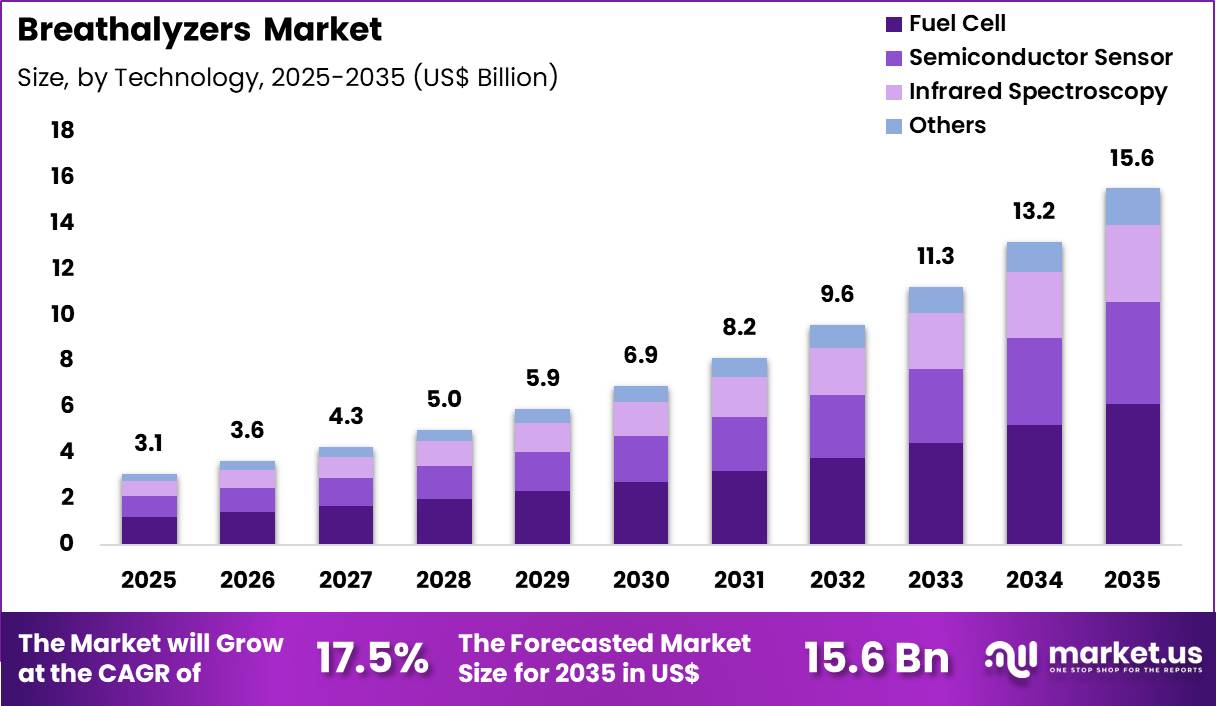

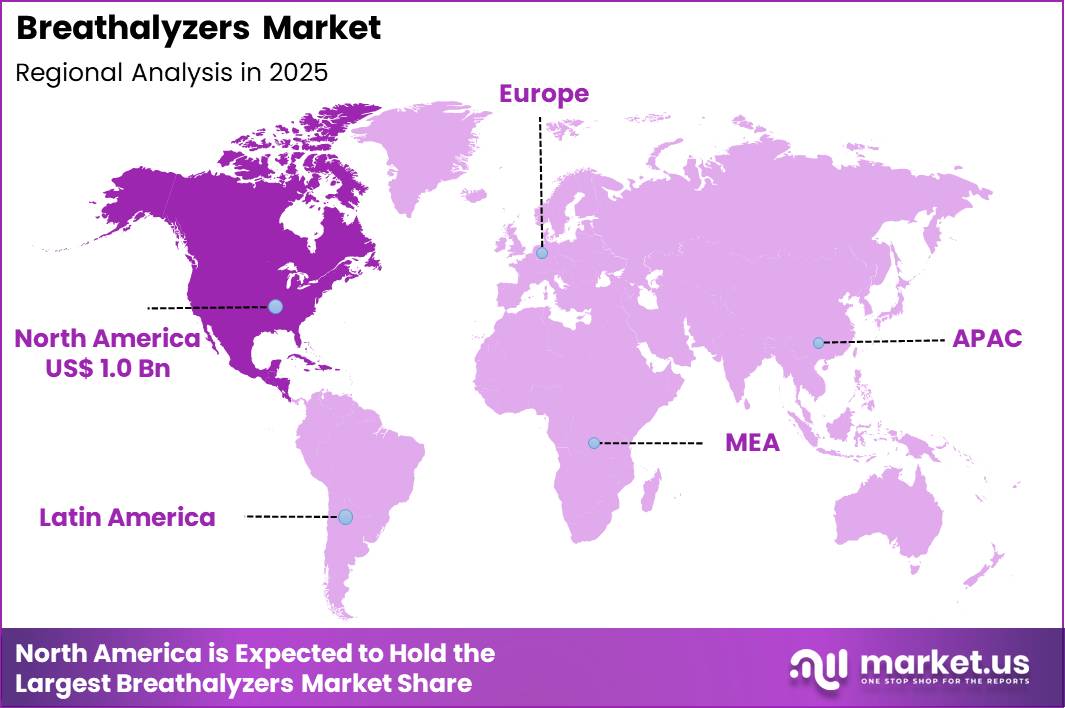

The Global Breathalyzers Market size is expected to be worth around US$ 15.6 Billion by 2035 from US$ 3.1 Billion in 2025, growing at a CAGR of 17.5% during the forecast period 2026-2035. In 2025, North Americaled the market, achieving over 32.6% share with a revenue of US$ 1.0 Billion.

Rising emphasis on non-invasive diagnostics and public safety measures accelerates the Breathalyzers market as healthcare providers and law enforcement agencies seek accurate, convenient tools for real-time assessment of alcohol levels and metabolic markers.

Law enforcement officers increasingly deploy evidential breathalyzers during roadside testing to measure blood alcohol concentration with high precision, supporting enforcement of driving-under-the-influence laws and reducing alcohol-related accidents.

These devices also serve workplace safety programs by enabling employers to conduct random or post-incident testing, ensuring compliance with occupational health standards in transportation, construction, and manufacturing sectors.

In clinical settings, breathalyzers assist emergency departments in evaluating intoxication levels in trauma or overdose cases, guiding rapid treatment decisions and distinguishing alcohol intoxication from other metabolic disturbances.

During 2025, breath-based diagnostics expanded into medical applications, highlighted by the introduction of the Isaac device developed through a collaboration led by Indiana University. The technology is designed to estimate blood glucose levels through breath analysis, offering a non-invasive alternative for diabetes monitoring.

Manufacturers pursue opportunities to integrate artificial intelligence and cloud connectivity into breathalyzer systems, expanding applications in continuous monitoring for alcohol use disorder treatment and remote patient management.

Developers advance portable, handheld units with automated calibration tracking and secure data logging, broadening utility in forensic toxicology and court-mandated monitoring programs. These enhancements support real-time data sharing with healthcare providers for patients undergoing substance abuse rehabilitation.

Opportunities emerge in multi-analyte breath analyzers capable of detecting additional biomarkers beyond alcohol, such as ketones or volatile organic compounds, for metabolic and respiratory condition screening.

Companies invest in user-friendly interfaces and tamper-proof designs to improve reliability in both medical and legal contexts. Entering 2026, manufacturers such as Drägerwerk and Intoximeters incorporated artificial intelligence capabilities into evidential breathalyzer systems.

These enhancements include automated calibration tracking and secure cloud-based monitoring features, supporting compliance requirements for legal and forensic use in several regions.

Recent trends emphasize non-invasive metabolic monitoring, AI-driven accuracy improvements, and seamless data integration, positioning breathalyzers as versatile tools in both public safety enforcement and clinical diagnostics.

Key Takeaways

- In 2025, the market generated a revenue of US$ 3.1 Billion, with a CAGR of 17.5%, and is expected to reach US$ 15.6 Billion by the year 2035.

- The technology segment is divided into fuel cell, semiconductor sensor, infrared spectroscopy and others, with fuel cell taking the lead with a market share of 39.5%.

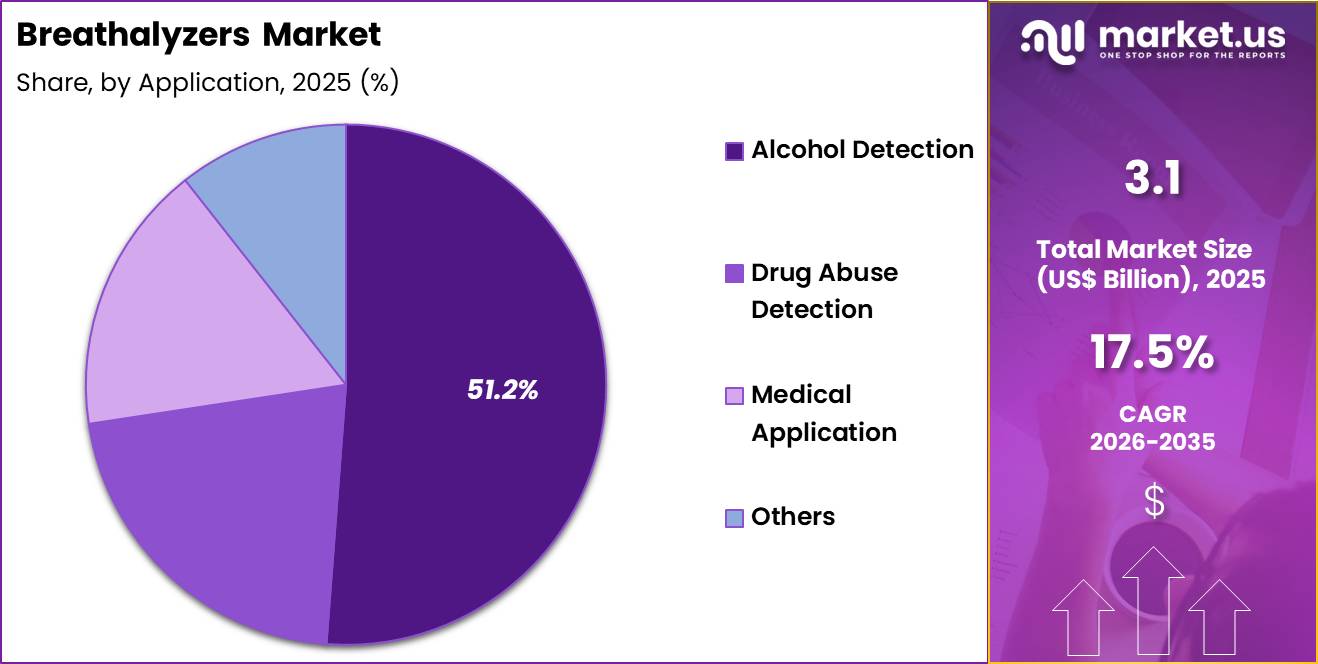

- Considering application, the market is divided into drug abuse detection, alcohol detection, medical application and others. Among these, alcohol detection held a significant share of 51.2%.

- Furthermore, concerning the end-use segment, the market is segregated into law enforcement agencies, enterprises, individuals and others. The law enforcement agencies sector stands out as the dominant player, holding the largest revenue share of 41.6% in the market.

- North America led the market by securing a market share of 32.6%.

Technology Analysis

Fuel cell technology accounted for 39.5% of growth within technology and dominates the breathalyzers market due to its high accuracy, reliability, and strong selectivity for alcohol detection. Law enforcement agencies widely adopt fuel cell-based devices because they provide precise blood alcohol concentration readings with minimal interference from other substances.

Regulatory bodies emphasize accuracy in alcohol testing, which strengthens demand for advanced sensing technologies. Fuel cell breathalyzers are expected to expand further as governments continue to enforce strict drunk driving regulations globally.

These devices are likely to gain preference because they offer consistent performance in both roadside and evidential testing. The segment benefits from advancements in sensor durability and calibration stability.

Increasing use of portable and handheld devices is projected to support wider adoption. As accuracy and compliance remain critical in alcohol detection, fuel cell technology is estimated to maintain its dominant position in this market.

Application Analysis

Alcohol detection accounted for 51.2% of growth within application and dominates the breathalyzers market due to the widespread need to monitor and control drunk driving and alcohol consumption. Governments across regions enforce strict legal limits for blood alcohol concentration, which drives consistent demand for testing devices.

Road safety authorities report that alcohol-related accidents contribute significantly to traffic fatalities, which increases the importance of detection systems. This segment is expected to grow as awareness of road safety continues to rise and enforcement measures become more stringent.

Alcohol detection is likely to remain the primary use case for breathalyzers due to its regulatory significance. The segment benefits from continuous deployment in roadside checks, workplaces, and public safety programs.

Increasing adoption of preventive testing in enterprises is projected to further support growth. As safety concerns and regulatory enforcement intensify, alcohol detection is anticipated to retain its leading position in this market.

End-Use Analysis

Law enforcement agencies accounted for 41.6% of growth within end use and dominate the breathalyzers market due to their central role in enforcing traffic safety laws and preventing alcohol-impaired driving. Police departments and traffic authorities use breathalyzers extensively for roadside screening and evidential testing.

Governments prioritize road safety initiatives, which increases procurement of reliable testing devices by law enforcement bodies. This segment is expected to expand as stricter regulations and penalties for drunk driving are implemented globally.

Law enforcement agencies are likely to continue investing in advanced breathalyzer technologies to improve accuracy and efficiency. The segment benefits from ongoing public safety campaigns and increasing focus on reducing accident rates.

As enforcement activities increase and technology adoption improves, law enforcement agencies are estimated to maintain their dominant position in the breathalyzers market.

Key Market Segments

By Technology

- Fuel cell

- Semiconductor sensor

- Infrared spectroscopy

- Others

By Application

- Drug abuse detection

- Alcohol detection

- Medical application

- Others

By End-use

- Law enforcement agencies

- Enterprises

- Individuals

- Others

Drivers

Increasing incidence of alcohol-impaired driving is driving the Breathalyzers market.

The persistent occurrence of alcohol-related traffic incidents has heightened the need for reliable, rapid-testing devices across law enforcement, workplaces, and personal applications. According to the National Highway Traffic Safety Administration, 13,524 people died in alcohol-impaired driving crashes in 2022, accounting for 32 percent of all traffic-related deaths in the United States.

In 2023, this figure stood at 12,429 fatalities, with approximately one person dying every 42 minutes in such preventable crashes. These statistics underscore the ongoing public safety challenge that sustains demand for breath analysis technology.

Governments worldwide have responded by implementing stricter enforcement measures, including mandatory roadside testing and ignition interlock programs. Law enforcement agencies rely on accurate devices to determine blood alcohol concentration levels efficiently during traffic stops.

The data from official sources illustrate a sustained volume of incidents across multiple years within the 2022–2025 period. Heightened public awareness campaigns further amplify the requirement for accessible testing solutions.

Professional guidelines and regulatory frameworks emphasize the role of breathalyzers in reducing impaired driving risks. Consequently, these epidemiological and enforcement patterns establish a primary driver for market expansion during the specified timeframe.

Restraints

High costs of advanced devices and limited reimbursement are restraining the Breathalyzers market.

Sophisticated fuel-cell and infrared-based breathalyzers command premium pricing, which restricts adoption among smaller law enforcement agencies and individual consumers in cost-sensitive environments.

Calibration, maintenance, and periodic sensor replacement add to the total cost of ownership over the device lifecycle. Many public sector budgets face constraints that prioritize essential equipment over advanced testing tools despite recognized accuracy benefits. Reimbursement mechanisms for non-clinical or workplace applications remain inconsistent across regions, discouraging broader deployment.

Training requirements for proper device operation and result interpretation further elevate operational expenses for end users. These financial barriers result in slower replacement cycles and selective utilization of high-end models.

Resource-limited settings often continue with basic semiconductor devices despite their comparatively lower precision. Persistent economic pressures moderate the pace of technology upgrades across various segments. As a result, such cost-related factors impose measurable restraint on accelerated market growth throughout the 2022–2025 timeframe.

Opportunities

Expansion of personal and workplace screening applications is creating growth opportunities in the Breathalyzers market.

Rising corporate adoption of zero-tolerance alcohol policies generates demand for reliable, user-friendly devices suitable for routine employee testing in safety-critical industries. Opportunities emerge for portable, smartphone-connected units that enable self-monitoring and data logging for personal responsibility or fleet management programs.

Integration with ignition interlock systems supports compliance with expanding regulatory mandates for repeat offenders and commercial drivers. Potential exists for scaling solutions in healthcare settings for monitoring alcohol use disorders through non-invasive breath analysis.

Partnerships between device manufacturers and digital health platforms facilitate development of subscription-based monitoring services. Expansion into emerging markets benefits from affordable, compact designs that align with increasing road safety initiatives.

These applications align with value-based safety programs that reward demonstrated reductions in impairment-related incidents. Broader accessibility through consumer channels unlocks new revenue streams beyond traditional law enforcement procurement.

Overall, such diversification generates substantial prospects for market broadening and sustained utilization across multiple sectors.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic conditions and geopolitical developments are influencing demand, pricing, and regulatory adoption in the breathalyzers market. Rising enforcement of road safety laws and workplace compliance requirements are supporting steady demand, while inflation is increasing manufacturing and calibration costs for devices, which can affect procurement budgets for law enforcement agencies and enterprises.

Economic pressure in some regions may delay large-scale equipment upgrades or replacement cycles. Geopolitical tensions disrupt supply chains for sensors, semiconductors, and electronic components, leading to longer lead times and cost variability.

Current US tariffs on imported electronic parts and sensor technologies increase production costs for breathalyzer manufacturers, which can translate into higher device prices and impact adoption in cost-sensitive markets. These cost pressures may slow expansion in certain regions, especially where budgets remain constrained.

At the same time, tariffs are encouraging domestic production and technological self-reliance, which improves supply stability over time. Overall, despite pricing and supply challenges, strong regulatory enforcement and public safety priorities are expected to sustain consistent market growth.

Latest Trends

Integration of smartphone connectivity and advanced sensor technologies represents a recent trend in the Breathalyzers market.

In 2024 and 2025, manufacturers have accelerated development of connected devices that pair with mobile applications for real-time blood alcohol concentration tracking, result sharing, and cloud-based data storage. This advancement enables seamless documentation and remote monitoring capabilities valued by both professional and personal users.

Fuel-cell and infrared spectroscopy sensors have seen refinements that improve accuracy and reduce calibration frequency compared to earlier models. Implementations support features such as tamper detection and automated reporting aligned with regulatory requirements.

The trend aligns with broader digital transformation in safety and health monitoring, allowing users to access historical data and personalized insights directly from their devices. Industry observations during this period highlight growing consumer preference for compact, Bluetooth-enabled units suitable for everyday carry.

This evolution prioritizes multifunctionality and ease of use over standalone hardware. Prominent in 2024–2025, smartphone integration continues to redefine standards for accessible and intelligent breath analysis solutions.

Regional Analysis

North America is leading the Breathalyzers Market

North America accounted for 32.6% of the breathalyzers market in 2025 as law enforcement agencies and workplace safety programs expanded alcohol detection measures to improve public safety and regulatory compliance.

Police departments across the United States and Canada continue to rely on handheld and evidential breath testing devices for roadside screening and legal enforcement. According to National Highway Traffic Safety Administration, the alcohol-impaired driving was responsible for 32% of all traffic fatalities in the United States in 2022, highlighting the ongoing need for reliable detection technologies.

Governments are strengthening enforcement of drunk driving laws, which has increased procurement of advanced breath testing equipment. Workplaces in industries such as transportation, construction, and manufacturing are also adopting alcohol screening devices to ensure employee safety and compliance with occupational regulations.

Technological improvements, including fuel cell sensors and connectivity features, are enhancing accuracy and real-time data tracking capabilities. Healthcare and rehabilitation centers are also using breath testing devices for monitoring alcohol use in treatment programs.

Public awareness campaigns around road safety and substance use have further supported adoption. These factors collectively contributed to steady growth of alcohol detection solutions across North America in 2025.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to experience strong growth during the forecast period as governments strengthen road safety regulations and increase adoption of alcohol monitoring technologies.

Countries such as China, India, Japan, and Australia are implementing stricter laws to reduce alcohol-related accidents and improve public safety outcomes. The World Health Organization reports that alcohol consumption contributes to over 3 million deaths globally each year, reinforcing the importance of effective detection and prevention measures.

Law enforcement agencies across the region are expanding roadside testing programs and increasing use of portable detection devices. Rapid urbanization and rising vehicle ownership are also driving the need for stricter traffic monitoring systems.

Employers in high-risk industries are introducing alcohol screening protocols to enhance workplace safety. Technology providers are developing cost-effective and easy-to-use devices suited for large-scale deployment.

Governments are promoting awareness campaigns to discourage impaired driving and encourage responsible alcohol consumption. These developments are expected to accelerate adoption of alcohol detection technologies across Asia Pacific in the coming years.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

Key participants in the Breathalyzers Market expand growth by developing high-precision alcohol detection technologies, integrating semiconductor and fuel cell sensors, and strengthening partnerships with law enforcement agencies and workplace safety programs.

Companies invest in portable, smartphone-connected devices and cloud-based data management systems that improve real-time monitoring and reporting. They also focus on expanding product applications across personal use, healthcare screening, and enterprise compliance solutions.

Lifeloc Technologies represents a prominent participant in the Breathalyzers Market and operates as a U.S.-based manufacturer that develops professional-grade breath alcohol testing devices and related monitoring systems for law enforcement, corrections, and workplace environments.

The company emphasizes accuracy, regulatory compliance, and user-friendly design to support reliable alcohol detection. Industry competitors continue to introduce advanced sensor technologies, expand distribution channels, and strengthen regulatory alignment to enhance adoption and sustain long-term market growth.

Top Key Players

- Abbott Laboratories

- AK GlobalTech Corp.

- Akers Biosciences Inc.

- Alcohol Countermeasure Systems Corp.

- AlcoPro

- BACtrack

- Bedfont Scientific Ltd.

- Drägerwerk AG & Co. KGaA

- Intoximeters, Inc.

- Lifeloc Technologies, Inc.

Recent Developments

- In March 2026, Abbott completed the acquisition of Exact Sciences, signaling a strategic shift toward expanding its presence in advanced cancer screening and molecular diagnostics. The move reflects a broader industry transition toward high-precision diagnostic solutions, while traditional screening tools continue to play a supporting role in routine testing environments.

- In early 2026, Lifeloc Technologies began the phased rollout of its SpinDetect centrifugal drug analyzer. The system uses microfluidic technology to identify multiple substances from oral fluid samples within a short turnaround time, helping bridge the gap between rapid screening and laboratory-level confirmation in drug detection.

Report Scope

Report Features Description Market Value (2025) US$ 3.1 Billion Forecast Revenue (2035) US$ 15.6 Billion CAGR (2026-2035) 17.5% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Technology (Fuel cell, Semiconductor sensor, Infrared spectroscopy and Others), By Application (Drug abuse detection, Alcohol detection, Medical application and Others), By End-use (Law enforcement agencies, Enterprises, Individuals and Others) Regional Analysis North America – The US, Canada; Europe – Germany, France, The U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America Competitive Landscape Abbott Laboratories, AK GlobalTech Corp., Akers Biosciences Inc., Alcohol Countermeasure Systems Corp., AlcoPro, BACtrack, Bedfont Scientific Ltd., Drägerwerk AG & Co. KGaA, Intoximeters, Inc., Lifeloc Technologies, Inc. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Abbott Laboratories

- AK GlobalTech Corp.

- Akers Biosciences Inc.

- Alcohol Countermeasure Systems Corp.

- AlcoPro

- BACtrack

- Bedfont Scientific Ltd.

- Drägerwerk AG & Co. KGaA

- Intoximeters, Inc.

- Lifeloc Technologies, Inc.

Our Clients

- 183534

- April 2026