Global Automotive Advanced Seating System Market Size, Share, Growth Analysis By Technology (Power Seat Adjustments, Electric Seat with Memory Function), By Vehicle Type (Passenger Cars, Commercial Vehicles), By Sales Channel (OEMs, Aftermarket), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2025-2034

- Published date: Dec 2025

- Report ID: 172601

- Number of Pages: 329

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

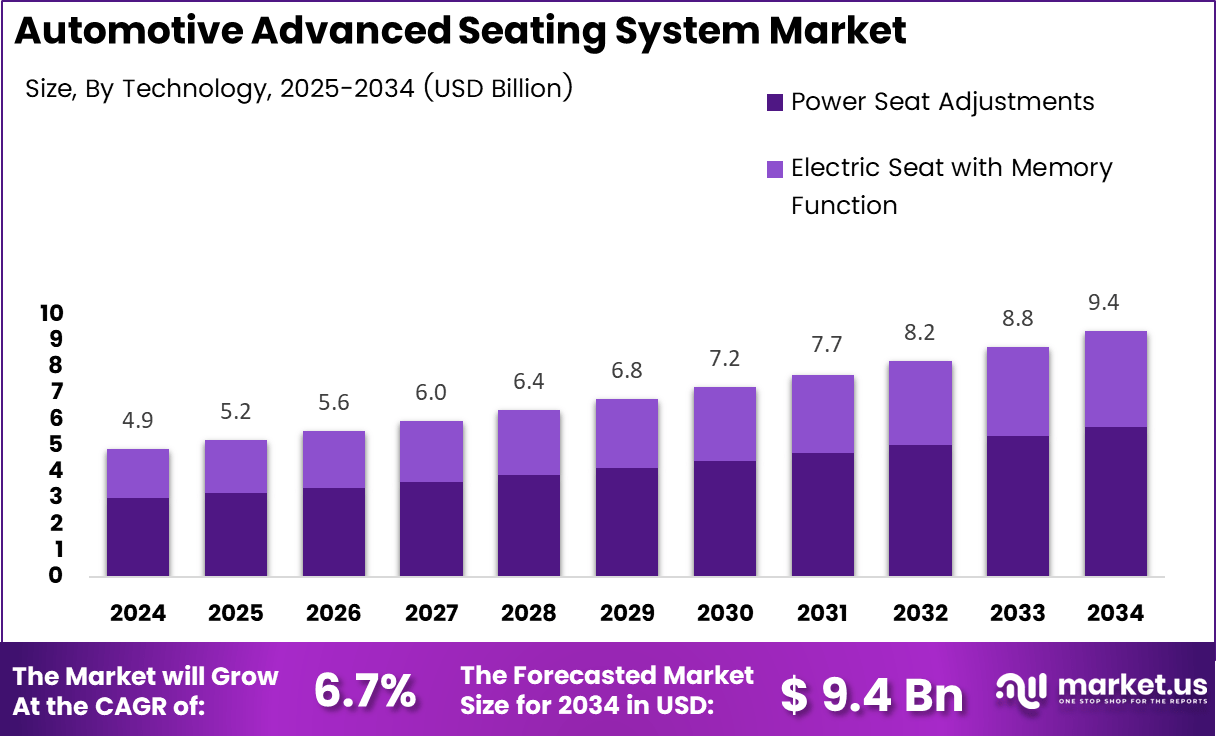

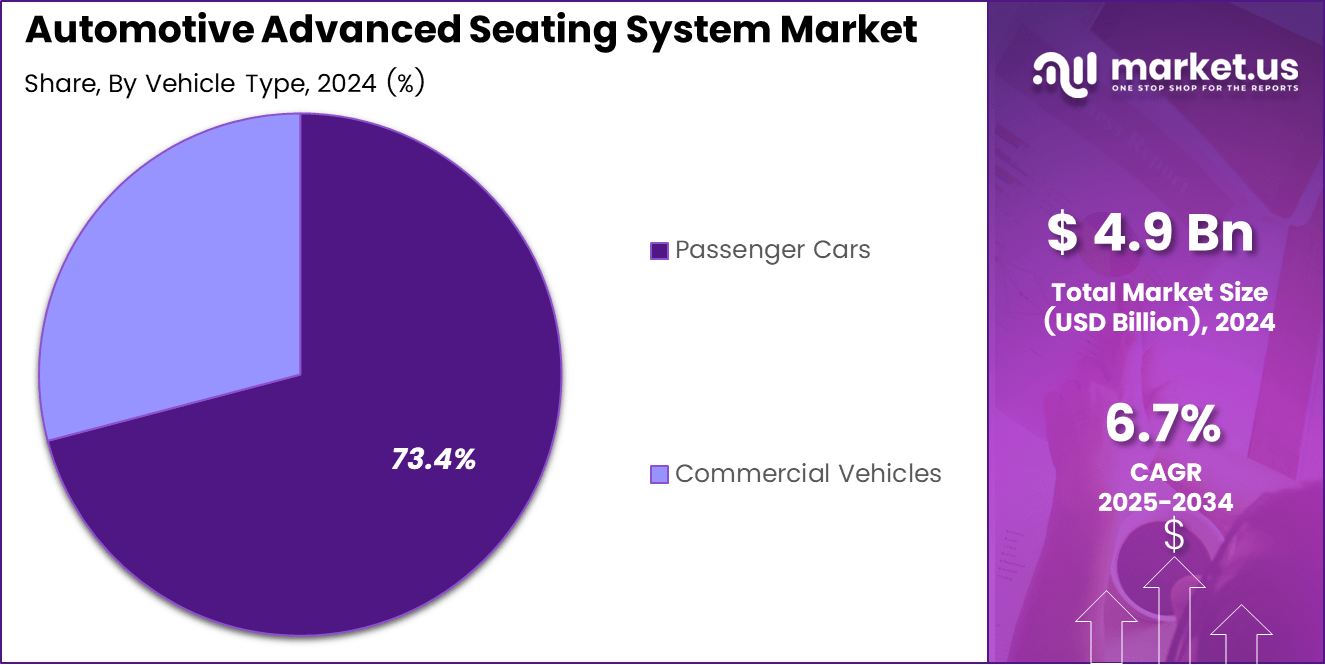

The Global Automotive Advanced Seating System Market size is expected to be worth around USD 9.4 billion by 2034, from USD 4.9 billion in 2024, growing at a CAGR of 6.7% during the forecast period from 2025 to 2034.

The Automotive Advanced Seating System represents the evolving ecosystem of intelligent, ergonomic, and safety focused seating technologies integrated into modern vehicles. This market reflects how vehicle interiors are transforming into comfort centric, technology enabled environments. As mobility expectations rise, seating systems increasingly influence purchase decisions and perceived vehicle value.

Automotive Advanced Seating System focuses on powered adjustment, thermal comfort, posture optimization, and adaptive safety integration. Consequently, OEMs prioritize seating as a strategic interior differentiator rather than a commodity component. Moreover, electrification and software defined vehicles are accelerating the transition toward smarter seating architectures supporting connected, user responsive driving experiences.

Automotive Advanced Seating System Market growth is supported by rising vehicle production, premium feature democratization, and interior personalization trends. Additionally, regulatory emphasis on occupant safety and ergonomics strengthens adoption. Governments globally continue supporting automotive manufacturing through localization incentives, skill development programs, and safety compliance frameworks, indirectly benefiting advanced seating integration.

Furthermore, opportunities emerge from electric vehicles, autonomous readiness, and shared mobility platforms requiring flexible seating layouts. As a result, rotating, reclining, and modular seat concepts gain traction. Advanced seating also aligns with sustainability policies encouraging lightweight materials, recyclable foams, and energy efficient seat actuation systems, improving regulatory acceptance across regions.

Operational efficiency also defines market scalability. According to studies, over 115 trucks deliver more than 4,000 car seats per hour across global assembly plants, highlighting industrial scale readiness. Meanwhile, according to vehicle interior survey, more than 80% of automotive seats worldwide remain manually operated, signaling substantial upgrade potential.

In parallel, innovation intensity remains exceptionally high. According to study, over 720,000 automotive patents were filed and granted during the last three years, reflecting rapid technological progress. Within this innovation wave, advanced seating patents increasingly focus on comfort automation, safety intelligence, and user behavior adaptation.

Looking ahead, the Automotive Advanced Seating System Market is expected to expand as interior comfort converges with digital vehicle platforms. Notably, emerging concepts such as seats rotating around 180 degrees to support non driving activities illustrate future cabin use cases. Therefore, advanced seating systems are positioned as both functional necessities and revenue enhancing automotive features.

Key Takeaways

- The Automotive Advanced Seating System Market is projected to reach USD 9.4 billion by 2034, expanding from USD 4.9 billion in 2024 at a 6.7% CAGR.

- Electric Seat with Memory Function leads the By Technology segment with a dominant share of 61.2%, reflecting strong demand for personalized comfort features.

- Passenger Cars dominate the By Vehicle Type segment, accounting for 73.4% of total market demand due to high production volumes.

- OEMs remain the primary sales channel with a market share of 67.9%, supported by factory level integration of advanced seating systems.

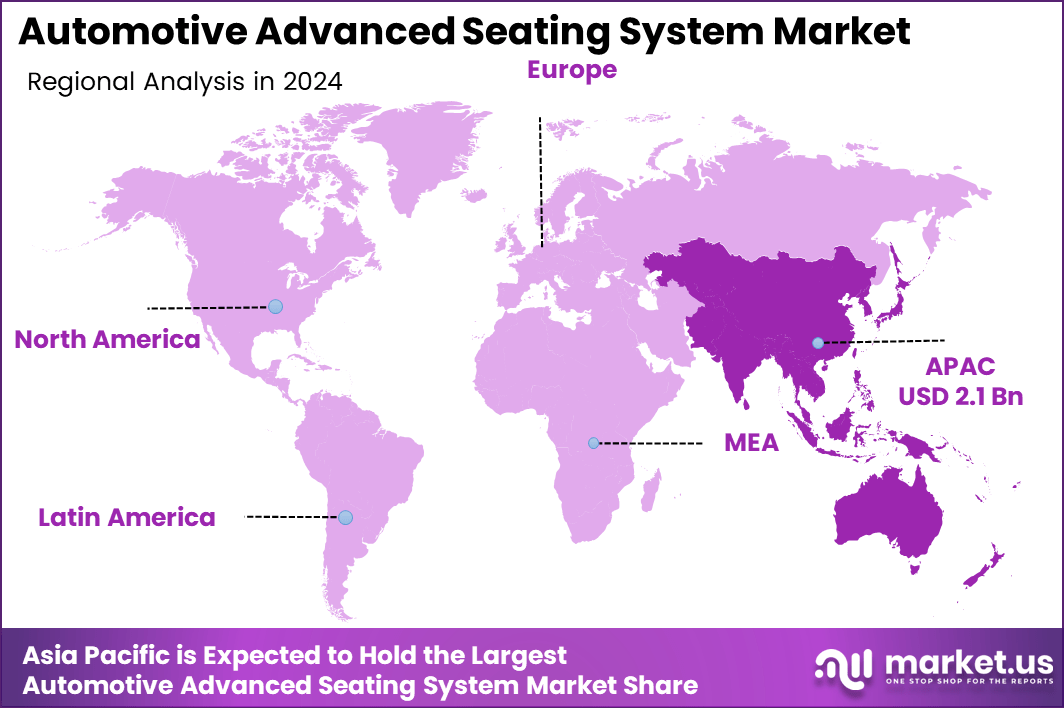

- Asia Pacific leads regional demand with a market share of 43.9%, valued at USD 2.1 billion, driven by high vehicle production and rising comfort adoption.

By Technology Analysis

Electric Seat with Memory Function dominates with 61.2% due to rising demand for personalized comfort and convenience.

Power Seat Adjustments held a significant market position in the By Technology Analysis segment of Automotive Advanced Seating System Market, driven by growing expectations for ease of use. These systems enable smoother seat positioning, improving driving ergonomics. As vehicle interiors evolve, powered adjustments remain a foundational comfort feature across segments.

Electric Seat with Memory Function held a dominant market position in the By Technology Analysis segment of Automotive Advanced Seating System Market, with a 61.2% share. This dominance reflects increasing preference for user specific seating profiles. Memory based systems enhance comfort, reduce driver fatigue, and align with connected vehicle personalization trends.

By Vehicle Type Analysis

Passenger Cars dominates with 73.4% due to higher production volumes and rapid adoption of comfort technologies.

Passenger Cars held a dominant market position in the By Vehicle Type Analysis segment of Automotive Advanced Seating System Market, with a 73.4% share. This leadership is supported by consumer demand for advanced comfort features. Automakers increasingly integrate advanced seating to improve driving experience and brand differentiation.

Commercial Vehicles held a smaller yet stable position in the By Vehicle Type Analysis segment of Automotive Advanced Seating System Market. Adoption is influenced by fleet cost considerations and durability requirements. However, demand for driver comfort and long haul ergonomics is gradually supporting advanced seating integration in this segment.

By Sales Channel Analysis

OEMs dominates with 67.9% due to factory level integration and standardization of advanced seating systems.

OEMs held a dominant market position in the By Sales Channel Analysis segment of Automotive Advanced Seating System Market, with a 67.9% share. OEM integration ensures system compatibility, quality control, and regulatory compliance. Advanced seating is increasingly offered as standard or bundled features at the manufacturing stage.

Aftermarket held a supporting position in the By Sales Channel Analysis segment of Automotive Advanced Seating System Market. This channel serves replacement and upgrade demand, particularly in older vehicles. Growth remains steady as consumers seek comfort enhancements, though adoption is limited compared to factory installed solutions.

Key Market Segments

By Technology

- Power Seat Adjustments

- Electric Seat with Memory Function

By Vehicle Type

- Passenger Cars

- Commercial Vehicles

By Sales Channel

- OEMs

- Aftermarket

Drivers

Rising Consumer Preference for Enhanced In Cabin Comfort Drives Market Growth

The Automotive Advanced Seating System Market is strongly driven by rising consumer preference for improved in cabin comfort, ergonomics, and flexible seating adjustment. Buyers increasingly expect seats to support posture, reduce fatigue, and enhance overall driving experience. As a result, seating is no longer viewed as a basic component but as a comfort focused value feature.

Moreover, the integration of powered, ventilated, and memory seating features is expanding beyond luxury models into mid range vehicles. This shift reflects changing customer expectations, where convenience and personalization are becoming standard. Consequently, manufacturers are scaling advanced seating technologies to meet broader market demand.

Another key driver is the growing focus on driver and passenger safety through advanced seat structures and active headrest systems. These features help reduce injury risk during collisions while improving occupant protection. Therefore, safety oriented seating designs increasingly align with regulatory and consumer safety priorities.

Additionally, OEMs emphasize vehicle interior differentiation to strengthen brand positioning and customer loyalty. Advanced seating designs allow automakers to create distinct cabin experiences. As competition intensifies, seating innovation plays a strategic role in enhancing brand identity and perceived vehicle quality.

Restraints

High System and Component Costs Limit Wider Adoption

Despite strong demand, the Automotive Advanced Seating System Market faces restraints related to high system and component costs. Multi motorized and sensor integrated seating designs increase manufacturing expenses. Consequently, cost sensitivity limits adoption in entry level and price focused vehicle segments.

In addition, increased vehicle weight from advanced seating components impacts fuel efficiency and electric vehicle driving range. Automakers must balance comfort features with efficiency targets. This challenge is particularly critical for electric vehicles where weight directly affects performance and range expectations.

Complexity in integration with vehicle electronics and software architectures also acts as a restraint. Advanced seating systems require seamless communication with control units and vehicle networks. As vehicle software becomes more complex, integration challenges can slow deployment timelines.

Furthermore, supply chain volatility affects the availability of seat motors, sensors, and electronic control units. Disruptions increase lead times and cost pressures. As a result, manufacturers face uncertainty in production planning and system scalability.

Growth Factors

Expanding Adoption in Electric Vehicles Creates New Opportunities

Growth opportunities in the Automotive Advanced Seating System Market are closely tied to expanding adoption of premium seating features in electric and hybrid vehicles. These platforms emphasize comfort and quiet cabins, making advanced seating a natural fit. Consequently, electric mobility supports higher value seating integration.

Rising demand for customized and modular seating solutions in shared mobility and autonomous vehicles also creates opportunity. Flexible seating layouts enhance passenger experience and cabin utilization. As mobility models evolve, adaptable seating becomes increasingly important.

Technological advancements in lightweight materials and smart textiles further open growth avenues. These innovations help reduce seat weight while improving comfort and durability. As a result, manufacturers can address efficiency concerns without sacrificing functionality.

Additionally, growing penetration of advanced seating systems in emerging automotive markets supports long term expansion. Improving income levels and vehicle feature expectations encourage adoption. Therefore, emerging regions represent strong future demand potential.

Emerging Trends

AI Enabled Adaptive Seating Shapes Market Trends

One of the most significant trends in the Automotive Advanced Seating System Market is the rapid development of AI enabled posture detection and adaptive seating technologies. These systems adjust seating positions in real time, enhancing comfort and reducing fatigue during long drives.

Another key trend is the increasing use of sustainable, recyclable, and bio based materials in seat manufacturing. Automakers aim to meet environmental targets while maintaining comfort standards. As sustainability gains importance, eco friendly seating materials gain traction.

Integration of health monitoring features such as pressure mapping and fatigue detection is also emerging. These technologies support driver wellbeing and safety. Consequently, seating systems are evolving into active contributors to vehicle health and safety ecosystems.

Together, these trends indicate a shift toward intelligent, sustainable, and user responsive seating solutions. As innovation continues, advanced seating systems will play a larger role in shaping future vehicle interiors.

Regional Analysis

Asia Pacific Dominates the Automotive Advanced Seating System Market with a Market Share of 43.9%, Valued at USD 2.1 Billion

Asia Pacific represents the leading region in the Automotive Advanced Seating System Market, accounting for a 43.9% share and a market value of USD 2.1 billion. This dominance is supported by high vehicle production volumes, rapid urbanization, and rising demand for comfort oriented interior features. Increasing adoption of electric vehicles and mid range passenger cars further accelerates advanced seating integration across the region.

North America Automotive Advanced Seating System Market Trends

North America demonstrates steady demand for automotive advanced seating systems, driven by strong consumer focus on comfort, safety, and interior personalization. Regulatory emphasis on occupant safety and ergonomics supports the integration of advanced seat structures. Additionally, rising penetration of electric and premium vehicles continues to strengthen regional market adoption.

Europe Automotive Advanced Seating System Market Trends

Europe shows consistent growth in advanced seating systems due to strict safety regulations and sustainability focused vehicle design. Automakers in the region emphasize lightweight materials and ergonomic seating solutions. The increasing shift toward electric mobility and premium interior standards further contributes to market expansion across European countries.

Middle East and Africa Automotive Advanced Seating System Market Trends

The Middle East and Africa region reflects gradual adoption of advanced seating systems, supported by growing passenger vehicle demand and improving automotive infrastructure. Consumer interest in comfort features is rising, particularly in urban centers. However, cost sensitivity and limited penetration of premium vehicles moderate overall growth.

Latin America Automotive Advanced Seating System Market Trends

Latin America exhibits moderate growth in the Automotive Advanced Seating System Market, supported by expanding automotive production and improving consumer purchasing power. Demand is primarily driven by passenger cars with basic comfort enhancements. Over time, increasing awareness of ergonomics and safety is expected to support broader adoption of advanced seating technologies.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Automotive Advanced Seating System Company Insights

Continental AG is positioned as a technology driven participant in automotive advanced seating through its strength in vehicle electronics integration and comfort related systems. Its role aligns with the market shift toward software aware seating functions, where sensors, control logic, and seamless cabin connectivity increasingly determine perceived seat value.

Faurecia continues to be associated with scalable seating architectures that support lightweighting and modular platform strategies. This positioning fits OEM demand for flexible seat frames, comfort enhancements, and cost disciplined industrialization, particularly as mid range vehicles adopt more powered and feature rich seat configurations.

NHK stands out for its relevance in mechanical and motion related seat components that enable reliability across high volume production programs. As advanced seating expands, consistent performance of seat actuation, adjustment mechanisms, and durability oriented sub systems remains critical for OEM quality targets and long lifecycle expectations.

Lear Corp maintains strong alignment with the market’s comfort and personalization trajectory, where heating, ventilation readiness, and trim innovations support premium cabin differentiation. Its positioning also matches the ongoing shift toward feature packaging, where seating becomes a central lever for OEMs to improve customer satisfaction and interior brand identity.

Top Key Players in the Market

- Continental AG

- Faurecia

- NHK

- Lear Corp

- Adient

- TS Tech

- Gentherm

- Brose

- Magna International

- Toyota Boshoku

Recent Developments

- In September 2025, Brose Sitech acquired Proseat Group to expand its vehicle seating portfolio by adding foam components for seats, headrests, and armrests, This acquisition strengthens Brose Sitech’s positioning as an integrated, full-range supplier of complete seat systems and interior solutions for the automotive industry.

- In February 2025, Lear acquired StoneShield Engineering to enhance advanced automation capabilities within its E-Systems business, The acquisition supports Lear’s focus on improving manufacturing efficiency, smart automation, and scalable production technologies across its global operations.

Report Scope

Report Features Description Market Value (2024) USD 4.9 billion Forecast Revenue (2034) USD 9.4 billion CAGR (2025-2034) 6.7% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Technology (Power Seat Adjustments, Electric Seat with Memory Function), By Vehicle Type (Passenger Cars, Commercial Vehicles), By Sales Channel (OEMs, Aftermarket) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Continental AG, Faurecia, NHK, Lear Corp, Adient, TS Tech, Gentherm, Brose, Magna International, Toyota Boshoku Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Automotive Advanced Seating System MarketPublished date: Dec 2025add_shopping_cartBuy Now get_appDownload Sample

Automotive Advanced Seating System MarketPublished date: Dec 2025add_shopping_cartBuy Now get_appDownload Sample -

-

- Continental AG

- Faurecia

- NHK

- Lear Corp

- Adient

- TS Tech

- Gentherm

- Brose

- Magna International

- Toyota Boshoku

Our Clients

- 172601

- Dec 2025