Quick Navigation

Report Overview

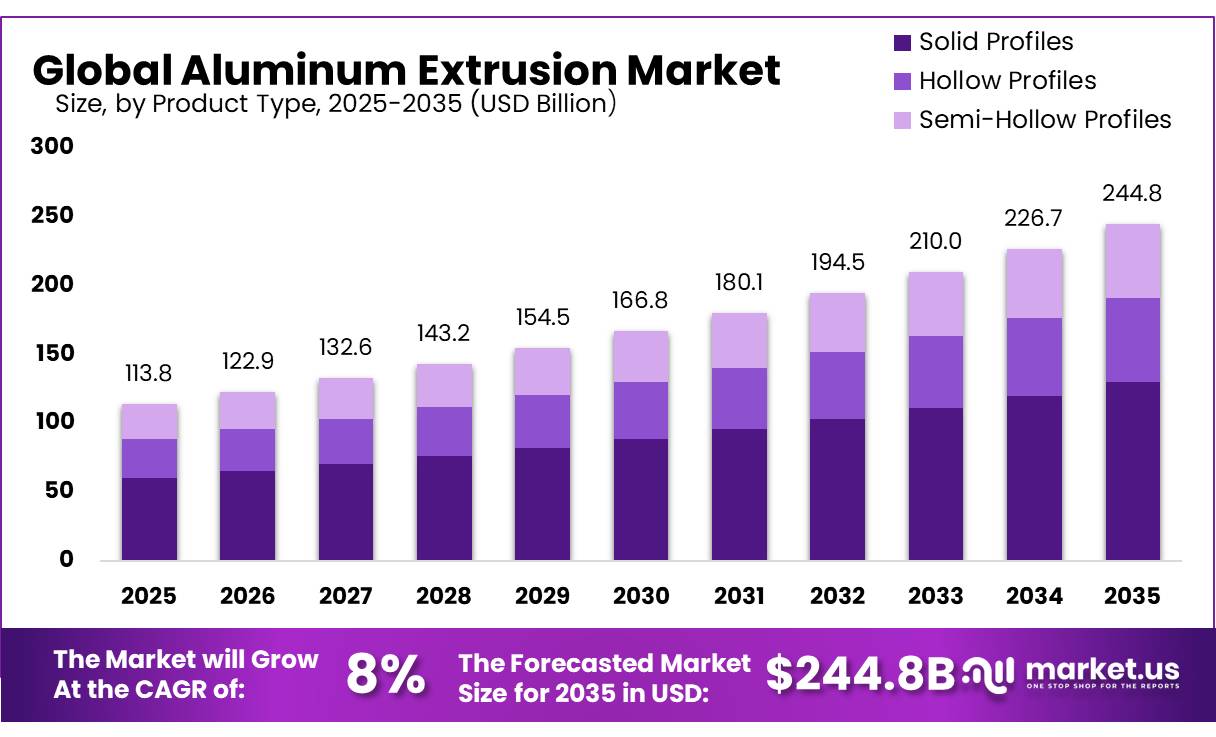

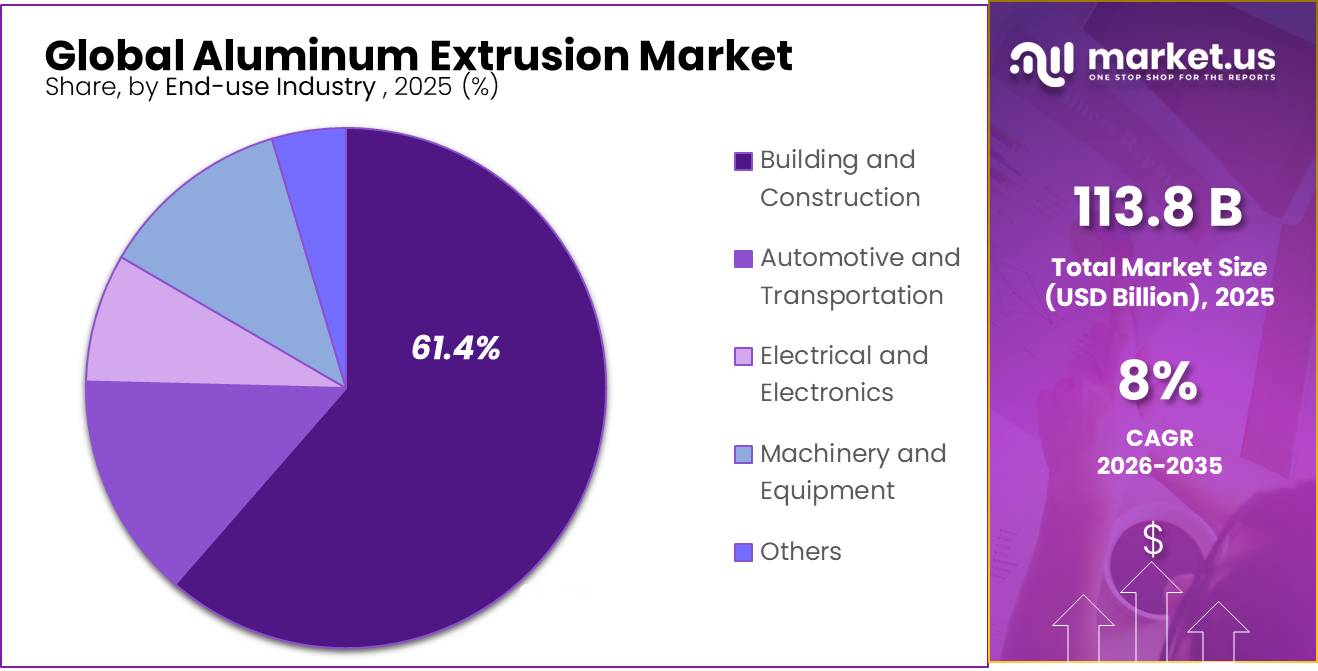

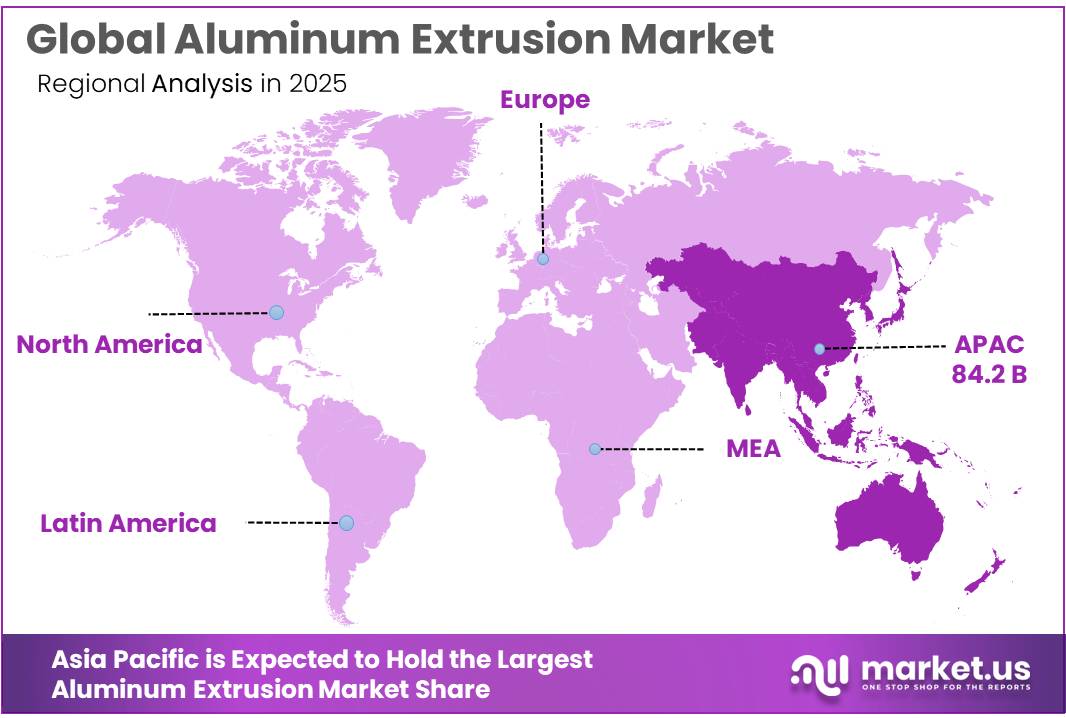

In 2025, the Global Aluminum Extrusion Market was valued at US$113.8 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 8%, reaching about US$244.8 billion by 2035. Asia Pacific held a dominant market position, capturing more than a 74% share, holding US$84.2 billion in revenue.

Key Takeaways

- The Global aluminum extrusion market was valued at US$113.8 billion in 2025.

- The Global aluminum extrusion market is projected to grow at a CAGR of 8% and is estimated to reach US$244.8 billion by 2035.

- By product type, solid profiles dominated the aluminum extrusion market, accounting for 53.0% of the total market share.

- Based on alloy type, the 6000 series segment led the market with 65.0% of the total market share, driven by its high strength, corrosion resistance, and versatility.

- By surface finish, mill finished extrusions held the largest share at 42.0%, supported by their cost-effectiveness and widespread industrial use.

- Among end-use industries, building and construction dominated the market, representing 61.4% of the total share, owing to strong demand from residential, commercial, and infrastructure projects.

- In 2025, Asia Pacific emerged as the leading regional market, accounting for 74% of the global market share, supported by rapid urbanization, infrastructure development, and expanding manufacturing activities.

The global aluminum extrusion market is a critical component of the larger aluminum industry, driven by rising demand for lightweight, robust, and recyclable materials in a variety of end-use applications. Aluminum extrusions are commonly used in building and construction, automotive and transportation, electrical and electronics, mechanical, and industrial applications due to their high strength-to-weight ratio, corrosion resistance, design flexibility, and extended service life.

Rapid urbanization, infrastructural expansion, increased acceptance of electric vehicles, and more investment in renewable energy projects are all helping the market grow. Aluminum’s capacity to support energy-efficient construction designs and environmentally friendly manufacturing techniques increases its commercial attractiveness.

To meet environmental and performance standards, the industry is shifting toward improved extrusion methods, bespoke profile designs, and growing usage of recycled aluminum.

- In March 2025, according to the International Renewable Energy Agency (IRENA), global renewable energy capacity expanded by more than 585 GW in 2024, marking the largest annual increase on record and boosting demand for aluminum extrusions used in solar mounting systems, wind energy structures, and electrical infrastructure.

- Government and trade policies are also influencing the industry. Reuters reported that the United States imported approximately US$27.4 billion worth of aluminum in 2024, reflecting the strategic importance of aluminum supply chains to transportation, construction, and manufacturing sectors. Meanwhile, several regions are implementing policies to secure aluminum scrap supplies as recycling becomes increasingly important for industrial decarbonization goals.

Aluminum Extrusion Market Segmentation

Product Type Analysis

Solid Profiles dominate with 53.0% due to strength, flexibility, and industrial use.

In 2025,Solid Profiles held a dominant market position, capturing more than a 53.0% share. In December 2025, demand remained strong across construction, automotive, transport, machinery, and consumer goods. These profiles are widely selected for frames, supports, rails, trims, and structural parts because they provide reliable strength, smooth finishing, and easy fabrication. Manufacturers also prefer solid profiles because they can be cut, drilled, machined, and shaped for different project needs.

Hollow Profiles emerged as the growing segment, supported by rising use in window systems, doors, curtain walls, vehicle structures, and modular construction. Their lighter weight, internal space, and balanced strength help reduce material use while improving design efficiency. Growing interest in energy-efficient buildings and lightweight transportation is expected to support adoption.

Alloy Type Analysis

6000 Series dominates with 65% due to its balanced strength, corrosion resistance, and easy processing.

In 2025, 6000 Series held a dominant market position, capturing more than a 65% share. In December 2025, its leadership was supported by strong use across construction, automotive, transportation, electrical, and industrial applications. This alloy series offers a practical balance of strength, lightweight performance, corrosion resistance, and surface quality. It can also be easily extruded, welded, machined, and treated, making it suitable for window frames, structural systems, vehicle components, solar-panel frames, and machinery parts. Its broad availability and ability to meet different design requirements further supported demand among manufacturers.

Others, including 1000 and 5000 Series alloys, emerged as the growing segment. Their adoption increased in applications requiring high corrosion resistance, good electrical conductivity, formability, and lightweight performance. Growing demand from marine, electrical, packaging, transportation, and specialized industrial uses continued to improve their market position.

Surface Finish Analysis

Mill Finished leads with 42.0% due to affordability, flexibility, and broad industrial use.

In 2025, Mill Finished held a dominant market position, capturing more than a 42.0% share. In December 2025, the segment remained preferred across construction, transport, machinery, electrical equipment, and engineering applications. Mill-finished extrusions require no additional surface treatment, which helps manufacturers control processing time and production costs. Their metallic appearance, easy machinability, and suitability for cutting, welding, drilling, and fabrication support use in structural frames, supports, channels, and industrial components. Strong availability and compatibility with later finishing processes also strengthened their position among fabricators and project contractors.

