Quick Navigation

Report Overview

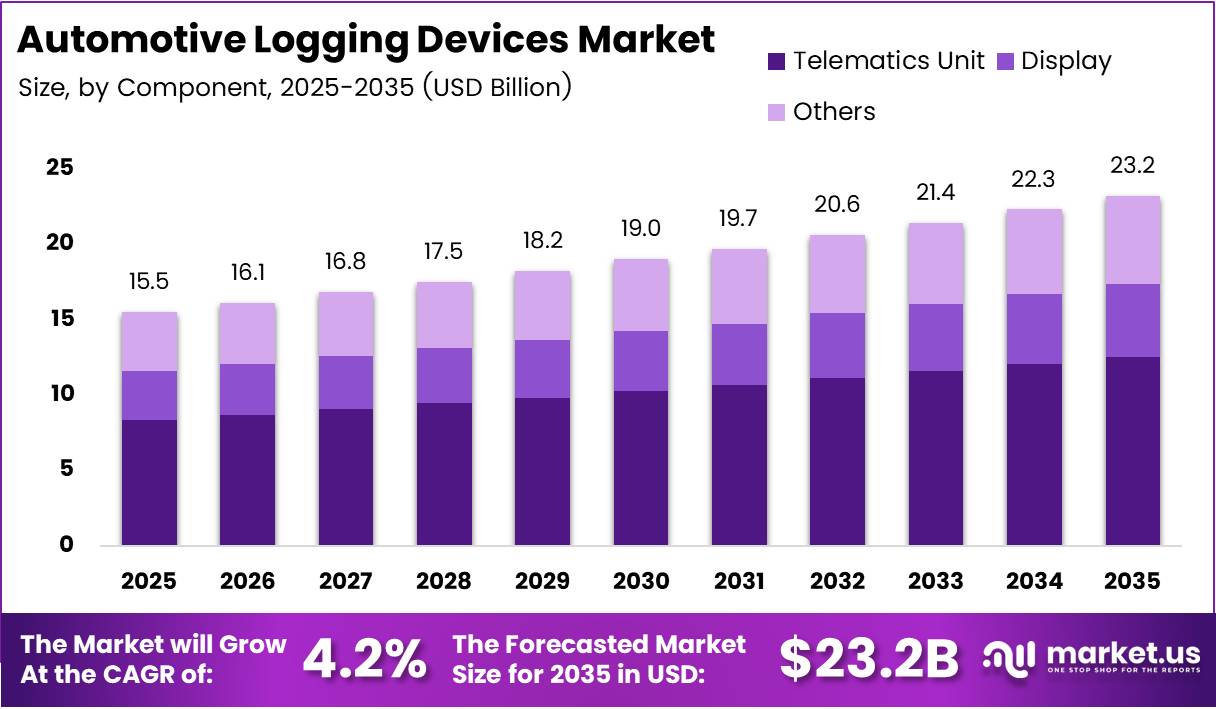

Global Automotive Logging Devices Market size is expected to be worth around USD 23.2 Billion by 2035 from USD 15.5 Billion in 2025, growing at a CAGR of 4.2% during the forecast period 2026 to 2035.

Automotive logging devices capture vehicle location, engine performance, driver hours, and compliance data across commercial fleets. These systems connect physical vehicle activity to digital records that fleet managers, insurers, and regulators rely on. The technology forms the operational backbone of modern freight, logistics, and transportation networks.

Government mandates define the demand floor for this market. Electronic logging devices are federally required for interstate commercial drivers under regulations established through MAP-21 legislation enacted in 2012. This federal requirement converts every regulated commercial vehicle into a guaranteed unit of demand, removing discretionary purchase risk for vendors with compliant products.

Compliance pressure intensifies the replacement cycle across the market. According to FMCSA, 12 electronic logging devices were removed from the registered devices list in May 2026 due to non-compliance. Each removal forces affected fleets to procure compliant replacements, creating recurring procurement events that sustain vendor revenue independent of organic fleet growth.

Enforcement actions carry a strict timeline. Fleets using the 12 revoked ELDs in 2026 were required to replace them within 60 days. This compressed replacement window prevents fleet operators from deferring purchases. Vendors with inventory depth and rapid provisioning capability capture disproportionate share during each enforcement cycle.

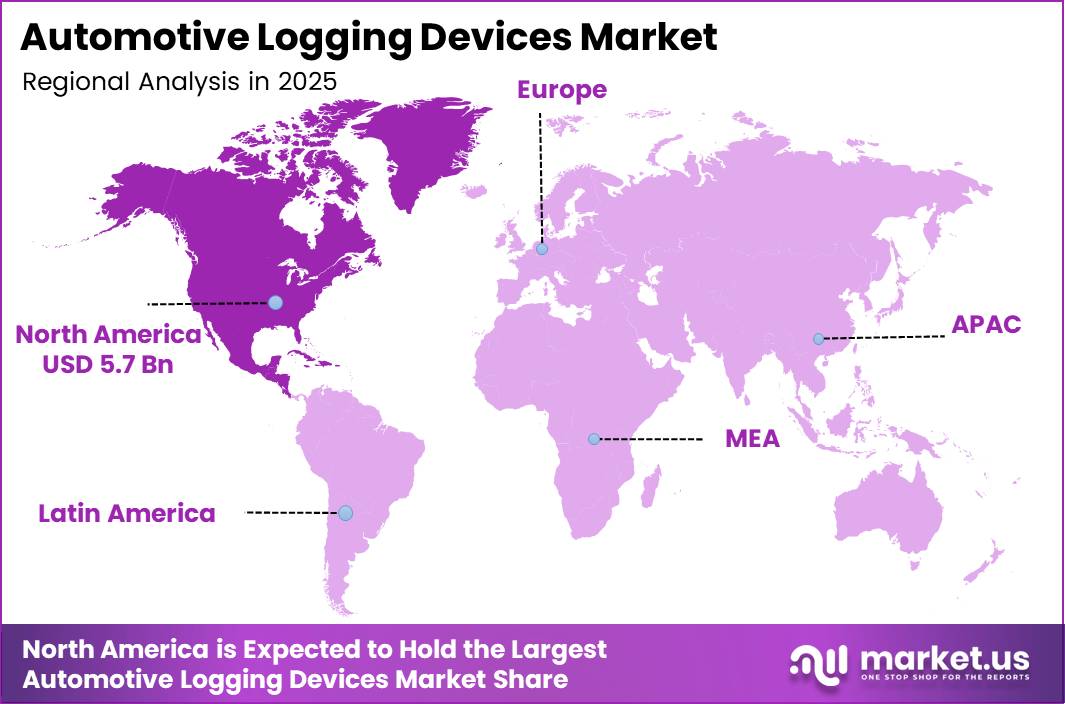

North America anchors market value. The region holds a 36.80% share, valued at USD 5.7 Billion, driven by dense regulatory infrastructure and large commercial fleet counts. However, logistics digitization in Asia Pacific and Latin America signals that the next growth phase will extend well beyond the North American compliance baseline.

The telematics unit segment holds a 53.8% component share, reflecting fleet operator preference for integrated hardware that combines tracking, communication, and compliance functions in a single device. Trucks account for 51.1% of vehicle-type demand, confirming that long-haul freight remains the primary commercial use case for logging device deployment.

Key Takeaways

- The Automotive Logging Devices Market is valued at USD 15.5 Billion in 2025 and will reach USD 23.2 Billion by 2035.

- The market grows at a CAGR of 4.2% during the forecast period 2026 to 2035.

- North America leads all regions with a 36.80% market share, valued at USD 5.7 Billion.

- By Component, Telematics Unit is the dominant segment with a 53.8% share.

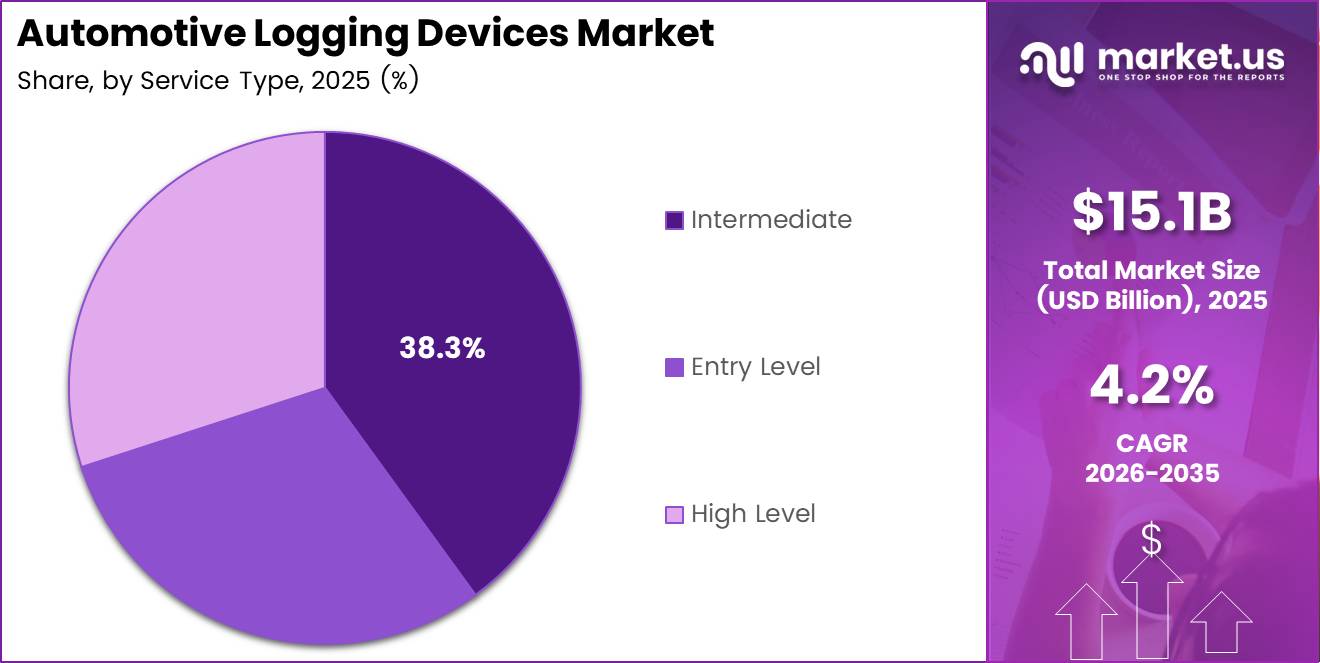

- By Service Type, Intermediate leads with a 38.3% share.

- By Form Factor, Embedded devices dominate with a 61.5% share.

- By Vehicle Type, Trucks hold the largest share at 51.1%.

- FMCSA removed 12 non-compliant ELDs from its registry in May 2026, triggering mandatory fleet replacements.

Component Analysis

Telematics Unit dominates with 53.8% due to combined tracking, compliance, and data functions.

In 2025, Telematics Unit held a dominant market position in the By Component segment of the Automotive Logging Devices Market, with a 53.8% share. Fleet operators prefer all-in-one units that handle hours-of-service logging, GPS tracking, and engine diagnostics simultaneously. This consolidation reduces onboard hardware complexity and lowers total cost of compliance.

Display components serve as the driver-facing interface in ELD-equipped vehicles. Drivers interact with display modules to confirm duty status, review violations, and acknowledge inspection requests. As regulations require clear data presentation to enforcement officers, display quality directly affects compliance outcomes and roadside inspection results.

Others in the component segment include communication modules, sensors, and connectivity hardware that support data transmission between the vehicle and fleet management platforms. These components enable real-time reporting and cloud integration. Their role becomes more critical as fleets adopt advanced telematics platforms requiring continuous data uplinks.

Service Type Analysis

Intermediate dominates with 38.3% due to balance of compliance coverage and cost efficiency.

In 2025, Intermediate held a dominant market position in the By Service Type segment of the Automotive Logging Devices Market, with a 38.3% share. Mid-tier service plans deliver core ELD compliance functions alongside basic fleet visibility tools. Fleet operators managing mixed vehicle types find intermediate plans the most practical without overcommitting to enterprise-grade costs.

Entry Level service plans target owner-operators and small fleets that need basic hours-of-service compliance without additional telematics features. These plans lower the financial barrier for regulatory adherence. However, they offer limited data analytics, which restricts their appeal to fleets with more than a handful of vehicles seeking operational insight.

High Level service plans support large fleet operators requiring advanced analytics, driver behavior monitoring, and predictive maintenance integration. According to FMCSA, fleets using revoked ELDs in 2026 were given 60 days to replace devices. This compliance pressure pushes larger operators toward high-level plans that include proactive compliance monitoring and automated alerts.

In February 2025, Geotab launched GO Focus, an AI-powered safety sensor integrated with its GO Device platform to improve driver safety while addressing fleet privacy and compliance concerns. This launch signals that high-level service offerings will increasingly embed AI-driven safety tools as a differentiating feature above entry and intermediate tiers.

Form Factor Analysis

Embedded dominates with 61.5% due to OEM integration and tamper-resistant compliance design.

In 2025, Embedded held a dominant market position in the By Form Factor segment of the Automotive Logging Devices Market, with a 61.5% share. Original equipment manufacturers increasingly install logging hardware directly into vehicle architecture during production. This approach eliminates aftermarket installation costs and ensures regulatory compliance from the vehicle’s first operational day.

Integrated form factor devices combine logging functionality with existing onboard vehicle systems such as infotainment or telematics control units. Fleet operators retrofitting older vehicles favor integrated solutions that minimize new hardware footprint. This segment captures demand from fleets managing legacy vehicle populations that require compliance upgrades without full hardware replacement.

Vehicle Type Analysis

Trucks dominate with 51.1% due to federal HOS mandate applicability across interstate freight.

In 2025, Trucks held a dominant market position in the By Vehicle Type segment of the Automotive Logging Devices Market, with a 51.1% share. Long-haul trucking operates under the most stringent federal hours-of-service rules. Every regulated truck represents a legally mandated ELD installation, making the segment immune to discretionary budget pressures that affect other vehicle categories.

Light Commercial Vehicles include delivery vans and pickup trucks used in last-mile logistics and service operations. ELD adoption in this category reflects voluntary fleet digitization rather than hard regulatory requirements in most jurisdictions. However, expanding state-level telematics incentives and insurance-linked monitoring programs are pulling this segment toward higher adoption rates.

Bus operators require logging devices to track driver duty hours on fixed-route and charter services. Regulatory frameworks for bus fleets differ from freight trucking but share the core compliance objective of preventing fatigued driving. Urban transit authorities and private charter operators represent distinct procurement channels within this sub-segment.

Cars represent the smallest vehicle type segment in this market. Corporate fleet programs and ride-share compliance monitoring drive the limited demand for logging devices in passenger cars. As gig economy platforms face increasing regulatory scrutiny around driver hours, car-category demand could expand beyond its current marginal position.

Key Market Segments

By Component

- Telematics Unit

- Display

- Others

By Service Type

- Intermediate

- Entry Level

- High Level

By Form Factor

- Embedded

- Integrated

By Vehicle Type

- Trucks

- Light Commercial Vehicles

- Bus

- Cars

Drivers

Federal ELD Mandates and FMCSA Enforcement Create a Non-Discretionary Demand Floor for Logging Devices

Electronic logging devices are federally mandated for interstate commercial drivers under MAP-21 legislation. This mandate eliminates voluntary purchasing decisions across regulated fleets and converts compliance into a baseline procurement requirement. Vendors meeting FMCSA technical standards compete on features and price within a structurally guaranteed customer base.

According to FMCSA, 8 ELD devices were revoked in May 2025 for failing federal technical compliance requirements. Each revocation forces affected fleets to re-procure compliant alternatives within 60 days. This enforcement cycle creates recurring demand spikes that supplement the steady-state replacement market driven by fleet expansion and vehicle lifecycle turnover.

In January 2025, Verizon Connect launched Extended View Cameras and a customizable Driver Vehicle Inspection Report solution to improve fleet safety, compliance, and operational efficiency for ELD-enabled fleets. This product expansion shows that vendors treat compliance-driven procurement as the entry point for upselling broader fleet safety and analytics solutions, extending revenue per customer beyond the core logging device purchase.

Restraints

High Platform Costs and Cybersecurity Vulnerabilities Limit ELD Adoption Across Small and Mid-Tier Fleet Operators

Advanced logging device platforms carry significant upfront hardware costs and recurring subscription expenses that strain the budgets of small fleet operators. Owner-operators and regional carriers with fewer than 20 vehicles find enterprise-grade telematics platforms economically difficult to justify. This cost barrier concentrates premium ELD adoption among larger national fleet operators.

According to FMCSA, 6 ELD devices were removed from the approved registry in January 2025 for non-compliance. Each removal disrupts fleet operations and introduces transition costs beyond the original hardware investment. Operators that selected non-compliant vendors absorb replacement hardware, re-provisioning labor, and potential Hours-of-Service gap exposure during the transition window.

Data privacy and cybersecurity risks further complicate fleet-wide ELD deployment. Connected logging devices transmit continuous location, driver behavior, and engine data through cellular and cloud networks. Fleet operators face growing exposure to data breaches targeting telematics platforms. Vendors that cannot demonstrate security certification lose bids to competitors with documented cybersecurity compliance frameworks.

Growth Factors

Cloud Analytics, EV Fleet Integration, and Predictive Maintenance Features Expand the Revenue Addressable Market

Cloud-based fleet analytics platforms convert raw ELD data into actionable operational intelligence. Fleet managers use this data to reduce fuel costs, optimize routes, and identify high-risk drivers before incidents occur. According to FMCSA, 5 ELD products were removed from the registry in October 2025 for failing compliance requirements, reinforcing that cloud-based compliance monitoring represents a growth layer above basic logging hardware.

In March 2025, Geotab introduced Driver Risk Insights, Maintenance Center enhancements, IOX-Keybox, and Cold Chain monitoring solutions at Geotab Connect 2025. These innovations demonstrate that logging device platforms are expanding beyond hours-of-service compliance into full-spectrum fleet intelligence tools. This functional expansion increases platform stickiness and raises switching costs for fleet customers.

Electric and connected commercial vehicle adoption creates new logging system requirements that legacy ELD hardware cannot fulfill. EV fleet operators require energy consumption tracking, charging event logging, and battery health data alongside traditional location and compliance records. Vendors that build EV-native logging capabilities into their platforms now position themselves to capture a structurally differentiated segment within the broader fleet market.

Emerging Trends

AI-Powered Safety Integration and SaaS Fleet Models Are Redefining the Commercial Value of Logging Platforms

Integrated dashcam and AI safety systems are merging with logging device platforms, converting compliance hardware into active safety infrastructure. Fleet operators increasingly demand video context alongside hours-of-service data to defend against liability claims and reduce insurance premiums. According to FMCSA, 5 additional ELD devices were revoked in November 2025 for non-compliance with Title 49 CFR Appendix A requirements, reinforcing that hardware quality and certification standards now gate market access.

Mobile app-based fleet compliance tools are reshaping driver interaction with ELD systems. Drivers manage duty status, review violation summaries, and communicate with dispatch through smartphone interfaces that sync with onboard logging hardware. This shift reduces driver resistance to compliance monitoring and extends the operational reach of ELD platforms beyond the cab.

Subscription-based SaaS fleet management models allow vendors to deliver continuous software updates, regulatory compliance patches, and new analytics features without hardware replacement cycles. This model improves vendor revenue predictability and reduces customer churn. Fleet operators benefit from platforms that self-update to reflect regulatory changes, eliminating manual recertification workflows.

Regional Analysis

North America Dominates the Automotive Logging Devices Market with a Market Share of 36.80%, Valued at USD 5.7 Billion

North America commands the largest share of the Automotive Logging Devices Market at 36.80%, valued at USD 5.7 Billion. The FMCSA federal ELD mandate, covering all interstate commercial motor vehicles, creates one of the world’s largest legally-defined demand pools. The 2 ELD devices revoked by FMCSA in July 2025 for federal non-compliance further demonstrate the enforcement intensity that sustains vendor activity in this region.

Europe Automotive Logging Devices Market Trends

Europe enforces tachograph regulations for commercial vehicle operators under EU Regulation No. 165/2014, with smart tachograph requirements expanding to additional vehicle categories. National transport authorities in Germany, France, and the UK operate enforcement programs that function similarly to North American ELD compliance structures. This regulatory alignment supports steady device replacement and upgrade demand across European fleets.

Asia Pacific Automotive Logging Devices Market Trends

Asia Pacific represents the highest-volume growth opportunity for automotive logging device vendors. China, India, and Southeast Asian economies are expanding commercial fleet populations while simultaneously introducing digital fleet compliance requirements. Government logistics modernization programs across the region mandate GPS tracking and driver records for freight operators, creating first-generation ELD demand at scale.

Latin America Automotive Logging Devices Market Trends

Latin America’s logistics sector is advancing fleet digitization through government-backed freight monitoring programs in Brazil and Mexico. Brazil’s ANTT transport regulator has expanded tachograph and electronic monitoring requirements for heavy freight operators. These frameworks create structured demand that mirrors North America’s compliance-driven procurement pattern, though at lower absolute device volumes.

Middle East & Africa Automotive Logging Devices Market Trends

Middle East fleet operators in GCC countries are adopting telematics and logging systems through Vision 2030-aligned logistics modernization initiatives in Saudi Arabia and UAE. Large-scale infrastructure and logistics projects demand compliant fleet monitoring. Africa presents an earlier-stage opportunity where commercial fleet growth outpaces regulatory enforcement, with South Africa leading adoption among sub-Saharan markets.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

AT&T Business positions its fleet telematics offering within its broader enterprise connectivity infrastructure. The company’s advantage lies in network scale — leveraging its nationwide carrier infrastructure to guarantee ELD data uptime across remote freight corridors where independent telematics vendors face coverage gaps. This integration of connectivity and compliance creates a bundled value proposition that is structurally difficult for software-only vendors to replicate.

Geotab Inc. operates one of the largest commercial telematics platforms globally, with its GO Device ecosystem serving as the hardware core for ELD compliance, driver safety analytics, and fleet intelligence. In October 2025, Geotab acquired the European and Australian commercial telematics operations of Verizon Connect, extending its global footprint into two key growth regions. According to FMCSA, 4 ELD devices were removed from the approved list in December 2025, reinforcing the market’s ongoing need for technically certified platforms like Geotab’s.

Motive Technologies, Inc. has built a vertically integrated fleet management platform that combines ELD compliance, AI-powered dashcams, and driver safety scoring within a single subscription model. In December 2025, Motive filed an S-1 for a planned 2026 IPO under the expected ticker “MTVE.” This move signals investor confidence in the SaaS fleet management model and positions Motive as a potential consolidator within a market where compliance mandates guarantee base-level recurring revenue.

Geotab Inc. and Garmin Ltd. represent contrasting approaches to fleet compliance hardware. Garmin’s ELD solutions leverage its established navigation hardware distribution network and brand recognition among owner-operators and small fleets. This positions Garmin in the entry-to-intermediate service tier where purchase decisions rely on brand trust and retail availability rather than enterprise sales cycles.

Key Players

- AT&T Business

- Coretex USA Inc

- ELD Solutions, Inc

- Garmin Ltd

- Geotab Inc.

- Motive Technologies, Inc.

- Orbcomm

- Teletrac Navman US Ltd

- Zonar Systems, Inc.

Recent Developments

- June 2025 – Samsara launched new AI-powered fleet safety, routing, navigation, and maintenance tools at its Beyond 2025 event, including AI Multicam, Commercial Navigation, and Route Planning capabilities for ELD-integrated fleet operations.

- October 2025 – Geotab acquired the European and Australian commercial telematics operations of Verizon Connect, expanding its global connected vehicle and ELD business footprint across 2 key international markets.

- December 2025 – Motive filed an S-1 for a planned 2026 IPO under the expected ticker “MTVE,” highlighting continued expansion in the ELD and fleet telematics sector.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 15.5 Billion |

| Forecast Revenue (2035) | USD 23.2 Billion |

| CAGR (2026-2035) | 4.2% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Component (Telematics Unit, Display, Others), By Service Type (Intermediate, Entry Level, High Level), By Form Factor (Embedded, Integrated), By Vehicle Type (Trucks, Light Commercial Vehicles, Bus, Cars) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | AT&T Business, Coretex USA Inc, ELD Solutions Inc, Garmin Ltd, Geotab Inc., Motive Technologies Inc., Orbcomm, Teletrac Navman US Ltd, Zonar Systems Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |