Global Antiscalants Market Size, Share, And Industry Analysis Report By Type (Phosphonates, Carboxylates and Carbonates, Sulfonates, Fluorides, Other), By Process Type (Threshold Inhibitors, Crystal Modification, Dispersion, Others), By Application (Power and Construction, Oil and Gas, Mining, Municipal Water Treatment and Desalination, Food and Beverage, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 180108

- Number of Pages: 326

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

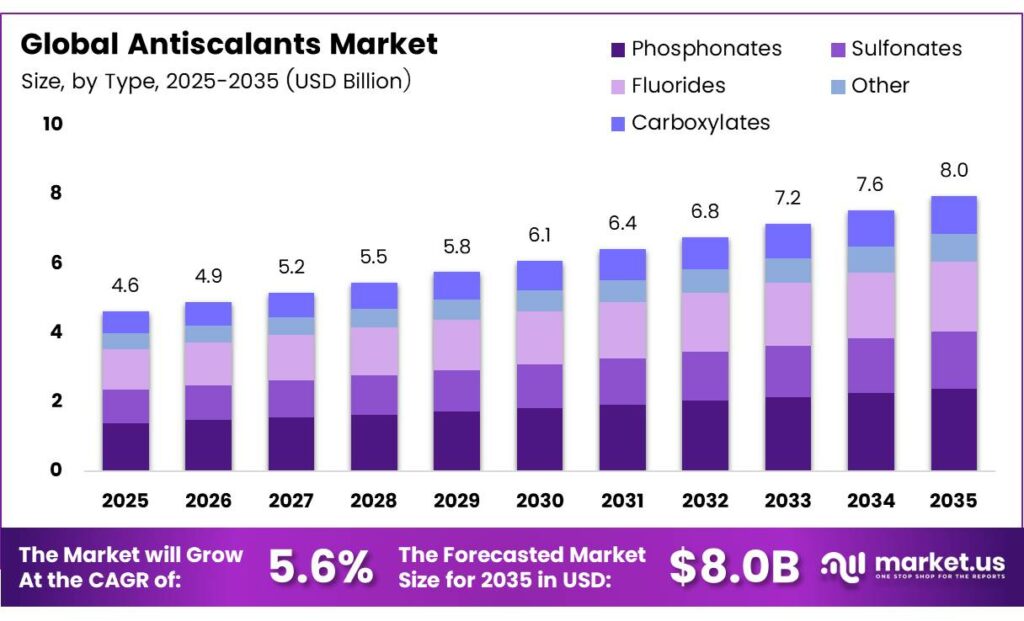

The Global Antiscalants Market size is expected to be worth around USD 8.0 billion by 2035 from USD 4.6 billion in 2025, growing at a CAGR of 5.6% during the forecast period 2026 to 2035.

Antiscalants are specialty chemicals used in water treatment systems to prevent scale formation on membranes, pipes, and heat exchangers. Industries apply these chemicals in reverse osmosis, cooling towers, and desalination plants. They extend equipment life, reduce downtime, and improve operational efficiency across water-intensive processes.

- Ecolab consolidated net sales reached USD 15,741.4 million in FY2024, reflecting the company’s extensive reach in water-treatment chemicals across industrial and institutional customers globally. This scale signals robust market demand for antiscalants within broader water chemistry portfolios.

Government investments in water infrastructure and desalination capacity continue to accelerate market growth. Regulatory frameworks in the Middle East, Asia Pacific, and North America mandate water treatment standards. Consequently, industrial facilities increase their chemical treatment budgets to comply with environmental discharge and reuse requirements.

- Veolia Water Technologies’ activity revenue reached EUR 4,973 million in FY2024, representing a major global platform for desalination and industrial water solutions. This revenue highlights how antiscalants remain core consumables in RO pretreatment and downstream process protection systems worldwide.

Desalination expansion in water-scarce regions creates strong, recurring demand for scale inhibitors. RO membrane systems require consistent antiscalant dosing to maintain flux and prevent fouling. Additionally, the shift toward zero liquid discharge policies in manufacturing sectors further amplifies the need for effective scaling control programs.

Key Takeaways

- The Global Antiscalants Market is valued at USD 4.6 billion in 2025 and is projected to reach USD 8.0 billion by 2035, at a CAGR of 5.6% during the forecast period 2026 to 2035.

- Phosphonates dominate with a 39.4% market share in 2025.

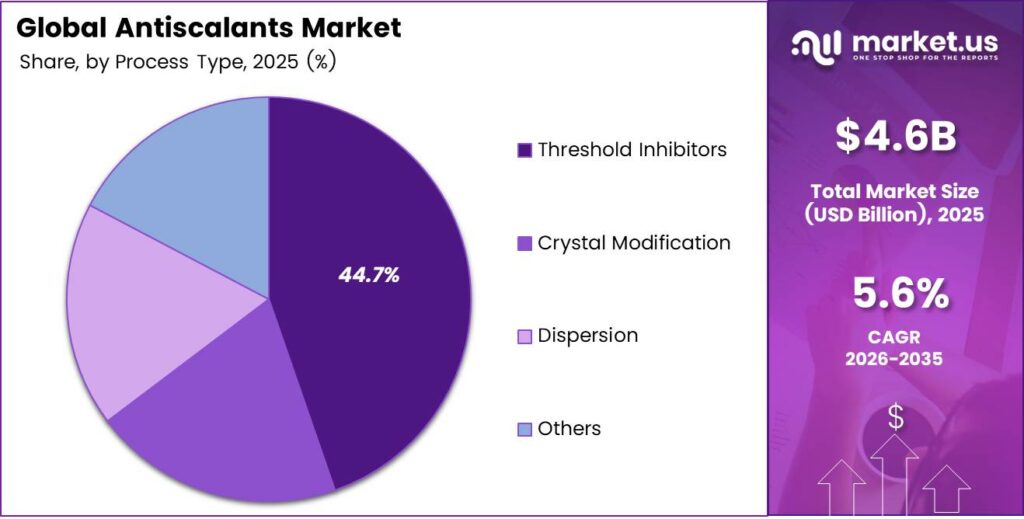

- Threshold Inhibitors hold the leading position with a 44.7% share.

- Power and Construction leads with a 32.6% share of the total market.

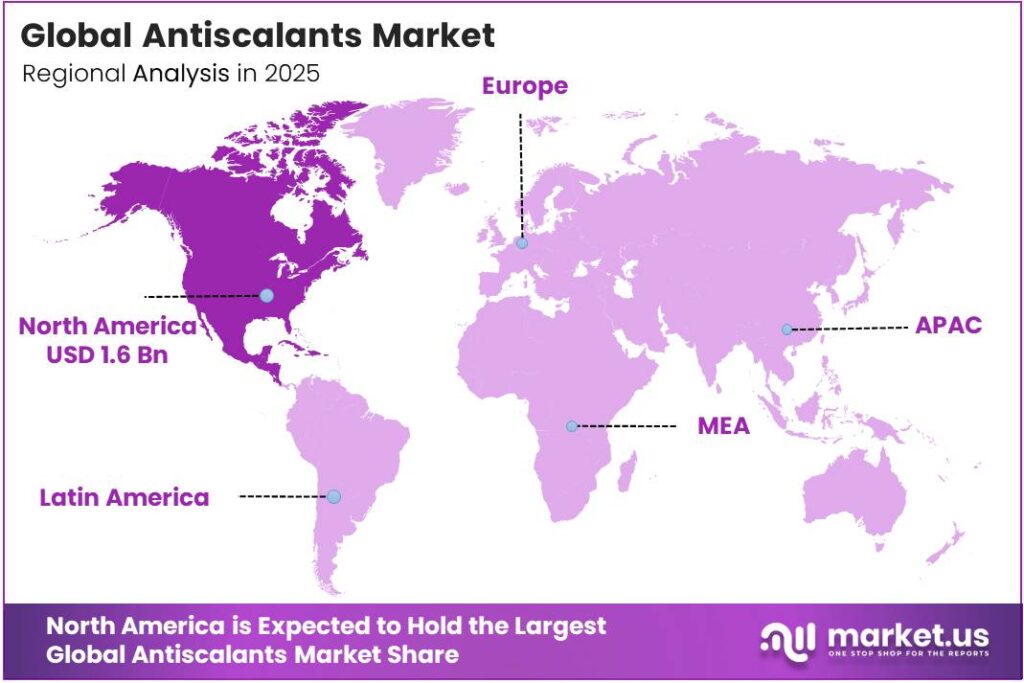

- North America holds the dominant regional position with a 34.9% share, valued at approximately USD 1.6 billion in 2025.

By Type Analysis

Phosphonates dominate with 39.4% due to superior scale inhibition performance and broad industrial compatibility.

In 2025, Phosphonates held a dominant market position in the By Type segment of the Antiscalants Market, with a 39.4% share. Phosphonates offer excellent threshold inhibition and chelation properties. They perform effectively across a wide pH range and temperature spectrum. Moreover, their stability under high-stress industrial conditions makes them the preferred choice in RO systems and cooling water treatment programs.

Carboxylates and Carbonates represent the second major category within the antiscalants type segment. These compounds provide effective dispersant and crystal modification functions. Consequently, they find broad use in municipal water treatment and food-grade applications where phosphonate restrictions apply. Their low toxicity profile also supports adoption in environmentally regulated industrial zones.

Sulfonates serve specialized applications in power generation and oil field water management. They demonstrate strong resistance to thermal degradation under extreme operating conditions. Additionally, sulfonate-based inhibitors show compatibility with mixed-salt brines in oilfield injection water systems. Their targeted performance in high-temperature environments ensures steady demand in energy-intensive industries.

Fluorides and Other types occupy smaller but technically significant portions of the antiscalants market. Fluoride-based compounds address silica and calcium fluoride scale challenges in specific process streams. Other specialty inhibitors include blended formulations that combine multiple inhibition mechanisms to tackle complex scaling scenarios in chemical processing and pharmaceutical water circuits.

By Process Type Analysis

Threshold Inhibitors dominate with 44.7% due to effectiveness at low concentrations and broad system compatibility.

In 2025, Threshold Inhibitors held a dominant market position in the By Process Type segment of the Antiscalants Market, with a 44.7% share. These inhibitors function effectively at very low dosage levels, making them cost-efficient for large-scale water treatment operations. Furthermore, their ability to delay crystallization and prevent mineral deposition supports continuous operation in RO and cooling water systems.

Crystal Modification inhibitors alter the growth pattern of scale crystals to reduce adhesion on surfaces. This process ensures that even when minerals precipitate, they remain dispersed rather than forming hard deposits. Consequently, crystal modification compounds see strong use in boiler feed water treatment and heat exchanger protection applications across power and manufacturing facilities.

Dispersion inhibitors keep already-formed particles suspended in solution, preventing their accumulation on equipment surfaces. These products complement threshold and crystal modification approaches in multi-mechanism treatment programs. Additionally, dispersion-type antiscalants support the performance of other water treatment chemistries, making them essential components of integrated chemical treatment packages in industrial facilities.

Others in the process type category include sequestration and chelation-based inhibition methods. These approaches bind scale-forming ions directly to prevent their participation in precipitation reactions. Though smaller in volume share, sequestrant-based programs address complex scaling in pharmaceutical water systems, specialty manufacturing, and food-grade process water circuits requiring ultra-pure water standards.

By Application Analysis

Power and Construction dominate with 32.6% due to intensive water use and critical infrastructure protection needs.

In 2025, Power and Construction held a dominant market position in the By Application segment of the Antiscalants Market, with a 32.6% share. Thermal and nuclear power plants rely heavily on antiscalants to protect cooling systems and boiler circuits. Moreover, large-scale construction projects increasingly integrate water recycling loops that require continuous scale management to sustain operational efficiency.

Oil and Gas applications demand antiscalants for injection water treatment, produced water management, and pipeline protection. Scale deposits in oilfield water circuits cause significant production losses and equipment damage. Therefore, operators invest consistently in advanced scale inhibition programs to maintain flow assurance and extend the productive life of subsurface and surface processing assets.

Mining operations use antiscalants in process water circuits where mineral-rich water interacts with equipment and membranes. Calcium carbonate, barium sulfate, and silica deposits commonly affect mining water systems. Consequently, antiscalant demand in mining grows alongside global mineral extraction activity, especially in copper, lithium, and gold processing operations in arid regions.

Municipal Water Treatment and Desalination applications represent a rapidly growing segment driven by global water scarcity challenges. Desalination plant operators depend on antiscalants to protect RO membranes from carbonate and sulfate fouling. Additionally, the Food and Beverage, Chemical and Pharmaceutical, and Pulp and Paper sectors contribute to diversified demand across industrial water treatment applications globally.

Key Market Segments

By Type

- Phosphonates

- Carboxylates and Carbonates

- Sulfonates

- Fluorides

- Other

By Process Type

- Threshold Inhibitors

- Crystal Modification

- Dispersion

- Others

By Application

- Power and Construction

- Oil and Gas

- Mining

- Municipal Water Treatment and Desalination

- Food and Beverage

- Chemical and Pharmaceutical

- Pulp and Paper

- Others

Emerging Trends

Eco-Friendly Formulations and Smart Dosing Technologies Reshape the Antiscalants Industry

Environmental regulations push chemical manufacturers to develop biodegradable and bio-based antiscalant formulations. Industries increasingly replace conventional phosphonate products with green alternatives that reduce aquatic toxicity. Moreover, regulators in Europe and North America enforce stricter discharge standards, accelerating the shift toward sustainable water treatment chemistries.

- AI-enabled smart dosing systems are transforming industrial water management practices. These platforms analyze real-time sensor data to optimize antiscalant injection rates and reduce chemical waste. Consequently, facilities achieve better scale control outcomes at lower operating costs. SUEZ’s total revenues reached EUR 9,189 million in FY2024, reflecting the scale of water operations where sustainable chemical demand is rising rapidly.

Sulfonate-based inhibitors gain traction in power generation and high-temperature process environments. Their thermal stability and compatibility with complex brine chemistries make them valuable in energy-intensive sectors. Additionally, rapid industrial expansion across the Asia Pacific drives regional demand for antiscalants, particularly in China and India, where water treatment infrastructure investments continue to accelerate at a significant pace.

Drivers

Industrialization, Desalination Expansion, and Oil Sector Growth Drive Antiscalants Market Demand

Rapid industrialization and urban growth worldwide increase the volume of water consumed and treated across industrial processes. Factories, power plants, and municipal systems require reliable scale management programs to protect equipment. Moreover, government-funded water infrastructure projects in developing economies consistently expand the installed base of water treatment systems requiring antiscalant dosing.

- Desalination capacity expansion in arid coastal regions drives persistent demand for high-performance scale inhibitors. Countries in the Middle East and North Africa invest heavily in seawater reverse osmosis plants. Kemira Group revenue reached EUR 2,948.1 million in FY2024, confirming robust demand for water-treatment chemistries co-specified alongside antiscalants in industrial programs.

Oil and gas sector growth necessitates advanced scale management in injection water, produced water, and pipeline systems. Oilfield operators face significant operational risks from barium sulfate and calcium carbonate deposition in subsurface equipment. Therefore, exploration and production companies allocate dedicated chemical treatment budgets that include antiscalant programs as non-negotiable components of flow assurance and asset integrity management strategies.

Restraints

Environmental Concerns and Raw Material Cost Volatility Restrain Antiscalants Market Growth

Traditional antiscalant formulations, particularly phosphonate-based products, face growing scrutiny over their environmental and aquatic toxicity profiles. Regulatory agencies in Europe and North America impose increasingly strict discharge limits on phosphorus-containing chemicals. Consequently, manufacturers bear higher compliance costs and face product reformulation pressures, slowing the introduction of new chemical treatment programs in regulated industrial markets.

Volatility in raw material prices significantly impacts the profitability of antiscalant producers. Key inputs such as phosphoric acid, acrylic acid, and maleic anhydride experience frequent price swings driven by energy costs and supply chain disruptions. Therefore, manufacturers struggle to maintain stable pricing for their customers while absorbing input cost increases. This uncertainty reduces investment confidence and constrains long-term capacity expansion planning.

Smaller industrial operators often resist adopting advanced antiscalant programs due to perceived high treatment costs. Budget constraints in water-intensive small and medium enterprises limit chemical treatment adoption. Moreover, a lack of technical awareness about the long-term cost savings from scale prevention versus equipment replacement further delays market penetration in price-sensitive industrial segments in developing markets.

Growth Factors

Bio-Based Innovation, Desalination Investment, and Digital Water Technologies Accelerate Market Expansion

Development of bio-based and environmentally compatible antiscalant formulations creates new growth pathways for specialty chemical producers. Bio-based products open access to regulated markets where traditional phosphonate chemistries face restrictions, expanding the total addressable customer base for antiscalant suppliers globally.

- Global investments in desalination infrastructure present significant long-term demand for antiscalants. Governments in the Middle East, India, and Southeast Asia fund large-scale seawater treatment capacity to address freshwater shortages. Italmatch Chemicals’ contribution margin improved to EUR 276 million from EUR 251 million in FY2023, signaling growing profitability in specialty water treatment product lines.

Technological advancements in antiscalant chemistry improve inhibition efficiency at lower dosage levels. Next-generation polymer-based inhibitors deliver superior performance against silica, calcium sulfate, and carbonate scales. Additionally, the integration of digital sensors and analytics platforms enables predictive scaling risk management, helping industrial water operators apply antiscalants more precisely and cost-effectively across complex water treatment systems.

Regional Analysis

North America Dominates the Antiscalants Market with a Market Share of 34.9%, Valued at USD 1.6 Billion

North America leads the global antiscalants market with a 34.9% share, valued at approximately USD 1.6 billion in 2025. The region benefits from a large industrial base spanning power generation, oil and gas, and municipal water treatment sectors. Moreover, stringent EPA water quality regulations and substantial investments in aging water infrastructure drive consistent demand for advanced scale inhibition solutions across the United States and Canada.

Europe maintains a strong position in the global antiscalants market, supported by rigorous water treatment regulations and well-established industrial sectors. Germany, France, and the UK invest actively in water reuse and circular economy programs. Consequently, demand for eco-compatible and biodegradable antiscalant formulations grows faster in Europe than in any other region, pushing chemical manufacturers to innovate green product portfolios.

Asia Pacific represents the fastest-growing region in the antiscalants market, driven by rapid industrialization in China, India, and Southeast Asia. Expanding manufacturing capacity, power sector growth, and new desalination projects fuel chemical treatment demand. Additionally, governments across the region are increasing infrastructure investment in municipal water systems, creating large new markets for antiscalant suppliers serving both local and international industrial customers.

The Middle East and Africa region demonstrates strong antiscalant demand, primarily driven by extensive desalination activities. GCC nations operate some of the world’s largest seawater reverse osmosis plants, requiring consistent antiscalant dosing programs. Furthermore, oil and gas operations across the Gulf region and North Africa generate significant industrial water treatment needs, sustaining long-term demand for scale inhibition chemicals in challenging high-temperature environments.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Dow operates as one of the world’s leading specialty chemical and materials science companies. Its water solutions portfolio includes a comprehensive range of antiscalants and scale inhibitors for RO membrane systems, cooling towers, and industrial boilers. Dow’s global manufacturing network and deep technical expertise allow it to serve diverse end-use markets, including desalination, power generation, and municipal water treatment, with consistent product quality.

BASF SE delivers specialty water treatment chemicals through its Performance Chemicals division, covering scale inhibition, corrosion control, and deposit management applications. The company applies its polymer chemistry strengths to develop high-performance antiscalant formulations suited to demanding industrial environments. BASF’s global R&D infrastructure enables continuous product innovation, helping customers in oil and gas, mining, and water treatment sectors improve operational efficiency and reduce total chemical treatment costs.

Ecolab, through its Nalco Water platform, provides integrated water management solutions to industrial and institutional customers worldwide. The company’s antiscalant and scale inhibitor programs address challenges in cooling water, boiler treatment, and membrane separation systems. Ecolab combines chemical treatment with digital monitoring technologies, enabling customers to optimize antiscalant dosing in real time. Its broad service network supports customers across the power, food processing, and manufacturing industries globally.

Solenis focuses on specialty water treatment and process chemicals for industrial and institutional markets. The company offers targeted antiscalant solutions for RO systems, cooling towers, and mining process water. Solenis emphasizes sustainable formulations and technical service support to help customers achieve water efficiency goals. Its acquisition-driven growth strategy and specialized application expertise position it as a significant player in the global antiscalants market across multiple end-use verticals.

Top Key Players in the Market

- Dow

- BASF SE

- Ecolab

- Solenis

- Kemira

- Kurita Water Industries Ltd.

- Syensqo

- Clariant

- Veolia

- Italmatch Chemicals S.p.A.

Recent Developments

- In 2025, Kemira, an older scale-inhibition monitoring technology at the SPE Oilfield Scale Conference, now marketed as KemConnect SI, uses a portable in-field detection protocol for residual polymeric inhibitors in produced waters. The company continues to market its established KemGuard family of polymeric antiscalants and dispersants, described as versatile chemistries for challenging scale-control applications.

- In 2025, Solenis official product pages prominently feature current innovations in the antiscalants/scale-inhibitors portfolio for industrial water and process streams: Use multiple mechanisms (dispersion, inhibition, crystal modification, and sequestration) to control common and uncommon scales (calcium, barium, magnesium, manganese, silicate, sulfate). Applications span heavy process-water users; case histories include superior digester performance and a gold mine pairing with OnGuard.

Report Scope

Report Features Description Market Value (2025) USD 4.6 Billion Forecast Revenue (2035) USD 8.0 Billion CAGR (2026-2035) 5.6% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Phosphonates, Carboxylates and Carbonates, Sulfonates, Fluorides, Other), By Process Type (Threshold Inhibitors, Crystal Modification, Dispersion, Others), By Application (Power and Construction, Oil and Gas, Mining, Municipal Water Treatment and Desalination, Food and Beverage, Chemical and Pharmaceutical, Pulp and Paper, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Dow, BASF SE, Ecolab, Solenis, Kemira, Kurita Water Industries Ltd., Syensqo, Clariant, Veolia, Italmatch Chemicals S.p.A. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- Dow

- BASF SE

- Ecolab

- Solenis

- Kemira

- Kurita Water Industries Ltd.

- Syensqo

- Clariant

- Veolia

- Italmatch Chemicals S.p.A.

Our Clients

- 180108

- March 2026