Global Automotive Micromotor Market Size, Share, Growth Analysis By Motor (Brushed DC Motors, Brushless DC Motors, Stepper Motors), By Power Consumption (3V–12V, 12V–24V, 25V–48V, More than 48V), By Vehicle (Passenger Cars, Commercial Vehicles), By Application (Power Windows, Windshield Wipers, Electric Power Steering, Seat Adjustments, Mirror Adjustments, Sunroof Actuators, HVAC Systems, Others), By Sales Channel (OEM, Aftermarket), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 179878

- Number of Pages: 325

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

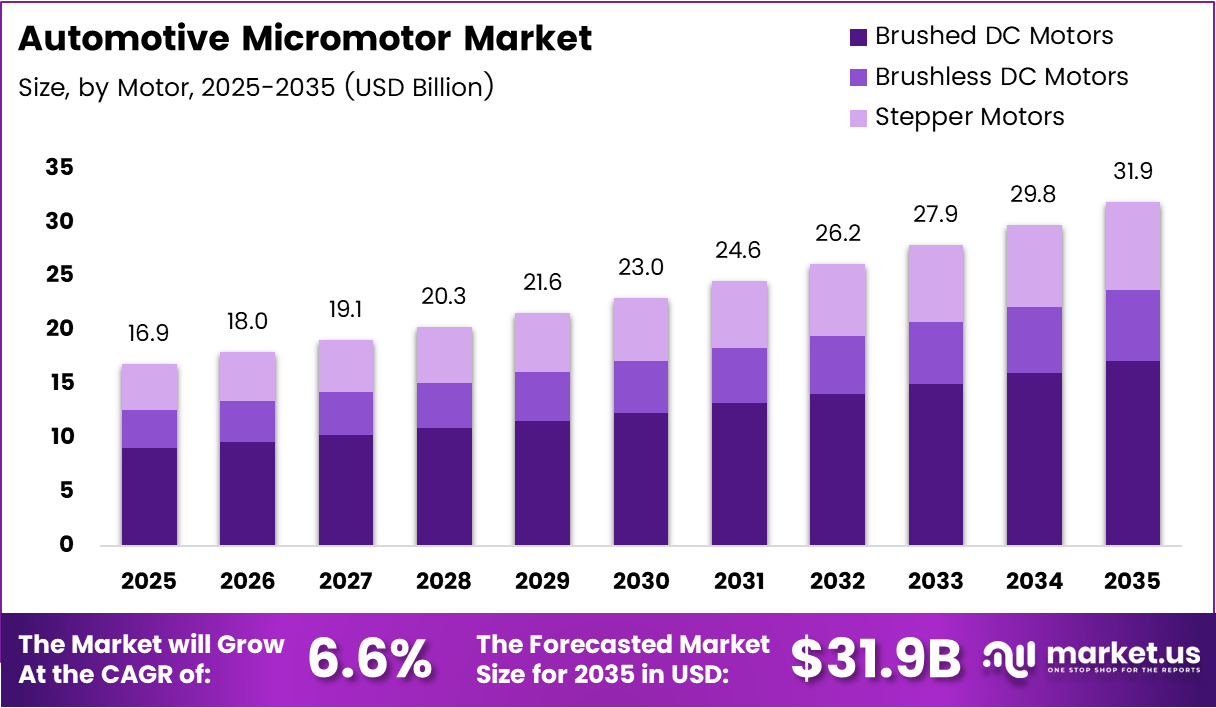

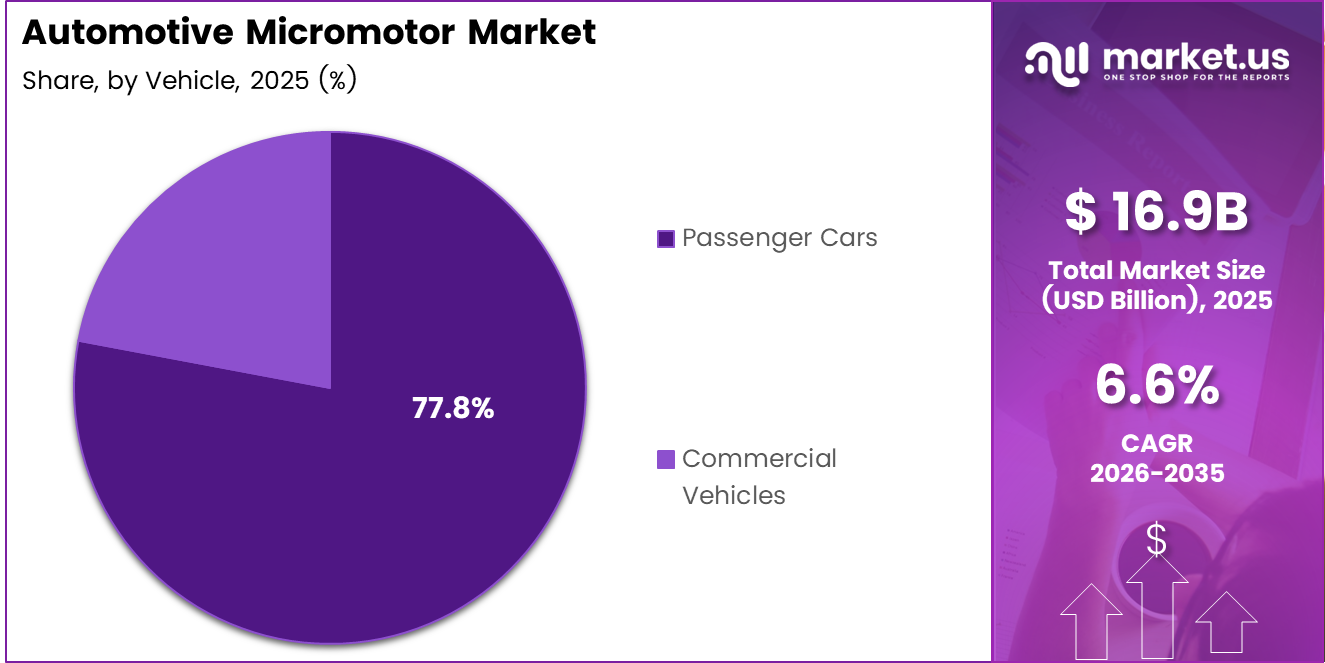

Global Automotive Micromotor Market size is expected to be worth around USD 31.9 Billion by 2035 from USD 16.9 Billion in 2025, growing at a CAGR of 6.6% during the forecast period 2026 to 2035.

Automotive micromotors are compact electromechanical devices that power a broad set of vehicle functions — from power windows and seat adjustments to electric power steering and HVAC actuators. These precision components sit at the intersection of mechanical performance and electrical efficiency, making them structurally essential as vehicles add more motorized functions per platform.

The market spans brushed DC, brushless DC, and stepper motor technologies, each serving distinct vehicle applications. Brushed DC motors dominate current deployments with a 53.7% share, while brushless variants attract investment for next-generation platforms. This split signals a market in active technology transition — one where incumbents face pressure to upgrade product lines or risk losing design wins to more efficient alternatives.

Passenger cars account for 77.8% of vehicle demand for micromotors, reflecting the scale advantage of high-volume production and the accelerating feature density per car. As automakers compete on in-cabin experience, each new comfort or safety feature adds one or more micromotor units to the bill of materials — compounding unit demand per vehicle cycle.

OEM channels control 87.4% of micromotor sales, which tells a specific story about how this market operates: design-in relationships and long-term supply contracts dominate procurement decisions. For suppliers, this creates high barriers to entry but also high switching costs — once qualified in a platform, the revenue is sticky across a multi-year production cycle.

The electrification of the global vehicle fleet is the clearest structural force reshaping micromotor demand. According to the IEA, 18% of all new cars sold globally in 2023 were electric — a figure that directly translates to more micromotors per vehicle, given that EVs require additional actuators for battery thermal management, charging mechanisms, and sensor systems not present in combustion platforms.

According to Our World in Data, more than 22% of new cars sold globally in 2024 were electric — a year-on-year acceleration that reinforces the structural demand shift. For micromotor suppliers, this trajectory means EV-specific design requirements are no longer niche engineering challenges but core product development priorities demanding immediate R&D reallocation.

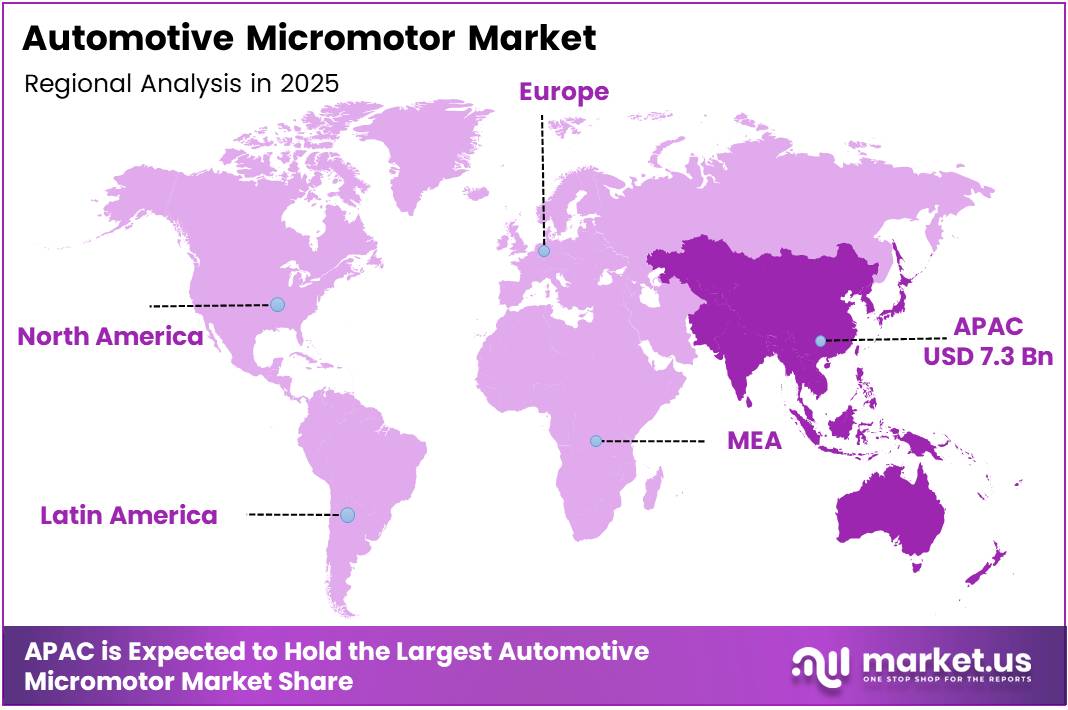

Asia Pacific anchors the market with a 43.7% share, valued at USD 7.3 Billion, driven by high-volume automotive production across China, Japan, South Korea, and India. The region’s combination of established OEM supply chains and rapidly expanding EV manufacturing capacity makes it the most consequential geography for micromotor sourcing strategies over the forecast period.

Key Takeaways

- The global Automotive Micromotor Market was valued at USD 16.9 Billion in 2025 and is forecast to reach USD 31.9 Billion by 2035, at a CAGR of 6.6%.

- By Motor, Brushed DC Motors lead with a 53.7% share in 2025.

- By Power Consumption, the 3V–12V segment holds the largest share at 41.5%.

- By Vehicle, Passenger Cars dominate with a 77.8% share, with SUVs, Sedans, and Hatchbacks as key sub-segments.

- By Application, Power Windows holds the largest share at 23.3%.

- By Sales Channel, OEM accounts for 87.4% of total market revenue.

- Asia Pacific leads all regions with a 43.7% share, valued at USD 7.3 Billion in 2025.

Motor Analysis

Brushed DC Motors dominate with 53.7% due to low cost and wide platform compatibility.

In 2025, Brushed DC Motors held a dominant market position in the By Motor segment of the Automotive Micromotor Market, with a 53.7% share. Their cost-per-unit advantage and ease of integration into existing vehicle electrical architectures make them the default choice for high-volume OEM procurement across passenger car platforms.

Brushless DC Motors carry the highest margin within the motor segment and attract the strongest R&D investment. These units eliminate brush wear, extending operational life in demanding automotive environments. As EV platforms prioritize reliability and energy efficiency, brushless designs increasingly win new design-in qualifications — positioning suppliers in this sub-segment for disproportionate share of next-cycle OEM contracts.

Stepper Motors serve precision-control applications where position accuracy outweighs cost sensitivity. Their role in HVAC valve control, mirror positioning, and instrument actuators is structurally protected — no alternative motor type replicates their step-based control behavior. Consequently, stepper motor demand correlates directly with comfort and control feature density per vehicle, an area where automakers continue to add specification.

Power Consumption Analysis

3V–12V dominates with 41.5% due to compatibility with standard 12V vehicle electrical systems.

In 2025, the 3V–12V segment held a dominant market position in the By Power Consumption segment of the Automotive Micromotor Market, with a 41.5% share. The overwhelming installed base of 12V electrical architectures in conventional passenger cars makes this voltage band the default specification for most interior and body-function micromotors.

The 12V–24V segment serves commercial vehicle applications where higher torque requirements exceed the capacity of standard 12V systems. Light and medium commercial vehicles sourcing from this band benefit from greater actuation force with manageable thermal loads. Suppliers serving this range occupy a differentiated position between standard passenger and heavy-duty vehicle requirements.

The 25V–48V segment reflects a structural shift now underway in premium and hybrid vehicle platforms. The 48V mild-hybrid architecture enables higher-performance micro actuation — including electric power steering and active suspension components — without the full-voltage costs of battery-electric platforms. This band is where the most technically competitive product development is currently concentrated.

The More than 48V segment addresses full battery-electric vehicle applications, where high-voltage architectures power primary drive and auxiliary systems simultaneously. While volumetrically smaller today, this band will capture a larger portion of new design wins as EV adoption accelerates and automakers standardize high-voltage component sourcing. Suppliers entering now benefit from early qualification advantages before the segment scales.

Vehicle Analysis

Passenger Cars dominate with 77.8% due to high unit volume and rising per-vehicle feature density.

In 2025, Passenger Cars held a dominant market position in the By Vehicle segment of the Automotive Micromotor Market, with a 77.8% share. The combination of global production scale and accelerating comfort and safety feature content per vehicle makes passenger cars the primary volume driver for micromotor sourcing across all motor types and voltage bands.

SUVs differentiate through premium feature loading that drives above-average micromotor unit content per vehicle. Sunroof actuators, multi-zone HVAC systems, and power-adjustable seating are standard in most SUV configurations — each adding micromotor units to the bill of materials. SUV segment growth consequently benefits micromotor suppliers disproportionately compared to entry-level passenger car segments.

Sedans serve as the volume backbone of passenger car production in Asia and emerging markets, where standardized comfort features drive steady, predictable micromotor demand. Their well-defined feature architecture allows suppliers to optimize production for high-volume, cost-sensitive OEM contracts — making sedans a reliable volume anchor even as premium segments attract more R&D attention.

Hatchbacks function as the entry-level micromotor deployment platform, typically featuring fewer actuated functions than SUVs or premium sedans. However, as automakers push comfort features into lower price points to remain competitive, hatchback micromotor content per unit is gradually rising — creating a slow but structurally meaningful volume expansion in the segment.

Commercial Vehicles represent a structurally distinct demand category, where durability and torque requirements exceed passenger car specifications. Fleet operators and OEM procurement teams prioritize service life and reliability over feature richness, which means commercial vehicle micromotors command different design and testing standards — and typically higher per-unit prices reflecting those requirements.

LCVs (Light Commercial Vehicles) account for the largest share within commercial vehicle micromotors, driven by the global expansion of last-mile delivery and small fleet operations. Their proximity to passenger car specifications allows some component overlap, giving suppliers serving both segments a cost efficiency advantage in design and manufacturing.

MCVs (Medium Commercial Vehicles) serve regional freight and specialized transport applications where power window, mirror, and HVAC actuation are standard fitments. This sub-segment offers stable micromotor demand tied to infrastructure investment cycles in construction, logistics, and municipal services — sectors that run on different procurement timelines than consumer automotive.

HCVs (Heavy Commercial Vehicles) require the most robust micromotor specifications, with thermal tolerance and vibration resistance as primary design criteria. Demand in this sub-segment correlates strongly with freight activity and commercial fleet renewal rates. While lower in unit volume, HCV micromotors carry higher per-unit value — making the sub-segment attractive for suppliers with specialized manufacturing capability.

Application Analysis

Power Windows dominate with 23.3% due to universal fitment across all passenger vehicle segments.

In 2025, Power Windows held a dominant market position in the By Application segment of the Automotive Micromotor Market, with a 23.3% share. Their near-universal presence across passenger car segments makes power window actuators the single largest application category by volume — and the most price-competitive segment, where supplier scale and cost efficiency determine contract outcomes.

Windshield Wipers represent a safety-critical application where performance standards are set by regulatory requirements rather than optional feature tiers. Every passenger and commercial vehicle requires wiper actuation, creating a non-discretionary demand base. For micromotor suppliers, wiper actuation is a stable, low-risk volume category with predictable OEM replacement cycles.

Electric Power Steering (EPS) carries the highest functional criticality among micromotor applications, directly affecting vehicle controllability. Regulatory mandates for EPS adoption — tied to fuel efficiency and emissions standards — drive replacement of hydraulic systems across new platforms. This application demands the tightest performance specifications, giving qualified suppliers a durable competitive position once design-in approval is secured.

Seat Adjustments reflect automakers’ investment in interior differentiation, particularly in premium and SUV segments where multi-directional power seating is a competitive specification. Each power seat axis requires a dedicated micromotor, meaning premium trim levels can contain four to eight seat adjustment units per vehicle — making seat actuators a high-unit-count application relative to other comfort features.

Mirror Adjustments provide a standardized comfort and safety function now present across most passenger vehicle segments globally. The application’s regulatory overlap — mirrors are increasingly integrated with camera and blind-spot systems — means mirror actuator design complexity is rising. Suppliers embedding positioning precision into mirror actuators open a path into adjacent ADAS-linked hardware.

Sunroof Actuators serve a premium feature segment where consumer preference for panoramic and sliding roofs drives per-vehicle micromotor content higher. Sunroof penetration rates are rising across mid-range and premium passenger cars in Asia and Europe, making this application one of the faster-growing sub-categories by unit volume within the comfort actuation space.

HVAC Systems integrate multiple micromotors for air distribution, temperature zone control, and valve actuation. In electric vehicles, HVAC efficiency directly impacts battery range — making thermal management actuator precision a more technically demanding and higher-value specification than in combustion vehicles. EV adoption consequently upgrades the engineering and commercial importance of HVAC micromotor sourcing.

Others encompass emerging actuation applications including active grille shutters, door cinch systems, and fuel filler actuators. These lower-volume but structurally growing applications benefit from the broader trend of motorizing vehicle functions previously operated mechanically — extending the total addressable unit count per vehicle platform over successive model generations.

Sales Channel Analysis

OEM dominates with 87.4% due to long-term supply contracts and platform-level design integration.

In 2025, the OEM channel held a dominant market position in the By Sales Channel segment of the Automotive Micromotor Market, with an 87.4% share. Design-in qualification processes and platform-specific engineering lock suppliers into multi-year OEM contracts — creating a supply structure where established relationships and technical certification act as the primary competitive barrier.

The Aftermarket channel captures replacement demand from vehicles outside warranty, particularly in older fleets where original micromotor components reach end-of-life. While significantly smaller by revenue share, aftermarket margins are typically higher than OEM pricing, offering suppliers a complementary revenue stream. Price sensitivity and fitment compatibility are the primary factors that determine aftermarket supplier selection.

Key Market Segments

By Motor

- Brushed DC Motors

- Brushless DC Motors

- Stepper Motors

By Power Consumption

- 3V–12V

- 12V–24V

- 25V–48V

- More than 48V

By Vehicle

By Application

- Power Windows

- Windshield Wipers

- Electric Power Steering (EPS)

- Seat Adjustments

- Mirror Adjustments

- Sunroof Actuators

- HVAC Systems

- Others

By Sales Channel

- OEM

- Aftermarket

Drivers

Vehicle Electrification and ADAS Expansion Drive Micromotor Demand Across Passenger and Commercial Platforms

Electric vehicle adoption is restructurally expanding the micromotor unit count per vehicle. According to the IEA, nearly 14 million new electric cars were registered globally in 2023. Each EV platform requires micromotors for battery thermal management, charging lock actuators, and sensor positioning systems absent in combustion vehicles — directly compounding per-unit demand beyond traditional body-function applications.

ADAS integration amplifies this demand further. Between 8% and 25% of U.S. vehicles carried ADAS features in 2022, according to ResearchGate — a penetration range that signals ADAS is crossing from premium fitment into mainstream adoption. Each ADAS function requiring physical actuation, from sensor cleaning to mirror repositioning, adds dedicated micromotor units to the vehicle architecture.

In June 2024, Mabuchi Motor announced the acquisition of OKI Micro Engineering’s small motor business, signaling that leading suppliers view the ADAS actuation opportunity as significant enough to expand capacity through acquisition rather than organic growth alone.

Automotive safety regulations compound both forces. Mandates for motorized safety mechanisms — including automatic emergency braking actuators and electronic parking systems — convert previously optional micromotor applications into regulatory requirements. This regulatory-driven conversion is the most durable demand mechanism in the market because it is non-cyclical: automakers must comply regardless of consumer feature preference or economic conditions.

Restraints

Raw Material Cost Volatility and Thermal Complexity Constrain Micromotor Margin and Design Scalability

Rare earth magnet and copper price volatility creates direct margin pressure for micromotor manufacturers. These two inputs are non-substitutable in most motor designs — particularly brushless DC and stepper motors where magnet performance determines efficiency output. When commodity prices spike, suppliers face a choice between absorbing margin compression or renegotiating OEM contracts that typically lock pricing for multi-year platform cycles.

Miniaturization compounds this cost challenge by increasing thermal management complexity. As automakers require smaller motor packages with higher power density, heat dissipation per unit volume rises — demanding more sophisticated thermal design and higher-grade materials. This engineering requirement adds development cost and extends qualification timelines, creating a structural barrier that disadvantages smaller suppliers without dedicated thermal engineering capability.

Together, these two restraints reinforce each other: a commodity price spike hits margins at the same time that thermal redesign budgets are elevated. Suppliers managing both simultaneously face capital allocation conflicts that slow product development cycles — a risk that is most acute for companies serving multiple vehicle platforms with distinct specification requirements and limited engineering bandwidth to address both challenges concurrently.

Growth Factors

EV Battery Thermal Systems, Autonomous Sensor Mechanisms, and Emerging Market OEM Expansion Open New Micromotor Revenue Streams

Electric vehicle battery thermal management is a structurally new demand category for micromotors, requiring precision actuation for coolant valves, pump controls, and airflow management within battery enclosures. In March 2024, Nidec Corporation announced development of a new automotive air suspension motor targeting vehicle comfort systems — illustrating how tier-one suppliers are already extending their micromotor portfolios into EV-specific thermal and ride-control applications. This development signals that EV platform requirements are now influencing mainstream supplier R&D roadmaps.

Autonomous vehicle sensor systems create an adjacent demand layer. Camera cleaning mechanisms, radar positioning actuators, and lidar adjustment systems all require micromotors with high cycle life and contamination resistance. According to ScienceDirect, more than 50% of European vehicles are projected to carry ADAS features by 2030 — a deployment target that confirms sensor actuation will become a standard-fitment requirement rather than a premium add-on within this decade.

Emerging market OEM expansion adds a volume dimension to these technology-driven opportunities. Automotive production growth in India, Southeast Asia, and Latin America extends OEM sourcing networks into new geographies — creating entry points for micromotor suppliers to establish regional supply relationships before local production volumes mature. Suppliers that qualify with OEM platforms early in a new production region capture design-in advantages that typically persist across multiple vehicle generation cycles.

Emerging Trends

Brushless Technology Adoption, Smart Motor Integration, and 48V Architecture Expansion Redefine Automotive Micromotor Performance Standards

The transition from brushed to brushless and coreless micromotor designs is a supplier-level strategic imperative, not merely a technical preference. Brushless motors eliminate mechanical wear at the commutation point — extending service life in high-cycle applications like seat adjustment and HVAC actuation. According to Reuters, 95.9% of new cars sold in Norway in 2025 were electric — a market that already demands brushless standards as the default, signaling where global OEM specifications are heading as EV penetration rises in other regions.

Smart control electronics embedded within micromotor assemblies represent the next integration frontier. Combining position sensing, speed feedback, and fault detection within the motor package reduces system complexity and improves diagnostic capability for OEMs. This convergence of mechanical and electronic functions shifts competitive advantage from motor manufacturing alone toward integrated system design — favoring suppliers with electronics engineering capability alongside precision motor production.

The expansion of 48V mild-hybrid electrical architectures creates a specific product development opportunity. Higher-voltage systems enable actuation functions — including active chassis control and advanced EPS — that cannot be efficiently powered at 12V. Suppliers developing 48V-optimized micromotors now position themselves for design wins on the next wave of electrified platforms, where 48V architecture is becoming a standard specification in European and Asian premium vehicle programs.

Regional Analysis

Asia Pacific Dominates the Automotive Micromotor Market with a Market Share of 43.7%, Valued at USD 7.3 Billion

Asia Pacific commands a 43.7% share of the global automotive micromotor market, valued at USD 7.3 Billion in 2025. China, Japan, South Korea, and India collectively represent the world’s highest concentration of automotive OEM and tier-one supplier activity. The region’s combination of domestic vehicle production scale and aggressive EV manufacturing investment makes it the structural center of gravity for global micromotor procurement decisions.

North America Automotive Micromotor Market Trends

North America maintains a significant market position, driven by strong passenger car production in the U.S. and Mexico, alongside sustained OEM investment in electrified platforms. ADAS regulatory momentum and federal EV incentive programs accelerate micromotor content per vehicle — making North America a high-value market for suppliers capable of meeting both volume and technical specification requirements.

Europe Automotive Micromotor Market Trends

Europe advances micromotor adoption through stringent CO2 emission targets that accelerate 48V mild-hybrid and full-EV platform development. Germany, France, and the UK concentrate the highest share of premium vehicle production where per-vehicle micromotor content is structurally elevated. Regulatory pressure on fleet emissions makes European OEMs the fastest adopters of energy-efficient brushless micromotor specifications.

Latin America Automotive Micromotor Market Trends

Latin America functions as an emerging OEM production and sourcing region, with Brazil and Mexico anchoring automotive manufacturing activity. Mexico’s proximity to U.S. OEM supply chains and its established auto parts export infrastructure position it as a growing micromotor sourcing hub. Rising domestic vehicle sales in Brazil create incremental aftermarket demand that complements OEM supply growth.

Middle East and Africa Automotive Micromotor Market Trends

The Middle East and Africa represent an early-stage but structurally developing market for automotive micromotors. GCC countries show demand for premium passenger vehicles with high comfort feature content, supporting above-average per-vehicle micromotor unit requirements. Infrastructure investment and fleet modernization programs across South Africa and Gulf states provide a gradual but consistent demand foundation.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Robert Bosch GmbH leverages its integrated automotive systems platform to position micromotors as part of broader mechatronic assemblies rather than standalone components. This bundling strategy gives Bosch a procurement advantage: OEMs sourcing steering, braking, and HVAC systems from a single supplier face higher switching costs across all product lines — making Bosch’s micromotor position structurally more defensible than that of pure-play motor specialists.

Constar MicroMotor competes on specialized precision motor design for applications requiring high torque density within constrained physical envelopes. Their focus on application-specific engineering — rather than catalogue-based supply — positions them to serve emerging EV actuation requirements where standard motor specifications do not meet packaging or performance demands. This specialization creates a differentiated value proposition in technically demanding design-in processes.

Buhler Group applies manufacturing process expertise to micromotor component production, with strength in the precision die-casting and forming processes that determine motor housing accuracy and thermal performance. Their upstream manufacturing position means they influence motor quality at the component level — a structural advantage in markets where dimensional tolerance directly impacts motor efficiency and end-of-life reliability.

Johnson Electric Holdings Limited brings global manufacturing scale and platform diversification across automotive and industrial micromotor applications. In April 2025, Johnson Electric launched an EV locking actuator designed for safe and secure EV charging — demonstrating that the company is actively converting its motor design capability into EV-specific application products. This development signals a deliberate portfolio shift toward high-growth EV infrastructure adjacent markets.

Key Players

- Robert Bosch GmbH

- Constar MicroMotor

- Buhler Group

- Johnson Electric Holdings Limited

- NIDEC CORPORATION

- Brose Fahrzeugteile GmbH & Co. KG

- Mitsuba Corp.

- MABUCHI MOTOR CO., LTD

- Valeo SA

- Denso Corporation

- Maxon

Recent Developments

- July 2025 – Mabuchi Motor completed its acquisition of OKI Micro Engineering’s small motor business and established a new subsidiary, MABUCHI MOTOR MICRO TECH CO., LTD. This move expands Mabuchi’s precision motor manufacturing capability and consolidates its position in the compact automotive motor segment.

- January 2025 – Nidec Corporation inaugurated an expanded manufacturing facility in Reynosa, Mexico, following a USD 23 million investment. The facility expansion strengthens Nidec’s North American production capacity to serve growing OEM demand across the region’s automotive manufacturing base.

- April 2025 – Johnson Electric launched an innovative electric vehicle locking actuator designed specifically for safe and secure EV charging applications. The product targets the expanding EV infrastructure market, extending Johnson Electric’s micromotor expertise into a structurally adjacent and fast-scaling application segment.

Report Scope

Report Features Description Market Value (2025) USD 16.9 Billion Forecast Revenue (2035) USD 31.9 Billion CAGR (2026-2035) 6.6% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Motor (Brushed DC Motors, Brushless DC Motors, Stepper Motors), By Power Consumption (3V–12V, 12V–24V, 25V–48V, More than 48V), By Vehicle (Passenger Cars, Commercial Vehicles), By Application (Power Windows, Windshield Wipers, Electric Power Steering, Seat Adjustments, Mirror Adjustments, Sunroof Actuators, HVAC Systems, Others), By Sales Channel (OEM, Aftermarket) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Robert Bosch GmbH, Constar MicroMotor, Buhler Group, Johnson Electric Holdings Limited, NIDEC CORPORATION, Brose Fahrzeugteile GmbH & Co. KG, Mitsuba Corp., MABUCHI MOTOR CO., LTD, Valeo SA, Denso Corporation, Maxon Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Automotive Micromotor MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample

Automotive Micromotor MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Robert Bosch GmbH

- Constar MicroMotor

- Buhler Group

- Johnson Electric Holdings Limited

- NIDEC CORPORATION

- Brose Fahrzeugteile GmbH & Co. KG

- Mitsuba Corp.

- MABUCHI MOTOR CO., LTD

- Valeo SA

- Denso Corporation

- Maxon

Our Clients

- 179878

- Feb 2026