Global Alternative Financing Market Size, Share and Analysis Report By Type (Peer-to-Peer Lending, Crowdfunding, Invoice Trading, Equity-Based Crowdfunding, Reward-Based Crowdfunding, Donation-Based Crowdfunding, Real Estate Crowdfunding, Balance Sheet Lending, Others), By End User (Individuals, Businesses, Small and Medium-sized Enterprises, Large Enterprises, Startups), By Payment Instrument (Credit Transfer, Debit Transfer, Cash, Check, Cryptocurrency Wallet, E-Money), By Tenure (Short-term, Mid-term, Long-term), By Regional Analysis, Global Trends and Opportunity, Future Outlook By 2025-2035

- Published date: Feb. 2026

- Report ID: 177918

- Number of Pages: 211

- Format:

-

keyboard_arrow_up

Quick Navigation

- Alternative Financing Market Size

- Top Market Takeaways

- Report Overview

- Drivers Impact Analysis

- Restraint Impact Analysis

- By Type

- By End User

- By Tenure

- By Payment Instrument

- Regional Analysis

- Investor Type Impact Matrix

- Technology Enablement Analysis

- Top Emerging Trends

- Opportunity Analysis

- Challenge Analysis

- Customer Impact: Trends and Disruptors

- Key Market Segments

- Competitive Analysis

- Recent Developments

- Report Scope

Alternative Financing Market Size

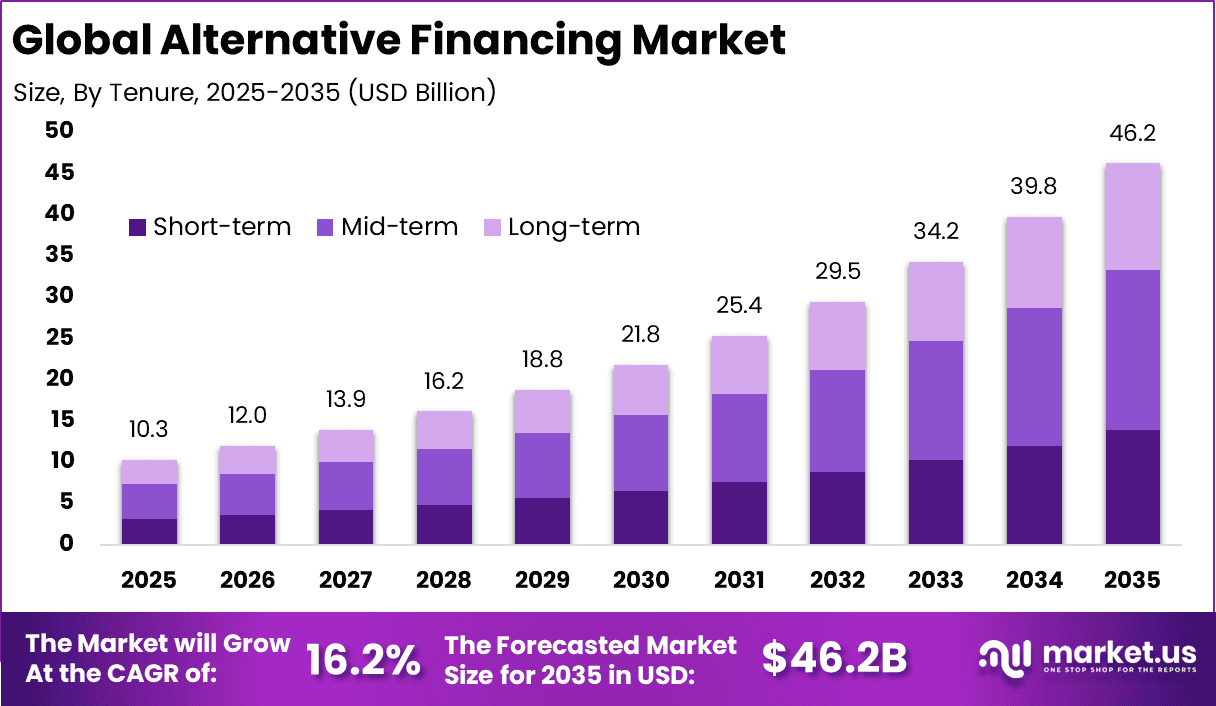

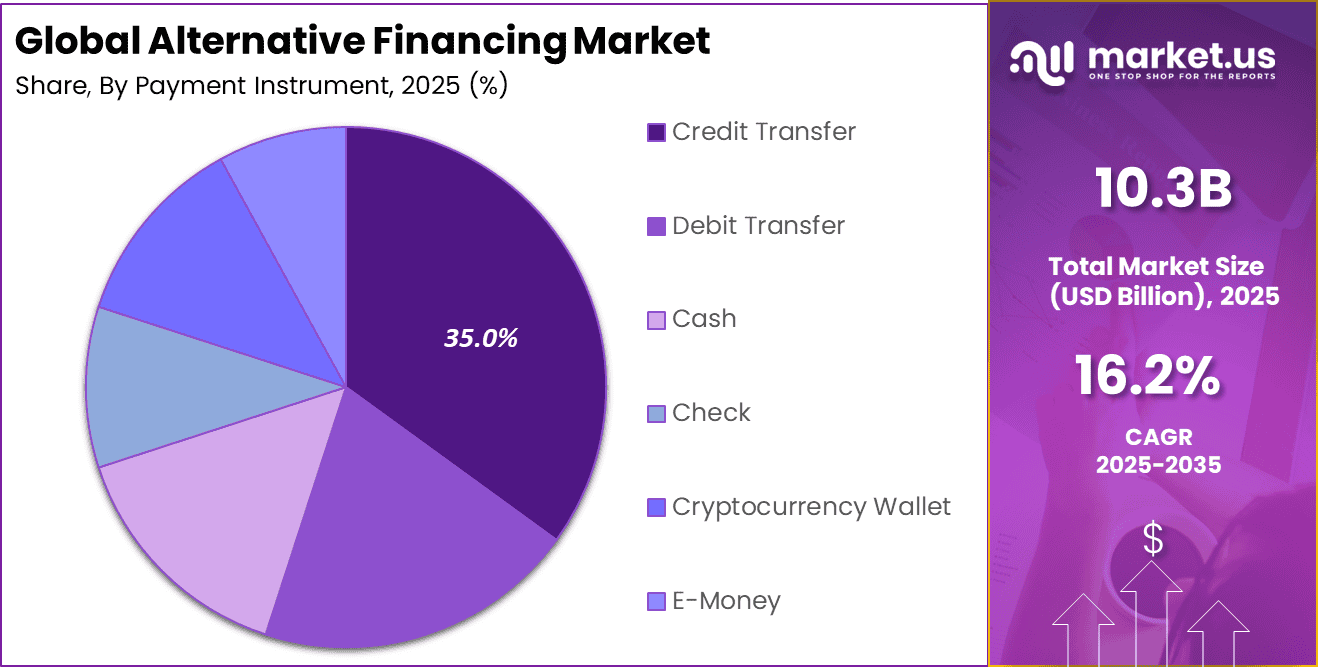

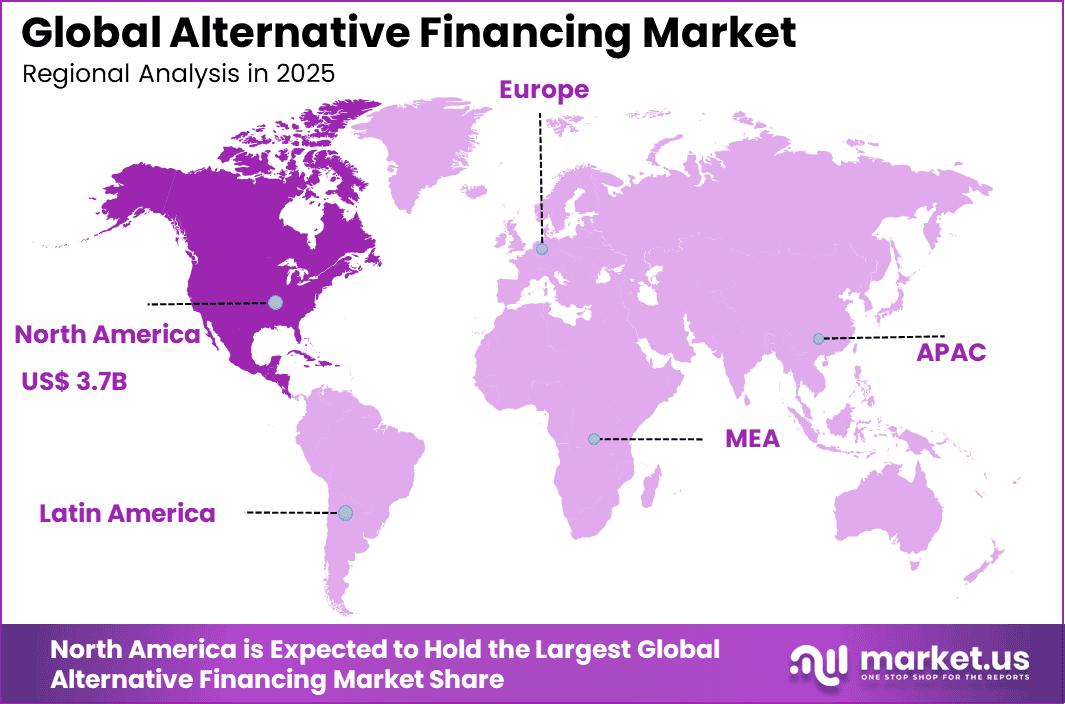

The Global Alternative Financing Market size is expected to be worth around USD 46.2 Billion By 2035, from USD 10.3 billion in 2025, growing at a CAGR of 16.2% during the forecast period from 2026 to 2035. North America held a dominant Market position, capturing more than a 36.5% share, holding USD 3.7 Billion revenue.

Top Market Takeaways

- By type, peer to peer lending led the Alternative Financing Market with a 41.5% share, supported by growing digital lending platforms and direct borrower investor models.

- By end user, businesses accounted for 71.0% of total market demand, reflecting strong reliance on non traditional funding sources for working capital and expansion.

- By tenure, mid term financing represented 42.0% of total transactions, indicating preference for structured repayment schedules beyond short term funding.

- By payment instrument, credit transfer held a 35.0% share, driven by secure and direct digital fund movement mechanisms.

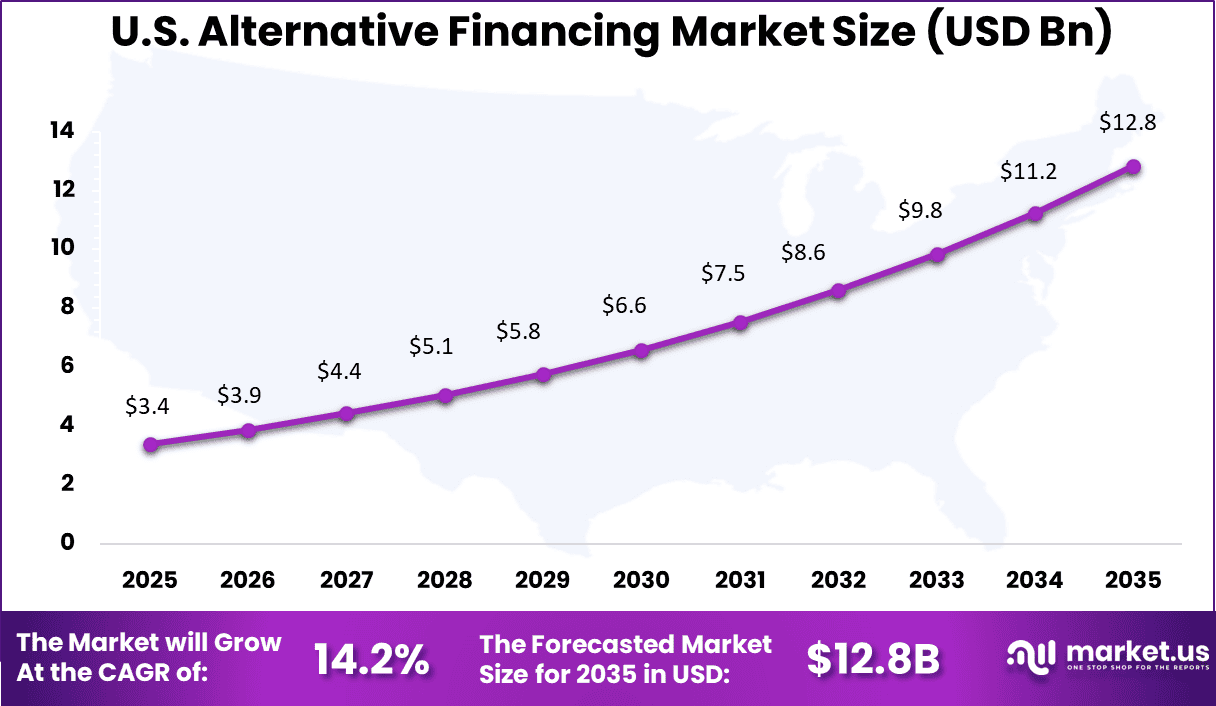

- Regionally, North America captured 36.5% of the market, with the US valued at USD 3.40 billion and recording a CAGR of 14.28%, reflecting steady growth in digital lending adoption.