Anodized emerged as the growing segment because the treatment improves corrosion resistance, surface hardness, appearance, and service life. Its clean finish and low maintenance needs supported wider use in architectural façades, doors, windows, consumer products, transportation parts, and interior applications during 2026, particularly where durability and visual quality were important.

End- Use Industry Analysis

Building and Construction dominates with 61.4% due to strong demand for lightweight and durable structural solutions.

In 2025, Building and Construction held a dominant market position, capturing more than a 61.4% share. In December 2025, demand remained strong across residential, commercial, and infrastructure projects. Aluminum extrusions were used in windows, doors, curtain walls, roofing systems, partitions, railings, and structural frames. Their low weight, corrosion resistance, design flexibility, and easy installation helped contractors reduce handling effort and maintenance needs. The material supported modern architecture by allowing clean finishes, complex shapes, and efficient use of space. Growing renovation activity and demand for energy-efficient buildings further strengthened the segment’s leading position.

Automotive and Transportation emerged as the growing segment in 2026. Manufacturers increasingly used aluminum extrusions in vehicle frames, battery housings, roof rails, crash-management systems, and rail components. Their lightweight strength helped improve fuel efficiency, extend electric-vehicle range, and support safer vehicle designs.

Key Market Segments

By Product Type

- Solid Profiles

- Hollow Profiles

- Semi-Hollow Profiles

By Alloy Type

- 6000 Series

- Others (1000, 5000, etc.)

By Surface Finish

- Mill Finished

- Anodized

- Powder Coated

By End-Use Industry

- Building and Construction

- Automotive and Transportation

- Electrical and Electronics

- Machinery and Equipment

- Others

Drivers

EV lightweighting demand

Electric vehicle scale-up is now a direct extrusion demand catalyst because OEMs are shifting aluminum from cosmetic and closure parts into battery enclosures, crash-management systems, roof rails, cross-members, thermal-management channels, and side-structure profiles, where extrusion offers high section complexity with lower joining count than stamped alternatives. The IEA expected global electric car sales to exceed 20 million in 2025, while BloombergNEF puts 2026 passenger EV sales at 23.3 million, up 11% year on year, with China still accounting for the largest share and Europe, India, Brazil, Mexico, and Southeast Asia adding momentum.

That volume growth changes extrusion economics because EV platforms typically prioritize range-per-kilogram and battery protection, so even a 15–25 kg increase in extruded aluminum content per vehicle across incremental EV output implies several hundred thousand tonnes of additional annual profile demand; strategically, this shifts extruders toward tighter-tolerance automotive grades, higher scrap-recovery systems, and just-in-time contract models with OEMs and Tier 1s, supporting an estimated +1.8 percentage-point uplift to baseline CAGR.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV lightweighting demand | +1.8% | China core, EU, U.S., SE Asia spill-over | Medium term (2-4 years) |

| Solar frame expansion | +1.6% | China, U.S., EU, India, MENA | Short term (≤ 2 years) |

| Green building facade demand | +1.4% | EU, GCC, China, N. America core | Medium term (2-4 years) |

| Grid & electrification hardware | +1.1% | EU, India, U.S., APAC corridors | Medium term (2-4 years) |

| Tariff-led regional sourcing | +0.9% | U.S. core, Mexico, Canada spill-over | Short term (≤ 2 years) |

| Low-carbon recycled extrusion premium | +1.0% | EU core, U.K., Japan, India | Long term (≥ 4 years) |

Restraints

Tariff-loaded import costs

U.S.-led tariff escalation is the clearest immediate restraint on aluminum extrusion market expansion because it raises landed costs fast enough to suppress order conversion, distort sourcing, and compress downstream demand. The U.S. raised its Section 232 aluminum tariff from 25% to 50% on June 4, 2025, and the April 2, 2026 proclamation further applied revised tariff treatment to aluminum articles and derivative products on the full customs value, not merely metal input value, with changes effective April 6, 2026 and no in-transit exception.

This has translated directly into higher domestic input surcharges: following the 2025 tariff increase, the Midwest premium reportedly jumped from about 38 cents/lb to 62–63 cents/lb, equivalent to roughly $1,377–1,393/ton, with risk of 70–76 cents/lb under tight supply assumptions. For extruders serving price-sensitive building systems, transport equipment, and general engineering customers, a 20–25 cents/lb premium shift can erase contribution margins on standard profiles unless surcharges are passed through immediately, and many long-term contracts lag by one to three months.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tariff-loaded import costs | -2.3% | US core, APAC export corridors, Mexico-Canada lanes | Short term (≤ 2 years) |

| Power-cost inflation | -1.9% | EU core, Middle East-linked supply, energy-sensitive Asia | Medium term (2-4 years) |

| CBAM cost burden | -1.4% | EU, Turkey, MENA-EU routes, Asian exporters to Europe | Medium term (2-4 years) |

| Weak construction orders | -1.6% | Europe, China, North America non-residential | Short term (≤ 2 years) |

| Billet and premium volatility | -1.3% | North America core, EU processors, global scrap-linked hubs | Short term (≤ 2 years) |

| Full-value derivative duties | -1.1% | US derivative imports, Asia fabricators, OEM supply chains | Short term (≤ 2 years) |

Opportunity

Modular facade kit supply

Factory-finished modular façade systems represent a future opportunity beyond standard window and curtain-wall demand. Global modular construction is projected to exceed USD 200 billion by 2027, while prefabricated homes could reach USD 153.7 billion by 2026. Extruders offering CNC cutting, thermal breaks, powder coating, brackets, and installation-ready kits could increase revenue per kilogram by 30–60%, reduce installation time by 15–25%, and add nearly 1.5 percentage points to baseline CAGR across Europe, the GCC, India, and North America.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR | Geographic Relevance | Execution Window |

|---|---|---|---|

| EV battery enclosure systems | +1.9% | China, EU, India, U.S. core | Medium term (2-4 years) |

| Modular facade kit supply | +1.5% | EU, GCC, India, N. America | Medium term (2-4 years) |

| Closed-loop low-carbon programs | +1.4% | EU core, U.S., Japan, Korea | Short term (≤ 2 years) |

| Solar repowering frame retrofits | +1.2% | EU, U.S., India, Australia | Medium term (2-4 years) |

| Digital twin yield uplift | +1.0% | China, EU, U.S., Turkey | Short term (≤ 2 years) |

| Fabricator roll-up M&A | +0.9% | U.S., Germany, Italy, CEE, Mexico | Medium term (2-4 years) |

Challenge

Energy-intensive operations and decarbonisation

Aluminum’s power intensity and the emerging decarbonisation agenda constitute a long-cycle challenge that trims roughly 1.4 percentage points from potential CAGR because it raises structural operating risk and capital complexity without directly halting production. Billet-market analysis estimates around 48% of production costs are attributable to energy, and smelting-roadmap documents highlight that decarbonising power for smelters is constrained by infrastructure, contract tenor, and renewable integration challenges specific to aluminum’s continuous-load profile.

In practice, extruders inherit this risk via metal cost and via their own gas and electricity bills for presses, heat treatment, anodising, and finishing, with compressed margins when power tariffs, carbon costs, and CBAM-like frameworks are layered onto existing price structures. Even where plants remain profitable, the combination of higher baseline energy spend, potential carbon surcharges, and the need to invest in efficiency upgrades or low-carbon certification schemes can defer growth capex by 2–4 years as management prioritises energy risk mitigation over capacity expansion.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Billet availability and pricing risk | -1.6% | Europe, North America, MENA smelter-linked hubs | Medium term (2-4 years) |

| Energy-intensive operations and decarbonisation | -1.4% | EU regulatory hubs, India, GCC smelting corridors | Long term (≥ 4 years) |

| Labour shortages and multi-shift constraints | -1.3% | North America core, EU plants, APAC logistics corridors | Medium term (2-4 years) |

| Logistics and transit volatility | -1.1% | Global, APAC–US/EU lanes, intra-regional corridors | Short term (≤ 2 years) |

| CBAM data and compliance workload | -1.0% | EU import market, Asia–EU exporters, Turkey/MENA | Medium term (2-4 years) |

| Demand forecasting and mix uncertainty | -0.9% | Global OEM chains, construction and transport clusters | Long term (≥ 4 years) |

Geopolitical Impact Analysis

Geopolitical Realignment and Supply Chain Fragmentation Reshaping Aluminum Extrusion Manufacturing.

The aluminum extrusion industry is extremely susceptible to geopolitical developments since its supply chain is dependent on global trade in bauxite, alumina, raw aluminum, and energy resources. Trade conflicts between major economies, economic sanctions, import taxes, and export restrictions can disrupt raw material flows and raise manufacturers’ procurement costs. Because aluminum manufacturing is strongly reliant on a consistent supply of raw materials and affordable energy, any geopolitical instability can result in supply shortages, transportation delays, and price variations across the value chain. These problems frequently result in higher production costs and uncertainty for extrusion manufacturers and end users.

Recent geopolitical developments have increased attempts by governments and businesses to strengthen domestic manufacturing capabilities and reduce reliance on overseas suppliers. At the same time, rising energy prices due to regional conflicts and disruptions in global energy markets have increased pressure on aluminum manufacturers, as electricity accounts for a large amount of production expenses.

- For instance, in November 2024, the World Trade Organization (WTO) reported that the number of trade-restrictive measures affecting industrial goods and critical raw materials continued to rise as countries increasingly focused on supply chain resilience, domestic manufacturing, and economic security. Such measures can affect the availability and cost of aluminum feedstock, creating challenges for extrusion manufacturers operating in global markets.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Aluminum Extrusion Market.

In 2025, Asia Pacific dominated the global aluminum extrusion market, with 74% of the overall market share. The region’s leadership is primarily driven by increasing urbanization, robust economic growth, and significant investments in infrastructure, building, transportation, and industrial manufacturing. Countries like China, India, Japan, and South Korea have created strong industrial ecosystems that enable large-scale manufacturing and consumption of aluminum extrusion products.

North America, Europe, Latin America, and the Middle East and Africa are key markets for aluminum extrusions, with rising demand from the building, transportation, industrial, and renewable energy sectors. North America gains from infrastructure renovation and electric vehicle production, whereas Europe is fueled by sustainable building, automotive manufacturing, and aluminum recycling activities. Urbanization and infrastructure development, particularly in Brazil and Mexico, are driving Latin America’s stable growth rate.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Aluminum extrusion makers are focused on improving product innovation, making their operations more efficient, and integrating their supply chains to stay ahead in the market. A major goal is creating extrusion products that are strong, light, and eco-friendly, which fits the changing needs of industries like construction, transportation, manufacturing, and renewable energy. More companies are putting money into new extrusion tech, automation, precise engineering, and extra finishing steps to boost product quality, make production faster, and offer custom solutions. They are also increasing their ability to recycle materials and producing aluminum with a lower carbon footprint to meet higher sustainability standards and environmental rules.

Companies are investing in expanding their production areas, especially in high-growth places like the Asia Pacific region, to meet the growing needs of infrastructure, auto, and industrial markets. Additionally, businesses are forming mergers, partnerships, and long-term supply deals to improve their distribution systems, ensure they have enough raw materials, and keep customers satisfied. At the same time, stricter environmental rules and trade policies related to carbon, like carbon border adjustment systems, are changing how trade works in the aluminum industry.

Market Key Players

- Alcoa Corporation

- Hindalco Industries Limited

- Kaiser Aluminum Corporation

- Norsk Hydro ASA

- China Zhongwang Holdings Limited

- Gulf Extrusions Co. LLC

- Constellium SE

- Jindal Aluminium Limited

- Arconic Corporation

- Sapa Extrusions AB

- QST, Inc.

- TALCO (Tower Aluminum Limited Company)

- Balexco (Bahrain Aluminum Extrusion Company)

- Aluar Aluminio Argentino S.A.I.C.

- Capral Aluminium

- Others

Key Development

- In April 2025, EAS Aluminium announced the launch of a 35,000 m² extrusion facility equipped with a fully automated Presezzi extrusion line for manufacturing 6000-series aluminum profiles, significantly expanding its European extrusion production capacity.

- In July 2025, Metra North America was formed through the combination of Extruded Aluminum Company, Profile Custom Extrusions, and Metra Canada, creating a larger cross-border aluminum extrusion platform serving building and industrial markets in the U.S. and Canada

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$113.8 Bn |

| Forecast Revenue (2035) | US$244.8 Bn |

| CAGR (2026-2035) | 8% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Solid Profiles, Hollow Profiles, and Semi-Hollow Profiles), By Alloy Type (6000 Series and Others (1000, 5000, etc.)), By Surface Finish (Mill Finished, Anodized, and Powder Coated), By End-Use Industry (Building and Construction, Automotive and Transportation, Electrical and Electronics, Machinery and Equipment, and Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Alcoa Corporation, Hindalco Industries Limited, Kaiser Aluminum Corporation, Norsk Hydro ASA, China Zhongwang Holdings Limited, Gulf Extrusions Co. LLC, Constellium SE, Jindal Aluminium Limited, Arconic Corporation, Sapa Extrusions AB, QST, Inc., TALCO (Tower Aluminum Limited Company), Balexco (Bahrain Aluminum Extrusion Company), Aluar Aluminio Argentino S.A.I.C., Capral Aluminium, Other players. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |