Global Automotive Glass Market By Glass Type (Tempered and Laminated), By Application (Windshield, Backlite, and Others), By Technology, and Passive Glass, Vehicle Type, Distribution Channel, By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2023-2032

- Published date: Oct 2023

- Report ID: 62302

- Number of Pages: 229

- Format:

- keyboard_arrow_up

Quick Navigation

Report Overview

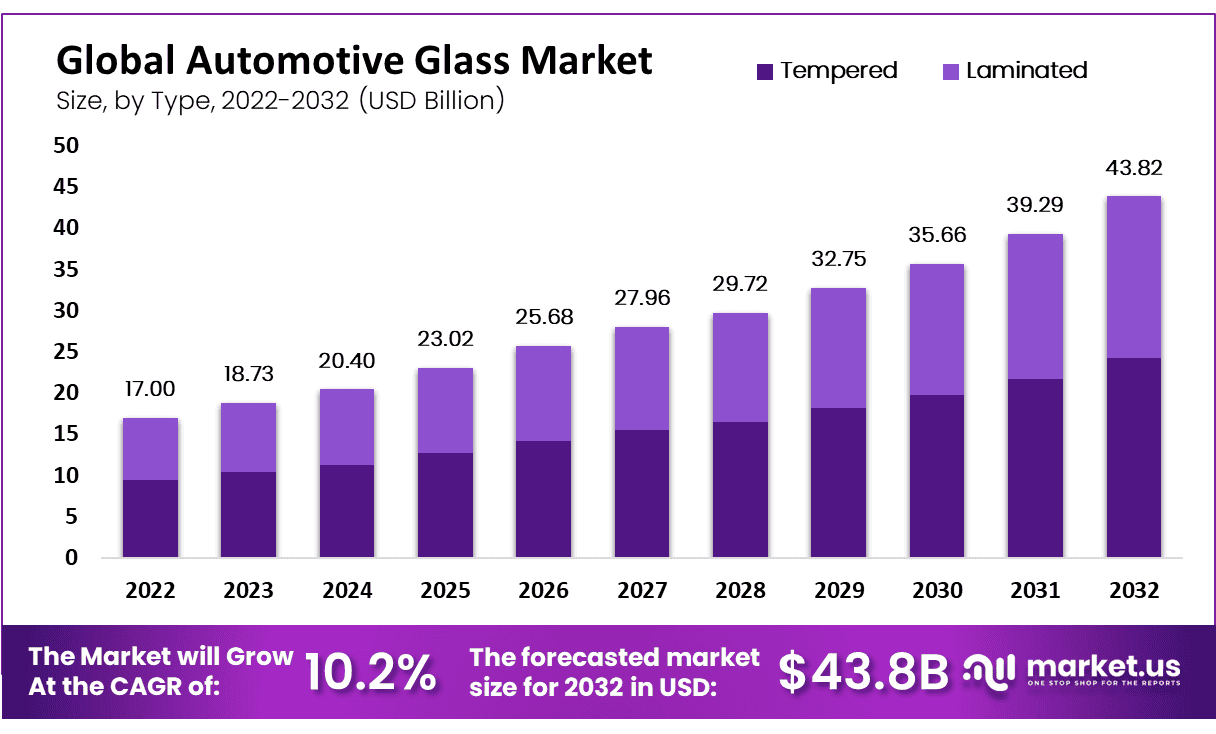

The Global Automotive Glass Market size is expected to be worth around USD 43.8 Billion by 2032, From USD 17 Billion by 2023, growing at a CAGR of 10.20% during the forecast period from 2023 to 2032.

Automotive glass is a type of laminated or tempered glass used in the manufacture of vehicle windscreens and windows. To withstand extreme heat and impact without shattering, laminated glass is made from two sheets of glass with a layer of PB (polyvinyl butyral) between them.

Tempered glass, on the other hand, is a single-ply product that breaks into small pieces after being broken. This increases safety for passengers. Automotive glass is also water-resistant, has superior aerodynamic features, and protects against UV radiation, rain, fog, and sun.

Driving Factors

Market Expansion is Being Aided by Technological Advancement.

One of the primary drivers of this market is the rapid expansion of the automobile industry worldwide. The market’s expansion is significantly aided by consumers’ growing preference for luxury and premium automobiles with advanced utility and safety features like glass sunroofs.

The development of smart automotive glass and its integration with in-vehicle entertainment systems are two additional technological innovations that are boosting market expansion. The vehicle’s temperature, voltage, and light intensity can all be altered by the smart glass, enhancing overall driving efficiency, passenger comfort, and safety.

The glass is used for panoramic experiences, advertising, and entertainment as a digital interactive surface. The growing purchasing power of consumers, the rapid urbanization of emerging nations, and the widespread use of electric and hybrid vehicles all contribute to the growth of the market.

Restraining Factors

High Cost and Intensive Capital Investment to Restrain Market Growth

Laminate glass is more expensive than tempered glass, and the technology isn’t widely used in developing countries because of its higher cost.

Additionally, the production of thin laminated glass for side windows and research and development both necessitate high capital expenditures. The market’s expansion is anticipated to be slowed by this investment and an emphasis on lowering production costs and consumer costs.

Growth Opportunities

Use of Smart Glass

In the market for automotive glass, new technologies, and applications, such as smart glass and gorilla glass, are aimed at increasing efficiency and comfort. The auto-dimmable property of smart glass, like thermos chromic glass, is used to control how much light enters the vehicle. It reduces cabin heat buildup, thereby reducing air conditioning demand, which in turn reduces carbon emissions and boosts fuel economy.

Passengers can adjust the transparency of the glass to suit their needs with electrochromic glass. Sunroofs typically make use of suspended particle device glass, which switches between dark and light shades with electricity.

In order to reduce the weight of its off-road Wrangler, the company Jeep (US) decided in 2021 to use gorilla glass instead of traditional automotive glass. The replacement was successful in reducing the vehicle’s gross weight by 7 kg. Because of this advantage, Jeep has decided to provide Corning Incorporated with OE-fit gorilla glass for its newest Wrangler SUV.

To improve fuel economy and reduce emissions, automobile manufacturers are concentrating on making lighter vehicles. New regulations requiring automobile emissions reductions are being implemented by governments all over the world. Gorilla glass and smart glass present a fantastic chance for glass producers to not only cut down on emissions but also boost revenue.

Trending Factors

Increased Adoption of Sunroofs and Growing Focus on Safety to Drive Market Growth

Investments in the technological advancement of automotive glass have increased as a result of the focus on enhancing the use of sunroofs in mainstream automobiles and the utilization of features like head-up displays to enhance driver alertness.

Market trends are being driven by the establishment of standards for rollover roof crush and windshield retention. The market is experiencing significant expansion as a result of the support and complementarity provided by all of these elements.

Increasing Application of Glass in Automobiles and Environmental Benefits to Boost Market

Aerodynamic styling causes windshields and back windows to have a more pronounced installation angle, making them longer. Sunroofs and moonroofs are becoming increasingly popular as a result of the increased value placed on the appearance of glass on automobiles due to the increased surface area.

By reducing the use of air conditioning, reflective coatings save gas and reduce air pollution. As a result, the anticipated positive effects on the market of environmental benefits from advancements in this kind of glass are positive.

Glass Type Analysis

Tempered Glass Segment Dominated Market in 2022 Due to Low Cost

Based on type, this market is segmented into laminated glass and tempered glass.

Over the forecast period, the market is expected to be dominated by laminated glass. Mercedes and BMW, two European OEMs, include standard side windows in their most popular models. This market is expected to expand since laminated side glazing improves occupant safety in the event of a vehicle rollover.

It is anticipated that the market for tempered glass will experience steady expansion. This market is expected to expand due to the high demand for sideline and backlite as well as the simpler manufacturing process and low cost.

Application Analysis

Windshields dominating this market

By application, the market is segmented into windshield, side & rearview mirror, backlite, and sunroof.

Windshields dominated the market in 2022 in terms of revenue, and it is projected that this trend will continue during the forecast period. The windscreen plays a key role in a vehicle’s structure, thus both glass and automotive makers are working to improve the windscreen’s characteristics and aesthetics. For instance, it is predicted that the category growth over the forecast period will be driven by the introduction of new types of windshields with self-cleaning glass.

Over the forecast period, it is anticipated that the sunroof segment will dominate the market. The sunroof gives you more control over how much natural light comes into the car. This market is likely to expand as a result of rising investment by new market entrants and rising demand for energy-efficient products.

Technology advancements like embedded sensors and smart materials, augmented displays, self-cleaning glass, and so on are expected to significantly expand the windshield market.

Due to the rising number of road accidents, which will accelerate the demand for side glass of higher quality, it is anticipated that the sidelite segment of the market will experience strong growth. In this market, the backlite segment is also anticipated to experience steady expansion.

Technology Analysis

In 2022, the electrochromic glass sector held a sizable share of more than 83%. This is large because of the product’s advantages, such as its low driving voltage, high UV and IV ray blockage ratio, and ease of integration with large glass panels. In addition, electrochromic glass can be colored, tinted, or made opaque to change how heat and light are transmitted depending on the situation.

Due to the high UV-ray resistance of SPD smart glasses, the Suspended Pixel Device (SPD), a segment of smart glass is expected to see the highest CAGR at around 15.0% through 2032. These glasses can change from transparent to dark in 1-3 seconds. They also provide precise and immediate light control. These glasses also feature exceptional optical quality, which allows for effective control of the sun’s glare.

The vast majority of electronic devices use polymer-dispersed liquid crystal (PDLC) glass. Also known as magic glass, switchable glass, or privacy glass. This technology is used primarily in offices and homes to provide privacy and ample light. It is applicable in many dynamic sectors such as aviation, marine, and architecture. Further driving demand for PDLC smart glasses technology is the growing interest in ‘Green Energy’ resources.

Vehicle Type

Passenger Car Segment to Hold Largest Automotive Glass Market Share Owing to High Demand in Developing Countries

This market is divided into passenger cars, light commercial vehicles, and heavy commercial vehicles in terms of the type of vehicle. Over the forecast period, the market is expected to be dominated by the passenger car segment. This market is likely to expand due to rising passenger car sales in China and India.

Due to the high demand for intra-city trucks and buses and the rising popularity of crossover SUVs, it is anticipated that the LCV segment will experience steady growth in the market. Due to the need for long-haul transport vehicles that are both lightweight and focused on safety, the HCV segment is anticipated to experience significant market expansion.

Due to the early adoption of technologies like head-up displays and smart glass for the panoramic sunroof, electric vehicles are also anticipated to show significant growth in this market.

Distribution Channel Analysis

During the forecast period, it is anticipated that the OEM segment will expand at a higher CAGR (Compound Annual Growth Rate) owing to the most automotive glass being used for vehicle production.

Additionally, it is anticipated that the original equipment manufacturer (OEM) market will experience a rapid expansion as a result of the construction of new automobile assembly plants, particularly those devoted to the production of electric vehicles.

Moreover, companies that manufacture glass for new vehicles make up the OEMs segment, while companies that manufacture glass for replacement purposes make up the aftermarket suppliers segment. Aftermarket markets are driven by the need to maintain and upgrade older vehicles as well as an increase in road accidents.

Key Market Segments

Based on Glass Type

- Tempered

- Laminated

Based on Application

- Windshield

- Backlite

- Side & Rear View Mirror

- Sunroof

Based on Technology

- Active Smart Glass

- Suspended Particle Glass

- Electrochromic Glass

- Liquid Crystal Glass

- Passive Glass

- Thermochromic

- Photochromic

Based on Vehicle Type

- Passenger Car

- Light Commercial

- Heavy Commercial

Based on the Distribution Channel

- Original Equipment Manufacturer (OEM)

- Aftermarket Replacement (ARG)

COVID-19 Impact Analysis

Due to the strict lockdowns and social isolation implemented to stop the virus from spreading, the COVID-19 outbreak had a negative impact on the automotive glass market. Demand for automotive glass was impacted by the business’s partial shutdown, economic uncertainty, and low consumer confidence.

During the pandemic, the supply chain was hampered as logistics activities were delayed. The easing of restrictions, on the other hand, is expected to accelerate the automotive glass market following the pandemic.

Regional Analysis

Asia Pacific is dominating this automotive glass market. China and India are the key drivers of this market’s growth. Increasing vehicle production has been a result of improving economic conditions and high population growth. This has resulted in increased demand and consumer preference for SUVs. The market growth is likely to be driven by the higher glass volume in India and China.

Europe has the second-largest market share and is predicted to experience significant growth during the forecast period. The market’s expansion in this region is being fueled by strict safety regulations for automobiles, the presence of leading innovators like Saint-Gobain Sekurit, and an increasing number of electric vehicles.

The market is expected to grow steadily in North America during the forecast period. Market growth is expected to be positive due to the early adoption of advanced glazing techniques by many companies such as Magna International and Guardian Glass.

Key Regions and Countries Covered in this Report:

- North America

- The US

- Canada

- Mexico

- Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

- Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

- Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

New strategies for expanding their market share are being developed and implemented by the leading manufacturers. Integration across various stages of the value chain is also one of the strategies that key players employ to assist them in gaining a competitive advantage over other manufacturers. This is in addition to capacity expansion, mergers, acquisitions, and the development of new products. Other strategies include these.

The automotive glass market is heavily dependent on manufacturers of raw materials, distributors, manufacturers, manufacturers, and end-users. Despite the existence of many players in the market, the market is stable due to the presence of a few major manufacturers like AGC Ltd. Saint-Gobain Fuyao Glass Industry Group Co. Ltd., and NSG Group.

Market Key Players:

Listed below are some of the most prominent automotive glass industry players.

- Dura Automotive Systems

- Saint-Gobain S.A.

- Fuyao Glass Industry Group Co. Ltd.

- Guardian Industries Corporation

- AGC Ltd.

- Nippon Sheet Glass Co. Ltd.

- Central Glass Co. Ltd.

- Xinyi Glass Holdings Ltd.

- Corning Incorporated

- Taiwan Glass Ind Corp

- Other Key Players

Recent Developments:

- In July 2022, Compagnie de Saint-Gobain S.A. expanded its building products with technology transfer from Kaycan Ltd. (Canada) through Kaycan Ltd’s acquisition. The acquisition is also expected to improve Compagnie de Saint-Gobain S.A.’s market presence in North America.

- January 2022, AGC Inc. improved its Infoverre Paper-like Screen Series, ultra-thin glass signage that applies AGC’s glass processing technology to OLEDs. The signage finds its application in buses, trains, and commercial vehicles.

Report Scope

Report Features Description Market Value (2022) US$ 17 Bn Forecast Revenue (2032) US$ 43.8 Bn CAGR (2023-2032) 10.2% Base Year for Estimation 2022 Historic Period 2016-2022 Forecast Period 2023-2032 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered Based on Glass Type · Tempered

· Laminated

Based on Application

· Windshield

· Backlite

· Side and rear View Mirror

· Sunroof

Based on Technology

· Active Smart Glass

· Suspended Particle Glass

· Electrochromic Glass

· Liquid Crystal Glass

· Passive Glass

· Thermochromic

· Photochromic

Based on Vehicle Type

· Passenger Car

· Light Commercial

· Heavy Commercial

Regional Analysis North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; the Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA Competitive Landscape Dura Automotive Systems, Saint-Gobain S.A., Fuyao Glass Industry Group Co. Ltd., Guardian Industries Corporation, AGC Ltd., Nippon Sheet Glass Co. Ltd., Central Glass Co. Ltd., Xinyi Glass Holdings Ltd., Corning Incorporated, Taiwan Glass Ind Corp., and Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) Frequently Asked Questions (FAQ)

What is the size of the Automotive Glass Market in 2022?The Automotive Glass Market size was estimated to be USD 17 billion in 2022.

What is the projected CAGR at which the Automotive Glass Market is expected to grow at?The Automotive Glass Market is expected to grow at a CAGR of 10.2% (2023-2032).

List the key industry players of the Automotive Glass Market?Dura Automotive Systems, Saint-Gobain S.A., Fuyao Glass Industry Group Co. Ltd., Guardian Industries Corporation, AGC Ltd., Nippon Sheet Glass Co. Ltd., Central Glass Co. Ltd., Xinyi Glass Holdings Ltd., Corning Incorporated, Taiwan Glass Ind Corp, Other Key Players Other Key Players engaged in the Automotive Glass Market.

Which region is more appealing for vendors employed in the Automotive Glass Market?Asia Pacific is dominating this market. China and India are the key drivers of this market's growth.

- Dura Automotive Systems

- Saint-Gobain S.A.

- Fuyao Glass Industry Group Co. Ltd.

- Guardian Industries Corporation

- AGC Ltd.

- Nippon Sheet Glass Co. Ltd.

- Central Glass Co. Ltd.

- Xinyi Glass Holdings Ltd.

- Corning Incorporated

- Taiwan Glass Ind Corp

- Other Key Players

- settingsSettings

Our Clients

- 62302

- Oct 2023

| Single User $4,599 $3,499 USD / per unit save 24% | Multi User $5,999 $4,299 USD / per unit save 28% | Corporate User $7,299 $4,999 USD / per unit save 32% | |

|---|---|---|---|

| e-Access | |||

| Report Library Access | |||

| Data Set (Excel) | |||

| Company Profile Library Access | |||

| Interactive Dashboard | |||

| Free Custumization | No | up to 10 hrs work | up to 30 hrs work |

| Accessibility | 1 User | 2-5 User | Unlimited |

| Analyst Support | up to 20 hrs | up to 40 hrs | up to 50 hrs |

| Benefit | Up to 20% off on next purchase | Up to 25% off on next purchase | Up to 30% off on next purchase |

| Buy Now ($ 3,499) | Buy Now ($ 4,299) | Buy Now ($ 4,999) |