Global Border Security Technologies Market Size, Share, Growth Analysis By Systems (Radar Systems, Laser Systems, Camera Systems, Unmanned Vehicles, Wide Band Wireless Communication Systems, Command and Control Systems, Biometric Systems, Drones, Optical Surveillance Systems, Electric Fencing Systems), By Application (Ground Based, Aerial Based, Naval Based), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Apr 2026

- Report ID: 183651

- Number of Pages: 373

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

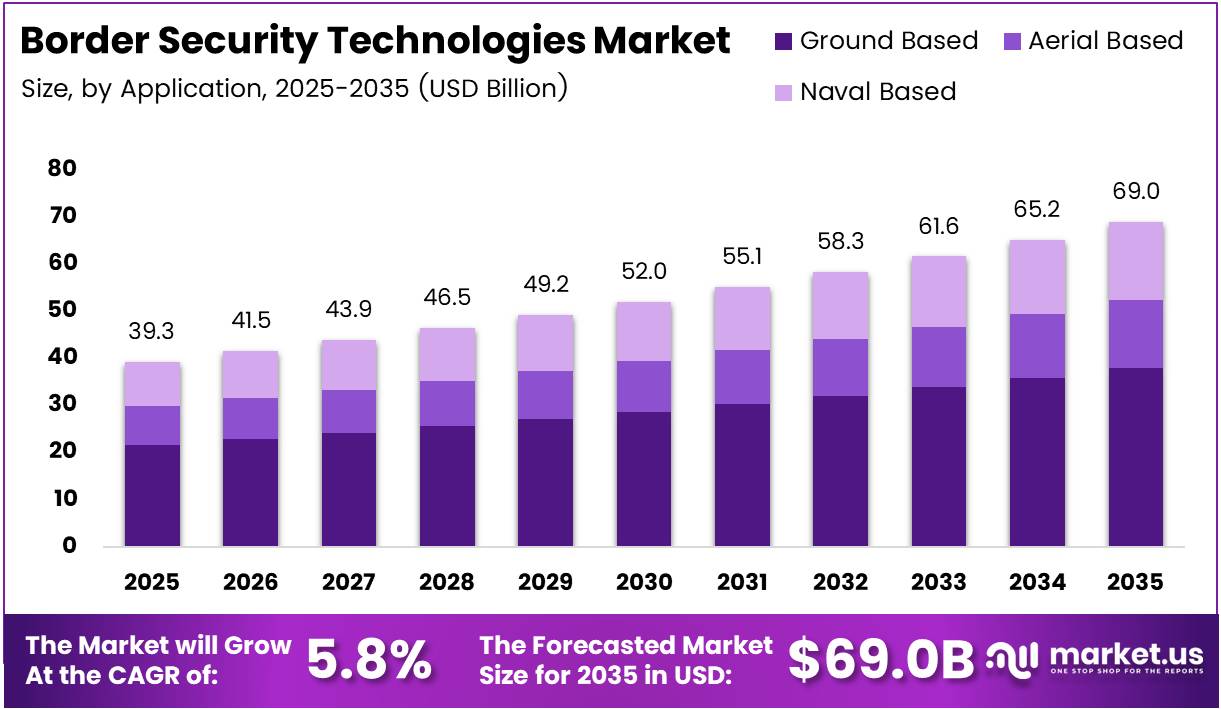

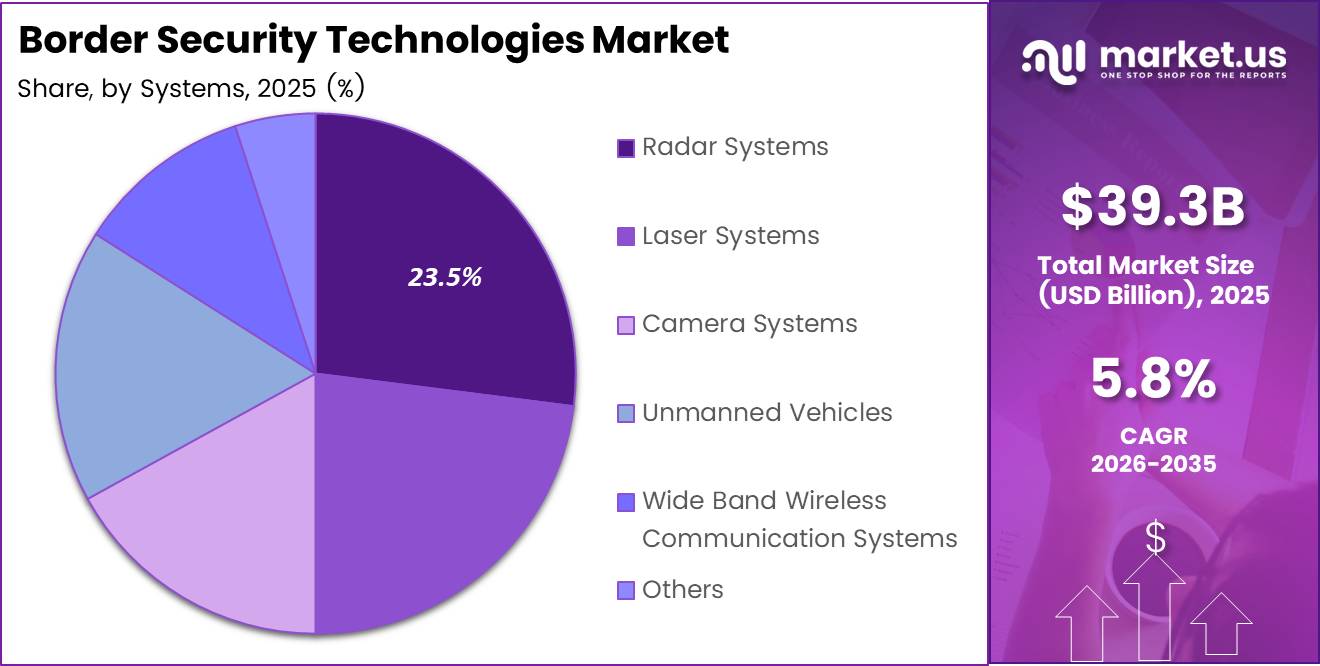

Global Border Security Technologies Market size is expected to be worth around USD 69.0 Billion by 2035 from USD 39.3 Billion in 2025, growing at a CAGR of 5.8% during the forecast period 2026 to 2035.

The border security technologies market covers systems and solutions governments deploy to monitor, detect, and control unauthorized crossings at national boundaries. These include radar systems, biometric identification, unmanned vehicles, surveillance cameras, and command and control infrastructure. Demand originates primarily from defense ministries and homeland security agencies.

Ground-based surveillance commands the largest application share at 54.8%, which reflects the sheer scale of land border exposure relative to aerial or naval perimeters. This concentration signals that vendors with strong ground sensor portfolios hold a structural advantage when competing for large national border modernization contracts.

Radar systems lead the By Systems segment with a 23.5% share, underscoring the continued reliance on wide-area detection before visual confirmation becomes possible. However, the fastest repositioning in procurement is shifting toward integrated multi-sensor platforms that combine radar, cameras, and AI-based analytics into unified command architectures.

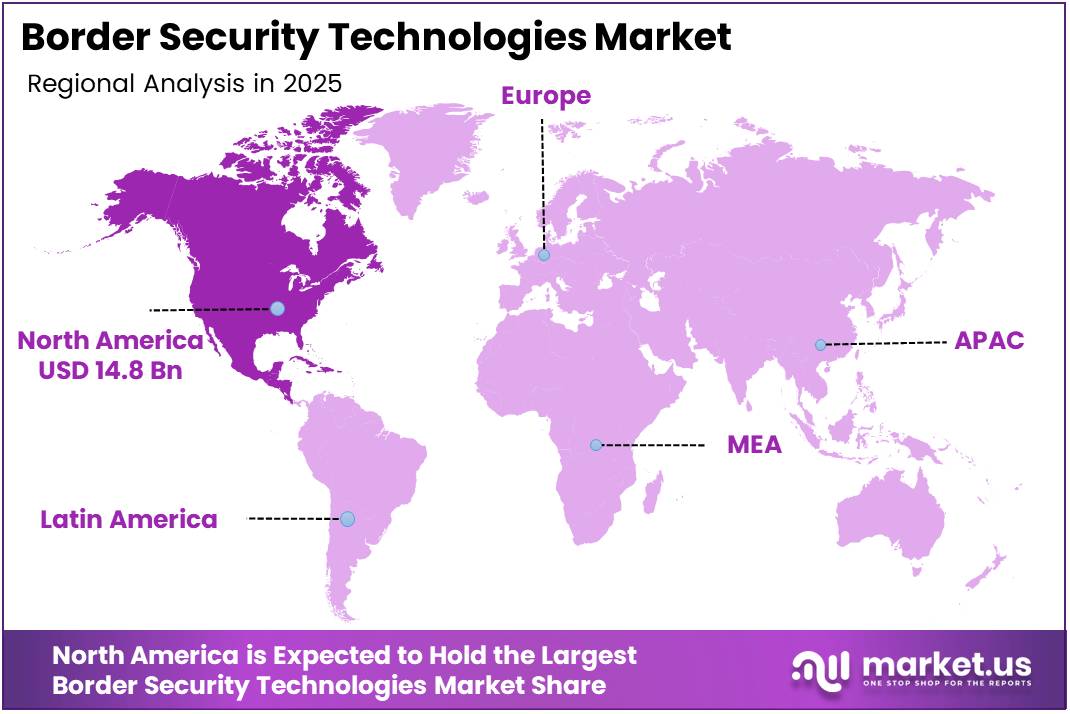

North America holds a dominant regional position with 37.9% share, valued at USD 14.8 Billion. The U.S. government’s sustained investment in smart border infrastructure — including nationwide biometric rollout and autonomous patrol technologies — cements this lead and sets the procurement template other regions are now replicating.

According to Biometric Update, by 2025, U.S. Customs and Border Protection deployed biometric entry-exit capabilities at all U.S. airports handling more than 50,000 annual international arrivals. This near-universal coverage marks a maturation point — biometric identity verification is no longer a pilot program but a standard operational requirement.

According to the same report, CBP’s biometric facial-comparison systems now process over 99% of non-U.S. citizen arrivals by air. This scale of deployment creates a compounding procurement effect: as biometric infrastructure becomes default at air entry points, pressure builds to extend equivalent capability to land and sea borders — expanding the addressable market for biometric vendors significantly.

Key Takeaways

- The global border security technologies market was valued at USD 39.3 Billion in 2025 and is forecast to reach USD 69.0 Billion by 2035.

- The market grows at a CAGR of 5.8% from 2026 to 2035.

- North America leads all regions with a 37.9% share, valued at USD 14.8 Billion.

- Radar Systems hold the largest share in By Systems segment at 23.5%.

- Ground Based applications dominate By Application segment with a 54.8% share.

- Base year for estimation is 2025, with historic data covering 2020 to 2024.

Product Analysis

Radar Systems dominates with 23.5% due to wide-area detection before visual range.

In 2025, Radar Systems held a dominant market position in the By Systems segment of the Border Security Technologies Market, with a 23.5% share. Radar provides the first layer of detection across vast, often remote perimeters where camera or sensor coverage alone is insufficient. Governments prioritize radar because it functions in all weather conditions and at distances that allow reaction time before a threat reaches the border line.

Laser Systems serve as a precision complement to broad radar coverage. Laser-based detection offers high-accuracy intrusion alerts along defined corridors, particularly in areas where false alarms from radar clutter create operational noise. Procurement agencies deploy laser systems to tighten the detection chain in high-sensitivity zones.

Camera Systems convert detection alerts into visual confirmation, closing the identification gap that radar and laser systems leave open. Modern border camera deployments integrate AI-driven video analytics, reducing operator workload significantly and allowing smaller teams to monitor longer perimeters without reducing alert response rates.

Unmanned Vehicles extend physical response capability without risking personnel in dangerous terrain. Ground and aerial unmanned platforms now handle patrol routes that previously required human teams, compressing the cost per kilometer of active border surveillance. Their adoption accelerates as governments face pressure to cover more border length with constrained personnel budgets.

Wide Band Wireless Communication Systems form the data backbone connecting all sensor layers to central command. Without reliable high-bandwidth communication, real-time data from radar, cameras, and drones cannot reach decision-makers quickly enough. Vendors offering integrated communication architecture alongside surveillance hardware hold a distinct contract advantage.

Command and Control Systems translate incoming sensor data into actionable decisions for border operators. Their value is less about hardware and more about software intelligence — fusing data from multiple sources into a single operational picture. Buyers increasingly evaluate command platforms on integration capability across legacy and new sensor types.

Biometric Systems deliver identity-layer verification at points of entry, addressing the enforcement gap that physical surveillance alone cannot close. According to U.S. Travel Association, under DHS guidance effective December 2025, CBP gained authority to require biometric collection including facial images for all non-U.S. travelers entering and exiting the country. This regulatory mandate transforms biometric systems from optional enhancement into non-negotiable procurement, directly accelerating spending across air, land, and sea ports of entry.

Drones provide aerial surveillance flexibility that fixed infrastructure cannot replicate. Drone deployments cover temporary border surges, remote mountain terrain, and maritime coastlines that require mobile coverage rather than fixed sensor arrays. Their relatively low capital cost compared to manned aircraft makes them a preferred tool for budget-constrained border agencies.

Optical Surveillance Systems provide long-range daytime and night vision capability that supports both detection and documentation of border events. High-resolution optical systems produce evidence-quality imagery for enforcement actions, making them essential not just for detection but for legal processing of apprehensions.

Electric Fencing Systems represent the physical deterrence layer within integrated border security architectures. Modern electric fencing pairs detection sensors with access barriers, alerting operators to contact attempts in real time. Their role is less standalone deterrent and more trigger mechanism for deploying rapid response assets to confirmed contact points.

Application Analysis

Ground Based dominates with 54.8% due to the scale of land border exposure globally.

In 2025, Ground Based applications held a dominant market position in the By Application segment of the Border Security Technologies Market, with a 54.8% share. Land borders represent the longest and most continuously active perimeters for most nations, requiring permanent fixed infrastructure combined with mobile response capability. According to iProov, biometric lanes at Orlando International Airport processed up to 14 passengers per lane per minute, with each traveler verified in under 3 seconds — demonstrating that ground-based biometric processing capacity now exceeds legacy manual throughput by a significant margin and validates continued capital investment in ground infrastructure upgrades.

Aerial Based applications address the surveillance gaps that fixed ground infrastructure cannot cover, particularly over mountainous terrain, dense forest crossings, and active maritime coastlines. Aerial surveillance assets — including manned aircraft and unmanned platforms — serve as force multipliers that extend the operational reach of ground-based teams without proportional increases in personnel costs.

Naval Based applications protect maritime borders and exclusive economic zones where conventional land-based sensors have no reach. Nations with significant coastlines or island territories rely on naval-integrated radar, sonar, and unmanned surface vessels to detect illegal crossings, smuggling routes, and unauthorized vessel approaches. As maritime migration routes shift in response to land border enforcement, naval application spending rises correspondingly.

Key Market Segments

By Systems

- Radar Systems

- Laser Systems

- Camera Systems

- Unmanned Vehicles

- Wide Band Wireless Communication Systems

- Command and Control Systems

- Biometric Systems

- Drones

- Optical Surveillance Systems

- Electric Fencing Systems

By Application

- Ground Based

- Aerial Based

- Naval Based

Drivers

Government Mandates for Biometric and AI-Enabled Border Control Accelerate Technology Procurement

Governments worldwide have moved border security from discretionary spending to mandated infrastructure investment. The U.S. DHS directive requiring biometric collection for all non-U.S. travelers — combined with CBP’s planned rollout across all commercial airports and seaports within three to five years — converts regulatory policy directly into a defined procurement pipeline for biometric vendors.

According to U.S. Travel Association, CBP’s facial-comparison technology achieves over 98% accuracy in verifying traveler identity — a performance standard that exceeds manual document checks by a measurable margin. This accuracy threshold matters because it satisfies the evidentiary standard required by courts and immigration agencies, removing a long-standing institutional barrier to full biometric adoption at border checkpoints.

Illegal migration pressures and cross-border security threats have forced governments to fund smart border surveillance infrastructure at scale. AI-enabled monitoring systems reduce the human-to-perimeter ratio needed for effective coverage, making them attractive to agencies managing long borders with fixed staffing budgets. This structural need — more coverage, lower cost per kilometer — creates durable procurement demand across both developed and developing border economies.

Restraints

High Technology Costs and Surveillance Ethics Create Structural Barriers to Rapid Adoption

Advanced border surveillance systems carry significant upfront capital costs and ongoing maintenance obligations that strain procurement budgets, particularly in developing nations with long borders and limited defense spending. Radar arrays, command infrastructure, and biometric networks require not just purchase financing but sustained technical support contracts, creating multi-year budget commitments that slow procurement cycles.

Privacy and ethical concerns around biometric surveillance create a secondary friction layer that affects deployment timelines even where funding exists. Civil liberties organizations, parliamentary oversight bodies, and international human rights frameworks challenge the proportionality of persistent biometric monitoring at borders. These objections translate into legislative delays, mandatory impact assessments, and scope restrictions that extend project timelines and raise compliance costs for vendors.

According to IDGA, total apprehensions at U.S. borders dropped from 46,837 in December 2024 to 7,634 by April 2025 — roughly an 84% reduction. While this validates the effectiveness of technology-enabled enforcement, it also creates a political argument that reduced threat levels justify slowing capital investment in new systems. Budget committees use declining apprehension metrics to question incremental spending on surveillance expansion, creating a cyclical restraint on market growth during low-pressure periods.

Growth Factors

Autonomous Surveillance Drones and Integrated Sensor Networks Open New Revenue Segments for Border Technology Vendors

Autonomous surveillance drones for border monitoring represent a structurally new product category that existing ground infrastructure vendors cannot easily replicate. Drone platforms combine aerial mobility with persistent surveillance capability, addressing the terrain and distance limitations that ground sensor networks face. For vendors, drone programs carry recurring revenue potential through maintenance contracts, software updates, and sensor payload upgrades.

The integration of satellite and radar technologies for wide-area border surveillance creates procurement opportunities that extend beyond national defense budgets into multilateral security programs. Regional bodies funding joint border monitoring infrastructure — particularly along shared land or maritime borders — represent contract sizes that individual national procurements rarely match. Vendors with satellite integration capability position themselves for these larger, longer-duration contracts.

According to IDGA, CBP recorded a 93% drop in apprehensions at the southwest border between April 2024 and April 2025, an outcome linked directly to technology-enabled border operations. This performance data serves as a proof point that funding agencies and legislators reference when approving next-cycle border technology budgets. Demonstrated ROI at this scale reduces the political risk of authorizing large surveillance infrastructure investments, accelerating approval timelines for vendors in the pipeline.

Emerging Trends

Multi-Sensor AI Platforms and Cloud-Based Management Shift Border Security from Hardware to Intelligence Architecture

Artificial intelligence for automated threat detection is reshaping what border agencies buy and how they evaluate vendor capability. The competitive differentiation is moving from sensor quality to algorithmic performance — how accurately and quickly a system distinguishes genuine threats from environmental noise. Vendors who lead on AI detection precision gain a durable advantage as agencies standardize on fewer, more capable integrated platforms.

In September 2025, Elbit Systems unveiled Frontier, a next-generation AI-based wide-area persistent surveillance system for autonomous threat detection across land, air, and maritime borders. This launch signals that multi-domain coverage through a single AI architecture is becoming a procurement expectation, not a premium option. Buyers looking for unified situational awareness will favor vendors who can deliver cross-domain capability over those offering siloed sensor products.

According to iProov, biometric lanes at Orlando International Airport reduced average wait times by approximately 65% — from up to 15 minutes to a stabilized range of 2 to 8 minutes — while passenger throughput increased by 25 to 30%. This operational efficiency gain demonstrates that AI-integrated biometric processing delivers measurable service improvements alongside security benefits, a combination that accelerates government approval for cloud-based border management deployments where throughput and accuracy data justify infrastructure investment.

Regional Analysis

North America Dominates the Border Security Technologies Market with a Market Share of 37.9%, Valued at USD 14.8 Billion

North America leads the global border security technologies market with a 37.9% share, valued at USD 14.8 Billion. The United States drives this dominance through mandated federal investment in biometric entry-exit systems, AI-enabled surveillance infrastructure, and multi-agency border management programs. Mature procurement frameworks and a defined DHS rollout timeline across commercial airports and seaports within three to five years sustain predictable spending at scale.

Europe Border Security Technologies Market Trends

Europe allocates substantial border security budgets through Frontex, the European Border and Coast Guard Agency, alongside national defense programs. The migration pressures across Mediterranean maritime and Eastern land borders have pushed member states toward integrated multi-sensor solutions that align with EU interoperability standards. This regulatory alignment creates a structured procurement environment for vendors that meet EU certification requirements.

Asia Pacific Border Security Technologies Market Trends

Asia Pacific holds significant growth potential driven by the scale of land borders across South Asia, Southeast Asia, and the Indian subcontinent. Countries including India and China are investing in fencing systems, radar networks, and biometric checkpoints to address both illegal crossings and cross-border militant activity. Defense modernization budgets in the region support multi-year procurement cycles for integrated border surveillance.

Middle East and Africa Border Security Technologies Market Trends

The Middle East and Africa region faces complex border security challenges driven by active conflict zones, porous desert borders, and maritime smuggling routes in the Red Sea and Gulf of Aden. Gulf Cooperation Council members invest in radar and surveillance drone infrastructure, while African nations increasingly access border security financing through international security assistance programs that fund technology deployments.

Latin America Border Security Technologies Market Trends

Latin America addresses border security primarily through counter-narcotics and anti-trafficking programs funded partly through U.S. and multilateral security assistance. Brazil and Mexico lead regional procurement, focusing on aerial surveillance, integrated checkpoint biometrics, and communication systems along high-traffic smuggling corridors. Budget constraints in smaller nations limit large-scale infrastructure investment, creating a stronger market for modular and lower-capital surveillance solutions.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Lockheed Martin Corporation positions itself at the intersection of aerospace and border security, leveraging its satellite surveillance and C2 systems capabilities to compete for large integrated border management contracts. Its strength lies in multi-domain coverage — combining space-based intelligence with ground sensor networks — giving it a distinct advantage when agencies require persistent wide-area surveillance that single-domain vendors cannot match.

BAE Systems plc brings a defense electronics heritage that translates directly into border surveillance applications, particularly radar, electronic warfare detection, and command systems integration. Its established relationships with NATO member governments accelerate procurement approvals in European border security programs, where interoperability with existing defense infrastructure is a mandatory evaluation criterion that new market entrants struggle to meet.

Raytheon Technologies Corporation competes on sensor precision and missile defense integration, offering radar systems that serve dual-use roles across both border surveillance and national air defense architectures. This dual-use positioning reduces the procurement risk for defense ministries that want border infrastructure to integrate with existing national defense networks, effectively locking Raytheon into larger, longer-term contract structures.

Thales Group specializes in integrated border management systems that combine biometric identification, surveillance, and data analytics into unified platforms for both civilian and military border applications. Its strength in digital identity and secure communications gives it a competitive edge in European and Middle Eastern markets where data sovereignty requirements shape vendor selection criteria and favor established European defense technology providers.

Key Players

- Lockheed Martin Corporation

- BAE Systems plc

- Raytheon Technologies Corporation

- Thales Group

- Leonardo S.p.A.

- Northrop Grumman Corporation

- Saab AB

- Indra Sistemas, S.A.

- FLIR Systems, Inc.

Recent Developments

- September 2025 — Elbit Systems unveiled Frontier, a next-generation AI-based wide-area persistent surveillance system designed for autonomous threat detection and assessment across land, air, and maritime border environments, marking a significant advance in multi-domain AI border surveillance architecture.

- September 2025 — Deloitte was awarded a $15 million DHS CBP task order on the Alliant 2 contract to provide border security technology systems support, reflecting the U.S. government’s continued outsourcing of border technology integration and systems management to specialized commercial partners.

- 2025 — iProov’s hardware-light biometric lanes at Orlando International Airport increased passenger throughput by 25 to 30%, demonstrating that high-volume biometric processing deployments can deliver measurable capacity gains alongside identity verification accuracy improvements at major international entry points.

Report Scope

Report Features Description Market Value (2025) USD 39.3 Billion Forecast Revenue (2035) USD 69.0 Billion CAGR (2026-2035) 5.8% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Systems (Radar Systems, Laser Systems, Camera Systems, Unmanned Vehicles, Wide Band Wireless Communication Systems, Command and Control Systems, Biometric Systems, Drones, Optical Surveillance Systems, Electric Fencing Systems), By Application (Ground Based, Aerial Based, Naval Based) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Lockheed Martin Corporation, BAE Systems plc, Raytheon Technologies Corporation, Thales Group, Leonardo S.p.A., Northrop Grumman Corporation, Saab AB, Indra Sistemas, S.A., FLIR Systems, Inc. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Border Security Technologies MarketPublished date: Apr 2026add_shopping_cartBuy Now get_appDownload Sample

Border Security Technologies MarketPublished date: Apr 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Lockheed Martin Corporation

- BAE Systems plc

- Raytheon Technologies Corporation

- Thales Group

- Leonardo S.p.A.

- Northrop Grumman Corporation

- Saab AB

- Indra Sistemas, S.A.

- FLIR Systems, Inc.

Our Clients

- 183651

- Apr 2026