Quick Navigation

Report Overview

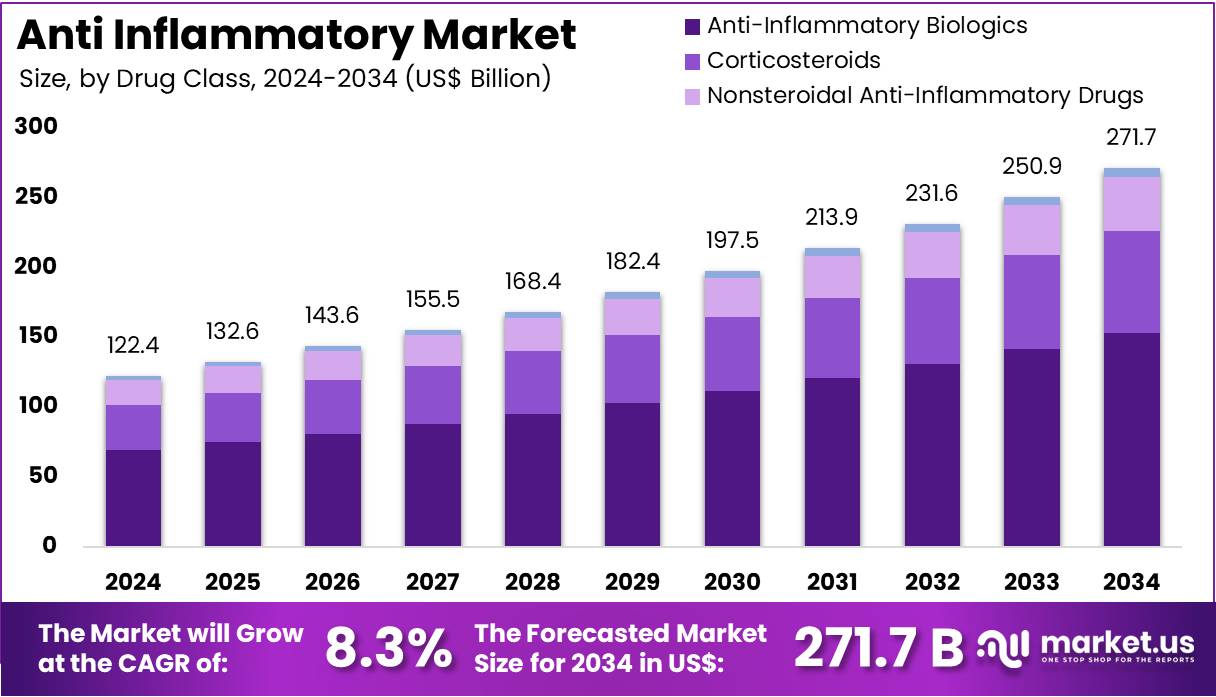

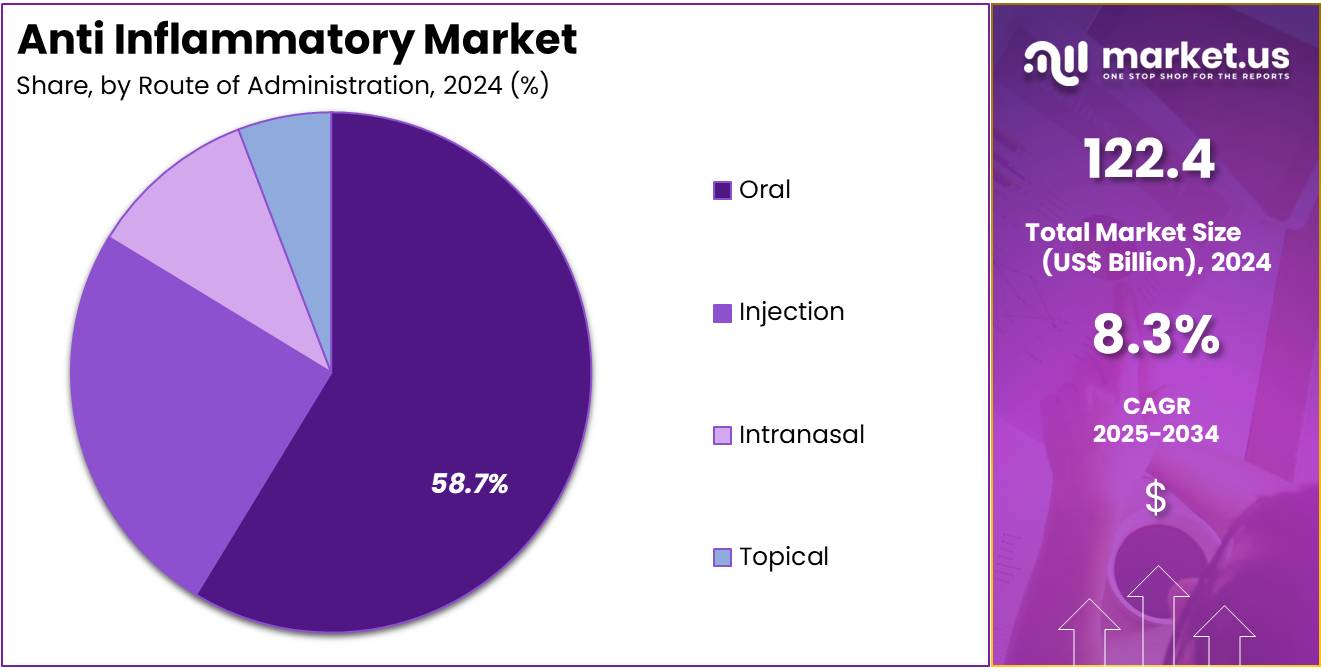

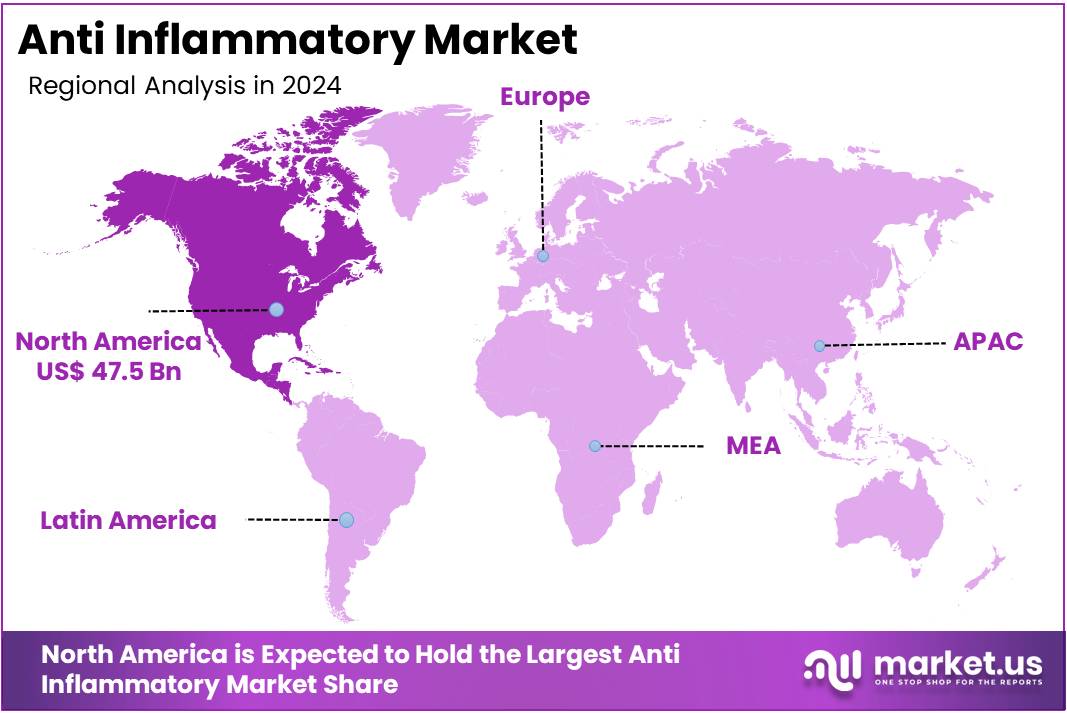

The Global Anti Inflammatory Market size is expected to be worth around US$ 217.7 Billion by 2034, from US$ 122.4 Billion in 2024, growing at a CAGR of 8.3% during the forecast period from 2025 to 2034. North America held a dominant market position, capturing more than a 38.8% share and holds US$ 47.5 Billion market value for the year.

Increasing awareness of chronic inflammatory conditions and the rising prevalence of autoimmune diseases are key drivers fueling the growth of the anti-inflammatory market. The demand for effective anti-inflammatory treatments spans various applications, including pain management, rheumatoid arthritis, asthma, cardiovascular diseases, and inflammatory bowel diseases.

Patients and healthcare providers alike are seeking innovative therapies that can manage inflammation more efficiently and with fewer side effects. The market has seen a surge in biologic therapies, especially monoclonal antibodies, which offer targeted treatment options.

In March 2022, Pfizer Inc. completed the acquisition of Arena Pharmaceuticals, further strengthening its position in the fields of gastroenterology, dermatology, and cardiology. This strategic acquisition significantly augmented Pfizer’s capabilities, particularly within its inflammation and immunology division, advancing its overall therapeutic portfolio.

With advancements in molecular biology and biotechnology, pharmaceutical companies are positioning themselves to bring novel, more personalized anti-inflammatory treatments to the market, addressing unmet needs in both acute and chronic inflammation management.

Key Takeaways

- In 2024, the market for anti inflammatory generated a revenue of US$ 112.4 billion, with a CAGR of 8.3%, and is expected to reach US$ 271.7 billion by the year 2034.

- The drug class segment is divided into anti-inflammatory biologics, corticosteroids, nonsteroidal anti-inflammatory drugs, and others, with anti-inflammatory biologics taking the lead in 2024 with a market share of 56.5%.

- Considering treatment, the market is divided into arthritis, chronic obstructive pulmonary disease, inflammatory bowel disease, multiple sclerosis, and others. Among these, arthritis held a significant share of 48.2%.

- Furthermore, concerning the route of administration segment, the market is segregated into oral, injection, intranasal, and topical. The oral sector stands out as the dominant player, holding the largest revenue share of 58.7% in the anti inflammatory market.

- The sales channel segment is segregated into prescription and over-the-counter, with the prescription segment leading the market, holding a revenue share of 62.3%.

- North America led the market by securing a market share of 38.8% in 2024.

Drug Class Analysis

The anti-inflammatory biologics segment led in 2024, claiming a market share of 56.5% as biologic therapies continue to demonstrate superior efficacy in treating chronic inflammatory diseases. The increasing prevalence of autoimmune diseases such as rheumatoid arthritis, psoriasis, and inflammatory bowel diseases, coupled with the growing adoption of biologics in treatment regimens, is likely to fuel this growth.

Biologics, which target specific molecules involved in the inflammatory process, are anticipated to provide better-targeted treatments with fewer side effects compared to traditional therapies, making them a preferred choice for both patients and healthcare providers.

Treatment Analysis

The arthritis held a significant share of 48.2% due to the rising global incidence of arthritis, particularly osteoarthritis and rheumatoid arthritis. The aging population and increasing obesity rates are expected to contribute significantly to the growing prevalence of these conditions.

Moreover, advancements in biologic treatments and an improved understanding of disease mechanisms will likely enhance the effectiveness of arthritis management. The continuous innovation in drug therapies, including disease-modifying anti-rheumatic drugs (DMARDs) and biologics, is anticipated to drive market growth in this segment.

Route of Administration Analysis

The oral segment had a tremendous growth rate, with a revenue share of 58.7% as oral formulations offer convenience and ease of use, making them a preferred option for patients with chronic conditions requiring long-term treatment. The ongoing development of new oral anti-inflammatory drugs with improved efficacy and fewer side effects is anticipated to contribute to the growth of this segment.

Moreover, the increasing demand for at-home treatments for conditions like arthritis and inflammatory bowel disease will likely drive the adoption of oral anti-inflammatory drugs over other administration routes.

Sales Channel Analysis

The prescription segment grew at a substantial rate, generating a revenue portion of 62.3% due to the rising demand for prescription-strength medications for the management of chronic inflammatory conditions. Patients with severe forms of arthritis, psoriasis, and inflammatory bowel diseases often require stronger anti-inflammatory medications that can only be obtained through prescriptions.

The growing healthcare infrastructure, along with increased awareness and diagnosis of inflammatory diseases, is projected to contribute to the growth of this segment, as healthcare providers prescribe more specialized treatments to manage these conditions effectively.

Key Market Segments

By Drug Class

- Anti-inflammatory biologics

- Corticosteroids

- Nonsteroidal anti-inflammatory drugs

- Others

By Treatment

- Arthritis

- Chronic obstructive pulmonary disease

- Inflammatory bowel disease

- Multiple sclerosis

- Others

By Route of Administration

- Oral

- Injection

- Intranasal

- Topical

By Sales Channel

- Prescription

- Over-the-counter

Drivers

Rising Global Burden of Chronic Diseases is driving the market

The increasing prevalence of chronic inflammatory diseases worldwide is a major driver for the anti-inflammatory market. Conditions such as arthritis (rheumatoid and osteoarthritis), inflammatory bowel disease (IBD), asthma, and other autoimmune disorders are becoming more common due to factors like the aging global population, sedentary lifestyles, and unhealthy dietary habits. The European Pain Federation reported in 2023 that 740 million people experienced severe pain, with approximately 20% of these cases becoming chronic.

Furthermore, the World Health Organization (WHO) stated in 2023 that around 262 million people globally suffer from asthma, a condition characterized by airway inflammation. As the incidence of these chronic inflammatory conditions rises, the demand for effective anti-inflammatory drugs to manage pain and improve the quality of life for patients also increases, thereby fueling market growth. The need for both prescription and over-the-counter anti-inflammatory medications is expected to remain substantial in the foreseeable future due to these demographic and lifestyle trends.

Restraints

Side Effects and Safety Concerns are restraining the market

Despite their effectiveness, many anti-inflammatory drugs, particularly non-steroidal anti-inflammatory drugs (NSAIDs) and corticosteroids, are associated with potential side effects that can restrain market growth. Long-term use of NSAIDs can lead to gastrointestinal issues such as ulcers and bleeding, as well as increase the risk of cardiovascular events. Corticosteroids can cause a range of side effects including weight gain, mood changes, and increased blood pressure.

These safety concerns can lead to cautious prescribing by healthcare professionals and reluctance among patients to adhere to long-term treatment, especially for mild to moderate conditions where the perceived risks might outweigh the benefits. The French Health Minister raised concerns in 2020 regarding the potential negative effects of NSAIDs on COVID-19 outcomes, highlighting the ongoing scrutiny of these drugs’ safety profiles. Consequently, the market growth for certain traditional anti-inflammatory drugs can be hampered by these well-documented adverse effects and the search for safer alternatives.

Opportunities

Development of Novel Biologics and Targeted Therapies is creating growth opportunities

The increasing understanding of the complex mechanisms underlying inflammatory diseases has spurred the development of novel biologic therapies and targeted small molecules, creating significant growth opportunities in the anti-inflammatory market. Biologics, derived from living organisms, offer more specific targeting of inflammatory pathways compared to traditional broad-acting drugs, often resulting in improved efficacy and fewer systemic side effects.

The anti-tumor necrosis factor (TNF) segment held a substantial share of the anti-inflammatory biologics market in 2022, reflecting the effectiveness of these drugs in treating conditions like rheumatoid arthritis and IBD. Furthermore, the development of Janus kinase (JAK) inhibitors and other targeted therapies provides new options for patients with autoimmune and inflammatory diseases.

Impact of Macroeconomic / Geopolitical Factors

The anti-inflammatory market’s performance is intertwined with macroeconomic conditions. Economic growth typically supports increased healthcare expenditure, driving demand for anti-inflammatory drugs. Conversely, economic contractions can lead to tighter healthcare budgets and potentially affect patient access to these medications. Inflationary pressures can increase the cost of pharmaceutical production, potentially translating to higher drug prices.

Geopolitical events, such as trade disputes or regional instabilities, can disrupt the global supply chains of active pharmaceutical ingredients and finished drug products, leading to price fluctuations and potential shortages. The global prevalence of conditions requiring anti-inflammatory treatment is substantial; for instance, osteoarthritis affects over 32.5 million adults in the United States alone, creating a significant and consistent demand for related medications.

The potential imposition of a 10% baseline US tariff on imported pharmaceuticals, including anti-inflammatory drugs, has raised concerns within the market. A significant portion of the active pharmaceutical ingredients and finished anti-inflammatory products consumed in the US are sourced from overseas. For example, in 2023, the US imported approximately $70 billion worth of pharmaceutical preparations. Tariffs could increase the cost of these imports, potentially leading to higher drug prices for consumers.

Generic anti-inflammatory drugs, which constitute a large segment of the market and are often price-sensitive, could be particularly affected. Data from 2022 indicated that generic drugs accounted for about 90% of all prescriptions dispensed in the US but only about 20% of the total drug spending. Increased tariffs could reduce the cost advantage of these generics, potentially impacting patient access and healthcare costs.

Latest Trends

Growing Preference for Topical and Localized Anti-inflammatory Formulations is a recent trend

A notable recent trend in the anti-inflammatory market is the increasing preference for topical and localized formulations to treat pain and inflammation. These formulations, such as creams, gels, and patches, offer the advantage of delivering the drug directly to the site of inflammation, minimizing systemic exposure and reducing the risk of systemic side effects associated with oral or injectable medications.

This trend is particularly evident in the management of musculoskeletal pain and localized inflammatory conditions like osteoarthritis and tendonitis. The oral segment is expected to maintain a significant market share due to convenience, but the topical segment is witnessing increased adoption due to its safety profile.

This shift towards localized therapies aligns with the growing emphasis on patient safety and the desire to minimize drug exposure to the entire body. Pharmaceutical companies are increasingly investing in the development of advanced topical formulations with enhanced penetration and efficacy to cater to this growing demand.

Regional Analysis

North America is leading the Anti Inflammatory Market

North America dominated the market with the highest revenue share of 38.8% owing to an aging population and the increasing prevalence of chronic inflammatory conditions. The Centers for Disease Control and Prevention (CDC) reported in 2023 that approximately 54.4 million adults in the US had doctor-diagnosed arthritis between 2019 and 2021, a condition frequently requiring anti-inflammatory medications.

The American Academy of Orthopaedic Surgeons (AAOS) highlighted the rising incidence of osteoarthritis, particularly among individuals aged 65 and older, a demographic that continues to expand. Furthermore, the National Institutes of Health (NIH) has ongoing research into inflammatory diseases such as rheumatoid arthritis and inflammatory bowel disease, indicating a sustained focus on managing these conditions with pharmacological interventions.

In 2024, the US Food and Drug Administration (FDA) approved several new formulations and biosimilars for inflammatory conditions, expanding treatment options available to patients. This regulatory activity reflects the persistent need for effective therapies in this area.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to a growing geriatric population and a rise in lifestyle-related inflammatory disorders. The United Nations Economic and Social Commission for Asia and the Pacific (ESCAP) projected in 2024 that the number of people aged 65 and over in the Asia-Pacific region will reach nearly 650 million by 2050, indicating a substantial increase in the population susceptible to inflammatory conditions. The World Health Organization (WHO) has noted an increasing prevalence of autoimmune diseases in several countries within the Asia Pacific region.

Additionally, increased awareness regarding chronic pain management and the availability of advanced diagnostic techniques are expected to contribute to greater demand for medications that reduce inflammation. Government initiatives aimed at improving healthcare access and affordability across the region are also likely to facilitate market expansion for these therapeutic agents.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the anti-inflammatory drugs market drive growth through technological innovation, strategic acquisitions, and expanding their global presence. They invest in developing novel therapeutics and vaccines to address various inflammatory diseases and improve patient outcomes. Collaborations with research institutions and healthcare providers facilitate the integration of new technologies and broaden market reach.

Additionally, targeting emerging markets with increasing healthcare infrastructure and rising disease prevalence presents significant growth opportunities. AbbVie Inc., headquartered in North Chicago, Illinois, is a global biopharmaceutical company specializing in immunology, oncology, neuroscience, eye care, virology, and women’s health.

In 2023, AbbVie reported revenues of approximately US$ 58 billion, with a significant portion attributed to its immunology segment, which includes treatments for rheumatoid arthritis and inflammatory bowel disease. The company operates in over 70 countries, focusing on advancing care for patients through continuous innovation and strategic expansions.

Top Key Players in the Anti Inflammatory Market

- Montai Therapeutics

- AbbVie Inc.

- Pfizer Inc.

- Johnson & Johnson

- Novartis AG

- Merck & Co., Inc.

- Bristol Myers Squibb

- Sanofi S.A.

Recent Developments

- In February 2025, Montai Therapeutics launched an innovative approach in the field of inflammatory and immunological diseases by combining small molecule development with AI-powered discovery. This cutting-edge strategy has led to the creation of the next generation of therapeutics aimed at treating complex immune disorders.

- In May 2023, AbbVie Inc received FDA approval for RINVOQ (upadacitinib) to treat adults suffering from moderately to severely active Crohn’s disease. This approval marks a significant milestone for AbbVie, enhancing its anti-inflammatory drug portfolio and bolstering the company’s growth in the immunology market.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 122.4 billion |

| Forecast Revenue (2034) | US$ 271.7 billion |

| CAGR (2025-2034) | 8.3% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Drug Class (Anti-inflammatory Biologics, Corticosteroids, Nonsteroidal Anti-inflammatory Drugs, and Others), By Treatment (Arthritis, Chronic Obstructive Pulmonary Disease, Inflammatory Bowel Disease, Multiple Sclerosis, and Others), By Route of Administration (Oral, Injection, Intranasal, and Topical), By Sales Channel (Prescription and Over-the-counter) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Montai Therapeutics, AbbVie Inc., Pfizer Inc., Johnson & Johnson, Novartis AG, Merck & Co., Inc., Bristol Myers Squibb, Sanofi S.A. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |