Global Automated Weapon System Market Size, Share, Growth Analysis By Type (Land Systems, Naval Systems, Aerial Systems, Cyber Systems), By Component (Sensors, Weapons, Command & Control Systems, Communication Systems), By Technology (Artificial Intelligence, Machine Learning, Robotics, Autonomous Navigation), By Deployment Mode (On-Premises, Cloud-Based Systems), By End User (Military, Defense Contractors, Government Agencies), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Apr 2026

- Report ID: 183771

- Number of Pages: 242

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

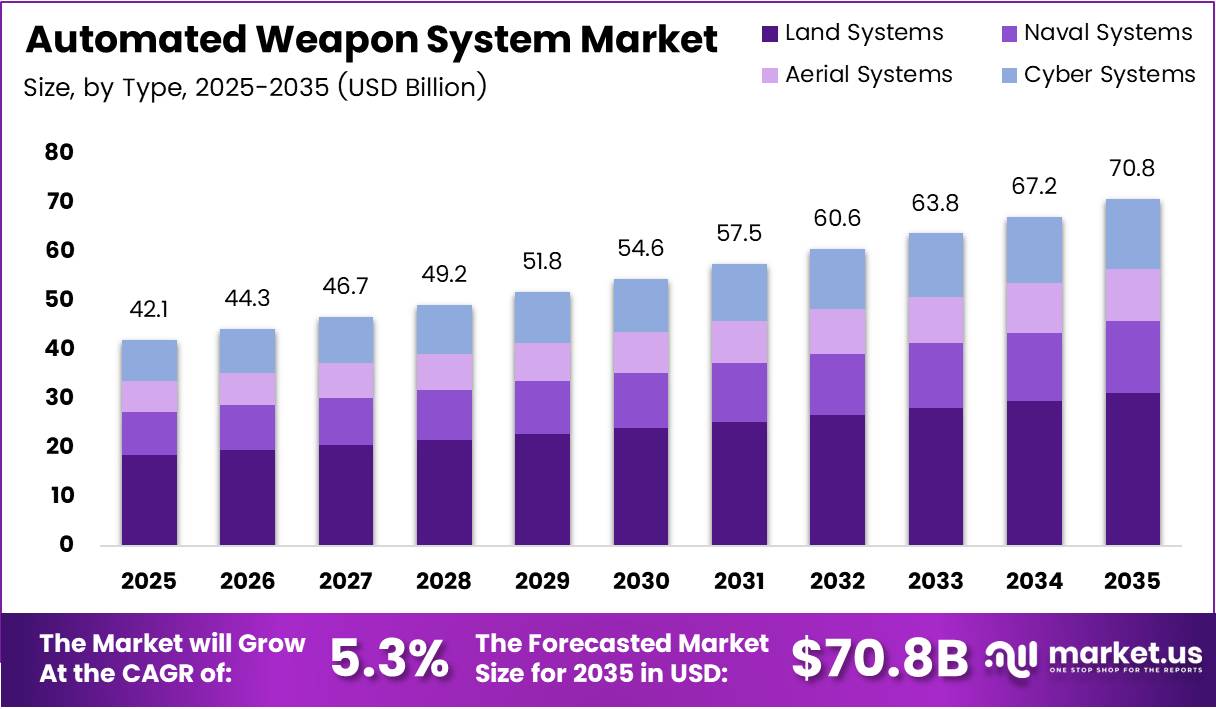

Global Automated Weapon System Market size is expected to be worth around USD 70.8 Billion by 2035 from USD 42.1 Billion in 2025, growing at a CAGR of 5.3% during the forecast period 2026 to 2035.

Automated weapon systems combine sensors, artificial intelligence, and autonomous navigation to execute precision strikes, border surveillance, and missile defense with reduced human intervention. Defense forces worldwide now treat autonomy not as a future capability but as a present procurement priority, reshaping acquisition cycles across land, naval, aerial, and cyber domains.

The 5.3% CAGR signals that defense budgets are shifting from platform-centric spending toward software-defined, AI-enabled combat systems — a transition that compresses the window for traditional hardware vendors and opens sustained opportunities for technology integrators. Buyers are no longer evaluating weapons alone; they are evaluating entire autonomous engagement architectures.

Military investment in smart battlefield programs continues to accelerate procurement timelines. Major defense forces are deploying unmanned combat platforms not as supplements to manned units but as primary assets in contested environments. This shift places systems integration, real-time data processing, and network-centric coordination at the center of every new platform specification.

Precision strike capability now drives procurement decisions at the national level. Conventional munitions cannot satisfy modern mission requirements for speed, accuracy, and minimal collateral risk. Automated systems close that gap by enabling rapid target acquisition and engagement with reduced crew exposure — a structural advantage that becomes more valuable as conflict scenarios grow more complex.

According to a study published in the World Journal of Advanced Research and Reviews, deep neural networks identify targets with accuracy rates exceeding 95% under optimal conditions, enabling simultaneous tracking of multiple objects across complex battlefield environments. This level of machine perception now exceeds what human operators can sustain under stress, making automation a force-multiplier rather than a convenience.

According to a study published by the Institute for Defence Studies and Analyses, AI-integrated missile defense achieves a prediction accuracy of 0.90 versus 0.70 for non-AI systems, and an interception success rate of 0.85 versus 0.60 for traditional systems. That performance delta directly justifies the higher procurement cost of AI-enabled platforms — and signals that defense procurement teams will continue prioritizing automation investment over legacy system upgrades.

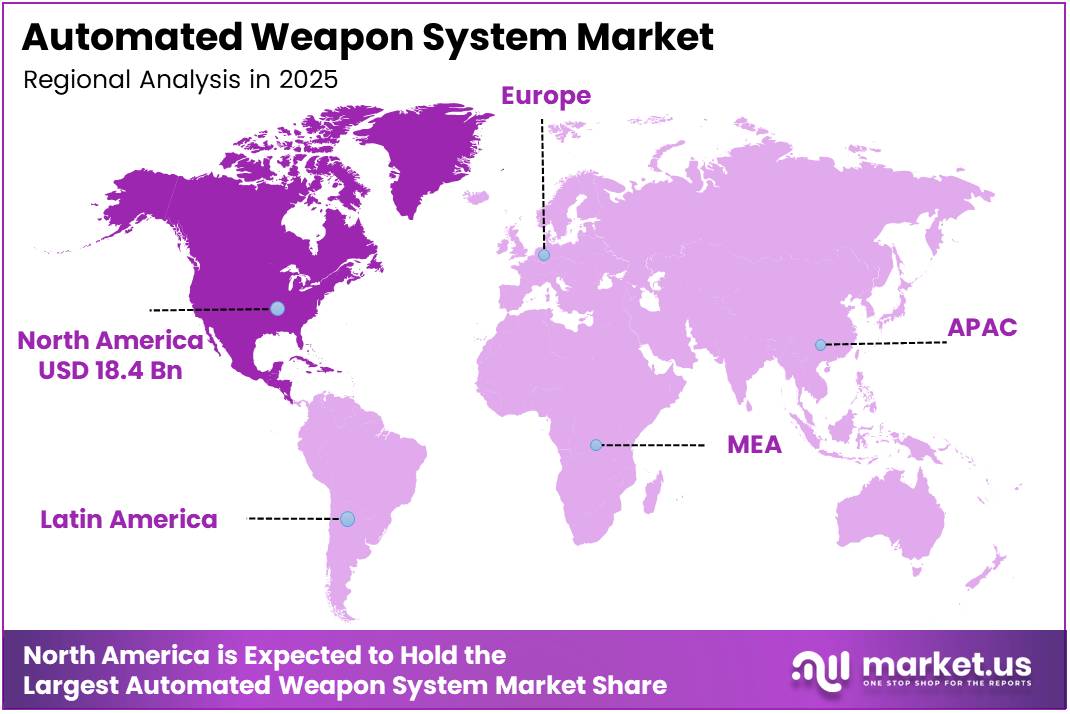

North America leads this market with a 43.80% share valued at USD 18.4 Billion, driven by established defense procurement infrastructure and active smart battlefield program expansion. However, defense modernization programs in emerging economies are creating new demand pools that will redistribute geographic concentration over the forecast period.

Key Takeaways

- The Global Automated Weapon System Market is valued at USD 42.1 Billion in 2025 and is forecast to reach USD 70.8 Billion by 2035.

- The market grows at a CAGR of 5.3% during the forecast period 2026 to 2035.

- By Type, Land Systems holds the dominant share at 42.7% of the market.

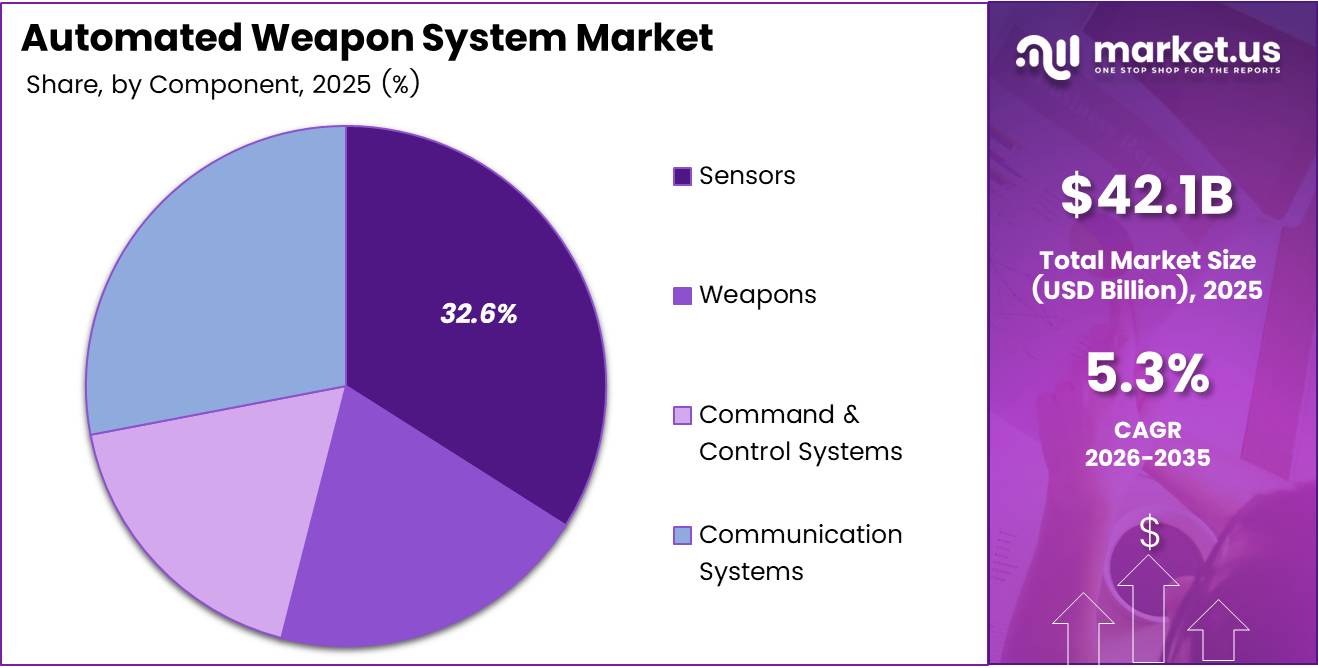

- By Component, Sensors leads with a 32.6% share, reflecting the centrality of perception technology in autonomous platforms.

- By Technology, Artificial Intelligence accounts for 38.9%, confirming AI as the primary enabler of weapon automation.

- By Deployment Mode, On-Premises systems dominate with 79.3% share, reflecting security and sovereignty requirements in defense environments.

- North America holds the largest regional share at 43.80%, valued at USD 18.4 Billion.

- Key end users include Military forces, Defense Contractors, and Government Agencies.

Type Analysis

Land Systems dominate with 42.7% due to large-scale ground force modernization programs.

In 2025, Land Systems held a dominant market position in the By Type segment of the Automated Weapon System Market, with a 42.7% share. Ground forces constitute the largest uniformed segment across all major defense establishments, and modernization budgets consistently prioritize land platforms. This concentration reflects where most active conflict and border security operations occur, making land automation the highest-volume procurement category.

Naval Systems serve as the primary deployment layer for long-range automated engagement in maritime theaters. Naval platforms require highly integrated weapon control architectures that coordinate radar, fire control, and interceptor systems with minimal latency. Consequently, naval automation investments tend toward higher unit value and longer procurement cycles, making the segment smaller by volume but strategically significant by contract size.

Aerial Systems differentiate through speed-of-engagement requirements that make human-in-the-loop control physically impractical at supersonic ranges. Unmanned aerial combat platforms and loitering munitions now constitute a distinct procurement subcategory with dedicated development pipelines. Moreover, aerial autonomous systems increasingly integrate directly into joint-force network architectures, amplifying their strategic value beyond individual mission profiles.

Cyber Systems carry the highest complexity-to-cost ratio within the automated weapon category. Offensive and defensive cyber capabilities require continuous algorithmic refinement, real-time threat intelligence integration, and strict sovereignty controls. Therefore, cyber automation budgets grow in proportion to adversary capability escalation, making this segment sensitive to geopolitical conditions rather than fixed procurement schedules.

Component Analysis

Sensors dominate with 32.6% due to their role as the core perception layer across all automated platforms.

In 2025, Sensors held a dominant market position in the By Component segment of the Automated Weapon System Market, with a 32.6% share. No autonomous weapon system functions without accurate environmental perception. Sensors form the upstream dependency for every downstream decision — target classification, engagement authorization, and trajectory control all depend on sensor data quality. This foundational position makes sensor procurement non-discretionary across every platform type.

Weapons represent the terminal-effect component of any automated system. Their procurement is directly linked to authorized engagement rules and platform integration specifications. However, the shift toward precision munitions reduces the volume required per mission, meaning weapons spending per engagement is declining even as total program values rise due to higher per-unit sophistication and guidance integration costs.

Command and Control Systems act as the decision architecture that translates sensor data into authorized weapon release. As multi-domain operations become standard, command and control platforms must process inputs from land, naval, aerial, and cyber sensors simultaneously. This integration complexity drives sustained investment in C2 software and hardware upgrades, particularly within NATO-aligned defense establishments expanding network-centric warfare capacity.

Communication Systems enable the real-time data exchange that makes networked autonomous combat architectures operationally viable. Secure, low-latency communication links between platforms, command nodes, and sensor arrays determine the overall responsiveness of an automated weapon system. Therefore, hardened communication infrastructure increasingly attracts dedicated line items in defense modernization budgets rather than being treated as a utility cost.

Technology Analysis

Artificial Intelligence dominates with 38.9% due to its role in enabling real-time target recognition and decision support.

In 2025, Artificial Intelligence held a dominant market position in the By Technology segment of the Automated Weapon System Market, with a 38.9% share. AI enables automated weapon systems to distinguish between targets, assess threat priority, and recommend engagement sequences without waiting for human cognitive processing. This capability addresses the primary operational bottleneck in modern high-tempo conflict: decision speed under information overload.

Machine Learning provides the adaptive layer that allows weapon systems to improve target classification accuracy over time and across operating environments. Unlike rule-based systems, machine learning models refine their performance as new engagement data accumulates. Consequently, procurement programs increasingly require ML integration as a baseline specification rather than an optional upgrade, particularly for counter-drone and electronic warfare applications.

Robotics translates autonomous decision logic into physical platform movement and weapons delivery. Ground-based robotic platforms, unmanned maritime vessels, and aerial drones all depend on robotic actuation systems to execute engagement commands with precision. Additionally, robotic platforms reduce personnel risk in contested terrain, which is a force-structure argument that sustains procurement even under budget pressure.

Autonomous Navigation enables platforms to operate across complex environments without continuous operator guidance. GPS-denied navigation, terrain-following algorithms, and obstacle-avoidance systems allow autonomous platforms to reach target areas even under electronic jamming. This resilience against adversary countermeasures makes autonomous navigation a critical technology differentiator in high-threat environments where remotely piloted systems face signal disruption.

Deployment Mode Analysis

On-Premises deployment dominates with 79.3% due to sovereignty requirements and classified data security mandates.

In 2025, On-Premises deployment held a dominant market position in the By Deployment Mode segment of the Automated Weapon System Market, with a 79.3% share. Defense organizations operate under strict data classification and sovereignty rules that prohibit external hosting of weapons system logic and targeting data. On-premises architecture is therefore a compliance requirement, not merely a preference, which structurally limits cloud migration regardless of cost or flexibility arguments.

Cloud-Based Systems occupy a narrow but expanding niche within non-classified support functions — logistics optimization, training simulation, and maintenance scheduling are among the functions defense agencies are cautiously migrating to cloud environments. However, any cloud deployment involving live weapons data faces multi-jurisdictional regulatory barriers. Therefore, cloud adoption in this market will grow selectively, confined to non-operational functions rather than core engagement architecture.

End User Analysis

Military dominates due to direct operational ownership of automated combat platforms.

In 2025, Military end users held a dominant market position in the By End User segment of the Automated Weapon System Market. National armed forces control weapons procurement policy, define capability requirements, and hold the primary budgets that fund platform development and deployment. This direct ownership of the entire acquisition chain — from specification through operational use — makes the military the structurally dominant end-user category across all geographies.

Defense Contractors function as both secondary end users and primary delivery partners. They procure automated weapon technologies, integrate them into platform systems, and deliver completed weapons architectures to military clients. Their buying behavior closely mirrors military procurement cycles, creating a multiplier effect on market demand during periods of accelerated defense spending or capability refresh programs.

Government Agencies outside traditional military structures — border security services, intelligence agencies, and national security organizations — represent a distinct demand pool for automated surveillance, cyber defense, and non-lethal autonomous systems. However, their procurement operates on different legal frameworks, requiring vendors to maintain separate product lines and compliance documentation for this segment.

Key Market Segments

By Type

- Land Systems

- Naval Systems

- Aerial Systems

- Cyber Systems

By Component

- Sensors

- Weapons

- Command & Control Systems

- Communication Systems

By Technology

- Artificial Intelligence

- Machine Learning

- Robotics

- Autonomous Navigation

By Deployment Mode

- On-Premises

- Cloud-Based Systems

By End User

- Military

- Defense Contractors

- Government Agencies

Drivers

National Defense Budgets Accelerate Spending on AI-Enabled Autonomous Combat Platforms

Major military establishments now treat autonomous combat capability as a strategic necessity rather than a modernization option. Defense forces are embedding AI-enabled systems into ground, aerial, and naval platforms to execute precision strikes, border surveillance, and missile interception faster than adversaries can respond. This shift is moving budget allocations away from conventional munitions and toward integrated autonomous architectures.

Unmanned combat platform deployment for border security and surveillance represents one of the fastest-converting procurement segments. Autonomous ground and aerial systems reduce personnel exposure in high-threat perimeter zones while maintaining continuous monitoring. In November 2024, Kongsberg Defence and Aerospace received a not-to-exceed $329 million contract to deliver 175 remotely operated RT20 turrets for the U.S. Marine Corps ACV-30, demonstrating active scaled deployment of unmanned weapon stations within existing force structures.

According to a study published in the World Journal of Advanced Research and Reviews, AI-secured surveillance systems achieved a 23% reduction in false positive rates compared to unprotected systems, while detecting 97% of attempted adversarial attacks during testing. For defense procurement teams, that accuracy differential directly reduces friendly-fire risk and operational liability — translating a technical performance metric into a concrete force-protection argument that sustains acquisition investment.

Restraints

Ethical Constraints and Prohibitive System Costs Create Structural Barriers to Full Autonomous Weapon Deployment

International legal frameworks governing autonomous lethal weapons remain unresolved, creating compliance uncertainty for defense ministries and their procurement agencies. Nations disagree on what constitutes a meaningful human role in the engagement decision. This ambiguity forces defense programs to design costly human-in-the-loop override systems into platforms that could technically operate more efficiently without them — adding development time and integration expense.

High development, integration, and maintenance costs compound the legal uncertainty. Automated weapon systems require simultaneous engineering of AI software, sensor hardware, communication networks, and weapons interfaces — all to classified specifications. Each integration layer introduces custom engineering costs that cannot be amortized across commercial markets. Consequently, only the largest defense contractors and the most generously funded national programs can absorb full development cycles, limiting competitive supply dynamics.

Maintenance costs present a secondary but sustained barrier. Unlike conventional weapons, AI-enabled platforms require ongoing algorithm updates, adversarial testing, and hardware refresh cycles to remain operationally effective against evolving threats. Defense agencies that underestimate lifecycle costs at the procurement stage frequently face mid-program funding shortfalls. Therefore, the total cost of ownership — not just acquisition price — functions as a practical ceiling on adoption rates, particularly for mid-tier defense budgets.

Growth Factors

AI and Autonomous Platform Integration Create New Revenue Channels Across Naval, Aerial, and Emerging Economy Defense Programs

The integration of artificial intelligence and machine learning into target recognition systems directly expands the functional scope of automated weapon platforms. Systems that previously required operator confirmation for each engagement decision can now classify, prioritize, and track multiple simultaneous threats with machine speed. According to research published on arXiv, AI-generated Course of Action plans produce tactical recommendations in seconds rather than hours or days — compressing the OODA loop in ways that give AI-enabled forces a measurable decision advantage.

Naval and aerial platform deployment programs represent the highest-value growth vectors within the autonomous defense segment. In October 2024, AeroVironment secured a $743 million additional contract ceiling from the U.S. Army for Switchblade loitering munition systems, confirming that expendable automated attack munitions now constitute a recognized and recurring procurement line. This contract structure signals that autonomous strike systems have moved from experimental programs into standard force readiness budgets.

Defense modernization programs in emerging economies add a geographic dimension to market expansion. Countries across Asia Pacific, the Middle East, and Latin America are establishing national defense technology programs that prioritize autonomous systems, network-centric warfare capability, and indigenous production. This demand pool operates on different procurement timelines than established NATO markets — creating parallel growth pathways that reduce the market’s dependence on any single defense budget cycle.

Emerging Trends

Human-in-the-Loop Control, Swarm Robotics, and Sensor Fusion Redefine Autonomous Combat Architecture

Defense programs globally are converging on human-in-the-loop autonomous control as the default architecture for next-generation weapon systems. This approach preserves legal accountability while capturing the speed advantages of machine decision support. Rather than full autonomy, the operational model positions human commanders as authorization authorities while AI handles threat classification and engagement sequencing — satisfying both operational performance requirements and evolving international conduct-of-war standards.

Military collaborations for next-generation smart weapon platforms are creating multi-nation technology development programs that accelerate capability timelines. Joint procurement and co-development agreements distribute R&D costs across allied defense budgets while ensuring interoperability across coalition force structures. Additionally, swarm robotics applications in autonomous combat missions introduce a new operational concept — distributed, coordinated engagement by large numbers of low-cost autonomous units — that challenges traditional platform-centric defense doctrine.

Sensor fusion and real-time battlefield data processing represent the enabling technology layer beneath all other trends. Systems that integrate radar, infrared, acoustic, and signals intelligence into a unified targeting picture give commanders a situational awareness advantage that no single-sensor platform can replicate. Therefore, vendors that establish sensor fusion capability as a core competency — rather than a single product feature — are positioned to capture the highest-margin integration contracts as multi-domain operations become standard military doctrine.

Regional Analysis

North America Dominates the Automated Weapon System Market with a Market Share of 43.80%, Valued at USD 18.4 Billion

North America holds a 43.80% share valued at USD 18.4 Billion, driven by the United States’ sustained defense modernization budgets, active smart battlefield program expansion, and a mature defense industrial base capable of rapid autonomous system integration. U.S. procurement cycles consistently prioritize AI-enabled platforms across all service branches, reinforcing North America’s structural lead over every other region.

Europe Automated Weapon System Market Trends

Europe accelerates defense investment following NATO capability commitments and escalating regional security requirements. Member states are increasing autonomous system procurement, with Germany, France, and the UK leading platform integration programs. In July 2024, RTX’s Raytheon received a $1.2 billion contract to supply additional Patriot air and missile defense systems to Germany, illustrating the scale of European automated defense spending currently being executed.

Asia Pacific Automated Weapon System Market Trends

Asia Pacific represents the fastest-expanding geographic demand pool for autonomous weapon systems, driven by sustained defense budget increases across China, India, South Korea, and Japan. Regional powers are investing in indigenous autonomous combat development programs while simultaneously procuring proven foreign platforms. This dual-track strategy accelerates regional capability development and creates diverse procurement pipelines across naval, aerial, and land system categories.

Middle East and Africa Automated Weapon System Market Trends

Middle East defense agencies prioritize border security automation and precision strike capability given persistent regional conflict conditions. GCC nations deploy unmanned combat and surveillance platforms across contested perimeters, creating consistent demand for integrated automated weapon solutions. Government procurement programs in Saudi Arabia and the UAE maintain multi-year defense technology acquisition pipelines that include both platform hardware and AI-enabled software systems.

Latin America Automated Weapon System Market Trends

Latin America remains an emerging market for automated weapon systems, with defense modernization programs in Brazil and Mexico driving the primary procurement activity. Budget constraints limit adoption of the most sophisticated autonomous platforms, concentrating regional demand on surveillance automation, border monitoring systems, and lower-cost unmanned platforms. However, expanding defense cooperation agreements with North America and Europe gradually introduce more advanced autonomous system specifications into regional procurement frameworks.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

BAE Systems positions itself as a full-spectrum autonomous defense integrator, maintaining deep relationships across land, naval, and aerial platform programs. Its strategic advantage lies in multi-domain system integration — the ability to combine sensors, weapons, and command architecture across service branch requirements. This breadth reduces customer concentration risk while enabling BAE to capture platform upgrade contracts as existing installations require AI-capability retrofit programs.

Honeywell leverages its aerospace electronics and navigation technology heritage to supply critical subsystems for autonomous weapon platforms rather than competing as a prime contractor. This component-level positioning insulates Honeywell from the highest-risk phases of weapons program development while capturing recurring revenue from sensor, guidance, and communication systems embedded across multiple prime contractor platforms worldwide.

Kongsberg Gruppen builds its competitive position around remote weapon station technology and precision naval systems. Its RT20 turret program — with a $329 million U.S. Marine Corps contract secured in November 2024 — demonstrates that Kongsberg has converted component expertise into prime contract wins at scale. This shift from subsystem supplier to platform-level contractor expands its addressable market while establishing operational deployment track records that support future program bids.

Textron focuses its autonomous system strategy on ground vehicle automation and unmanned aircraft systems, maintaining a competitive position in the medium-endurance unmanned platform category. Textron’s integrated defense portfolio — spanning both air and ground autonomous platforms — allows it to pursue joint procurement programs that require cross-domain coordination. This positions the company well for network-centric warfare programs where single-domain vendors face structural disadvantages in multi-domain contract competitions.

Key Players

- BAE Systems

- Honeywell

- Kongsberg Gruppen

- Textron

- Northrop Grumman

- Israel Aerospace Industries

- Mitsubishi Heavy Industries

- Thales Group

- Leonardo

- L3Harris Technologies

- Lockheed Martin

Recent Developments

- July 2024 — RTX’s Raytheon business received a $1.2 billion contract to provide additional Patriot air and missile defense systems to Germany. This contract expands deployment of systems that integrate automated engagement control and interceptor launch into a NATO ally’s active air defense architecture.

- October 2024 — RTX’s Raytheon business secured a $736 million contract from the U.S. Navy for AIM-9X Block II missiles. These missiles integrate into highly automated air-combat and shipborne weapon-control systems, reinforcing the U.S. Navy’s investment in autonomous engagement-ready munition inventories.

- November 2024 — The U.S. Army awarded Lockheed Martin a contract to increase PAC-3 MSE production capacity to approximately 650 missiles per year. This production expansion supports larger volumes of interceptor rounds integrated into automated air-and-missile-defense architectures, directly addressing U.S. and allied air defense readiness gaps.

Report Scope

Report Features Description Market Value (2025) USD 42.1 Billion Forecast Revenue (2035) USD 70.8 Billion CAGR (2026-2035) 5.3% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Land Systems, Naval Systems, Aerial Systems, Cyber Systems), By Component (Sensors, Weapons, Command & Control Systems, Communication Systems), By Technology (Artificial Intelligence, Machine Learning, Robotics, Autonomous Navigation), By Deployment Mode (On-Premises, Cloud-Based Systems), By End User (Military, Defense Contractors, Government Agencies) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape BAE Systems, Honeywell, Kongsberg Gruppen, Textron, Northrop Grumman, Israel Aerospace Industries, Mitsubishi Heavy Industries, Thales Group, Leonardo, L3Harris Technologies, Lockheed Martin Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Automated Weapon System MarketPublished date: Apr 2026add_shopping_cartBuy Now get_appDownload Sample

Automated Weapon System MarketPublished date: Apr 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- BAE Systems

- Honeywell

- Kongsberg Gruppen

- Textron

- Northrop Grumman

- Israel Aerospace Industries

- Mitsubishi Heavy Industries

- Thales Group

- Leonardo

- L3Harris Technologies

- Lockheed Martin

Our Clients

- 183771

- Apr 2026