Report Overview

The Alternative Financing Market represents financial funding channels that operate outside traditional bank lending systems. It includes peer to peer lending, revenue based financing, crowdfunding, invoice financing, and private credit arrangements delivered through digital platforms and specialized intermediaries. These models provide capital access to businesses and individuals who may not qualify for conventional loans.

The market has expanded alongside digital financial infrastructure and online risk assessment methods. Across small business segments, nearly 40% of applicants experience difficulty securing bank credit due to collateral and documentation requirements. Alternative financing addresses this gap by evaluating cash flow patterns and transactional history instead of relying only on balance sheet strength. This shift has transformed financing from asset based approval toward data driven underwriting.

As digital payments expand, lenders gain broader visibility into borrower performance. One major driver is the tightening of traditional lending standards following financial risk regulations. Banks increasingly prioritize low risk borrowers, which leaves emerging companies underserved. Alternative lenders fill this credit gap by applying flexible eligibility models. These structures allow funding decisions to occur within hours rather than weeks.

Drivers Impact Analysis

Key Driver Impact on CAGR Forecast (~%) Geographic Relevance Impact Timeline Rising demand for non-bank funding among SMEs and startups +4.3% North America, Europe Short to medium term Expansion of digital lending and peer-to-peer platforms +3.8% Asia Pacific, North America Medium term Increasing credit gaps in traditional banking systems +3.4% Emerging Markets Medium term Adoption of fintech-enabled underwriting and risk analytics +2.9% Global Medium term Growth in revenue-based and embedded finance models +2.6% North America, Europe Medium to long term Restraint Impact Analysis

Key Restraint Impact on CAGR Forecast (~%) Geographic Relevance Impact Timeline Regulatory uncertainty across alternative lending models -3.2% Europe, North America Short to medium term Higher default and credit risk exposure -2.8% Emerging Markets Medium term Funding constraints during macroeconomic volatility -2.5% Global Medium term Limited investor confidence in early-stage platforms -2.1% Global Medium term Dependence on capital markets and institutional funding -1.9% North America, Europe Medium to long term By Type

Peer to peer lending accounted for 41.5% of financing activity. This model directly connects borrowers with individual or institutional investors through online platforms. Automated credit scoring evaluates risk using transaction behavior and financial records instead of only traditional credit history. As a result, funding decisions are processed quickly and with broader eligibility criteria.

The model expands access to capital for borrowers underserved by traditional institutions. Investors are attracted by diversified lending portfolios and transparent performance metrics. Platforms typically provide repayment tracking and risk categorization to support informed participation. This improves trust between participants in the funding ecosystem.

Operational efficiency is achieved because intermediaries are reduced. Transaction costs decline and approval cycles shorten significantly. Digital verification also lowers administrative overhead. These advantages strengthen the adoption of marketplace lending frameworks.

By End User

Businesses represented 71.0% of borrowing demand. Small and growing enterprises often require working capital for inventory, expansion, and operational expenses. Alternative financing provides faster access compared to conventional credit evaluation processes. This helps firms respond quickly to market opportunities.

Cash flow variability also drives adoption among companies with seasonal revenue patterns. Flexible repayment structures align obligations with business cycles. Digital underwriting evaluates transaction data rather than only collateral. This enables financing even for firms lacking extensive credit history.

Operational resilience improves when businesses diversify funding sources. Access to multiple lenders reduces dependency on single institutions. The availability of quick financing supports continuity during economic fluctuations. Companies therefore increasingly integrate alternative funding into financial planning.

By Tenure

Mid term financing held 42.0% share of repayment duration. Borrowers often require funding periods long enough to support operational improvements but shorter than long term investment cycles. This tenure balances manageable repayment commitments with meaningful capital utilization. Businesses frequently use it for equipment purchases and market expansion.

Investors also prefer moderate duration exposure because risk predictability improves over intermediate periods. Platforms can evaluate repayment behavior and adjust risk grading models accordingly. This improves portfolio stability and investor confidence. Predictable maturity cycles enhance liquidity planning.

The structure supports both growth and repayment discipline. Borrowers avoid prolonged obligations while maintaining sufficient time to generate returns from financed activities. This balance contributes to strong adoption across sectors.

By Payment Instrument

Credit transfer accounted for 35.0% of transaction settlement. Digital bank transfers provide traceability and regulatory transparency. Payments are recorded automatically within platform ledgers, simplifying reconciliation. This supports secure financial operations across jurisdictions.

Electronic transfers also reduce settlement delays compared to manual processing. Lenders receive repayments promptly and can reinvest capital faster. Automated tracking improves financial reporting accuracy. The process enhances operational efficiency across lending ecosystems.

Regulatory compliance benefits from verifiable payment records. Authorities can audit transaction flows when required. Digital settlement therefore supports both operational convenience and governance requirements. This strengthens institutional participation in alternative financing platforms.

Regional Analysis

North America represented 36.5% of market participation. The region shows strong adoption due to developed digital financial infrastructure and widespread investor engagement. Borrowers demonstrate familiarity with online financial services and automated underwriting processes. Regulatory frameworks also provide operational clarity for marketplace lending models.

The United States contributed USD 3.40 Bn with an estimated growth rate of 14.28% annually. Businesses increasingly use digital financing channels to complement traditional credit access. Investors continue allocating capital to diversified lending portfolios supported by transparent performance data. Adoption expands as digital financial ecosystems mature.

Investor Type Impact Matrix

Investor Type Growth Sensitivity Risk Exposure Geographic Focus Investment Outlook Alternative lending platforms Very High Medium to High North America, Asia Pacific Scalable digital growth Institutional investors and private credit funds High Medium North America, Europe Portfolio diversification opportunity Fintech infrastructure providers High Medium Global Embedded lending enablement Private equity firms Medium Medium North America, Europe Platform consolidation Venture capital investors High High North America Innovation in digital underwriting Technology Enablement Analysis

Technology Enabler Impact on CAGR Forecast (~%) Primary Function Geographic Relevance Adoption Timeline AI-driven credit scoring and risk assessment tools +4.5% Faster underwriting Global Short to medium term API-based lending infrastructure and embedded finance tools +3.9% Seamless funding integration North America, Europe Medium term Blockchain and smart contract-based financing models +3.3% Transparent transaction processing North America, Asia Pacific Medium term Cloud-native loan management systems +2.8% Scalable platform operations Global Medium to long term Real-time payment and settlement integration +2.2% Faster disbursement Global Long term Top Emerging Trends

One emerging trend is the use of automated decision systems for credit approval. Analytical models evaluate borrower performance continuously, allowing financing limits to adjust dynamically according to business activity. This enables responsive lending structures that adapt to real operating conditions.

Another trend is the growth of revenue-linked repayment structures where repayment varies with business performance. Flexible payment arrangements reduce default probability and align lender returns with borrower success, supporting long-term participation in financing ecosystems.

Opportunity Analysis

Significant opportunity exists in using behavioral and transactional data to improve lending decisions. Digital payment records, sales patterns, and operational activity provide insight into repayment capacity beyond traditional credit scores. Improved analytics supports fairer access to capital while maintaining risk discipline.

The integration of embedded finance within business software also opens new funding pathways. Financing options delivered directly within operational platforms allow businesses to access working capital at the point of need. This seamless integration reduces friction in the borrowing process and encourages broader adoption.

Challenge Analysis

A core challenge is building trust between borrowers and capital providers in a decentralized environment. Participants must rely on digital verification and platform governance rather than established banking relationships. Transparent disclosure and standardized reporting practices are necessary to maintain confidence in funding transactions.

Another challenge is maintaining sustainable funding liquidity during economic fluctuations. Alternative funding ecosystems depend on investor participation, which may decline during uncertainty. Platforms must balance borrower demand with stable capital supply to ensure consistent service availability.

Customer Impact: Trends and Disruptors

For borrowers, the most noticeable impact is faster and simpler funding access. Applications can be completed digitally with minimal documentation, enabling quick operational decisions. This convenience improves financial inclusion for smaller businesses and independent operators.

For investors and capital providers, alternative financing introduces diversified exposure opportunities. Participation across multiple borrowers spreads risk and enables steady returns tied to economic activity. The model reshapes lending relationships by creating a more direct connection between capital supply and real business demand.

Key Market Segments

By Type

- Peer-to-Peer Lending

- Crowdfunding

- Invoice Trading

- Equity-Based Crowdfunding

- Reward-Based Crowdfunding

- Donation-Based Crowdfunding

- Real Estate Crowdfunding

- Balance Sheet Lending

- Others

By End User

- Individuals

- Businesses

- Small and Medium-sized Enterprises

- Large Enterprises

- Startups

By Payment Instrument

- Credit Transfer

- Debit Transfer

- Cash

- Check

- Cryptocurrency Wallet

- E-Money

By Tenure

- Short-term

- Mid-term

- Long-term

Regional Analysis and Coverage

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of Latin America

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Competitive Analysis

Peer-to-peer and marketplace lending platforms such as LendingClub Bank, Prosper Funding LLC, and Funding Circle Limited play a central role in the alternative financing market. Upstart Network, Inc. and OnDeck Capital, Inc. focus on data-driven underwriting and fast credit approval. These platforms benefit from streamlined digital onboarding and flexible loan structures. Demand is driven by limited access to traditional bank financing.

Crowdfunding and community-based financing providers such as Kiva and GoFundMe, Inc. expand access to capital for individuals and microenterprises. CircleUp Network Inc. and Funding Societies address early-stage businesses and regional SMEs. These players emphasize transparency and digital engagement. Adoption is strong among underserved borrowers and startup communities.

SME-focused fintech lenders such as Fundbox, BlueVine Inc., Tala, Biz2Credit Inc., and LenDenClub offer working capital and invoice financing solutions. American Express Company extends alternative credit through merchant financing programs. Other vendors increase competition and innovation across the global alternative financing landscape.

Top Key Players in the Market

- LendingClub Bank

- Funding Circle Limited

- Prosper Funding LLC

- OnDeck Capital, Inc.

- Upstart Network, Inc.

- Kiva

- GoFundMe, Inc.

- CircleUp Network Inc.

- Funding Societies

- Fundbox

- BlueVine Inc.

- Tala

- Biz2Credit Inc.

- LenDenClub

- American Express Company

- Others

Recent Developments

- In November 2025, Nomura committed USD 150 million as an anchor investment in Park Square Capital’s U.S. senior direct lending fund under a strategic private credit alliance. The partnership strengthens underwriting capacity and expands financing availability for mid market borrowers.

- In April 2025, Redsquid partnered with alternative finance provider ThinCats to support its acquisition strategy and expand its presence across the United Kingdom. The arrangement provides funding to accelerate mergers and business purchases, enabling faster growth.

Report Scope

Report Features Description Market Value (2025) USD 10.3 Bn Forecast Revenue (2035) USD 46.2 Bn CAGR(2026-2035) 16.2% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends Segments Covered By Type (Peer-to-Peer Lending, Crowdfunding, Invoice Trading, Equity-Based Crowdfunding, Reward-Based Crowdfunding, Donation-Based Crowdfunding, Real Estate Crowdfunding, Balance Sheet Lending, Others), By End User (Individuals, Businesses, Small and Medium-sized Enterprises, Large Enterprises, Startups), By Payment Instrument (Credit Transfer, Debit Transfer, Cash, Check, Cryptocurrency Wallet, E-Money), By Tenure (Short-term, Mid-term, Long-term) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape LendingClub Bank, Funding Circle Limited, Prosper Funding LLC, OnDeck Capital, Inc., Upstart Network, Inc., Kiva, GoFundMe, Inc., CircleUp Network Inc., Funding Societies, Fundbox, BlueVine Inc., Tala, Biz2Credit Inc., LenDenClub, American Express Company, Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Alternative Financing MarketPublished date: Feb. 2026add_shopping_cartBuy Now get_appDownload Sample

Alternative Financing MarketPublished date: Feb. 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- LendingClub Bank

- Funding Circle Limited

- Prosper Funding LLC

- OnDeck Capital, Inc.

- Upstart Network, Inc.

- Kiva

- GoFundMe, Inc.

- CircleUp Network Inc.

- Funding Societies

- Fundbox

- BlueVine Inc.

- Tala

- Biz2Credit Inc.

- LenDenClub

- American Express Company

- Others

Our Clients

- 177918

- Feb. 2026