Quick Navigation

Report Overview

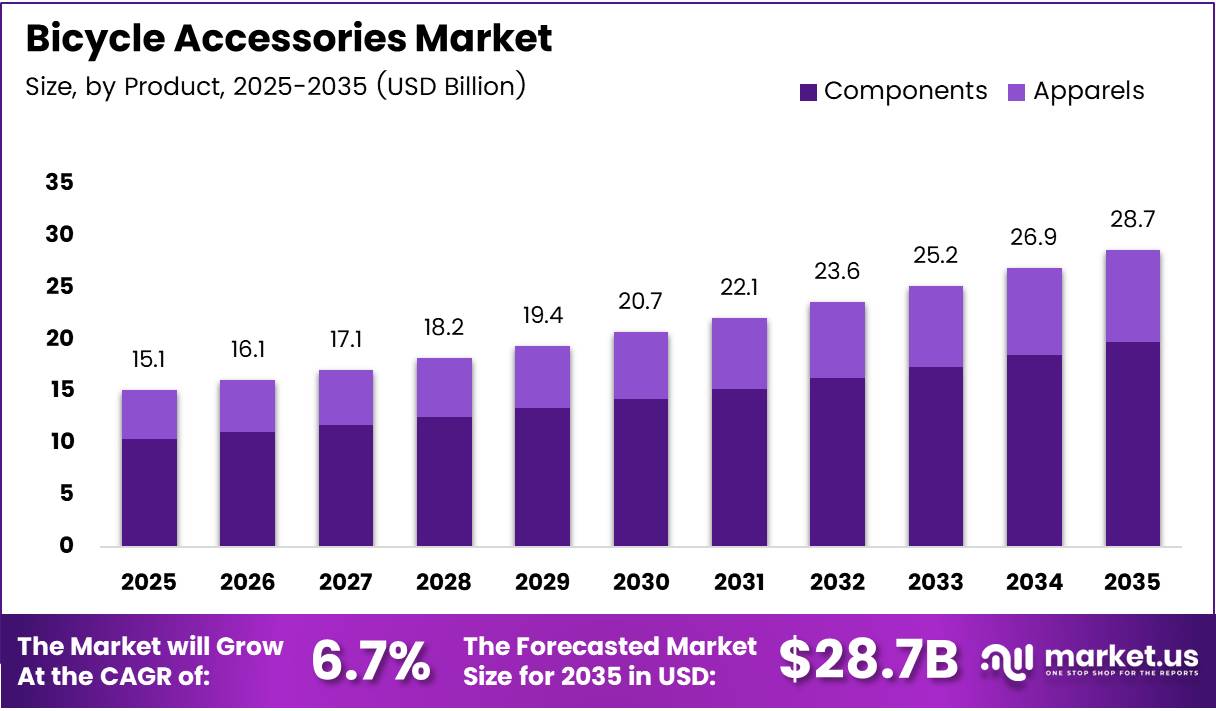

Global Bicycle Accessories Market size is expected to be worth around USD 28.7 Billion by 2035 from USD 15.1 Billion in 2025, growing at a CAGR of 6.7% during the forecast period 2026 to 2035.

The bicycle accessories market covers a broad commercial ecosystem supplying components, safety gear, apparel, and smart devices to cyclists worldwide. Products range from saddles and pedals to GPS computers and smart helmets. This market sits at the intersection of health, urban mobility, and consumer technology, attracting buyers across recreational, commuter, and professional cycling segments.

Urban infrastructure investment is reshaping cycling demand across major economies. Governments in Europe, North America, and Asia Pacific are allocating capital to dedicated cycling lanes, bike-share programs, and EV incentives that include e-bikes. These policy actions convert occasional riders into regular cyclists, directly expanding the addressable base for bicycle accessories across all product categories.

Electric bicycle adoption is a structural accelerator for this market. E-bike owners require specialized accessories including battery mounts, charging docks, extended lighting systems, and GPS anti-theft devices. This creates a higher average spend per user than traditional bicycle ownership. The e-bike segment therefore lifts the overall revenue ceiling for accessory manufacturers and retailers.

The aftermarket channel remains critical for sustained revenue. Cyclists regularly replace components such as tyres, brake pads, and lighting systems, generating recurring purchase cycles independent of new bicycle sales. This recurring demand provides revenue stability even during periods when new bicycle unit sales soften, making the accessories market less cyclically exposed than the bicycle hardware market itself.

In December 2024, Rhino-Rack acquired RockyMounts, a Colorado-based bicycle transport and bike rack accessories brand. This deal reflects how accessories companies are consolidating to build portfolio depth in the outdoor adventure segment, a buyer group that spends significantly more per transaction than casual urban cyclists.

According to the Transport for New South Wales Safety Performance Indicators Report 2025, the observed bicycle helmet wear rate in New South Wales, Australia, was 85.3% in 2025, down from 89.5% in 2023. This decline signals a compliance gap that regulators and brands must address together. For safety accessory manufacturers, it identifies an active intervention opportunity in one of the world’s most helmet-regulated markets.

According to Virginia Tech’s 2026 bicycle helmet ratings study covering 296 helmets tested, top-performing helmets achieved STAR scores as low as approximately 9.86. These ratings directly influence retailer stocking decisions and consumer purchasing behavior. Brands with top-rated helmets hold a measurable shelf and conversion advantage, confirming that safety performance data now functions as a competitive differentiator in the premium accessories tier.

Key Takeaways

- The Global Bicycle Accessories Market was valued at USD 15.1 Billion in 2025 and is forecast to reach USD 28.7 Billion by 2035.

- The market grows at a CAGR of 6.7% during the forecast period 2026 to 2035.

- By Product, Components dominated with a 68.30% share in 2025.

- By Bicycle, Road Bikes held the leading position with a 48.80% share in 2025.

- By Type, OEM led with a 56.20% share in 2025.

- By Sales Channel, Offline channels captured 62.40% of market share in 2025.

- Asia Pacific dominated regionally with a 43.80% share, valued at USD 6.6 Billion in 2025.

Product Analysis

Components dominates with 68.30% due to high replacement frequency and e-bike accessory expansion.

In 2025, Components held a dominant market position in the By Product segment of the Bicycle Accessories Market, with a 68.30% share. Saddles, pedals, lighting systems, locks, and air pumps drive consistent repeat purchases independent of new bike sales. The e-bike boom has intensified demand for specialized lighting and security components, reinforcing this segment’s structural lead over apparel.

Apparels serves a distinct buyer profile seeking performance enhancement and personal protection. Categories including cycling gloves, shoes, and protective gear attract premium pricing from performance and recreational cyclists. According to the MassCEC ACT4All Final Report, 203 e-bike program participants recorded 92,353 miles of trips, demonstrating active riding behavior that directly translates into higher apparel replacement rates among committed cyclists.

Bicycle Type Analysis

Road Bikes dominates with 48.80% due to high accessory spend per rider among performance cyclists.

In 2025, Road Bikes held a dominant market position in the By Bicycle segment of the Bicycle Accessories Market, with a 48.80% share. Road cyclists consistently purchase premium components, GPS computers, aerodynamic helmets, and performance apparel. Their high engagement frequency and willingness to invest in upgrades make road bike users the highest-value accessory buyers across all bicycle categories.

Mountain Bikes generate strong accessory demand through a distinct product mix centered on protective gear, suspension components, and trail-specific lighting. The rise of enduro and bikepacking disciplines is broadening the accessory set per rider, as athletes equip for multi-day off-road excursions requiring multi-functional gear solutions.

Hybrid Bikes serve the urban commuter segment, where accessories prioritize practicality over performance. Locks, fenders, lighting systems, and cargo solutions form the core purchase basket. Hybrid bike users represent a structurally stable demand source because their accessory needs are driven by daily utility rather than discretionary sport spending.

Cargo Bikes carry a distinct accessory profile including reinforced kickstands, cargo-rated racks, and high-output lighting systems designed for commercial and family transport use. Urban logistics operators adopting cargo bikes for last-mile delivery are emerging as a B2B buyer segment with repeatable bulk accessory procurement needs.

Type Analysis

OEM dominates with 56.20% due to integrated supply agreements with major bicycle manufacturers.

In 2025, OEM held a dominant market position in the By Type segment of the Bicycle Accessories Market, with a 56.20% share. Bicycle manufacturers prefer factory-fitted accessories to ensure brand consistency, safety compliance, and supply chain efficiency. OEM relationships with component suppliers like Shimano and SRAM lock in volume commitments that are difficult for aftermarket competitors to displace at scale.

Aftermarket channels serve cyclists seeking performance upgrades, personalization, or replacement parts outside manufacturer specifications. The aftermarket segment benefits from the installed base of existing bicycles, which vastly outnumbers annual new bicycle sales. This dynamic gives aftermarket suppliers a durable and growing addressable market independent of new bicycle production cycles.

Sales Channel Analysis

Offline dominates with 62.40% due to fit-sensitive product categories requiring in-person trial.

In 2025, Offline channels held a dominant market position in the By Sales Channel segment of the Bicycle Accessories Market, with a 62.40% share. Helmets, shoes, and saddles require physical fitting to ensure safety and comfort, making specialty bike shops and sporting goods retailers irreplaceable for high-value purchases. This fit dependency structurally protects offline channels from full e-commerce displacement.

Online retail is capturing an expanding share of commodity and replacement accessory purchases including locks, pumps, and bottle cages. Direct-to-consumer brands are using performance data, subscription models, and customization tools to build loyalty outside the traditional retail channel, gradually shifting buyer behavior for non-fit-sensitive product categories.

Key Market Segments

By Product

- Apparels

- Cycling Gloves

- Cycling Clothes

- Cycling Shoes

- Protective Gears

- Others

- Components

- Saddles

- Pedals

- Lighting System

- Mirrors

- Water Bottle Cages

- Lock

- Bar Ends/Grips

- Kickstands

- Fenders & Mud Flaps

- Air Pumps & Tyre Pressure Gauge

- Others

By Bicycle

- Road Bikes

- Mountain Bikes

- Hybrid Bikes

- Cargo Bikes

- Others

By Type

- OEM

- Aftermarket

By Sales Channel

- Offline

- Online

Drivers

Government Cycling Infrastructure Investment and E-Bike Programs Are Expanding the Bicycle Accessories Buyer Base

Government-funded cycling programs are converting low-frequency riders into daily commuters, directly expanding the addressable market for bicycle accessories. Urban cycling infrastructure investment has moved from pilot projects to permanent capital budgets in major cities across Europe, North America, and Asia Pacific. Each new rider entering a structured cycling environment becomes a multi-category accessory buyer.

According to the MassCEC ACT4All Final Report, 203 participants in the Massachusetts e-bike program recorded 20,546 e-bike trips covering 92,353 miles. This level of active usage confirms that subsidized e-bike adoption programs generate sustained riding behavior, not just one-time purchases. Participants in such programs consistently require lighting, locks, helmets, and storage accessories throughout their riding lifecycle.

In June 2025, Garmin launched the Edge MTB, its first GPS cycling computer designed specifically for mountain bikers, featuring 5 Hz GPS recording and extended battery performance. This product launch signals that technology brands recognize specialized cycling segments as distinct and commercially viable accessory markets. Segment-specific product development accelerates accessory adoption and increases spend per rider beyond general-purpose devices.

Restraints

Price Sensitivity in Developing Markets and Seasonal Demand Cycles Constrain Consistent Accessory Revenue Growth

Consumers in developing markets in Southeast Asia, Latin America, and Sub-Saharan Africa prioritize functional, low-cost accessories over premium safety and smart technology products. Bicycle accessories in these markets are often purchased at the lowest available price point, compressing manufacturer margins and limiting the revenue contribution from high-growth population centers.

According to Virginia Tech’s updated STAR rating thresholds published in July 2025, only 38 helmets out of all tested products retained 5-star ratings after the new concussion risk reduction benchmarks took effect, down from 167 previously. This regulatory tightening forces manufacturers to invest in costly redesigns or accept lower safety classifications. Brands serving price-sensitive markets face the sharpest trade-off between compliance investment and retail price constraints.

Seasonal demand fluctuations create uneven cash flow for accessory retailers, particularly in temperate Northern Hemisphere markets where cycling activity drops sharply in winter months. Retailers carry inventory risk during low-demand quarters, and manufacturers face production planning complexity when orders cluster in spring and summer. This cyclicality disadvantages smaller specialty retailers who lack the working capital to absorb off-season inventory costs.

Growth Factors

E-Bike Adoption, Women-Specific Product Lines, and Adventure Cycling Are Opening New Accessory Revenue Streams

The expansion of electric bicycle ownership is directly creating demand for specialized accessories that did not exist at scale five years ago. Battery management systems, charging cable organizers, extended-range lighting, and GPS anti-theft units are now standard purchase considerations for e-bike owners. Each e-bike sold generates a secondary accessory basket that exceeds traditional bicycle accessory spend per unit.

According to a lifecycle analysis published in the journal Resources, Conservation and Recycling, e-bikes emit an average of 45 g CO₂e per kilometer over their operational lifespan. This low-emission profile directly supports government subsidy programs for e-bikes and associated accessories, as urban planners treat e-bikes as a tool for decarbonizing short urban trips. Policy support translates into continued consumer incentives, sustaining demand for the broader accessories ecosystem.

Women-specific and child-focused bicycle accessory lines represent a structurally underpenetrated opportunity. Female cyclists and parents equipping children require ergonomically distinct helmets, saddles, gloves, and protective gear. Brands that invest in purpose-built product lines for these segments capture buyers who previously compromised on fit, creating both first-time purchase and high-loyalty repeat purchase dynamics.

Emerging Trends

Smart Helmets, App-Connected Security Devices, and Eco-Material Innovation Are Redefining the Bicycle Accessories Product Standard

AI-enabled smart helmets integrating voice assistance and automatic crash detection are shifting the safety accessory category from passive protection to active risk management. These helmets connect to smartphones, alert emergency contacts, and adapt audio inputs to ambient noise. For premium buyers, smart helmets are becoming a safety platform rather than a single-function product, supporting a higher price tier and stronger brand loyalty.

According to LITEMOVE’s 2026 OE technical catalog, bicycle lighting systems now offer high beam outputs of 680 lumens with power consumption ranges from 5.4W to 17W depending on operating mode. These specifications reflect OEM-grade performance expectations entering the aftermarket. Consumers now evaluate lighting products against professional benchmarks, raising the baseline for what qualifies as a competitive product in this sub-segment.

In October 2025, Garmin introduced the Tacx Alpine accessory for the Tacx NEO indoor cycling trainer, enabling uphill and downhill gradient simulation for immersive indoor sessions. This development illustrates how accessory brands are bridging the indoor and outdoor cycling experience. As indoor cycling adoption grows year-round, accessories designed for training environments expand the total accessory spend per cyclist beyond outdoor riding seasons.

Regional Analysis

Asia Pacific Dominates the Bicycle Accessories Market with a Market Share of 43.80%, Valued at USD 6.6 Billion

Asia Pacific held a 43.80% share of the global bicycle accessories market in 2025, valued at USD 6.6 Billion. The region’s dominance reflects a combination of the world’s largest bicycle manufacturing base in China and Taiwan, dense urban commuter populations in India and Southeast Asia, and rapid e-bike adoption across multiple national markets. OEM supply chain depth gives regional manufacturers structural cost advantages unavailable to competitors elsewhere.

North America Bicycle Accessories Market Trends

North America is a high-value accessories market driven by strong consumer willingness to spend on premium safety and smart technology products. Urban cycling infrastructure investments across major US cities are converting commuter cyclists into year-round, high-frequency buyers. The aftermarket segment is particularly strong, supported by an established specialty retail network and a growing direct-to-consumer brand ecosystem.

Europe Bicycle Accessories Market Trends

Europe maintains one of the world’s highest cycling participation rates, underpinned by government policy mandates for urban mobility decarbonization. Countries including the Netherlands, Germany, and Denmark sustain structurally high accessory demand through daily commuter use. EU safety regulations governing helmets and lighting standards set a quality floor that elevates average selling prices across both OEM and aftermarket channels.

Latin America Bicycle Accessories Market Trends

Latin America represents a volume-driven market where price accessibility determines adoption rates for bicycle accessories. Brazil and Mexico anchor regional demand through large urban cycling populations and expanding recreational cycling communities. Infrastructure investment in dedicated cycling corridors in cities like Bogotá and São Paulo is gradually shifting buyers from basic utility accessories toward safety and performance products.

Middle East & Africa Bicycle Accessories Market Trends

The Middle East and Africa market is at an early commercialization stage for bicycle accessories, with demand concentrated in South Africa and GCC urban centers. Government-led smart city and wellness initiatives in Saudi Arabia and the UAE are creating structured demand for cycling infrastructure and associated accessories. This positions the region as a longer-term growth market rather than a near-term volume contributor.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Accell Group operates as a multi-brand bicycle and accessories conglomerate with deep distribution networks across European retail and e-bike channels. The company’s structural advantage lies in its ability to cross-sell accessories through its own branded bicycle sales network, reducing customer acquisition costs per accessory unit. However, its heavy Europe concentration creates exposure to regional policy and consumer sentiment shifts that competitors with more diversified geographies do not face.

Garmin Ltd. occupies a distinct technology-led position within the bicycle accessories market, competing on GPS performance, software ecosystem integration, and brand trust built through marine and aviation markets. Its product roadmap for cycling, including purpose-built mountain bike computers and indoor trainer accessories, demonstrates systematic category expansion. Garmin’s software connectivity platform creates switching costs that commodity accessory brands cannot replicate through hardware alone.

Campagnolo S.R.L maintains an exclusive positioning at the performance end of the components market, with a product range targeting professional and high-dedication amateur road cyclists. The brand’s pricing power stems from a heritage of professional racing adoption and precision engineering, which functions as a durable marketing asset. Its narrow target segment limits volume potential but sustains premium margins that mass-market component suppliers cannot achieve.

Giant Manufacturing Co. Ltd. is the world’s largest bicycle manufacturer, and its integrated accessories business benefits from scale advantages in manufacturing, global retail distribution, and OEM supply relationships. Giant’s ability to bundle accessories with new bicycle sales creates a controlled first-purchase moment for its accessory brands. This bundling strategy converts new bike buyers into managed accessory customers before third-party brands enter the consideration set.

Key Players

- Accell Group

- Avon Cycles Ltd.

- Campagnolo S.R.L

- Garmin Ltd.

- Giant Manufacturing Co. Ltd.

- Merida Industry Co. Ltd.

- Specialized Bicycle Components, Inc.

- Trek Bicycle Corp.

- DT Swiss

- Lezyne

- Endura Ltd.

- Eastman Industries

Recent Developments

- September 2025 – Shimano released its first major SPD cleat update in nearly 30 years, introducing a new multi-entry engagement system alongside the RX910 S-Phyre gravel racing shoe for easier pedal clipping.

- July 2025 – SRAM launched upgraded Force and Rival AXS electronic groupsets for road and gravel bicycles, delivering premium-level braking, lighter designs, and advanced shifting technology to mid-tier cyclists.

- June 2025 – Bryton introduced the Rider 650 GPS cycling computer with a full-color touchscreen interface, enhanced navigation capabilities, and improved rider interaction features for performance cyclists.

- May 2026 – Firsthand Framebuilding acquired the intellectual property, tooling, and manufacturing assets of Paragon Machine Works to preserve and expand domestic bicycle component and frame accessory production in North America.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 15.1 Billion |

| Forecast Revenue (2035) | USD 28.7 Billion |

| CAGR (2026-2035) | 6.7% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Apparels, Components), By Bicycle (Road Bikes, Mountain Bikes, Hybrid Bikes, Cargo Bikes, Others), By Type (OEM, Aftermarket), By Sales Channel (Offline, Online) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Accell Group, Avon Cycles Ltd., Campagnolo S.R.L, Garmin Ltd., Giant Manufacturing Co. Ltd., Merida Industry Co. Ltd., Specialized Bicycle Components, Inc., Trek Bicycle Corp., DT Swiss, Lezyne, Endura Ltd., Eastman Industries |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |